For an education loan in India, lenders look at the co-applicant’s CIBIL score, almost always a parent, since most students have no credit history. The cutoff depends on lender type: PSU banks with collateral often go down to 650 to 680, private banks want 700 plus, and NBFCs lending without collateral want 720 to 750, with the best sub-11% rates needing 750 plus.

For an education loan in India, lenders look at the co-applicant’s CIBIL score, almost always a parent, since most students have no credit history. The cutoff depends on lender type: PSU banks with collateral often go down to 650 to 680, private banks want 700 plus, and NBFCs lending without collateral want 720 to 750, with the best sub-11% rates needing 750 plus.

A reader’s mother messaged me in February. Her daughter had a sanctioned admit to a UK master’s, a ₹32L education loan application pending with a major NBFC, and a rejection email she didn’t understand. The line in the email said “applicant credit profile does not meet sanction criteria.” Her daughter had never taken a loan. Never owned a credit card. Had no CIBIL score at all. The mother, who would have been the co-applicant, had a CIBIL of 712. The lender had rejected on her score. She was confused. 712 sounded good to her. It is good, in most other contexts. Not for an unsecured education loan to study abroad.

That email is the reason for this post. The CIBIL question is the single most-asked thing in our inbox, and the single most-misunderstood requirement at sanction stage. Whose score matters, what the actual cutoff is by lender category, and what you can do in the 30 days before applying if either credit file is thin or scarred.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The 60-second answer

For a student with no Indian credit history (the default), the lender looks at the co-applicant’s CIBIL score, almost always a parent. The score they need depends on the lender category and the loan type. PSU banks with collateral-backed loans often go down to 650-680. Private banks want 700+. NBFCs lending without collateral want 720-750 minimum, and the better rates (sub-11%) typically require 750+. The student’s own CIBIL (if any) becomes a secondary signal that helps but rarely makes or breaks the application. A “no-hit” file (no score at all) is treated as neutral, not as a negative.

Whose CIBIL the lender actually pulls

Here is the part that surprises most families. Lenders do not usually look at the student as the borrower whose creditworthiness drives the decision. Even when the loan is technically in the student’s name with a parent as co-applicant, the underwriting decision rests on the co-applicant’s credit profile, because the student has no income, no repayment history, and often no credit file at all.

Faz's rule

The co-applicant's CIBIL is the gatekeeper, the student's is rarely checked.

Even a 780 student CIBIL won’t offset a 680 co-applicant. The lender underwrites the parent’s repayment capacity, not the student’s potential. Plan the co-applicant first; everything else is downstream.

The exception is when the student has been earning for a few years (working professionals returning for an MBA, for instance, or a master’s after some years in industry). In those cases the student’s own CIBIL becomes relevant and the co-applicant requirement softens. We covered this kind of profile in the education loan for MBA post.

Three things this means in practice:

- A high student CIBIL does not compensate for a co-applicant with a damaged file. A student with a 780 (from a single credit card used responsibly over two years) cannot offset a co-applicant with a 680. The lender is underwriting the co-applicant’s repayment capacity, not the student’s.

- A “no-hit” student file is not a disqualifier. If the student has never had a loan or credit card, CIBIL returns no score. Lenders are used to this. They do not penalise it.

- Both files get pulled. Even though the co-applicant drives the decision, lenders still run a CIBIL check on the student. This is partly to verify identity and partly to flag any unknown existing credit (occasionally there are surprise hits, a forgotten co-applicant on a relative’s loan, or a credit card the student does not remember opening).

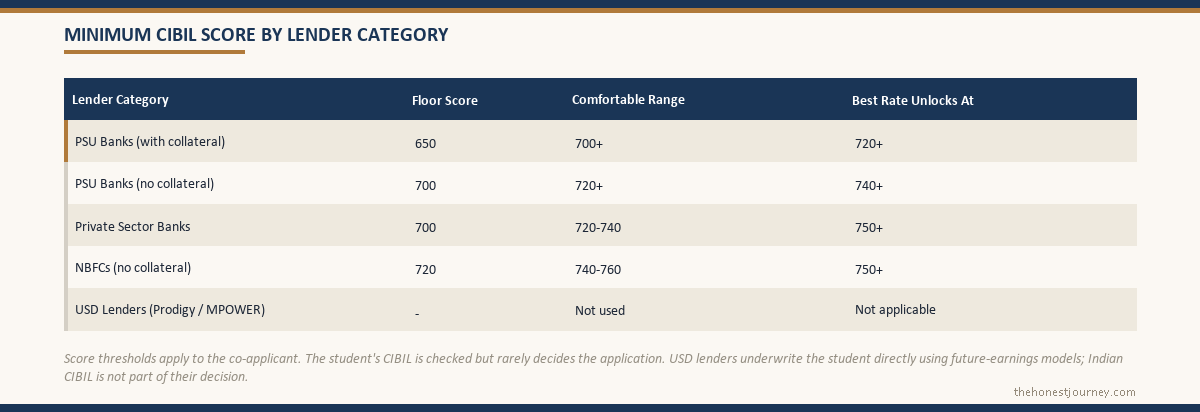

The actual score cutoffs by lender category

Cutoffs vary lender to lender, but the patterns hold by category. These are the working thresholds I have seen across applications over the last 18 months.

Public sector (PSU) banks

PSU banks underwrite using the IBA Model Education Loan Scheme as a baseline, with internal adjustments. For loans backed by collateral:

- Floor: usually 650 on the co-applicant

- Comfortable zone: 700+

- The collateral effectively underwrites the credit risk, so the score requirement is softer

For unsecured PSU loans (under ₹7.5L through the PM Vidyalakshmi credit guarantee scheme):

- Floor: 700

- The 75% Credit Guarantee Fund Trust backing helps, but PSU banks are still cautious here

Private sector banks

Private banks (Axis, Kotak, ICICI for collateral loans, HDFC main bank for select profiles) want a stronger co-applicant profile because they price more aggressively:

- Floor: 700

- Comfortable zone: 720-740

- For the better interest rate brackets: 750+

NBFCs (HDFC Credila, Avanse, Auxilo, InCred, IDFC First)

NBFCs do the heavy lifting for the no-collateral abroad-studies market. Without collateral, the credit profile is the only real underwriting handle. Cutoffs are tighter:

- Floor: 720 in almost every case

- For premier institutions: sometimes flexibility down to 700

- For best rates (sub-11%): 750+

- A 760+ co-applicant typically unlocks the fastest sanction and the lowest published rate within the lender’s range

We broke down what “best rate” means by lender type in the interest rate comparison post.

USD-loan lenders (Prodigy, MPOWER)

These do not pull Indian CIBIL at all. They underwrite the student directly using future-earnings models based on the destination institution and field of study. Co-applicant Indian CIBIL is irrelevant here. If your domestic options have failed because of a co-applicant credit issue, this is the escape route worth checking. Rates are higher (typically 11-13% USD plus forex risk).

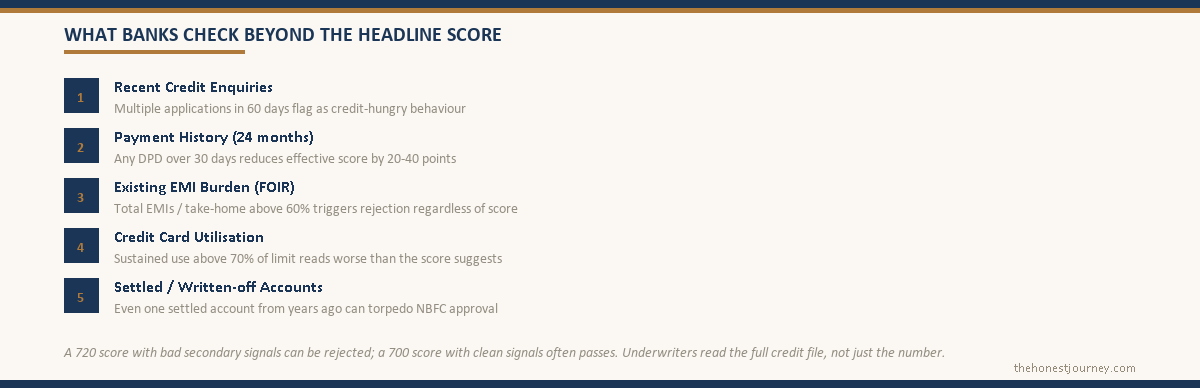

What banks check beyond the headline score

Faz's rule

A 720 score with bad secondary signals can be rejected. A 700 with clean signals often passes.

Underwriters read the full credit report, not just the headline number. High FOIR, recent enquiries, sustained 80% card utilisation, or one settled account from years ago can all torpedo an otherwise acceptable score.

A 720 score does not mean automatic approval. The CIBIL report has details that lenders read independently of the headline number. CIBIL itself operates under the RBI Credit Information Companies framework, which is why the report a lender pulls is standardised across the country.

Recent enquiries. If the co-applicant has applied to three lenders in the last two months, the report shows it. Multiple enquiries close together flag as “credit-hungry behaviour” and can pull the effective score down by 20-30 points in the underwriter’s eyes, even if the displayed number is unchanged. The fix is to apply selectively. Pre-qualify with one or two lenders, not five.

Payment history on existing loans and cards. A score of 740 with one 30-day late payment in the last 12 months is read differently from a 740 with a clean record. Lenders specifically look for any DPD (days past due) over 30 in the 24 months before application. One slip in 24 months is usually survivable. Two slips, or any DPD over 60, typically triggers a rejection.

Total existing EMI burden. This is the FOIR (fixed obligations to income ratio) check. If the co-applicant is already paying ₹85,000 a month in EMIs against a ₹1,30,000 take-home, adding a ₹40,000 education loan EMI tips the FOIR over 90%. Most lenders cap acceptable FOIR at 60-65%. A high score with high FOIR is still a rejection. We see this often with parents who have a home loan plus a car loan plus credit-card revolving balances.

Credit utilisation on cards. If the co-applicant is using 80%+ of their credit card limit consistently, even with on-time payments, the score reads lower in the lender’s eyes than the number suggests. A clean 720 with 25% utilisation is treated better than a 720 with 85% utilisation.

Settled or written-off accounts. Any account marked as “settled” (not “closed”) on the report is a red flag. “Settled” means the lender accepted less than the full amount owed. It depresses the score and is visible in the report for 7 years. One settled account in the co-applicant’s history, even from a small personal loan a decade ago, can torpedo an education loan sanction in the NBFC space.

The 30-day cleanup before applying

If the co-applicant’s CIBIL is close to the threshold but not quite there, there are a few moves that can lift it 20-40 points before the application goes in. None of these are tricks. They are basic credit hygiene that most people skip.

Pay down credit card balances to under 30% of the limit. Credit utilisation is one of the fastest score movers. If a card has ₹4L limit and ₹3.4L outstanding, paying it down to ₹1L before the next statement cycle can lift the score by 15-25 points within one credit cycle (typically 30-45 days).

Close any unused dormant credit accounts only carefully. Counterintuitively, closing old unused cards can hurt the score by reducing the average account age. Leave them open if possible. If they have annual fees, downgrade rather than close.

Settle any small disputes shown on the report. Pull the free CIBIL report from the official CIBIL site (one free report per calendar year) and check for errors. Disputed entries that should not be there (a credit card someone forgot they closed, a loan settled but still showing as active) can be raised through the CIBIL dispute resolution centre. Resolution takes 30 days; if the loan application is urgent, this is too slow.

Avoid any new credit applications in the 60 days before the education loan goes in. Every new application creates a hard enquiry. Stack them and the score can drop 10-15 points temporarily.

Do not close the education loan application file midway and re-apply. If you get a “soft rejection” or are asked for additional documents, complete the file. Withdrawing and re-applying creates two enquiries and signals indecision. Lenders pull the second application with extra caution.

When the co-applicant’s CIBIL is the actual problem

This is the harder situation. If the parent’s CIBIL is genuinely below the threshold (say 640, with a payment-history issue not just a clean low score), the cleanup options are slow. CIBIL takes 6-12 months to repair from a single major delinquency. The realistic paths:

- Use a different co-applicant. Spouse, sibling, in-laws (some lenders accept), or another close relative with a clean credit file and stable income. This needs to be raised with the lender at application stage, not after a rejection.

- Pivot to a collateral-backed PSU loan. With collateral, the credit threshold drops. A SBI Global Ed-Vantage loan with property collateral can be sanctioned to a co-applicant in the 650-670 zone if the collateral covers the loan amount with margin.

- Pivot to a USD lender (Prodigy or MPOWER). No Indian co-applicant CIBIL needed. The trade-off is rate, forex risk, and tighter institution lists. We covered the math comparison in the no-collateral loan post.

- Use the PM Vidyalakshmi portal for the smaller-amount, lower-threshold loans (up to ₹7.5L unsecured with credit guarantee). This works as a partial solution combined with family savings for the rest.

- Wait, repair, and reapply. If the timeline allows, 8-12 months of clean repayment behaviour on existing accounts can lift a 640 to a 700. Realistically, this means deferring the academic intake by a semester or a year.

When the student’s CIBIL starts to matter

For most undergraduate and direct-to-master’s applicants, the student’s own CIBIL is irrelevant to the sanction decision. It starts to matter in three cases.

Working professionals returning for an MBA. If you have 3-5 years of salaried income and have used credit cards or a personal loan or a home loan during that time, your CIBIL is the primary underwriting input. A co-applicant becomes a backup signal, not the primary one. Score requirement: 720+ for the better unsecured EMBA / MBA-abroad loans.

Students with existing personal loans or credit card debt. Occasionally we see students with personal loans from college years, or credit card balances built up over a part-time-work-while-studying-in-India period. These create a CIBIL file. If that file has bad marks (missed payments, settled accounts), it can complicate the application even when the parent’s CIBIL is strong. The lender adds the student’s exposure to the household FOIR calculation.

Post-disbursal, during repayment. Once the loan is disbursed, both the borrower and co-applicant get an active account showing on their CIBIL. The student, now on the credit grid, starts building a file. Missed EMIs hurt both. This matters in 2-4 years when the student tries to take their own first credit card or rent an apartment abroad that requires a credit check (some countries pull Indian CIBIL as part of background checks).

What the application form actually asks for

When you apply, the lender requires:

- The co-applicant’s PAN. Used to pull CIBIL.

- A signed consent for the credit pull. Standard in every application.

- Often, the student’s PAN as well (if they have one), even though the score is rarely the deciding signal.

- Bank statements for the last 6 months for the co-applicant. The lender cross-checks CIBIL with actual transaction behaviour.

- Income proof. Salary slips, ITR for last 2-3 years (filed on the income tax department e-filing portal), Form 16. The income proof and CIBIL together build the underwriting picture.

The documents list is identical to what we listed in the documents required for education loan post. What changes by lender is the strictness of the credit threshold, not what they ask for.

Two real applications, two outcomes

Application A. Student profile: 21-year-old engineering graduate, no credit history. Co-applicant: father, salaried, ₹18L gross annual, CIBIL 742, FOIR currently 35% (a small home loan plus one credit card paid in full monthly). Loan needed: ₹28L for a Canadian master’s. Lender approached: a major NBFC. Outcome: sanctioned in 8 working days at 10.85% interest. No second-round queries. The 742 score + clean credit utilisation + low FOIR + decent income made this an easy underwrite.

Application B. Student profile: same age, no credit history. Co-applicant: mother, salaried, ₹14L gross annual, CIBIL 698, FOIR 55% (active home loan + an EMI on a recent washing machine purchase + a credit card consistently at 70% utilisation). Loan needed: ₹35L for a US master’s. Lender approached: same NBFC. Outcome: rejection after 11 working days. The rejection note said “credit profile insufficient.” Translation: 698 is below threshold, FOIR is high, utilisation is high, and the loan amount is large relative to income.

The fix for Application B: switch the co-applicant to the father (if available and willing), pay down the credit card before re-applying, and pivot the difference to a co-secured loan with some collateral. With those changes the same family could likely sanction the same loan from a PSU bank within 3-4 weeks.

What to do before you apply

A practical checklist for the 30-60 days before submitting an education loan application:

- Pull the co-applicant’s CIBIL report. Not just the score, the full report. Look at every line item.

- Pay down high-utilisation credit cards to under 30% of limit. Time the payment so it shows on the next statement.

- Clear any small dues that might be sitting unnoticed (an old credit card with a ₹450 statement balance from 2024 can drag the score down by 40 points if it has rolled to a late status).

- Decide co-applicant before approaching lenders. Switching mid-application is messy.

- Pre-qualify with one lender. Most NBFCs offer soft-pull pre-qualification that does not affect the score. Use it to know whether you are in range before formal application.

- If pre-qualification fails or returns a low offer, pause. Either repair credit, change co-applicant, or pivot to a different loan type. Do not file four applications in two weeks.

- Once you proceed, do not let any existing EMI miss the due date during the application processing window. A missed EMI mid-process can pull the CIBIL down enough to fail the final underwriting check even after initial approval.

The honest summary: the co-applicant’s CIBIL is the gatekeeper. A clean 740+ co-applicant unlocks most options. A clean 700-740 co-applicant unlocks most domestic options. Below 700, it gets harder and the workarounds (collateral, PM Vidyalakshmi, USD lenders, different co-applicant) start to dominate the conversation. Plan this 60 days before the application, not the night before.

Frequently asked questions

I am a student with no CIBIL score. Will my application be rejected?

No. A “no-hit” student file is the default for first-time borrowers. Lenders underwrite the co-applicant. The student’s lack of credit history is not a negative.

My CIBIL score is 720 and my parent’s is 680. Whose score does the lender use?

The co-applicant’s. The lender will treat this as a 680 application. Your 720 helps secondary signals but does not raise the floor.

How long does it take to improve a CIBIL score from 680 to 720?

Realistically, 6-9 months of disciplined credit behaviour: paying down balances, on-time payments on every account, no new credit applications. A 40-point lift in this range is achievable but not fast.

Does a CIBIL hard enquiry from a loan application hurt my score?

Yes, temporarily, by 5-15 points. The effect fades over 6-12 months. Multiple enquiries stacked together hurt more because they signal credit-hungry behaviour to underwriters.

Can I apply to multiple lenders at once?

Technically yes, but each application creates a hard enquiry. Better practice: pre-qualify with one or two using soft pulls, then submit a formal application only to the one most likely to approve. We covered this in the documents required post.

My CIBIL shows a “settled” account from 8 years ago for ₹15,000. Will this affect the education loan?

It will register, especially with NBFCs. The right move is to contact the original lender (if traceable) and ask for an updated reporting status, sometimes a settled account can be re-marked if the full original amount was eventually paid. If not, disclose it upfront in the application and be prepared to explain the context. Lenders prefer disclosure over discovery.

Do USD-loan lenders like Prodigy or MPOWER check Indian CIBIL?

No. They use future-earnings underwriting based on the destination institution and field. Indian CIBIL is irrelevant.

My parent has no CIBIL because they have never taken any loan or credit card. Is that worse than a low score?

It is treated similarly to a low score by most lenders. A “no-hit” co-applicant file lacks the data to underwrite. The fix is either to add a co-applicant who does have a CIBIL file, or pivot to a collateral-backed PSU loan where the property is the primary underwriting input.

If you are preparing for an education loan application, start with the documents required guide and the interest rate comparison to set the right expectations on cost. If you are weighing whether collateral is the right move, the no-collateral loan post breaks down the trade-offs lender by lender category. If your worry is an academic blemish rather than the credit file, the education loan with backlogs in India post covers how lenders treat a pending or cleared backlog. And if the household tax planning matters as much as the rate (it usually does), the Section 80E tax benefit post shows how to set up the borrower-name decision so the deduction lands in the right hands.