Education loan disbursement in India happens in tranches, one per semester or per year, with the bank paying the university directly rather than depositing money in your account. Each tranche needs a fresh fee invoice and the previous semester’s mark sheet, the SWIFT transfer for overseas universities clears in 5 to 10 working days, and the bank can refuse a later tranche if you fail a semester or change course without informing them. The first tranche is the slowest because the bank is setting up the disbursement channel for the first time.

When my cousin got his sanction letter for a Manchester master’s, he assumed the money would land in his savings account within a week and he could wire it across himself. That is not how the education loan disbursement process works for any approved bank in India, and learning that the wrong way costs people their semester registration date.

This post walks through what actually happens between sanction and the money reaching the university, in the order it happens, for both domestic and overseas loans.

Waiting on disbursal? Half the delay is upstream, at the application stage. See how to track your portal status and chase the branch early.

What disbursement means and why it does not happen all at once

A sanction letter is not money. It is the bank’s commitment to lend up to a stated amount on stated terms, subject to you producing documents at each stage. The actual cash movement, called disbursement, happens in tranches tied to your academic calendar.

The reason banks structure it this way is risk management. If they hand over ₹30 lakh upfront and you drop out in semester two, recovering the unused balance is messy. By splitting disbursement into semester-wise or annual tranches, the bank limits its exposure at any given point and keeps the right to pause if you stop being a student in good standing. The Indian Banks Association model education loan scheme, which most PSU banks follow, formalises this tranche structure.

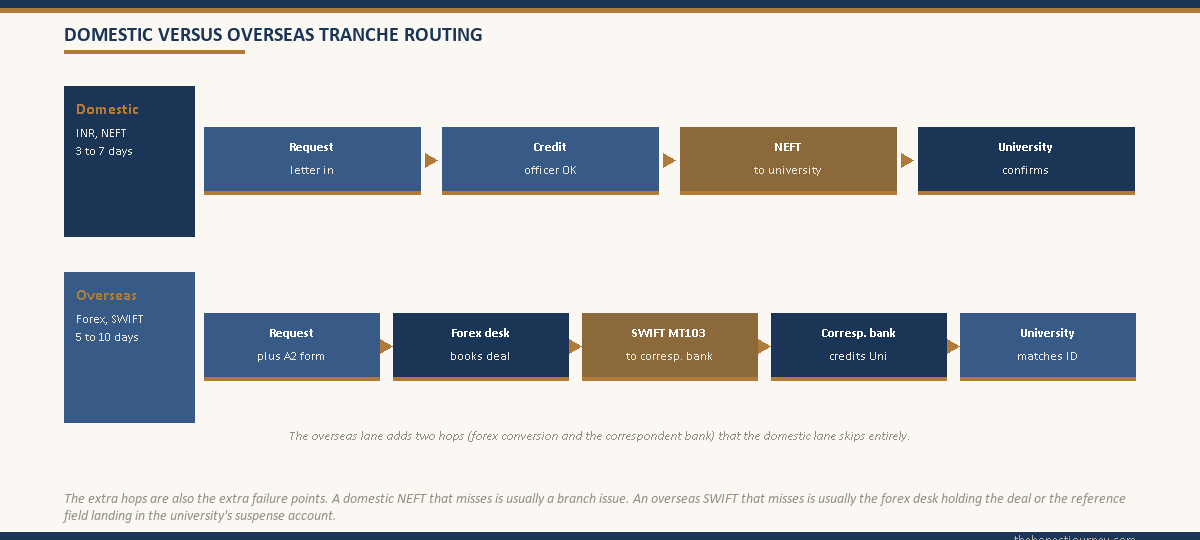

For domestic courses, tranches are usually semester-wise (two per year for most programs, three for trimester schools). For overseas courses, banks default to annual tranches because the SWIFT cost and forex paperwork make per-semester remittance uneconomical for both sides. The total number of tranches equals the program length: a 4-year B.Tech is 8 semester tranches, a 2-year overseas master’s is 2 annual tranches.

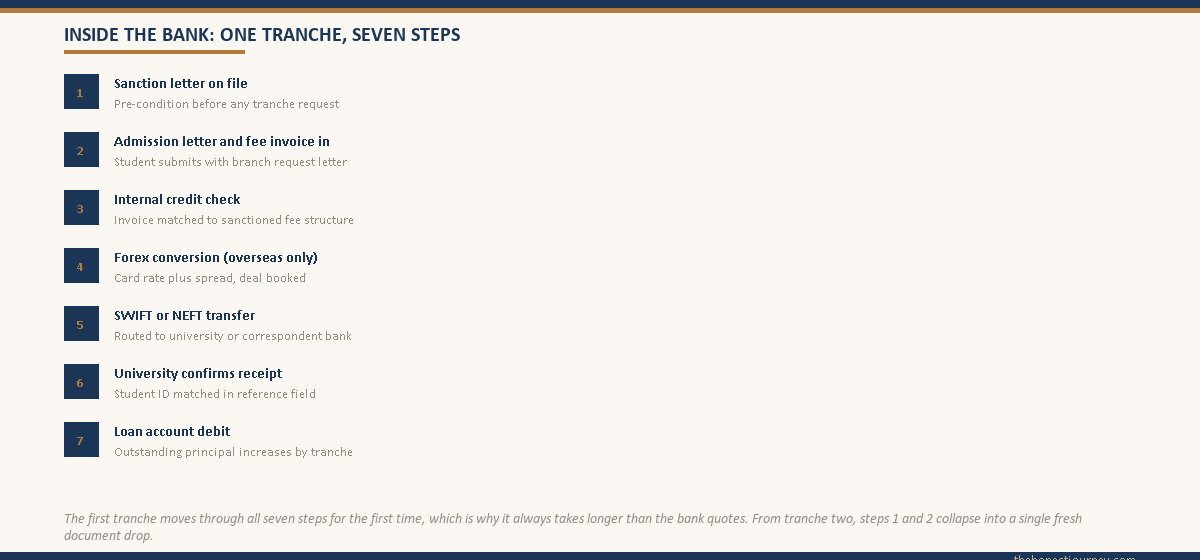

Step 1: What happens between sanction letter signing and the first tranche

Once you sign the sanction letter and the loan agreement, the bank opens a loan account in your name. This account is separate from your savings account and you cannot withdraw from it directly. Disbursements are debited from this account straight to the beneficiary the bank approves, which for tuition is almost always the university itself.

Before the first tranche moves, the bank needs three things from you in addition to what was already in the application file:

- The final, unconditional admission letter (not the conditional offer used during sanction).

- The first semester or first year fee invoice or demand letter from the university, with the exact amount, due date and the university’s bank account details.

- A request letter from you, addressed to the branch manager, asking for the first tranche to be disbursed to the named beneficiary.

For overseas loans, the bank also collects a Form A2 declaration under the RBI’s Liberalised Remittance Scheme framework, even though education loan remittances are TCS-exempt. The A2 documents the purpose of the foreign currency outflow, and our guide to the A2 form, LRS, and forex for students walks through exactly how to fill it.

Step 2: What the bank does internally before the money leaves

This is the part that takes longer than students expect. Once the branch has your documents, it does not just transfer the money. The file moves through three checks:

The branch credit officer verifies the invoice matches the sanctioned fee structure. If the invoice is for ₹1.8 lakh but the sanction modelled ₹1.5 lakh per semester, the gap needs explanation and sometimes an internal approval.

The processing team confirms the beneficiary bank account is genuine. For overseas universities, this means matching the SWIFT code and IBAN to the university’s published treasury details. Most banks maintain an internal whitelist for universities they have remitted to before.

For overseas tranches, the forex desk converts INR to the foreign currency at the day’s card rate and routes the SWIFT through a correspondent bank in the destination country. This is where the timing slips. SBI and Bank of Baroda tend to clear in 3 to 5 working days. Smaller branches and unfamiliar private branches have stretched to 10 working days for first overseas tranches.

Faz's ruleSubmit the first tranche request the day you receive the admission letter and fee invoice, not the day before the fee deadline.

The first tranche always takes longer than the bank quotes because the file is being set up for the first time. Two weeks of lead time is comfortable. Less than that is when people start chasing branch managers on WhatsApp and missing their registration confirmation slot at the university.

Step 3: Direct university payment versus your account, and why direct is the rule

Indian banks following the IBA model scheme are required to disburse tuition directly to the educational institution. This is non-negotiable for the tuition portion. The bank will not transfer tuition to your savings account so you can pay the university yourself, because that would defeat the audit trail and open the loan to misuse.

The components that can sometimes be disbursed to your account, against bills or invoices, are the smaller heads in the sanction: hostel fees if the hostel is not university-run, books and equipment, laptop, exam fees and living expenses for overseas students where the university does not collect them. Even these typically need either a quotation upfront or a reimbursement claim with receipts.

For overseas study, the rule is the same but the mechanics are stricter. The bank wires tuition in foreign currency directly to the university’s bank account via SWIFT. Living expenses for the first year go either to your designated overseas account (if you have already opened one) or to a specific instrument like the German blocked account provider. The full breakdown of that flow is in the education loan for Germany blocked account post.

Step 4: How tranche 2 onwards works and what each tranche needs

From the second tranche onwards, the bank does not just take your word that you are still enrolled. Each subsequent disbursement requires fresh proof.

The standard documents per tranche:

| Tranche | Documents needed | Typical timeline |

|---|---|---|

| Tranche 1 (first semester or first year) | Final admission letter, fee invoice, request letter, A2 form for overseas | 7 to 14 working days from request |

| Tranche 2 onwards (domestic) | Previous semester mark sheet or pass certificate, current semester fee invoice, request letter | 3 to 7 working days |

| Tranche 2 onwards (overseas) | Previous year transcript or progress report, current year fee invoice, request letter, fresh A2 | 5 to 10 working days |

| Final tranche | Same as previous, plus expected completion letter from university | 5 to 10 working days |

The previous-semester mark sheet is the gate. If you have a backlog or have failed the semester, the bank is within its rights to pause disbursement until you produce the cleared result. Most PSU banks will release one supplementary tranche with a written explanation from your faculty or registrar, but a pattern of repeated failures gives the bank grounds to stop disbursing entirely.

Faz's ruleGet the mark sheet or progress report from the university the week the result is published, not the week the next tranche is due.

Universities issue official transcripts on their own timeline, often two to four weeks after the unofficial result. If your tranche is due before the official sheet is ready, an interim letter from the registrar with the result and seal is usually accepted, but only if you ask for it. Nobody at the university will know your tranche calendar.

Step 5: How overseas tranche disbursement actually moves through SWIFT

For an overseas tranche, the sequence inside the bank looks like this:

You submit the request letter, fee invoice and prior-semester transcript to the branch. The branch raises a debit voucher against your loan account. The forex desk picks up the file the next working day, calculates the EUR or USD or GBP equivalent at the card rate, applies the bank’s spread, and books a forex deal. The deal is then sent to the correspondent bank as a SWIFT MT103 payment instruction with the university’s bank as the beneficiary.

The correspondent bank in the destination country credits the university’s account, usually within one to two working days of receiving the SWIFT. The university’s finance office then matches the payment to your student ID using the reference field in the SWIFT message, which is why the request letter must always include your university student ID number. Without it, the payment can sit unmatched in the university’s suspense account for weeks.

For sites where the university uses a centralised payment portal like Flywire or Convera, the SWIFT goes to the portal’s collection account rather than the university directly. The bank treats this the same way as long as the portal is listed in the sanction letter as a permitted beneficiary.

Step 6: When the bank can pause or refuse a tranche

The sanction letter is conditional. The bank reserves the right to stop disbursing if any of the following happens.

You fail a semester or have an unresolved backlog. PSU banks will usually allow one chance with a faculty letter; repeated failures or a year-long gap without medical or family reason gives the bank grounds to stop. NBFCs are stricter on this.

You change your course or university without prior approval. The sanction was issued against a specific program. Switching from a master’s to a diploma, or from one university to another, invalidates the disbursement structure and requires a fresh approval, sometimes a fresh sanction.

The co-applicant’s income drops materially or the co-applicant defaults on another loan with the same bank. This is rare but documented. The bank reviews the co-applicant’s profile at sanction and is not required to re-check at each tranche, but if a default surfaces in their system, the next tranche review will flag it.

You miss interest payment during the moratorium when the bank required simple interest servicing. Most education loans capitalise moratorium interest, but some products require monthly interest service during the study period. Default on this can pause the next tranche. The mechanics of how moratorium interest accumulates and capitalises are in the education loan India complete guide.

If a tranche is paused or refused, the bank has to communicate the reason in writing. You then have the right to respond, and most pauses get resolved with a single follow-up letter and supporting document. Outright refusal of a sanctioned tranche is uncommon when the student is still enrolled and progressing.

Step 7: What to do if a tranche is delayed and the university deadline is close

Universities, especially overseas ones, take their fee deadlines seriously. Late payment usually means a late fee (typically 1 to 5 percent of the unpaid amount), and missing the deadline by more than a couple of weeks can mean deregistration for that semester.

If the bank’s tranche is going to slip past the university deadline, the standard playbook is:

- Email the university bursar or international office immediately, attach your sanction letter and a written confirmation from the bank that disbursement is in process, and request a deadline extension. Most universities grant 2 to 4 weeks when the proof is a sanctioned education loan.

- Ask the bank for a deferred undertaking letter you can send to the university, stating the bank’s commitment to remit by a specific date.

- If neither buys enough time, pay the tuition from family savings against a written undertaking from the bank that the equivalent amount will be reimbursed to you (not the university) when the tranche releases. Some banks allow this; many do not. Confirm in writing before paying.

The path that always fails is silence. The university will not negotiate after the deregistration date passes, and the bank will not move faster without external pressure.

Step 8: How disbursement is reflected in your loan account and what you owe at each stage

The loan account starts at zero. Each tranche disbursement adds to the outstanding principal. Interest at the sanctioned rate accrues on the disbursed amount only, not on the unutilised sanction. So if your total sanction is ₹30 lakh and only ₹7.5 lakh has been disbursed in the first semester, interest accrues on ₹7.5 lakh until the next tranche.

For most education loans, this accrued interest is simple interest during the moratorium and gets capitalised (added to principal) at the end of the moratorium. So the EMI calculation at repayment start is based on the principal plus all the capitalised moratorium interest, which is materially higher than the original sanction amount.

For loans that require interest servicing during the moratorium (an option some banks offer at slightly lower rates), you pay the accrued monthly interest from your own funds, and the principal at repayment start equals the disbursed amount only. This saves significant total interest over the loan life.

The PM Vidyalakshmi portal is an application channel only. Once the bank sanctions and disburses, the actual tranche mechanics and accounting are handled at the chosen bank’s branch, not on the portal. The portal does not track or display disbursement status in real time.

The honest closing take

Disbursement is the part of the education loan process that nobody fully explains at sanction. The sanction letter feels like the finish line. It is not. It is the starting gun for a multi-year sequence where every semester you need to produce documents, request the next tranche on time, and stay in good academic standing or risk a pause.

The students who navigate this cleanly are the ones who treat each tranche as a small project: get the fee invoice the day registration opens, get the prior-semester mark sheet the week results are out, submit the request to the branch with two weeks of lead time, and confirm the SWIFT reference once it leaves the forex desk.

The ones who struggle are the ones who assumed the bank would push tranches automatically, or that the sanction letter alone would satisfy the university, or that the bank could not say no once the loan was sanctioned. The bank can say no, the university will not wait, and the loan account only debits when you ask it to.

FAQ

How does education loan disbursement work in India?

The bank disburses the sanctioned amount in tranches, usually one per semester for domestic courses and one per year for overseas courses, paying the university directly rather than depositing in your account. Each tranche requires the current fee invoice, the previous semester’s mark sheet (from tranche two onwards) and a written request from you. Interest accrues on the disbursed amount only, and the bank can pause disbursement if you fail a semester or change course without approval. The total number of tranches equals the program length in semesters or years.

How many days does education loan disbursement take?

The first tranche typically takes 7 to 14 working days from the date you submit the admission letter, fee invoice and request to the branch, because the bank is setting up the disbursement channel and beneficiary verification for the first time. Subsequent domestic tranches take 3 to 7 working days. Overseas tranches via SWIFT take 5 to 10 working days end to end. SBI and Bank of Baroda tend to be on the faster end; smaller branches stretch the first overseas tranche to 10 days or more.

Does the bank pay the university directly?

Yes. For the tuition portion of the loan, banks following the IBA model scheme are required to disburse directly to the educational institution, not to your savings account. This is non-negotiable. The smaller components of the sanction (hostel fees with non-university providers, books, laptop, exam fees, living expenses for overseas students) can sometimes be paid into your account against quotations or reimbursement claims with receipts. The tuition direct-payment rule applies whether the university is in India or abroad.

What is tranche disbursement?

Tranche disbursement means the sanctioned loan amount is released in scheduled instalments tied to your academic calendar, rather than as a single lump sum at the start. For a 4-year B.Tech with semester-wise disbursement, you would receive 8 tranches, one per semester, each covering that semester’s tuition and approved expenses. The structure protects the bank from over-exposure if you drop out mid-program and gives them the right to pause disbursement if you fail a semester or change course.

What documents are needed per tranche?

The first tranche needs the final admission letter, the first semester or first year fee invoice with university bank details, a request letter from you, and Form A2 for overseas remittance. From the second tranche onwards, you need the previous semester’s mark sheet or transcript, the current semester or year fee invoice, and a fresh request letter. Overseas tranches from year two also require a fresh A2 form. The previous-semester mark sheet is the gate; without it the bank will not release the next tranche.

Can the bank refuse the second tranche?

Yes, under specific conditions. The bank can refuse or pause a later tranche if you have failed a semester, have an unresolved backlog, have changed course or university without prior approval, have defaulted on required interest payments during the moratorium, or if the co-applicant has defaulted on another loan with the same bank. Outright refusal is uncommon when the student is still enrolled and progressing. Most pauses get resolved with a written explanation and supporting document from the university.

How does overseas tranche disbursement move through SWIFT?

The branch raises a debit voucher against your loan account, the forex desk converts INR to the foreign currency at the day’s card rate and books the forex deal, and a SWIFT MT103 instruction goes to a correspondent bank in the destination country with the university as beneficiary. The correspondent credits the university within one to two working days. The university matches the payment to your student ID using the reference field in the SWIFT message, which is why your request letter must always include the student ID. Without it, the payment can sit unmatched for weeks.

What if the tranche is delayed past my university fee deadline?

Email the university bursar or international office immediately with your sanction letter and a written disbursement-in-process confirmation from the bank, and request a deadline extension. Most universities grant 2 to 4 weeks when the proof is a sanctioned education loan. Ask the bank for a deferred undertaking letter you can forward to the university. If neither buys enough time, pay from family savings against a written bank undertaking that the equivalent will be reimbursed to you when the tranche releases. The path that always fails is staying silent.

Faz · The Honest Journey · 2026