An education loan in India typically takes 3 to 10 weeks from application to first disbursement. From what I see, NBFCs like HDFC Credila and Avanse are fastest at 5 to 12 working days. Private banks such as Axis and ICICI run 3 to 6 weeks, while PSU banks like SBI take 4 to 10. Incomplete documents add 1 to 3 weeks, and collateral title issues add 2 to 6.

A reader emailed last June. She had a sanctioned admit to a Canadian master’s starting in September, a ₹26L loan application submitted to a PSU bank in April, and a Form I-20 / Letter of Acceptance she still hadn’t been able to show at the visa appointment because the loan sanction letter hadn’t arrived. By the time the bank approved in mid-July, she had two weeks to get the visa, the GIC funded, the forex booked, and the flight changed. The visa came through, but the family paid about ₹35,000 extra in last-minute flight rebooking and a rushed forex transaction that could have been avoided with a clearer timeline four months earlier.

The “how long does an education loan take” question matters most because of this kind of downstream pressure. Course start dates, visa appointment slots, GIC funding windows, tuition deadlines, flight prices: they all key off the loan timeline. This post is what the actual week-by-week looks like, where each stage breaks, and how to keep the schedule realistic when you plan.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The 60-second answer

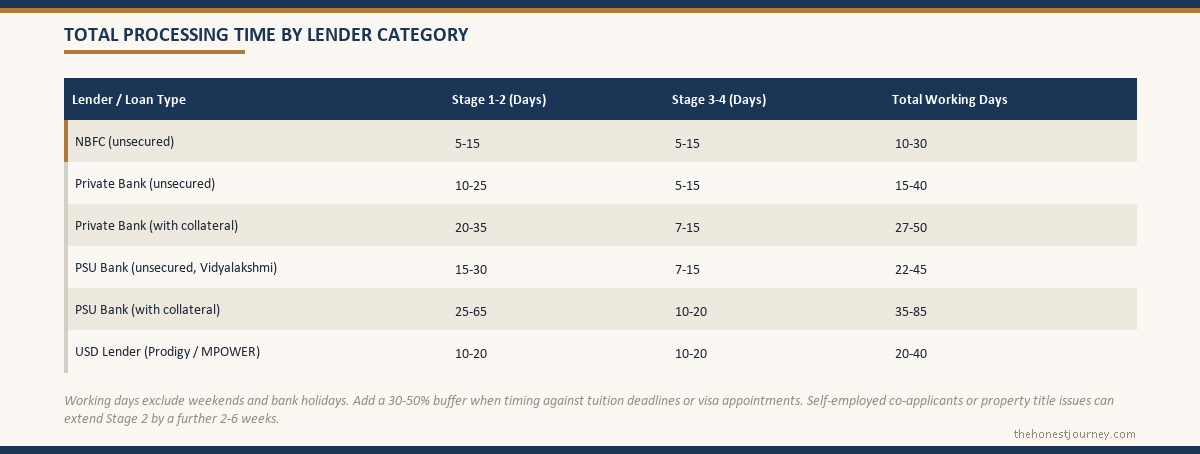

A typical education loan in India takes 3 to 10 weeks from application to first disbursement, depending on lender type and complexity. NBFCs (HDFC Credila, Avanse, Auxilo, InCred) are the fastest, with sanction letters in 5-12 working days and disbursement in another 1-2 weeks. Private banks (Axis, ICICI, Kotak) typically take 3-6 weeks end-to-end. PSU banks (SBI, Bank of Baroda, Union Bank, Canara) take 4-10 weeks, sometimes longer when collateral verification is involved. The biggest delays are: incomplete documents (adds 1-3 weeks), collateral title issues (adds 2-6 weeks), and back-and-forth on the institution’s “approved list” if you’re applying for a less common university.

The four stages of an education loan

Every education loan goes through four stages, in this order:

- Application + initial documents (Day 0 to Day 5-10)

- Underwriting + sanction letter (Day 5 to Day 25-45)

- Disbursement letter + agreement signing (after sanction, takes 3-10 days)

- First disbursement to college (1-10 working days after disbursement request)

Each stage has its own internal sub-steps and its own ways of slipping. The total elapsed time is the sum of these stages plus any back-and-forth in between, which is where the variability comes from.

Stage 1: Application and initial documents

Day 0 is when you submit the application. For NBFCs, this is usually a single online submission with documents uploaded. For private banks, it’s an online form plus a branch visit. For PSU banks, it’s typically a branch visit with physical documents (some PSU banks now have online application portals, but the documents still go in physically).

Time to complete Stage 1:

- NBFC: 1-3 days (online, fast back-and-forth)

- Private bank: 3-7 days (branch coordination involved)

- PSU bank: 5-14 days (file movement is slower in PSU systems)

What slows it down: missing documents. The documents required for an education loan post lists everything banks ask for. Practical observation: families typically submit Stage 1 with 80% of the documents, then take 1-2 weeks to gather the missing 20%. Plan for this. Have everything ready before you submit.

Stage 2: Underwriting and sanction

This is the longest stage and the one with the most variance. The bank pulls the co-applicant’s CIBIL (see the CIBIL score post for thresholds), verifies income proofs, runs the field investigation (a person from the bank visits or calls to verify the home address), and underwrites the case.

For collateral-backed loans, this stage also includes:

- Property valuation by a bank-empanelled valuer (5-10 working days)

- Legal verification of property title (5-15 working days, longer if there are encumbrances)

- Search at the sub-registrar’s office (3-7 working days)

Time to complete Stage 2:

- NBFC (unsecured): 3-10 working days

- Private bank (unsecured): 7-21 working days

- Private bank (with collateral): 14-30 working days

- PSU bank (unsecured, under ₹7.5L PM Vidyalakshmi): 10-25 working days

- PSU bank (with collateral): 21-60 working days

Sanction letter is the formal output of this stage. It lists the loan amount, rate, tenure, moratorium, processing fee, and disbursement conditions. This is the document you can show at the visa appointment and to the university.

What slows Stage 2 most often:

- Co-applicant CIBIL on the borderline. The case goes to a higher credit committee for review. Adds 5-15 days.

- Income proof issues. Self-employed parents whose ITR doesn’t match bank statements. Adds 7-21 days while the bank requests CA-attested computations.

- Property title encumbrances (for collateral loans). A pending bank dues entry on the property from a parent’s old home loan that was paid off but not officially closed. Adds 2-6 weeks of legal back-and-forth.

- The course or institution not being on the bank’s approved list. Less common for top global universities, more common for second-tier institutions. Adds 1-3 weeks of internal credit-committee approval.

Stage 3: Disbursement letter and loan agreement

After sanction, you need to sign the loan agreement and obtain a disbursement letter (or “disbursement request” in some lenders) before any money moves. This involves:

- Signing the master loan agreement at the branch (or via e-signature for NBFCs)

- Submitting the original university fee invoice or payment schedule

- Submitting a disbursement request form specifying the amount and beneficiary

- For first disbursement: submitting GIC payment proof (note that foreign remittances also attract TCS under the income tax department rules) (Canada) or blocked-account proof (Germany) or any other visa-stage funds requirement

Time to complete Stage 3: typically 3 to 10 working days.

What slows Stage 3:

- The university’s fee invoice not matching the sanctioned loan amount exactly (small variances are fine; large ones trigger queries)

- Trying to disburse to a foreign account directly when the loan was sanctioned for INR-INR transfer to the institution’s Indian agent

- Missing visa documents at the disbursement stage

Stage 4: First disbursement to the college

Once the disbursement request is approved, the bank wires the money. For domestic colleges this happens within 1-3 working days. For foreign universities, the bank initiates an outward remittance, governed by the RBI Liberalised Remittance Scheme, which takes:

- SWIFT transfer (most lenders): 2-7 working days to credit the university account

- Through a forex partner (some NBFCs): 1-3 working days

- Through the institution’s India remittance partner (Convera, Flywire, Western Union for Universities): 2-5 working days

Plan for the longer end of this range when timing it to a tuition deadline. The university’s accounts department needs to receive the money, match it to the student account, and update enrollment status. The end-to-end visibility takes 5-10 working days from when the bank wires the funds.

The realistic week-by-week schedule

Faz's ruleApply 8-12 weeks before your tuition deadline. Compressing further removes the safety margin.

Every stage has natural slippage points. A 4-6 week timeline only works for clean NBFC applications with strong co-applicants and zero document hiccups. For PSU banks, anything tighter than 10 weeks pushes you into panic territory.

Here is the week-by-week schedule that works for most families. Reverse-engineer from your tuition deadline.

Week -12 (3 months before tuition deadline): Pull CIBIL for the co-applicant. Make sure it is in the right range for the lender category you plan to approach. Start any 30-day credit cleanup if borderline.

Week -10: Finalise the lender shortlist. Pre-qualify with 1-2 NBFCs (soft pull, no impact on score). Have a clear primary application target.

Week -8 to -9: Submit the formal application. Document submission complete by end of week.

Week -5 to -7: Underwriting and field investigation. Respond to any queries within 24 hours. Aim for sanction letter by end of week -5.

Week -4: Sanction letter received. Use it for the visa appointment if needed.

Week -3: Submit disbursement request with university invoice. Sign loan agreement.

Week -2: First disbursement initiated.

Week -1: Funds credited to university. Confirm with the university’s accounts office that the payment matched and your enrollment is updated.

This schedule has roughly 2 weeks of buffer built in. If you compress further, you lose the safety margin and any minor hiccup (a missing document, a CIBIL query, a visa appointment delay) can push the tuition payment past the deadline.

When you can compress the timeline

You can compress the schedule to 4-6 weeks total if all of these are true:

Faz's rulePSU banks have the lowest rates but the slowest processing. NBFCs reverse both.

The rate differential of 1.5-2.5% on a ₹40L loan is roughly ₹4-6L of total interest over 10 years. Worth waiting the extra 3-4 weeks for a PSU sanction unless visa deadlines genuinely don’t allow it.

- You apply to an NBFC, not a PSU bank

- Loan is unsecured (no collateral verification needed)

- Co-applicant CIBIL is 750+ with a clean file

- Co-applicant income is salaried with simple ITRs (not self-employed)

- The institution is on the lender’s pre-approved premier list

- All documents are submitted complete on Day 0

This is the case for a typical engineering graduate with a salaried parent applying for a Canadian or UK master’s at a ranked university. The 4-6 week timeline is achievable but assumes nothing goes wrong.

For anything outside this profile, plan for 8-12 weeks.

When the timeline blows out

The cases that consistently take 12-20 weeks:

Collateral loans with title issues. Property with a closed but not officially discharged old home loan, ancestral property without clear succession, or property where the original sale deed is not traceable. Each of these takes 4-8 weeks to clear legally.

Self-employed parent without proper ITR documentation. Bank statements showing high turnover but ITR showing low income. Family business income that doesn’t tie out to declared returns. The bank will ask for 3 years of audited financials, CA certifications, GST returns. Adds 3-6 weeks of back-and-forth.

Less common institutions. A loan application for a master’s at a Tier-2 European university not on the lender’s pre-approved list goes to a credit committee for review. The committee meets weekly or fortnightly. Adds 2-4 weeks.

USD loan from Prodigy or MPOWER. While Indian CIBIL isn’t pulled, these lenders run their own underwriting using future-earnings models, employment-based projections, and institution-specific data. Sanction takes 2-4 weeks, then disbursement to the university adds another 2-3 weeks. Total: 4-7 weeks.

Bank takeover / balance transfer. If you’re moving an existing education loan from one lender to another for a better rate, allow 6-10 weeks for the takeover process. The new lender needs the old lender’s NOC and full loan statement; the old lender often takes 2-3 weeks to issue these.

Common scheduling mistakes

Underestimating Stage 1 by assuming documents are ready. Almost no family has every document ready on Day 0. Plan 1-2 weeks of buffer at Stage 1.

Applying after the visa appointment is booked. The visa appointment often requires the loan sanction letter as proof of funds. If you book the visa appointment for early August and apply for the loan in late June, you may not have a sanction letter in time.

Not coordinating disbursement with the university’s payment deadline. Universities have specific deadlines for tuition payment that determine whether your enrollment is confirmed. Time the disbursement so funds arrive 7-10 days before this deadline.

Treating the moratorium start date as the same as disbursement start date. Moratorium typically starts from the date of first disbursement, but some lenders treat it from sanction date. Check your sanction letter. We covered the moratorium mechanics in the moratorium post.

Applying to PSU bank for first-time premier-institution loans without checking course list. PSU banks have pre-approved institution lists for premier-rate loans (SBI Global Ed-Vantage, for instance). If your university isn’t on this list, you fall back to the general loan product with higher rates and slower processing.

Practical pre-application checklist

Two weeks before you submit:

- Pull co-applicant CIBIL. Confirm it meets the threshold for your target lender category.

- Gather complete documents: photo ID, address proof, last 3 years’ ITRs, last 6 months’ bank statements, salary slips (if salaried), Form 16, university admit letter, fee structure, course curriculum.

- For collateral loans: original sale deed, latest property tax receipt, NOC from society/builder, encumbrance certificate.

- Decide on the loan amount based on tuition + living costs + buffer. The cost breakdown for Canada post (or the corresponding destination post) covers what to include.

- Have a clear repayment plan in mind. The bank will ask: how do you plan to repay? Be specific.

One week before:

- Soft-pull pre-qualify with the target lender. Avoid hard enquiries until the formal application.

- Confirm your university’s exact disbursement requirements (which forms they need, what payment portal they use).

- Open a savings account at the target bank if it’s a PSU bank loan and you don’t already have one (some PSU banks require an existing relationship for loan eligibility).

Day of submission:

- Submit with all documents complete. Resist the urge to submit early with missing papers.

- Note the application reference number.

- Identify the relationship manager or loan officer assigned to your case.

- Get a clear estimated timeline from the lender at submission. Hold them to it.

When to switch lenders mid-process

Sometimes the right move is to abandon a stuck application and restart with a different lender. The decision points:

At Week 3 with no underwriting update from a PSU bank: consider parallel application to an NBFC. The NBFC sanction will likely arrive before the PSU bank’s, giving you optionality.

Sanction letter offered at a rate 1.5%+ higher than expected: counter-offer with another lender’s pre-qualification. Lenders sometimes revise rates downward to match competition, especially for strong profiles. We discussed rate negotiation in the interest rate comparison post.

Application stuck at a credit committee for 3+ weeks: restart elsewhere. The original application is unlikely to clear within a meaningful timeframe.

Frequently asked questions

How long does an education loan take to get approved in India?

For an unsecured loan from an NBFC with a clean co-applicant profile, typically 5-15 working days from application to sanction letter. For a PSU bank with collateral, typically 4-10 weeks. Disbursement adds another 1-3 weeks after sanction.

Can I get an education loan in 1 week?

For a pre-qualified NBFC application with all documents complete and a 750+ CIBIL co-applicant for a top-tier institution: yes, sometimes. Sanction in 5-7 working days is achievable. Disbursement to the university takes another 5-10 days. Real one-week end-to-end (application to college receiving the money) is rare and assumes nothing goes wrong.

Why is my PSU bank taking longer than 4 weeks for sanction?

Common causes: collateral title verification in progress, co-applicant income documentation review (especially for self-employed), the institution not being on the pre-approved list, or the file moving through multiple internal approval levels. Ask the bank directly which stage your file is at.

Can I expedite the loan if I have a tuition deadline?

Some lenders have “rush” or “premium” processing tracks for an additional fee. NBFCs typically don’t need a rush track because they’re already fast. PSU banks generally don’t offer expedited processing. The honest answer: applying 8-12 weeks before your deadline is more reliable than trying to expedite a late application.

What happens if disbursement is delayed past the university’s tuition deadline?

Most universities offer a grace period of 1-3 weeks after the deadline. Contact the university’s international student office directly, explain the situation, and ask for an extension. They have processes for this; international student deferrals due to bank-side delays are common. Get the extension in writing.

Does the moratorium start from sanction date or disbursement date?

Most lenders count it from the first disbursement date. Some count it from sanction date. Check your sanction letter under the section on “moratorium period” or “repayment terms.” The difference can be 2-4 weeks of additional interest accrual; not life-changing but worth knowing.

Can I withdraw my application after sanction without penalty?

Yes, before the loan agreement is signed and disbursement is initiated. Many lenders charge a small processing fee (typically ₹500-2,000) that’s non-refundable, but no other penalty applies. After agreement signing and disbursement, you can prepay the loan in full with no penalty (RBI rules on floating-rate retail loans), though you’ll have paid one or two months of interest.

If you’re preparing for the application stage, the documents required guide, the CIBIL score requirements post, and the interest rate comparison cover what to have ready before you submit. If timing the loan with a visa appointment matters (it usually does), the destination posts (Canada, Germany, Australia, Ireland) cover the visa-stage funds proof requirements lender-by-lender.