TCS on foreign education remittance is 5% on amounts above ₹10 lakh per financial year for self-funded transfers, and 0% for remittances funded by a sanctioned education loan from a notified Indian institution. I have seen banks default to charging the 5% rate even on loan-funded transfers because the counter staff miss the Section 206C(1G) exemption. Carry the sanction letter, flag the loan source upfront, and verify the receipt on the same day.

A reader’s father wired ₹12L to a Canadian university for tuition last September, through his regular bank under LRS. The transfer cleared. But the bank also collected an extra ₹10,000 as TCS. He didn’t notice it on the day because it was buried in the bank charges line of the remittance receipt. Three months later when he was filing returns, his CA flagged it. The TCS was claimable as a credit, but it took some back-and-forth to recover. More importantly, the family didn’t need to pay it at all. The same ₹12L sent through the sanctioned education loan would have been TCS-exempt. The form he filled at the bank didn’t ask the right questions, and the bank’s default flow charged TCS as if it was a self-funded education remittance, not a loan-funded one.

The TCS rules around foreign education remittances aren’t complicated, but the bank counters don’t always apply them correctly, and most families discover the implications only at tax-filing time. This post is the clear walk-through: when 5% TCS applies, when the loan exemption kicks in, how to ensure your bank doesn’t deduct it incorrectly, and how to claim it back when they do.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The 60-second answer

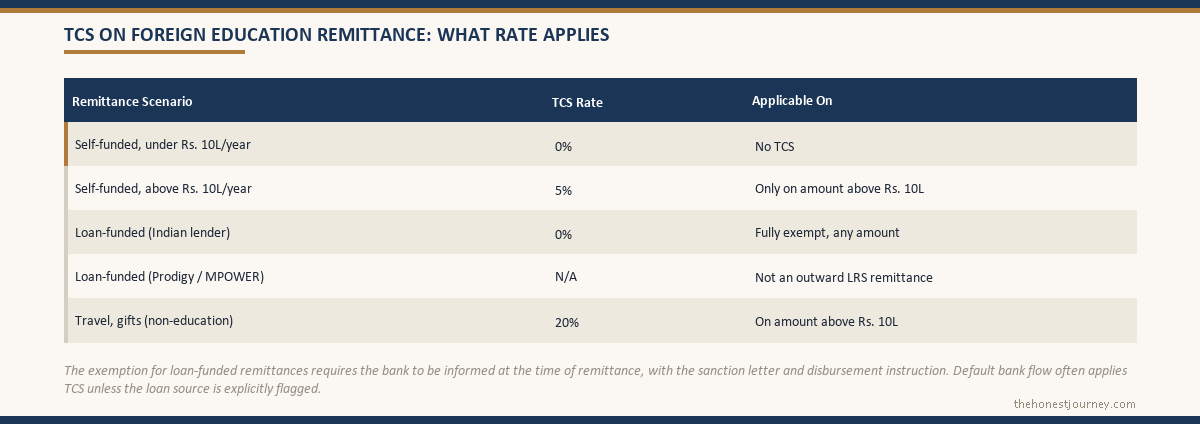

TCS (Tax Collected at Source) under Section 206C(1G) applies to foreign remittances under LRS. For education-purpose remittances, TCS is 5% on the amount exceeding ₹10 lakh in a financial year (the threshold was raised from ₹7L to ₹10L in Budget 2025). For education remittances funded by a sanctioned education loan from a notified institution, the TCS rate is 0% (fully exempt) with no threshold. TCS is not an additional tax; it is a tax credit that can be claimed against your income tax liability when filing returns, or refunded if you have no liability. The exemption for loan-funded remittances requires the bank to be told at the time of remittance, with the sanction letter and disbursement instruction as proof.

What TCS is and isn’t

TCS is collected at source by the remitting bank, not by the income tax department. The bank deducts the TCS from the amount being remitted (or charges it on top, depending on the bank’s process), and deposits it to the income tax department on your behalf. The amount appears on your Form 26AS and AIS at year-end. You then claim it as a credit against your tax liability when filing your ITR.

Three things people misunderstand about TCS:

- It is not a separate tax. You don’t pay TCS in addition to income tax. The TCS amount is fully claimable as a credit. If your total tax liability for the year is less than the TCS collected, the difference is refunded.

- It is not a penalty. TCS is a mechanism to track high-value foreign transactions and ensure income tax compliance. It’s not punishing the remittance; it’s monitoring it.

- The exemption is real, not theoretical. A sanctioned education loan from a notified financial institution genuinely makes the remittance TCS-free. The reason most families miss this is procedural: the bank needs to be informed at the remittance stage, and many bank staff are not familiar with the exemption clause.

The threshold structure (Budget 2025 update)

Before Budget 2025, the threshold for foreign education remittances was ₹7 lakh per financial year. Budget 2025 raised it to ₹10 lakh, effective FY2025-26 onwards. The current structure:

The ₹10 lakh threshold is per individual per financial year, not per transaction. If a parent sends ₹4L in May, ₹5L in August, and ₹2L in November (total ₹11L), the TCS at the third transaction would be 5% on the ₹1L excess above the threshold = ₹5,000.

For comparison, non-education foreign remittances under the Liberalised Remittance Scheme (travel, gifts to relatives abroad, investments) attract 20% TCS above ₹10 lakh. Education is the most favourable category, and loan-funded education is the most favourable sub-category.

How the loan exemption works in practice

When a remittance is funded by a sanctioned education loan, Section 206C(1G) provides a 0% TCS rate. The exemption applies if:

Faz's ruleLoan-funded education remittances are TCS-exempt, if you tell the bank.

The 0% rate under Section 206C(1G) only applies when the remittance is documented as funded by a sanctioned education loan. Default bank counter flow applies 5%. Carry the sanction letter; get written confirmation before the transfer.

- The remittance is for education purposes (tuition fees, living expenses, course-related costs)

- The funding source is a loan from a notified financial institution under Section 80E

- The student is enrolled in a recognised foreign institution

The “notified financial institution” definition is the same one used for Section 80E tax deduction. It includes:

- All scheduled commercial banks (PSU and private)

- NBFCs notified for this purpose: HDFC Credila, Avanse, Auxilo, InCred, Axis Finance, and several others

- Charitable institutions approved under Section 10(23C)

Note that USD loans from Prodigy Finance or MPOWER Financing are not from notified Indian institutions and don’t qualify for the TCS exemption. Their remittances flow differently anyway (the lender disburses directly to the university), so the question of TCS on outward remittance from India doesn’t usually arise. But it’s worth knowing that the exemption is specific to Indian-lender loans.

The mechanics:

- The bank disbursing the education loan (could be the same bank as the LRS remittance, or different)

- The borrower or co-applicant initiates the LRS remittance, specifying it is funded by the loan

- The bank requires proof: the loan sanction letter and the disbursement instruction matching this remittance

- The bank applies 0% TCS to that remittance

If you have a ₹40L sanctioned loan and your bank disburses ₹15L to the university for the first semester, that remittance is TCS-exempt. Even if it exceeds the ₹10L threshold. Even if other family remittances (gifts, travel) have already used up the threshold. The loan-funded portion is separately exempt.

The bank-counter problem

The single most common issue: the bank doesn’t apply the exemption automatically. The default flow at most retail banks treats all education-purpose LRS remittances the same: apply 5% TCS if cumulative remittances exceed ₹10L for the year.

Why this happens:

- The bank counter staff may not know about the loan exemption

- The bank’s internal LRS workflow may not have a “loan-funded” checkbox

- Even if it does, the form A2 (the mandatory LRS declaration) doesn’t explicitly distinguish loan vs self-funded

- The bank’s CBS (Core Banking System) might auto-calculate TCS on the remitter’s total annual remittances

The practical fix:

- At the time of remittance, explicitly state and document that the funding source is a sanctioned education loan. Reference the loan account number.

- Carry the sanction letter and the disbursement letter to the branch (or upload them in the LRS remittance request portal).

- Ask the branch officer to confirm that the TCS will not be charged. Get this in writing if possible (email confirmation, or a note on the remittance receipt).

- Check the remittance receipt immediately. TCS, if charged, will appear as a separate line item. If it’s there and shouldn’t be, raise it with the branch the same day. Refunds are easier same-day than retroactively.

When TCS is correctly applied to your remittance

If the remittance is self-funded (not from a loan), and the cumulative remittance for the year crosses ₹10L, TCS is correctly applied. The 5% rate applies only on the excess.

Faz's ruleTCS isn't a tax paid, it's a tax credit. But it sits with the government for 6-9 months before refund.

If you have no tax liability, the entire TCS amount is refunded after ITR filing. The cost is cashflow timing, not absolute rupees. For families with thin liabilities, that’s still ₹1L+ tied up for most of a year.

Example: a parent who has no education loan and is funding the student’s foreign education from savings, sends ₹15L in tuition for the financial year. TCS on the excess of ₹5L = ₹25,000. Bank deducts this and deposits to the government. It appears on the parent’s Form 26AS at year-end.

The parent then claims this ₹25,000 as a credit against their income tax liability when filing returns. If their tax liability is ₹3L for the year, the actual tax paid in cash is ₹3L to ₹25,000 already collected through TCS = ₹2.75L. If their liability is ₹15,000 (lower than the TCS), they get a refund of ₹10,000.

So TCS doesn’t make the remittance more expensive in absolute terms. It does mean a cashflow gap: the ₹25,000 was paid out in September and can only be recovered against tax liability around June the following year when returns are filed. For a family with tight cash flow, that 9-month gap matters.

Form 26AS and AIS: how to verify

After the financial year ends, the TCS collected appears in two places:

- Form 26AS (the consolidated tax statement), under Part II “TCS, Tax Collected at Source.” Each TCS entry shows the deductor (the bank), the date, the amount, and the TAN.

- AIS (Annual Information Statement), under “TCS” category. AIS provides slightly more context including the remittance purpose code.

When filing returns:

- The TCS amounts pre-populate in the ITR form’s “TCS” schedule

- These amounts are credited against your total tax liability

- If the credits exceed liability, the refund is processed automatically

It’s worth pulling Form 26AS and AIS before filing to confirm all TCS entries match your records. If a TCS was deducted but doesn’t appear in 26AS within 3-4 months of the remittance, the bank hasn’t deposited it correctly. Raise this with the bank’s TCS desk.

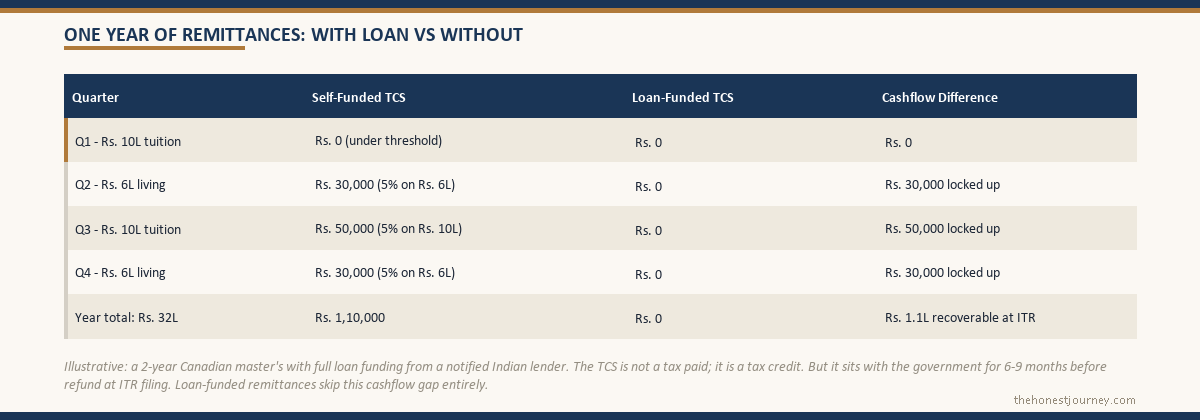

A year’s remittance walk-through

For an Indian family funding a 2-year Canadian master’s: tuition CAD 32K/year (~₹20L), living costs CAD 20K/year (~₹12.5L). Total per year: ~₹32.5L. Loan sanctioned: ₹50L.

Year 1 disbursements:

- August: bank disburses CAD 16K (₹10L) to university for Semester 1. Funded by loan. TCS = 0.

- September: bank disburses CAD 10K (₹6.3L) to student’s Canadian account for living costs. Funded by loan. TCS = 0.

- January: bank disburses CAD 16K (₹10L) to university for Semester 2. Funded by loan. TCS = 0.

- February: bank disburses CAD 10K (₹6.3L) to student’s account. Funded by loan. TCS = 0.

Cumulative remittance for Year 1: ₹32.6L. TCS collected: ₹0. Because every remittance was loan-funded.

If the same family had not taken a loan:

The same ₹32.6L over the year would attract TCS on the amount above ₹10L = 5% × ₹22.6L = ₹1.13L. This would be deducted at source and recovered at ITR filing. The cashflow impact: ₹1.13L tied up for 6-9 months.

The loan-funded route saves no actual rupees if the TCS would have been refunded anyway (assuming the family’s tax liability covers it). But it saves the cashflow gap. And for families with thin tax liabilities (parents close to retirement, parents on the new tax regime with minimal deductions), it can mean the TCS is effectively a forced advance payment that earns no interest and creates a refund-claim process.

The minor-child case

For students under 18 (rare in master’s-abroad cases, more common for parents sending children to UK boarding schools or US prep schools), the LRS limit applies to the minor as an individual, not clubbed with the parent’s limit. The TCS rules apply the same way. The parent signs the LRS declaration on behalf of the minor, and the TCS appears on the minor’s PAN.

For most education-abroad scenarios, the student is 18+ and a separate taxpayer. The TCS rules apply to whoever’s PAN is on the LRS form: typically the parent paying, or the student if they’re remitting their own funds.

The non-tuition remittance case

LRS remittances under “education” cover more than tuition:

- Tuition fees paid directly to the university: clearly education

- Living-expense remittances to the student’s foreign account: education (if the student is enrolled in a recognised course)

- Health insurance for the student: education (related)

- Travel costs for educational purposes: education (case-by-case)

- Books, equipment, course materials: education (related)

What doesn’t count as education for the lower-TCS treatment:

- Parents visiting the student: travel, not education. 20% TCS above ₹10L threshold.

- Gifts to the student: gift category, 20% TCS above ₹10L threshold.

- Investments made by the student or parent abroad: investments, 20% TCS above threshold.

When sending money for the student’s stay, make sure the LRS form correctly codes the remittance as “Higher Education” or “Studies abroad” purpose. Wrong purpose coding can trigger the wrong TCS rate.

The Section 80E + TCS interaction

The Section 80E tax deduction on education loan interest is separate from TCS. They interact at ITR filing stage:

- TCS is claimed as a credit (refund or set-off)

- 80E reduces taxable income (deduction)

Both can be claimed on the same loan in the same year. The 80E deduction reduces the tax payable; the TCS credit reduces the cash tax actually paid out. If a parent has paid ₹2L interest on the education loan and ₹50,000 was deducted as TCS on a self-funded portion of remittances, both come into the same return.

We covered the Section 80E mechanics in detail in our 80E post. The TCS treatment is in addition to, not instead of, 80E.

What to do if your bank deducted TCS incorrectly on a loan-funded remittance

This is the most common scenario where families get caught. The fix:

- Get the remittance receipt showing TCS was deducted.

- Email the bank’s branch manager (and CC their TCS desk if available) within 7 days. State: this remittance was funded by sanctioned education loan account number XYZ, copy of sanction letter attached, copy of disbursement letter attached, request reversal of TCS amount as it was incorrectly deducted under Section 206C(1G).

- The bank’s TCS desk has 30-60 days to process a reversal. If the TCS has already been deposited to the government, the bank will issue a credit to your account and adjust their TCS deposit in the next filing.

- If the bank refuses or doesn’t respond: the TCS amount will still appear on your Form 26AS. You can claim it as a credit at ITR filing time, but you’ve effectively given the government a 9-month interest-free loan.

To avoid this entirely: get written confirmation at the time of remittance that TCS will not apply. A WhatsApp confirmation from the relationship manager works in practice; an email is better.

Frequently asked questions

Is TCS applicable on education loan remittance to a foreign university?

No, if the remittance is funded by a sanctioned education loan from a notified Indian financial institution. The Section 206C(1G) exemption applies. If the remittance is self-funded (not from a loan), TCS at 5% applies on the amount exceeding ₹10L per financial year.

What is the TCS rate on foreign education remittance in 2026?

For self-funded education remittances, 5% on the amount above ₹10L per individual per financial year. For loan-funded education remittances from notified Indian institutions, 0%.

Can I claim TCS back if I have no tax liability?

Yes. If your total income tax liability is less than the TCS collected, the difference is refunded. You file your ITR, the TCS appears in the credits section, and the refund is processed.

Does TCS apply to remittances under ₹10 lakh?

No. The ₹10L threshold is per individual per financial year. Cumulative remittances under ₹10L attract 0% TCS regardless of funding source.

Why did my bank deduct TCS on my education loan disbursement?

Most likely the bank didn’t apply the Section 206C(1G) exemption because either (a) the bank counter staff weren’t told the remittance was loan-funded, (b) the bank’s CBS auto-calculated TCS without considering the loan source, or (c) the loan account was at a different bank from the remitting bank. In all cases the fix is to provide the sanction letter, disbursement letter, and request a reversal.

Does TCS apply if I’m paying my own foreign tuition from my Indian salary, not via loan?

Yes, at 5% on the amount above ₹10L per year. If you’re sending ₹12L for tuition from your own salary, TCS = 5% × ₹2L = ₹10,000. This is collected by the bank and recoverable as a credit at ITR time.

Does TCS apply to Prodigy Finance or MPOWER USD loan disbursements?

The TCS exemption under Section 206C(1G) applies to loans from notified Indian financial institutions. Prodigy and MPOWER aren’t on this list. In practice, USD lenders disburse directly to the university in foreign currency from an offshore account, so the question of TCS on an outward Indian remittance doesn’t apply. You’re not remitting under LRS at all.

When can I claim my TCS credit?

At ITR filing time after the financial year ends. TCS collected April-March of FY2025-26 is claimed in the ITR filed by July 2026 (or extended deadlines). The refund, if any, typically processes within 30-60 days of filing.

If you’re planning your education remittances, the remittance walk-through above and the Section 80E tax benefit post cover the tax side. For the loan-side mechanics that interact with TCS (when disbursement happens, what document the bank needs), the education loan disbursement post walks through the four stages, and the moratorium interest post explains what happens to interest while the student is still studying. And for the cost picture that determines how much you’ll be remitting in total, the Canada cost breakdown (or the destination post relevant to your case) lays out the annual numbers.