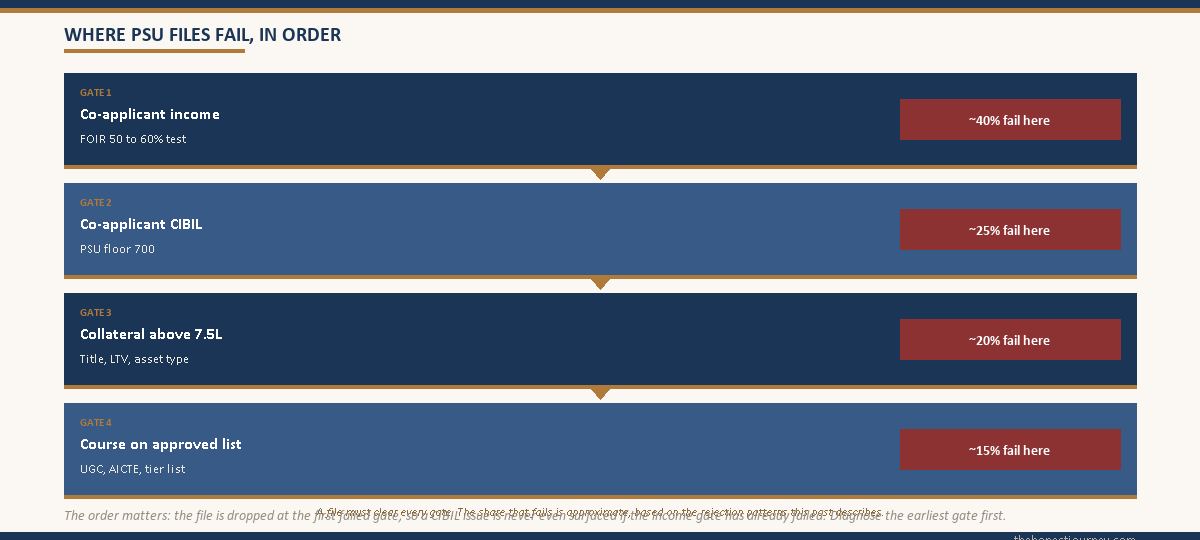

In my experience, education loan rejection is almost never about the student’s marks. Roughly 7 out of 10 PSU rejections I have seen come down to weak co-applicant income or a CIBIL score below 700. For a ₹30 lakh loan, the co-applicant usually needs around ₹81,000 net monthly income. Most are reversible by reapplying after 3 to 6 months.

Education loan rejection is one of those events that sounds dramatic the day it happens and looks almost mechanical six months later when you understand why it happened. A PSU branch officer types a polite line on the rejection letter (“application could not be approved at this time”), the relationship manager stops returning calls, and the family panics because admission deadlines are weeks away. Most of these rejections have the same handful of underlying causes, and most are fixable on a second application if you know what tripped the first one.

This post is the version I wish I had when my own first loan file came back from a PSU branch with a one-line rejection and no explanation. I went and pieced together what actually went wrong from a sympathetic branch officer over chai, and the pattern that emerged matches what almost every rejected borrower I have spoken to since has run into. The real reasons are boring, structural, and largely about the co-applicant and the collateral, not the student.

Education loan rejection in India is almost never about the student’s marks or admission letter. It is about the co-applicant’s income, CIBIL, and the bank’s internal view of the course and university. Roughly 7 out of 10 PSU rejections I have seen come down to weak co-applicant income or a CIBIL score below 700. Most rejections are reversible by fixing the underlying cause and reapplying after 3 to 6 months, or by switching to an NBFC that has a different risk model.

Other eligibility situations worth reading: the education loan for working professionals post, the education loan for distance mba post, and the education loan for CA students post.

Weak co-applicant income, the most common reason

The single largest reason PSU education loans get rejected is that the co-applicant’s income does not clear the bank’s internal debt-to-income test. Banks use a metric called FOIR (Fixed Obligations to Income Ratio) or DSCR (Debt Service Coverage Ratio) to decide whether the family can service the proposed EMI once the moratorium ends. The threshold most PSU banks use is that total monthly EMIs (existing + the proposed education loan EMI) should not exceed 50 to 60 percent of the co-applicant’s net take-home income.

For a ₹30 lakh loan at 10.5 percent over 10 years, the EMI works out to roughly ₹40,500 per month. To clear a 50 percent FOIR with no other loans, the co-applicant needs a net monthly income of at least ₹81,000 (around ₹12 lakh per year). Add an existing home loan EMI of ₹25,000 and the required income rises to around ₹1.3 lakh per month. Most PSU branches do not write this math down for the applicant; they just file the application as “income inadequate.” For a closer look at how the co-applicant equation actually works, the co-applicant for education loan India post covers the income tests in detail.

| Loan amount | Approx EMI (10.5%, 10 yr) | Min co-applicant net income (50% FOIR, no other EMI) |

|---|---|---|

| ₹10 lakh | ₹13,500 | ₹27,000 / month |

| ₹20 lakh | ₹27,000 | ₹54,000 / month |

| ₹30 lakh | ₹40,500 | ₹81,000 / month |

| ₹50 lakh | ₹67,400 | ₹1,35,000 / month |

| ₹75 lakh | ₹1,01,200 | ₹2,02,500 / month |

Self-employed co-applicants face a tougher version of this test. PSU banks look at the ITR of the last 2 to 3 years and average the net taxable income, not the gross turnover. If your parent runs a small business that shows ₹50 lakh in receipts but ₹8 lakh in net taxable income after expenses, the bank uses ₹8 lakh. This is the gap that catches a lot of business families: real cashflow exists, but the income shown on paper does not support a ₹40 lakh loan.

Faz's ruleIf your co-applicant's last 2 ITRs do not show enough income to service the proposed EMI at 50 percent FOIR, the PSU loan will be rejected. Fix the math before you file, do not after.

I have seen families file at three different PSU branches in a row hoping one of them will say yes. They never do, because the underwriting is centralised and the FOIR test is the same everywhere. The honest move is to drop the loan ask to a size the income supports, or add a second co-applicant (spouse, sibling) whose income can be clubbed.

Low CIBIL of the co-applicant, the silent killer

CIBIL score of the co-applicant matters more than most students realise. The student’s own CIBIL is usually thin or non-existent, so the bank leans almost entirely on the co-applicant’s credit history. The thresholds most banks use, based on the patterns I have seen and confirmed with branch officers, look roughly like this.

| Lender type | Minimum CIBIL of co-applicant | Comfort zone |

|---|---|---|

| PSU banks (SBI, Canara, BoB, PNB) | 700 | 750+ |

| Private banks (HDFC, ICICI, Axis) | 725 | 775+ |

| NBFCs (Avanse, Credila, Auxilo, Incred) | 650 (case by case) | 700+ |

Below 650, even NBFCs will usually decline. Between 650 and 700, NBFCs may approve with a higher interest rate (sometimes 12 to 14 percent vs the PSU rate of 9.5 to 11 percent). The reasons CIBIL drops are predictable: missed EMI on an earlier loan, credit card payment defaults, settled-not-closed status on a previous loan, or a high credit utilisation ratio on revolving cards. Check the report yourself before applying, from cibil.com, because banks will pull it the moment you submit the form and a hard inquiry is recorded regardless of approval. The IBA model scheme that PSU banks follow is published by the Indian Banks’ Association, and the borrower-side rules around scoring and disclosure flow from RBI’s master directions.

The settled-not-closed status is a particularly common trap. A co-applicant who settled a credit card bill 5 years ago for less than the full amount thinks the matter is closed. The CIBIL report carries the “settled” tag for years, and the bank reads it as “this person did not pay in full.” Get any settled accounts cleared and reported as “closed” before applying. This usually takes one or two months of follow-up with the original lender.

Course or university not on the bank’s approved list

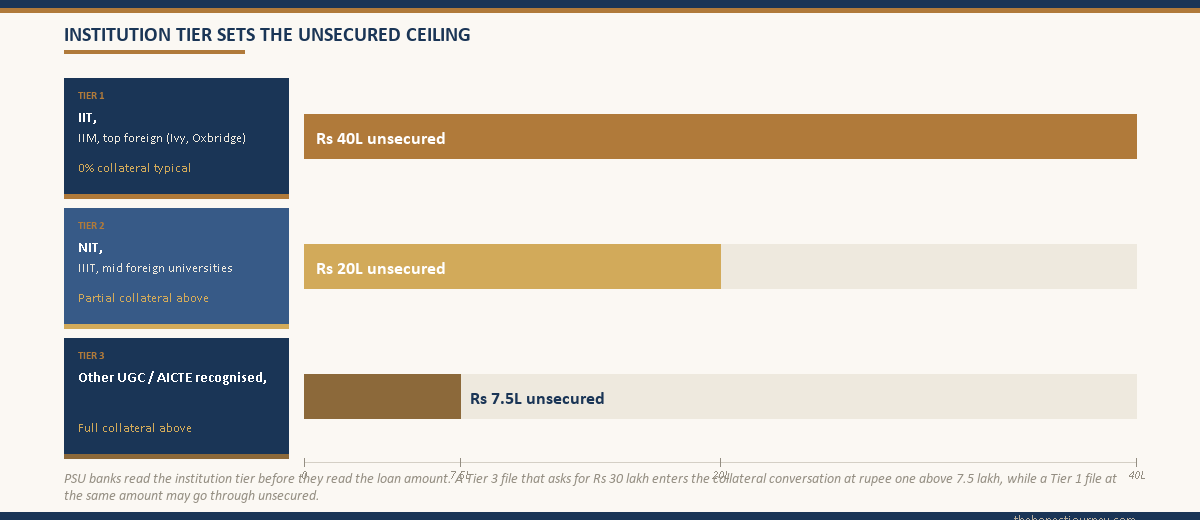

Banks maintain internal lists of approved universities and courses. For abroad studies, this list is usually structured as Tier 1, Tier 2, and Tier 3 institutions, with different sanction limits and collateral requirements per tier. SBI publishes a public version of this list as the “SBI Scholar Loan” institutions; other PSU banks keep their lists internal but the structure is similar. For India studies, the bank looks at whether the institution is approved by UGC, AICTE, MCI, NMC, BCI, or the relevant regulator for the discipline.

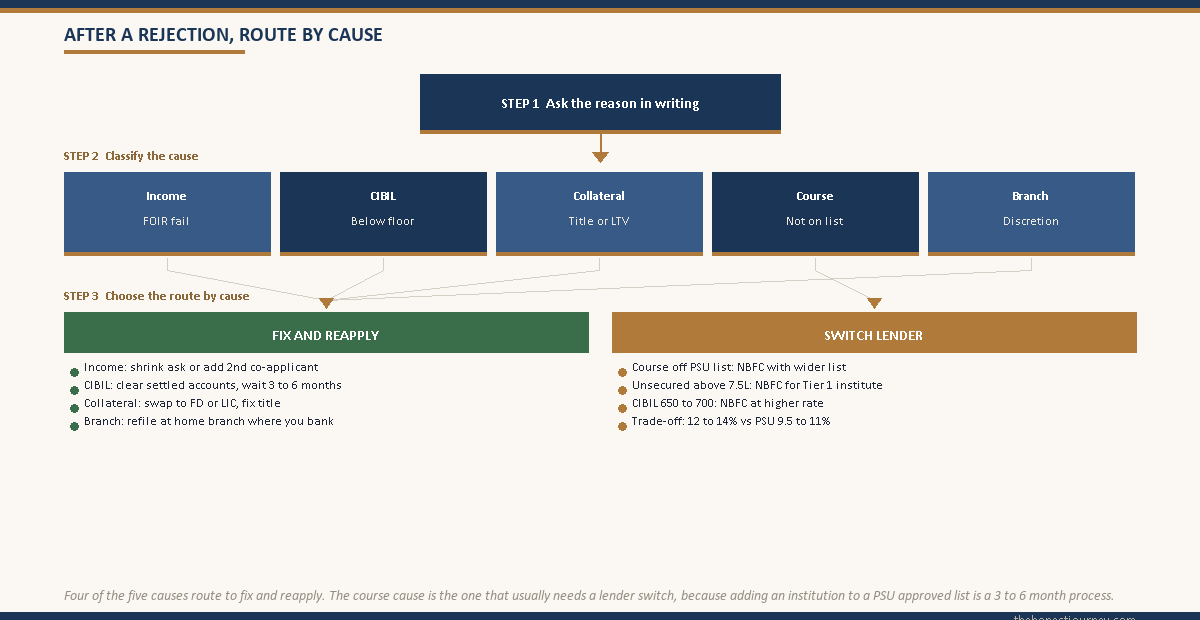

The fix, when the course is the issue, is to either switch lenders (NBFCs have wider approved lists, often including unaccredited international programmes if the student profile is strong) or to formally request the bank to add the institution to its approved list. The latter is slow (3 to 6 months) and usually requires the institution itself to apply for the bank’s tie-up programme. For a small or new programme, switching lenders is faster.

Inadequate or unacceptable collateral above the unsecured cap

Most PSU banks sanction up to ₹7.5 lakh as unsecured (no collateral required, only co-applicant). Above this threshold, collateral is mandatory. The acceptable collateral types and the loan-to-value (LTV) ratios are where rejections happen most frequently.

| Collateral type | Typical LTV | Common rejection reason |

|---|---|---|

| Residential property (self-owned) | 75 to 80% | Title not clear, property in joint name with disputes, agricultural land conversion not done |

| Fixed deposit | 90 to 95% | FD in third-party name without proper assignment, FD tenure shorter than loan tenure |

| LIC policy (surrender value) | 80 to 85% | Surrender value too low, policy not assignable, ULIP not accepted by most PSUs |

| Mutual funds / shares | 50 to 60% | Volatility haircut means the actual loan eligibility is much less than the market value |

The most common collateral rejection is for property where the title chain is unclear. PSU banks need a 30-year title search done by their empanelled lawyer. Any gap, dispute, or ancestral-property complication shows up as a “title not clear” remark, and the bank will not accept the property. Agricultural land in particular gets rejected by most PSU banks because conversion to non-agricultural use is needed before mortgage, and that process is slow and varies by state.

The fix is usually to switch to a different collateral asset. If the family has an FD or LIC policy with adequate surrender value, that is faster to mortgage than property. If only property is available, the title issues need to be resolved before reapplying, which can take 3 to 12 months. The IBA-model collateral norms followed by most PSU banks are documented on the SBI education loans page, which is a useful public reference for what the PSU underwriting actually asks for.

Faz's ruleIf the loan ask is above ₹7.5 lakh and the family does not have clear-title property, FD, or LIC policy of sufficient value, the PSU bank will reject. NBFCs may approve unsecured up to ₹40 to 50 lakh for premier institutes, at a higher rate.

The ₹7.5 lakh unsecured cap is a hard line at PSU banks. Above it, no collateral means no loan. NBFCs work differently; they use the institution’s tier and the student’s profile (IIT/IIM/top foreign university) to extend unsecured limits well past ₹7.5 lakh. The trade-off is the interest rate, which can be 2 to 4 percent higher.

Academic record gaps and unexplained breaks

Banks read the academic transcript before they sanction. A consistent record from 10th through current admission is the easy case. The harder cases are when there are gaps, course changes, or weak earlier results. A 1-year drop between 12th and undergrad, or between undergrad and the proposed master’s, raises a question that the bank will want answered with a gap certificate explaining what the student did during that time (preparation for entrance exams, family reasons, work experience).

What actually triggers rejection on academic grounds: a backlog or failed semester that is still open at the time of application, which the education loan with backlogs in India post addresses head-on, a gap of 2 years or more without a coherent explanation, switching courses multiple times (B.Com to engineering to MBA, for instance), and a sharp drop in marks between 12th and undergrad that the bank reads as a risk signal for course completion. None of these are absolute disqualifiers, but they shift the application to a higher-scrutiny pile, and a marginal application (borderline co-applicant income or CIBIL) that lands in that pile usually gets rejected.

The fix is documentation. A clear gap certificate, a written explanation from the student attached to the application, and evidence of what was done during the gap (course completion certificates, work experience letters, exam admit cards) can move the application back to the standard scrutiny pile. Reapply after you have the documentation, not before.

Branch-level discretion and the second-application effect

Even when the centralised underwriting clears all the technical filters, the branch manager has discretion to recommend or not recommend the loan. This discretion is loosely tied to the branch’s portfolio quality, the loan officer’s familiarity with the applicant family, and sometimes the relationship the family has with the branch (long-standing savings account, salary account, fixed deposits with the branch). A walk-in applicant with no prior relationship is treated differently from a family with a 15-year banking history at the same branch.

This is why the same loan file can get rejected at one PSU branch and approved at another a few kilometres away. The honest move, if you have flexibility, is to apply at the branch where the co-applicant’s salary account or main savings account is held. The branch already has the income history, the relationship is established, and the file moves faster. If you apply at a random branch you have no relationship with, you are competing with every other walk-in for the manager’s attention and the underwriting comes back more conservative.

For applications that get rejected at the branch level despite clearing the technical filters, the path forward is one of: reapply at the home branch (where the relationship is), apply at a different PSU bank (each bank’s centralised underwriting is independent), or switch to an NBFC. A second rejection at the same bank within 6 months is harder to overturn than starting fresh elsewhere.

Faz's ruleApply at the branch where the co-applicant already banks. Walk-in applications at random branches face conservative underwriting, because the loan officer has no relationship history to anchor on.

The first PSU loan I helped a friend get approved came after two rejections at random branches. The third application went to the branch where the father had held his salary account for 18 years, and the same file was approved in 3 weeks. The technical underwriting was identical. The branch-level discretion was completely different.

What to do after a rejection

The first step is to ask the bank, in writing, for the specific reason for rejection. PSU banks are required to provide this under RBI’s grievance redressal framework, though they often resist. A polite email to the branch manager and the bank’s grievance officer, citing the loan application reference number and asking for the rejection reason in writing, usually gets a response within 30 days. The RBI’s banking ombudsman is the escalation path if the bank does not respond.

Once you know the reason, the fix depends on what it is. If it is income, reduce the loan ask or add a second co-applicant. If it is CIBIL, work on the score for 6 months (clear settled accounts, bring utilisation below 30 percent, pay all EMIs on time) and reapply. If it is collateral, switch the collateral asset or move to an NBFC. If it is the course or institution, change the lender to one that approves the institution.

Rejection itself does not directly damage the student’s CIBIL, because the student usually has no significant credit history. The co-applicant’s CIBIL takes a small hit from the hard inquiry (typically 5 to 10 points) but the rejection itself is not flagged on the report. Multiple hard inquiries in a short window do hurt, so do not submit applications at 4 banks simultaneously. Apply at one, wait for the decision, then move on.

The case for trying an NBFC after a PSU rejection: NBFCs like Avanse, Credila, Auxilo, and Incred have different risk models. They accept lower CIBIL (sometimes 650), wider course lists, and unsecured amounts above the ₹7.5 lakh PSU cap for strong institute profiles. The trade-off is the interest rate (12 to 14 percent vs PSU’s 9.5 to 11 percent) and stricter prepayment terms. For abroad master’s at strong universities, NBFCs are often the realistic path. For domestic loans below ₹7.5 lakh where the PSU rejected on income or CIBIL grounds, an NBFC is less likely to approve either.

One important distinction: education loan rejection is not the same as student visa rejection. A US F1 visa rejection or a UK student visa refusal has its own causes (proof of funds shortfall, course-credibility doubts, ties-to-home weakness) and does not affect your education loan eligibility. Similarly, an education loan rejection does not directly affect your visa application, though the proof-of-funds requirement is harder to clear without a sanctioned loan. For loans where the co-applicant problem cannot be solved, the education loan without ITR post and the complete guide to education loans in India cover the alternative routes.

Faz's ruleA rejection is not a verdict on the student. It is usually a verdict on the co-applicant's income, the CIBIL score, or the collateral. Diagnose the cause first, then choose between fixing it and switching lenders.

The families I have seen recover fastest from a rejection are the ones that get the rejection reason in writing within 30 days, run a clear diagnosis, and either reapply with the fix or move to the right NBFC. The families that stall are the ones that file at the same bank twice in 3 months hoping for a different answer.

The honest closing take

Education loan rejection feels personal when it happens. It almost never is. The PSU underwriting machine runs 4 or 5 tests in sequence (co-applicant income, CIBIL, collateral, course approval, branch sign-off) and if any one fails, the file gets stamped rejected with a one-line reason that tells you nothing about which test failed. The honest first move after a rejection is to ask for the specific reason in writing, because each cause has a different fix and the fixes range from “reapply next week with a smaller loan ask” to “wait 6 months while CIBIL recovers.”

The second honest move is to recognise that PSU banks and NBFCs operate on different risk models, and a rejection at one does not predict a rejection at the other. PSU banks reward stable co-applicant income and clean CIBIL above all else. NBFCs reward institution tier and student profile, and they will quote a higher rate to take on what the PSU would not. Neither is universally better. The right lender depends on which test failed and which of your variables is hardest to change.

The thing I wish someone had told me earlier: most rejections are recoverable. The exceptions are the rare cases where the family genuinely cannot service the proposed EMI (income too low for any reasonable loan size) or where the course or institution is not financially supportable by any lender. Those are honest signals to rethink the funding plan. Everything else is paperwork, timing, and choosing the right lender on the second attempt.

FAQ

Why was my education loan rejected?

The most common reasons, in order of frequency, are: weak co-applicant income that fails the bank’s FOIR test, CIBIL score of the co-applicant below 700 for PSUs or 650 for NBFCs, collateral problems for loans above ₹7.5 lakh (unclear property title, agricultural land, FD in non-acceptable form), course or university not on the bank’s approved list, and academic gaps without a satisfactory explanation. Branch-level discretion can also play a role, especially for walk-in applicants without a prior banking relationship. Ask the bank in writing for the specific rejection reason, which they are required to provide under the RBI grievance framework.

Can I reapply after an education loan rejection?

Yes, but the timing depends on the cause. If the rejection was for income or collateral, you can reapply immediately with the fix (smaller loan ask, second co-applicant, different collateral). If the rejection was for CIBIL below threshold, wait 3 to 6 months while the score recovers, because reapplying immediately with the same score will produce the same outcome. Reapplying at the same bank within 90 days of a rejection is usually unproductive, because the prior application is in the bank’s system and the underwriting team has already declined. Move to a different bank or wait for the issue to be visibly resolved.

Does education loan rejection affect my CIBIL score?

The rejection itself is not recorded on your CIBIL report. What is recorded is the hard inquiry triggered when the bank pulled your credit report at the time of application. A single hard inquiry typically reduces the score by 5 to 10 points and the effect wears off within 6 to 12 months. The student’s CIBIL is rarely affected because students usually have thin credit files. The co-applicant’s CIBIL absorbs the inquiry impact. Avoid submitting applications to multiple banks simultaneously, because clustered hard inquiries compound the score impact.

Which banks reject education loans most often?

PSU banks have the strictest underwriting on co-applicant income and CIBIL, so they reject more applications in absolute terms but also process the largest application volume. Private banks like HDFC and Axis are stricter on CIBIL and tend to focus on premier institutions. NBFCs like Avanse and Credila have higher approval rates but charge 12 to 14 percent interest versus PSU’s 9.5 to 11 percent. There is no public bank-wise rejection statistic. The practical guidance is to apply at the PSU where your co-applicant holds the salary or savings account first, and treat NBFCs as the fallback for cases where the PSU declines.

Can I appeal an education loan rejection?

You can request a review through the bank’s internal grievance redressal channel. Write to the branch manager and copy the bank’s nodal officer or grievance redressal officer, citing the loan application reference number and asking for a review with any additional documentation you can provide. If the review is denied and you believe the rejection was procedurally unfair, you can escalate to the RBI banking ombudsman after 30 days. In practice, appeals succeed only when there is a clear documentation gap (a missing income proof, a wrongly classified collateral) that you can now supply, not when the underlying fundamentals (income, CIBIL) are the issue.

Will an NBFC approve a loan that a PSU bank rejected?

It depends on the rejection cause. If the PSU rejected because the loan exceeded ₹7.5 lakh unsecured and there was no collateral, an NBFC may approve unsecured up to ₹40 to 50 lakh for a strong institute profile. If the PSU rejected because CIBIL was below 700, an NBFC may approve at CIBIL 650 to 700 at a higher rate. If the rejection was for income inadequacy that fails the FOIR test, NBFCs run a similar test and are likely to decline as well. The rate trade-off is real: NBFC interest rates of 12 to 14 percent versus PSU rates of 9.5 to 11 percent can add ₹10 lakh or more in total interest on a ₹30 lakh loan over 10 years.

What is the minimum co-applicant income for an education loan?

There is no fixed minimum across all banks. The functional minimum is whatever income clears the bank’s FOIR test for your specific loan size, which is typically 50 to 60 percent of net take-home covering all monthly EMIs. For a ₹10 lakh loan, a net monthly income of around ₹27,000 is usually sufficient. For ₹30 lakh, around ₹81,000. For ₹50 lakh, around ₹1.35 lakh. These rise if the co-applicant has existing loans. Self-employed co-applicants are assessed on the average net taxable income from the last 2 to 3 ITRs, not on gross business turnover.

Is education loan rejection the same as student visa rejection?

No, they are independent processes with different causes. Education loan rejection is a credit decision based on co-applicant income, CIBIL, collateral, and the bank’s view of the institution. Student visa rejection is an immigration decision based on proof of funds, course credibility, ties to home country, and the genuineness of intent to study. A sanctioned education loan supports your proof of funds for the visa, so an education loan rejection makes the visa harder to clear, but the visa officer is not told about the loan rejection. Conversely, a visa rejection does not affect your education loan eligibility for future applications. The two have to be solved separately.

Faz · The Honest Journey · 2026