Yes, you can usually get an education loan with backlogs in India, though the path narrows. Active uncleared backlogs are the real problem, not cleared ones. From what I see, most lenders accept up to 4 to 6 cleared backlogs on unsecured loans without much push-back. Above that, the amount or rate may shift. Collateral-backed loans are far more forgiving, because the property does the underwriting work.

A reader in Hyderabad messaged in February. Her son had finished his BTech in computer science from a Tier-2 college with 6 backlogs across his 8 semesters, 4 of which he had since cleared. CGPA was 6.2. He had an admit to a UK master’s, decent IELTS, and a strong work-experience explanation (he had taken time off during the pandemic to support family business). The family was applying for a ₹32L education loan. Two NBFCs had rejected. A third had asked for additional documentation about the backlogs and the explanation, and was sitting on the application for three weeks.

The question every Indian family in this situation asks: can we get the loan at all? The answer is yes, more often than not, but the path is specific. Backlogs are not an automatic disqualifier, and lenders have differentiated policies on cleared vs active backlogs, count thresholds, and how academic history interacts with institution tier. This post walks through what actually matters for the loan decision when the academic transcript has backlogs.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

Other eligibility situations worth reading: the education loan without ITR post, the education loan for working professionals post, and the education loan for distance mba post.

The 60-second answer

Education loans for students with backlogs are possible but the path narrows. Active (uncleared) backlogs are the bigger problem than cleared ones. Most lenders accept up to 4-6 cleared backlogs without significant push-back for unsecured loans; above that, the loan amount or interest rate may be affected. Active backlogs at the time of loan application typically lead to rejection or postponement until cleared. Collateral-backed loans are more forgiving of backlogs because the property does the underwriting work. The destination country matters: UK and Australia are usually accepting; US and Germany lenders are stricter; Canada sits in the middle. The student’s overall academic trajectory (improving grades, work experience, strong test scores) can compensate for backlogs in the right narrative.

What banks actually look at on the transcript

Indian education loan underwriters check the transcript for these signals, in roughly this order of importance:

- Active vs cleared backlogs. Active backlogs at the time of loan application are flagged in the underwriting note. Cleared backlogs (failed initially but later passed) are noted but treated more leniently.

- Total backlog count over the program. A student with 2 cleared backlogs is in a different category from one with 10.

- Recent academic performance. Did the student improve in later semesters? Final-year grades carry more weight than first-year grades.

- Overall CGPA or final percentage. A clean 6.0 with no backlogs reads better than 6.5 with multiple backlogs to many lenders, despite the higher percentage.

- Institution tier. Backlogs from a Tier-1 institution (IIT, NIT, top private engineering) are more forgivable than the same from a less-known institution.

- The course the student is now applying for. A move from a regional engineering college to a master’s at an Ivy League institution suggests the student has grown; this counts in the narrative.

The actual decision is rarely about backlogs alone. It’s about backlogs in combination with all the other underwriting inputs (co-applicant CIBIL, loan amount, institution). Having a clean, complete file at the point of application matters more when the transcript is already a question mark, so the documents required for an education loan become worth getting right the first time.

The active vs cleared backlog distinction

This is the most important distinction. The pattern:

Faz's ruleActive backlogs are the deal-breaker. Cleared backlogs are usually survivable.

Lenders see active backlogs as risk that you won’t complete the degree. Most won’t proceed until they’re cleared. Cleared backlogs (even 6-10 of them) are usually fine with a brief explanation and a strong destination institution acceptance.

Active backlogs are courses where the student is currently failed and has not yet passed in a re-examination. These show on the transcript as “F” or “AB” (absent) or “Reappear” without a subsequent pass. Lenders see these as:

- Indicator that the student may not complete the degree

- Risk that the next institution may not accept the student if backlogs remain at admission

- Direct underwriting concern: 1-3 active backlogs usually lead to additional document requests; 4+ usually leads to rejection

Cleared backlogs are courses where the student initially failed but subsequently passed in a re-examination, supplementary exam, or course repeat. These show as the course appearing twice on the transcript, with the second attempt as a pass grade. Lenders see these as:

- Evidence that the student took the time to address the failure

- A less worrying signal than active backlogs

- Typically: up to 4-6 cleared backlogs accepted without question by most lenders; 7-12 raises eyebrows but doesn’t immediately reject; 12+ is harder

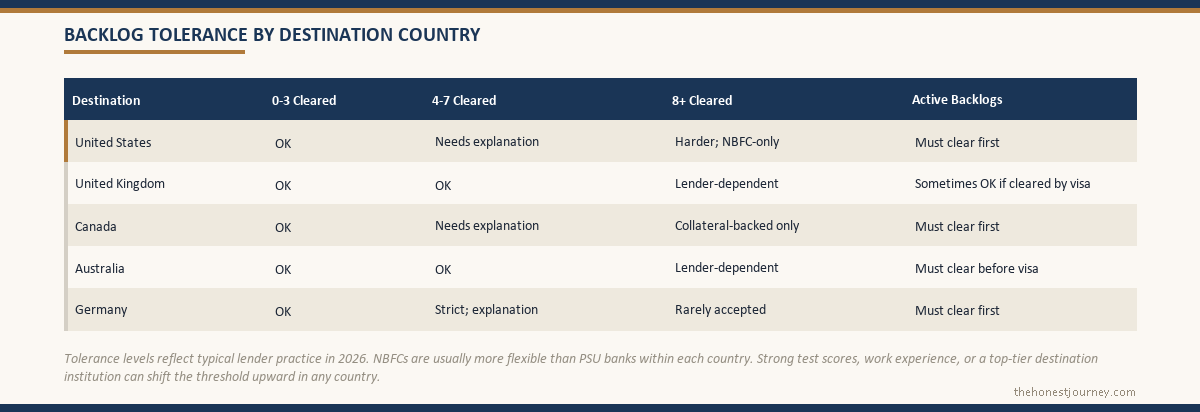

Country-specific patterns

The destination country influences the lender’s tolerance because the lender knows what kinds of students get visa approvals there.

United States

Lenders are stricter on backlogs for US-bound students. Reasons:

- US universities themselves often require detailed explanations for any failures

- US student visa officers (F-1 interviews) sometimes probe academic record

- US institutions can revoke an offer for non-disclosure of backlogs

Practical thresholds:

- 0-3 cleared backlogs: usually fine

- 4-7 cleared backlogs: needs explanation; many lenders accept

- 8+ cleared backlogs: harder; some lenders decline; NBFCs may price higher

- Any active backlog: typically reject until cleared

United Kingdom

UK universities and lenders are typically more accepting of backlogs. Reasons:

- UK universities emphasise the final-year project and final grade more than the full transcript

- Visa officers are less focused on the academic transcript details

- UK lenders price more around the institution tier than the transcript

- The post-study UK Graduate Route visa does not reassess the prior degree, so lenders worry less about the older transcript

Practical thresholds:

- 0-5 cleared backlogs: usually fine

- 6-10 cleared backlogs: needs explanation; usually accepted

- 11+ cleared backlogs: lender-dependent

- 1-2 active backlogs: sometimes accepted if cleared before visa stage

Canada

Canadian universities and lenders are moderately strict. The PGWP (post-graduation work permit) eligibility depends on completing the program, which makes backlogs at the student’s previous degree a relevant signal.

Practical thresholds:

- 0-4 cleared backlogs: usually fine

- 5-8 cleared backlogs: needs explanation; usually accepted

- 9+ cleared backlogs: lender-dependent; collateral-backed loans more forgiving

- Active backlogs: typically must be cleared before visa stage

Germany, France, other European destinations

These countries vary. Germany is particularly strict on academic record (especially for technical programs). France is more flexible.

For Germany specifically:

- 0-3 cleared backlogs: usually fine

- 4-6 cleared backlogs: needs explanation; some lenders accept

- 7+ cleared backlogs: harder; usually only with strong destination institution

- Active backlogs: must be cleared before applying

Australia

Australian universities and lenders are typically among the most flexible on backlogs. The 485 graduate visa pathway doesn’t probe the previous degree’s transcript heavily.

Practical thresholds:

- 0-5 cleared backlogs: usually fine

- 6-10 cleared backlogs: needs explanation; usually accepted

- 11+ cleared backlogs: lender-dependent

- Active backlogs: must be cleared before visa stage

How to compensate for backlogs in the application

The narrative matters. Specific things that strengthen an application with backlogs:

Faz's ruleThe destination institution's strength can override the academic record. A top-50 acceptance is strong evidence.

If a globally-ranked university has already evaluated the transcript and extended an offer, the lender takes that signal seriously. Pair the admit with strong test scores or work experience and the application shifts from ‘weak student’ to ‘growing professional with university validation’.

Strong test scores. A high GRE (315+), GMAT (700+), or IELTS (7.5+) signals that the student has academic capability even if the undergraduate transcript has gaps. We covered some of this in the scholarships post where high test scores also unlock scholarships.

Work experience between degrees. 1-3 years of relevant work experience between undergraduate and master’s signals maturity and recovery. The work experience changes the underwriting narrative from “weak student” to “growing professional.”

Strong final-year project or thesis. A published research paper, a noteworthy capstone project, or industry recognition during the final year compensates for earlier semester struggles.

Strong destination institution. An admit to a top institution (Top 50 globally) suggests that institution evaluated the transcript and decided to accept anyway. Lenders take this seriously.

Clear explanation in the application. A written note explaining the circumstances behind any active or large number of backlogs (health issues, family circumstances, course difficulty, change of major) helps. Don’t hide; explain.

Co-applicant strength. If the co-applicant has very strong CIBIL, income, and credit history, the backlog issue weighs less in the overall decision. Picking the right person for that role is a decision in itself, and the co-applicant rules post walks through who qualifies and how the choice changes the underwriting math.

How the backlog explanation letter should actually read

Most families treat the explanation letter as a formality and write three vague lines about “personal difficulties.” That is a wasted document. The underwriter reading it has seen hundreds of these, and a generic letter signals that the student has nothing concrete to say. A letter that works does four specific things.

It names the period, not the whole degree. Backlogs almost never spread evenly across 8 semesters. They cluster. A letter that says “the 4 backlogs all fell in semesters 3 and 4, during the period my father was hospitalised” is far stronger than one that apologises for the whole transcript. The underwriter can see the cluster on the transcript anyway, so matching the letter to the visible pattern builds credibility.

It shows the recovery with numbers. “I improved in later semesters” means nothing. “My semester 3 and 4 SGPA was 5.1 and 5.4; my semester 7 and 8 SGPA was 7.8 and 8.1” is evidence. The underwriting note will often quote exactly this kind of trajectory back to the credit committee, so handing it to them pre-written helps the case move.

It states the clearance status plainly. One line: “All 6 backlogs were cleared by re-examination; 4 by December 2024 and the final 2 by May 2025. No active backlogs remain as of this application.” Underwriters spend real time trying to confirm this from the transcript. Stating it removes a query round and can shave a week off processing.

It ends with the destination institution’s decision. “The University of Leeds reviewed this complete transcript and extended an unconditional offer for the MSc in Data Science.” That sentence reframes the entire letter. It tells the lender that an institution with its own academic standards already priced in the backlogs and still said yes. Keep the letter to one page. A long letter reads as anxiety; a tight one reads as a student who has understood the problem.

When backlogs aren’t the actual problem

Sometimes the rejection or query around backlogs is actually a proxy for something else:

- The institution isn’t strong enough to overcome the transcript (the institution policy is the real issue)

- The loan amount is too high for the profile (transcript is the supporting reason, not the primary one)

- The co-applicant is weak (transcript becomes the named issue in the rejection note)

- The destination policy is changing (Canada in 2024-2026, for example, where overall acceptance has tightened)

The way to test which: apply to a different lender with a similar profile. If the same case sanctions elsewhere, the original rejection was lender-specific. If it gets declined again with similar feedback, the underlying issue is real.

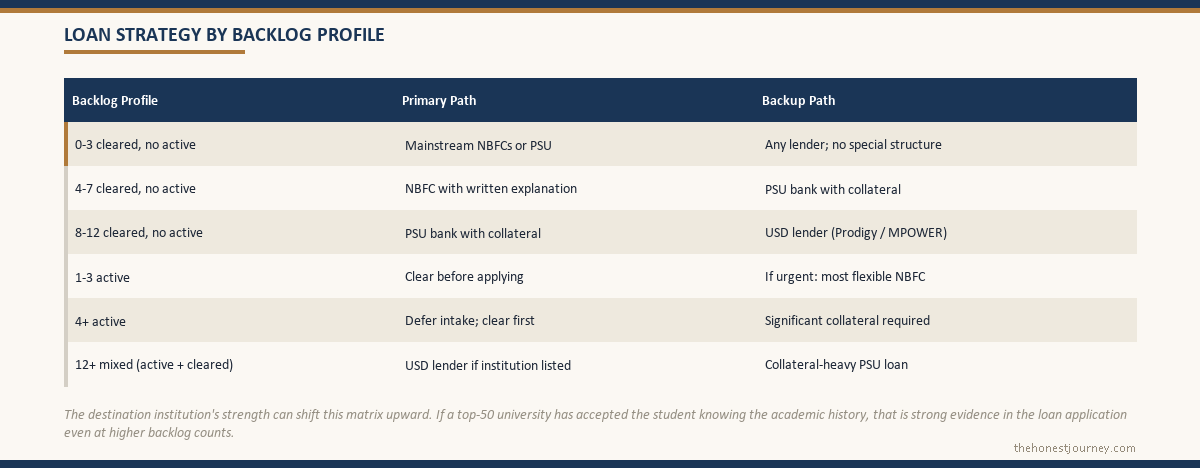

Strategy by backlog profile

0-3 cleared backlogs, no active

Apply to mainstream lenders (NBFCs first, PSU banks second). No special structuring needed. Most lenders will accept with a brief explanation if asked.

4-7 cleared backlogs, no active

Apply with a written explanation of academic circumstances. Strong test scores or work experience help. PSU banks with collateral are often more accommodating than unsecured NBFCs.

8-12 cleared backlogs, no active

Tighter path. NBFCs may decline or price higher. PSU banks with collateral are the primary route. Consider applying to a destination/institution that has the lender’s confidence.

1-3 active backlogs

Clear them before applying. Most lenders will not proceed with active backlogs on the transcript. If timing doesn’t allow, apply to NBFCs that have explicit policies for “in-progress” courses, but expect rejection or significant push-back.

4+ active backlogs

Almost certainly need to clear before any meaningful application. Defer the academic intake by a semester if needed to clear backlogs first.

Active + cleared backlog mix above 12

Hardest case. Most paths involve significant collateral or a different academic path. USD lenders (Prodigy, MPOWER) may still consider based on the destination institution’s acceptance.

Secured versus unsecured when the transcript is the weak point

When backlogs are the constraint, the secured loan route changes the conversation entirely. An unsecured NBFC loan is underwritten almost purely on profile signals: co-applicant CIBIL, income, and the academic record. The transcript carries real weight because there is nothing else to fall back on. A collateral-backed loan from a PSU bank works differently. The property valuation does most of the underwriting, and the academic record drops to a secondary check.

In practice this means a student with 9 cleared backlogs who is declined by three NBFCs can still sanction at SBI or Bank of Baroda against a property worth more than the loan amount. The PSU underwriter is looking at loan-to-value, the property title, and the co-applicant income, broadly along the lines of the RBI model education loan scheme that PSU banks anchor their policies to. The 9 backlogs become a noted item rather than a rejection trigger. The cost of that route is time: PSU collateral loans take 4 to 8 weeks against an NBFC’s 7 to 10 days, and the property paperwork (sale deed, encumbrance certificate, valuation) has to be clean.

There is also an interest cost angle. Secured loans typically price 1.5 to 3 percentage points below unsecured loans for the same borrower. A student pushed toward an NBFC because of backlogs may end up paying 12.5 to 13.5 percent, while the same family using property as collateral at a PSU bank lands closer to 9.5 to 10.5 percent. Over a 10-year repayment on a 30 lakh loan that gap is several lakh rupees. So the backlog problem is not only an approval problem, it is quietly a pricing problem, and the collateral route solves both at once. The trade-off table below is worth reading against your own timeline; if the intake is months away, the slower secured route is usually the better financial decision.

One caution: do not offer collateral reflexively just because the transcript is weak. If the co-applicant profile is genuinely strong and the backlogs are all cleared and under 6, an unsecured loan may still sanction at a fair rate, and you keep the property unencumbered. Offer collateral when the unsecured route has actually failed or when the backlog count is high enough that approval itself is in doubt, not before. The fuller trade-off is laid out in the secured versus unsecured education loan comparison.

The institution acceptance angle

If the destination institution has already accepted the student knowing the academic history, that’s strong evidence in the loan application. The application should explicitly call this out: “Despite the academic history, [University Name] has extended an admission offer based on [reason: high test scores, work experience, demonstrated capability].”

Some lenders specifically ask for the institution’s admission rationale or the student’s statement of purpose. Have these documents ready.

For applications to USD lenders, the destination institution is the primary underwriting input. If Prodigy or MPOWER has the institution on their approved list and has historical loan performance from graduates of that institution, the student’s transcript matters less.

Frequently asked questions

Can I get an education loan with backlogs?

Yes, in most cases. Cleared backlogs up to 4-6 are usually accepted by mainstream lenders. Active backlogs typically need to be cleared before the loan can be sanctioned. The specific tolerance depends on the lender, destination country, and the strength of other application inputs.

How many backlogs are too many for an education loan?

Roughly: 0-6 cleared backlogs are usually fine for most lenders. 7-12 cleared raises questions but is often workable. 12+ becomes harder. Active backlogs above 3 typically need to be cleared first.

Does CGPA matter for education loan?

Yes, indirectly. Lenders look at the overall academic profile. A clean transcript with 6.0 CGPA is often viewed more favourably than a 6.5 CGPA with multiple backlogs. But CGPA alone is not a deciding factor.

My education loan was rejected due to backlogs. What now?

Identify whether the backlogs are the real issue or a proxy for something else (co-applicant, institution, loan amount). Try a different lender first. Consider clearing any active backlogs before the next application. Strengthen the application with test scores, work experience, or co-applicant changes.

Do banks check my college transcript before sanctioning?

Yes, the academic transcript is a standard underwriting input. Some banks pull it from the institution directly; most accept the institutional copy provided by the applicant. Discrepancies between the provided transcript and the institutional record can cause delays.

Are backlogs from a Tier-1 institution different from a Tier-2?

Yes, in practice. Lenders implicitly weight the institution. Backlogs from an IIT or NIT are taken less seriously (the assumption is that these are difficult institutions where many students have some struggle) than the same from a less-known college.

Can I get a USD loan from Prodigy or MPOWER with backlogs?

These lenders underwrite the destination institution more than the student’s transcript. If the institution is on their approved list, backlogs in the previous degree matter less. Worth applying if domestic options have failed.

Should I disclose backlogs upfront in the loan application?

Yes. Always. Hiding them and having the bank discover them later (via the transcript) damages the application much more than upfront disclosure. Disclose, explain, and provide context.

Can I apply for an education loan while I still have active backlogs?

Most lenders won’t proceed with active backlogs on the transcript. Clear them first if possible. If urgent, apply to the most flexible NBFCs but expect rejection or a request to defer until backlogs are cleared.

For related context: the CIBIL score post covers the co-applicant credit thresholds that interact with the backlog narrative; the rejection reasons post covers how to identify whether backlogs are the true issue or a proxy; the no-collateral loan post covers the unsecured options when the academic record is the constraint; and the destination posts (Canada, Germany, Australia, Ireland) cover the country-specific visa requirements that interact with academic history.