An education loan for USA from an Indian PSU bank typically sanctions up to around ₹1.5 crore for a Master’s, but the unsecured ceiling without collateral stays around ₹7.5 lakh at PSU banks and ₹75 lakh or more at NBFCs for premier programs. The sanction is built on the I-20 cost of attendance, not your own estimate. A USD 60,000 program at ₹84 per dollar is roughly ₹50.4 lakh, which means most US-bound students need either tangible collateral above ₹7.5 lakh or an NBFC unsecured loan against a strong parent co-applicant. The bank also wants 10 to 15 percent margin money on the abroad tranches before it disburses.

A cousin of mine got into a Master’s in Computer Science at a state university in the US two years ago. He had the offer in February, the loan sanctioned by April, and still nearly missed the I-20 deadline because nobody told him the bank reads the I-20 itself, not the offer letter, and the cost of attendance number on that form is what sets the sanction ceiling. He scrambled to get a revised I-20 reissued with the correct funding source, and the bank reprocessed.

This post is the loan-product picture for the US, the one I wish someone had laid out for him before he signed the sanction letter. It is the funding angle, not a cost breakdown of living in America.

How an education loan for USA is actually structured

PSU banks treat the United States as their top tier, Tier-1, the same bucket as the UK, Canada and Australia. The flagship products are SBI Global Ed-Vantage, Bank of Baroda’s Baroda education loan for studies abroad, and Canara Bank’s IBA Premier scheme. Union Bank and PNB run parallel overseas products that follow the same Indian Banks’ Association framework.

For a US Master’s the structure splits into three layers, and which one you fall into decides almost everything about your interest rate, your collateral and your repayment runway.

- Up to ₹4 lakh: no margin, no collateral, no third-party guarantee. Almost no US program fits here.

- Above ₹4 lakh to ₹7.5 lakh: parent co-applicant and a third-party guarantee, usually no tangible collateral. Still far below a US ticket.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory at PSU banks, which is where every realistic US Master’s lands.

That third tier is the whole story for the US. A USD 60K program is ₹50 lakh-plus, so you are almost always in collateral territory unless you go to an NBFC. The general ceiling picture across destinations sits in the maximum education loan amount in India post.

How banks read the I-20 as the sanction basis

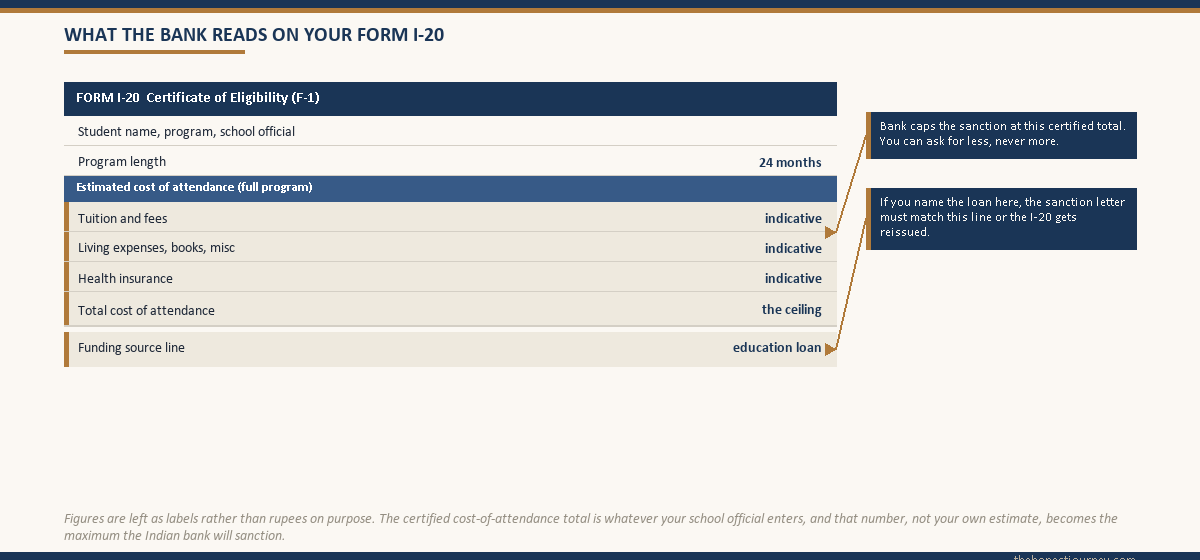

This is the single thing that makes a US loan different from a UK or Ireland loan. For most destinations the bank works off the offer letter plus a published cost-of-living estimate. For the US, the bank works off the Form I-20.

The I-20 is the Certificate of Eligibility for Nonimmigrant Student Status, issued by the university’s designated school official once you accept admission and submit your financial documents. It carries a line called the estimated cost of attendance, broken into tuition and fees plus living expenses, books, health insurance and miscellaneous, for the full program length. The official explainer on what the form is for sits on travel.state.gov under student visas.

Banks treat the I-20 cost of attendance as the maximum they will sanction, because that figure is what the university itself certifies the program costs. You cannot ask for more than the I-20 shows. You can ask for less, and many families do, funding part from savings. The I-20 also names your funding source, so if you list the education loan there, the bank wants the sanction letter to match the I-20 funding line. Get the sequence wrong and you end up reissuing the I-20, which my cousin learned the slow way.

One practical consequence: a two-year US Master’s shows the full two-year cost of attendance on the I-20, often USD 50K to 80K total. The bank sanctions against that full number, not one year. So the US ticket is structurally larger than a one-year UK or Ireland Master’s, which is exactly why the US pushes more families into the collateral tier.

The worked INR sanction example for a USD 60K program

Take a real-shaped case. Student admitted to a two-year MS in Computer Science at a US state university for Fall 2025. The I-20 shows an estimated cost of attendance of USD 60,000 for the full program (tuition and fees USD 38,000, living and other USD 22,000). At ₹84 per dollar, that is ₹50.4 lakh.

| Item | USD | INR (at 84) |

|---|---|---|

| Tuition and fees (two years) | 38,000 | 31,92,000 |

| Living, books, insurance, misc (two years) | 22,000 | 18,48,000 |

| I-20 cost of attendance | 60,000 | 50,40,000 |

This student goes to SBI for a Global Ed-Vantage loan. SBI can sanction the full ₹50.4 lakh, but because the amount is above ₹7.5 lakh, tangible collateral is mandatory. The family pledges a residential property valued at ₹80 lakh. SBI applies a haircut on the valuation, counts a security value comfortably above the loan, and sanctions.

Now the margin money. For studies abroad PSU banks ask for 10 to 15 percent margin on amounts above ₹4 lakh, contributed by the family alongside each disbursement, not upfront in one go. On a ₹50.4 lakh loan at 15 percent margin, the family puts in roughly ₹7.5 lakh of its own across the disbursement schedule, and the bank funds the balance. Some banks fold the scholarship or part-funding into the margin calculation, so confirm at the branch how your margin is computed.

| Funding layer | INR | Notes |

|---|---|---|

| I-20 cost of attendance | 50,40,000 | The sanction ceiling |

| Family margin (15 percent) | ~7,56,000 | Paid alongside disbursements |

| Bank-funded loan | ~42,84,000 | Disbursed per the fee schedule |

| Collateral pledged | Property ~80,00,000 | After valuation haircut |

If the family had no property to pledge, the same case at an NBFC (Avanse, HDFC Credila, Auxilo, InCred) would mean an unsecured sanction of around ₹50 lakh against the parent’s income, typically needing a clean CIBIL above 750 and demonstrable repayment capacity, at an interest rate of 11.5 to 13.5 percent versus SBI’s floating rate near 9.65 percent. Over a long repayment that spread is several lakh of extra interest. The honest economics of the unsecured route are in the education loan for abroad studies without collateral post.

Faz's ruleGet the I-20 cost of attendance right before you apply for the loan, not after. The number on that form is your sanction ceiling, and a mismatch between the I-20 funding line and your sanction letter means a reissued I-20 and lost weeks.

Ask the university’s designated school official for the cost-of-attendance breakdown the moment you accept. If you intend to fund partly from savings, tell them so the I-20 reflects the right loan figure. Banks read the certified I-20 number, not your own estimate, and the visa officer reads it too.

Margin money and how disbursement is timed for the US

For abroad studies, margin money is the family’s own contribution, set at 10 to 15 percent of the loan above ₹4 lakh. It is not a deposit you hand over on day one. The bank releases each tranche net of your margin share, so you contribute proportionally as tuition installments fall due. For a two-year US program, tuition is usually billed per semester or per year, so the disbursement happens in three or four tranches across the program, each one with the margin attached.

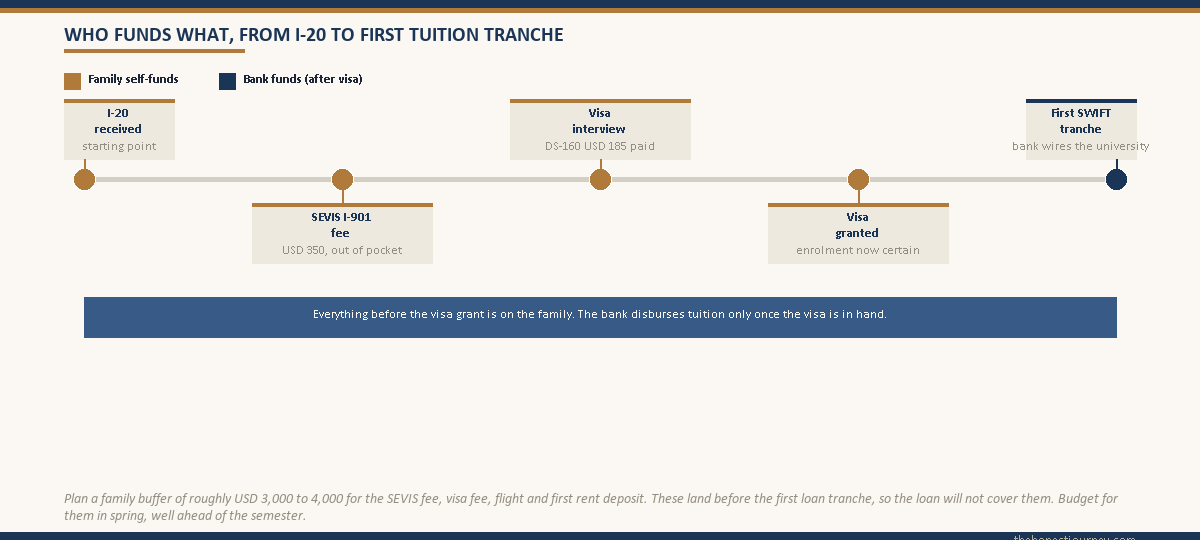

The US adds a timing wrinkle that other destinations do not have: the SEVIS fee and the visa fee both have to be paid before disbursement matters. The SEVIS I-901 fee (USD 350 for an F-1 student in 2025) and the DS-160 visa application fee (USD 185) are paid out of pocket by the student, typically not waited for as a bank tranche, because they are due before the visa interview and well before the first tuition installment.

So the practical sequence is: receive the I-20, pay the SEVIS fee yourself, book and attend the visa interview, get the visa, and only then does the first tuition tranche from the bank go out by SWIFT wire to the university before the semester start. The bank does not disburse tuition until the visa is granted, because a refused visa means no enrolment. This is why families fund the SEVIS and visa fees from their own pocket. The mechanics of how the disbursement actually moves are covered in the education loan disbursement process post.

Faz's ruleBudget the SEVIS fee, visa fee and first flight as out-of-pocket, not loan-funded. The bank releases tuition only after the visa is granted, so the pre-visa costs are on you and the family buffer.

The SEVIS I-901 fee and DS-160 visa fee together are over USD 500 due before your interview. Add the flight and the first month’s rent deposit in the US, and you need a clean USD 3,000 to 4,000 of family buffer that the loan will not cover before the first tranche lands. Plan for it in March, not August.

PSU versus NBFC for the US, and where the wall is

The wall every US-bound student hits is the ₹7.5 lakh unsecured ceiling at PSU banks. A USD 60K program is ₹50 lakh, far above it, so the choice is stark: pledge tangible collateral and take the cheaper PSU rate, or go unsecured at an NBFC and pay more.

| Route | Typical ceiling for US | Collateral | Rate band (2025) |

|---|---|---|---|

| PSU secured (SBI, BoB, Canara) | To around ₹1.5 crore | Property, FD or LIC mandatory above ₹7.5 lakh | ~9.5 to 11 percent floating |

| PSU unsecured | To ₹7.5 lakh | None tangible, co-applicant required | ~10 to 11.5 percent |

| NBFC unsecured | ₹75 lakh or more for premier programs | None tangible, strong co-applicant income | ~11.5 to 13.5 percent |

NBFCs lean on the program’s ranking and earning potential. For a premier US program (a top-ranked STEM Master’s at a well-known university), an NBFC will sanction unsecured to ₹75 lakh or beyond against a strong parent co-applicant, because their model bets on the graduate’s US earning power. For a lower-ranked program the unsecured appetite shrinks fast. PSU banks do not make that distinction; they want collateral above ₹7.5 lakh regardless of how the program ranks.

The RBI sets the regulatory framework these lenders operate under, and the IBA model scheme is the template PSU banks follow. The current rules are on the RBI site and the model educational loan scheme is published by the Indian Banks’ Association. Neither caps the US sanction amount; the ceiling comes from each bank’s product policy and your collateral.

The STEM OPT repayment runway, honestly

The reason families stomach a ₹50 lakh loan for the US is the post-study earning runway, and for STEM programs that runway is genuinely longer than anywhere else. An F-1 graduate gets 12 months of Optional Practical Training (OPT) after graduation. If the degree is a designated STEM field, the graduate can apply for a 24-month STEM OPT extension, for a total of 36 months of work authorisation before needing an H-1B or other status.

That three-year window is the repayment engine. A graduate earning a US tech salary during 36 months of OPT can service, and often substantially prepay, a ₹50 lakh loan in a way that a one-year work window elsewhere cannot match. This is the honest case for the US ticket being worth the larger loan.

But the runway has a real risk attached, and it is the H-1B lottery. STEM OPT buys 36 months; staying beyond that needs an H-1B, which is selected by lottery, not merit. Plenty of capable graduates do not get picked in three tries and have to leave. So the honest framing is this: model your repayment on the 36 months of OPT income you can reasonably count on, not on a 6-figure-dollar career you assume will continue indefinitely. If the loan only repays comfortably on the assumption of long-term US employment past OPT, the math is too tight.

Faz's ruleModel loan repayment on 36 months of STEM OPT income, not on an H-1B you have not won yet. The OPT window is near-certain for a STEM grad; staying beyond it is a lottery.

A ₹50 lakh loan is serviceable, even prepayable, on a STEM OPT salary across 36 months if you live frugally and prepay aggressively in years one and two. Treat the H-1B as upside, not as the base case. If your repayment plan needs the H-1B to work, shrink the loan or pick a cheaper program.

What banks check on US-specific paperwork at sanction

Beyond the standard income and KYC documents, a US sanction file leans on a few US-specific items.

- The university admission letter, on letterhead, confirming the program and start term.

- The Form I-20 showing the certified cost of attendance for the full program length. This is the document the sanction amount is built on.

- The fee structure or cost breakdown, which the bank cross-checks against the I-20 figure.

- For collateralised loans, the property title documents and a valuation from the bank’s empanelled valuer.

- Co-applicant income proof, since even secured US loans rely on the parent’s repayment capacity to support a loan this size.

The point banks scrutinise most is the alignment between the I-20 cost of attendance, the sanctioned amount and the funding source named on the I-20. A clean file has all three agreeing. A messy file, where the I-20 lists a different funding source or a cost that does not match the sanction, gets sent back, and you lose weeks reissuing the I-20.

The honest take on a US education loan

The US works as a loan-funded destination when two things hold. One, the program is STEM or otherwise gives you the OPT runway, because the larger US loan only repays comfortably on the longer earning window. Two, the family can either pledge collateral for the inevitable above-INR-7.5-lakh amount or accept the higher NBFC rate with eyes open.

What does not work is treating the US as a default because everyone applies there. A two-year US Master’s at a mid-ranked program, fully loan-funded at NBFC rates without collateral, with a non-STEM degree that gives only 12 months of OPT, is the combination that goes wrong. The loan is large, the rate is high, and the earning runway is short. That is the case where the math breaks.

The US ticket is the biggest loan most Indian families will take for education. It is worth it when the program quality, the STEM runway and the collateral position all line up. When they do not, a one-year UK or Ireland Master’s funds at a fraction of the ticket. Redo the math against the I-20 number before you sign the sanction letter, not after.

FAQ

Can I get an education loan for USA from Indian banks?

Yes. All major PSU banks (SBI, Bank of Baroda, Canara, Union, PNB) cover the United States under their Tier-1 overseas education loan products, and NBFCs like Avanse, HDFC Credila, Auxilo and InCred fund it unsecured. PSU banks sanction up to around ₹1.5 crore with collateral, and up to ₹7.5 lakh without tangible security. The sanction is built on the Form I-20 cost of attendance, so the bank reads that certified figure rather than your own estimate.

What is the maximum loan for USA from Indian banks?

PSU banks like SBI Global Ed-Vantage sanction up to around ₹1.5 crore for the US, provided collateral and co-applicant income support the amount. The unsecured ceiling at PSU banks stays at ₹7.5 lakh; anything above needs tangible security such as property, FD or LIC. NBFCs sanction unsecured loans up to ₹75 lakh or more for premier US programs against a strong parent co-applicant, at interest rates higher than PSU floating rates and without the central interest subsidy benefit.

Do banks sanction the loan on the I-20?

Yes. For the US, the Form I-20 is the sanction basis. Its estimated cost of attendance line, covering tuition, fees, living and insurance for the full program length, sets the maximum the bank will sanction. You cannot borrow more than the I-20 certifies, and the funding source named on the I-20 should match your sanction letter. A mismatch means the university reissues the I-20, which costs weeks, so get the I-20 figure settled before you apply for the loan.

How much margin money is needed for a US loan?

For studies abroad, PSU banks ask for 10 to 15 percent margin money on the loan amount above ₹4 lakh. Margin is the family’s own contribution, paid alongside each disbursement rather than upfront, so on a ₹50 lakh loan at 15 percent you contribute roughly ₹7.5 lakh across the tranches. Some banks fold any scholarship or part-funding into the margin calculation, so confirm at the branch exactly how your margin is computed before you sign.

Is collateral needed for a US Master’s loan?

At PSU banks, yes, for almost every US Master’s. The unsecured ceiling is ₹7.5 lakh, and a US program runs far above that, so any amount above ₹7.5 lakh needs tangible collateral such as property, fixed deposit or LIC. NBFCs sanction unsecured up to ₹75 lakh or more for premier programs against parent income and a clean CIBIL, but at higher interest rates. The trade-off between PSU collateral at a lower rate and NBFC unsecured at a higher rate is worth modelling carefully.

What is the STEM OPT repayment runway?

An F-1 graduate gets 12 months of Optional Practical Training after graduation. If the degree is a designated STEM field, the graduate can apply for a 24-month extension, giving 36 months of total work authorisation before needing an H-1B. That three-year window is the repayment engine for a US loan, since US tech salaries can service or prepay a large loan within it. Model repayment on the OPT window you can count on, not on an H-1B that is selected by lottery.

How does disbursement timing work with the visa for a US loan?

The bank disburses tuition only after the F-1 visa is granted, because a refused visa means no enrolment. The student pays the SEVIS I-901 fee and the DS-160 visa fee out of pocket before the interview, since these fall due before any tuition tranche. After the visa is approved, the first tuition tranche goes out by SWIFT wire to the university before the semester begins. So families fund the SEVIS fee, visa fee and first flight from their own buffer, not the loan.

Is a US Master’s loan worth it compared to a one-year program?

It depends on the program and the runway. A two-year US Master’s is the largest education loan most Indian families take, so it makes sense mainly for STEM programs where the 36-month OPT window gives a long earning runway to repay. A non-STEM US program fully funded at NBFC rates, with only 12 months of OPT, is where the math breaks. A one-year UK or Ireland Master’s funds at a fraction of the US ticket, so compare the total cost against the realistic earning window before committing.

Faz · The Honest Journey · 2026