A co-applicant in an education loan is a person, usually a parent, who shares the legal responsibility for repaying the loan alongside the student. Almost every education loan in India requires one, since the student rarely earns during the moratorium. The bank assesses their income, credit score, and repayment history. For loans above 7.5 lakh, banks usually want collateral plus a co-applicant.

My cousin called me in a panic last August. Her education loan application for a Master’s in the UK had been “under review” at a PSU bank for six weeks, and the branch manager had finally told her father, off the record, that the file was stuck because the co-applicant income looked thin on paper. Her father is a small business owner. His ITR showed ₹4.2 lakh net for FY24. The loan ask was ₹28 lakh. The bank was not saying no. It was saying nothing, which is worse.

We spent a Saturday morning rebuilding the file with her mother added as a second co-applicant (she had a small salaried teaching income), pulling the family CIBIL reports, and rewriting the FOIR worksheet. The loan was sanctioned 11 days later. The problem was not the student. It was that nobody had explained to the family what the bank actually checks on a co-applicant for an education loan in India. This post is that explanation, written down.

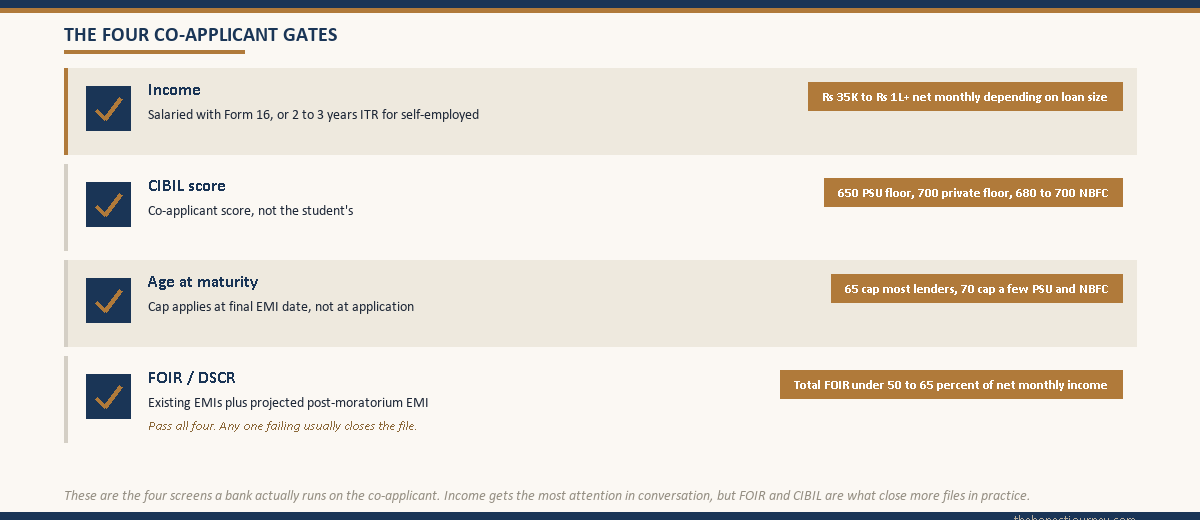

A co-applicant for an education loan in India is a financially liable joint borrower, not just a signature. Banks check the co-applicant’s income (typically ₹25,000 to ₹35,000 per month minimum for unsecured ticket sizes above ₹7.5 lakh), CIBIL score (650+ for PSU banks, 700+ for private banks and most NBFCs), age at loan maturity (usually capped at 65 to 70), and existing EMI load via the FOIR or DSCR calculation. The student’s profile decides whether the loan is considered. The co-applicant’s profile decides whether it is sanctioned.

Who actually qualifies as a co-applicant for an education loan

The IBA model education loan scheme, which most public sector banks follow, defines the co-applicant as a parent, spouse, or in case of married female students, the parent-in-law. The full model scheme text sits on the Indian Banks’ Association site. In practice the list is wider than the model document suggests, but it narrows fast as you move away from the immediate family.

Parent (father or mother). The default. Every PSU bank and private bank accepts a parent as co-applicant without question. If both parents have income, adding the second parent as a third joint applicant is the easiest way to strengthen a thin file. SBI’s education loan documentation on the SBI education loans page explicitly allows this and so does HDFC Credila and Bank of Baroda.

Spouse. Accepted for married students. The bank will ask for the marriage certificate and the spouse’s income proof. If the student is going abroad and the spouse will continue earning in India, this is actually a stronger profile than a retired parent in many cases.

Sibling. Accepted at most PSU banks and several NBFCs if the parent is unavailable, deceased, or has insufficient income. The sibling must be an adult, earning, and willing to sign joint liability. Banks often ask for a written explanation of why the parent is not the co-applicant.

Uncle, aunt, grandparent, or other blood relative. Possible at NBFCs and a few private banks with documentation: relationship proof, sometimes an affidavit, and a satisfactory explanation. PSU banks rarely accept this without escalation to the regional office. If the proposed co-applicant is not a direct relative, expect questions.

Legal guardian. Accepted if formally appointed and documented. Common for orphaned students or students whose parents are NRIs with no Indian income.

Faz's ruleThe bank is not asking who loves you. It is asking who pays if you do not.

This is the mental model that clears up most of the confusion. Joint liability means the co-applicant is on the hook for the EMI from day one of repayment, just as much as the student. The bank’s underwriting question is not “is this person a relative.” It is “if the student does not pay, will this person pay, and can they.” That filters the list of acceptable co-applicants very quickly.

The income criteria banks actually check

The IBA scheme does not specify a minimum income for the co-applicant. The minimum is set by each bank’s internal credit policy, and the number depends on the loan amount, the unsecured versus secured split, and the student’s course economics. The thresholds I see consistently in 2026 are these.

| Loan amount | Minimum co-applicant monthly income (PSU) | Minimum co-applicant monthly income (private/NBFC) | Income proof required |

|---|---|---|---|

| Up to ₹4 lakh | ₹15,000 to ₹20,000 | ₹20,000 to ₹25,000 | Salary slip or ITR |

| ₹4 to 7.5 lakh | ₹20,000 to ₹30,000 | ₹30,000 to ₹40,000 | 3 months salary slip, 2 years ITR |

| ₹7.5 to 20 lakh (unsecured) | ₹30,000 to ₹50,000 | ₹50,000 to ₹75,000 | 6 months salary slip, 2 to 3 years ITR, Form 16 |

| ₹20 lakh and above (secured) | ₹50,000+ plus collateral | ₹75,000 to ₹1,00,000+ plus collateral | 3 years ITR, Form 16, property papers, bank statements |

These are starting points, not hard rules. A weak income can be offset by strong collateral, a clean CIBIL, low existing EMIs, or a high-employability course (top-tier engineering, medicine, or a recognised MBA at a target school). A strong income with messy CIBIL or high existing EMIs can still get refused.

For self-employed co-applicants, the bank averages the net income across the last two to three ITRs and discounts cash-only or volatile income. A small business owner showing ₹5 lakh net income in the latest ITR but ₹2 lakh and ₹3 lakh in the previous two years will be averaged at roughly ₹3.3 lakh, not ₹5 lakh. This trips up a lot of business families.

How banks calculate FOIR or DSCR on the co-applicant

FOIR (Fixed Obligation to Income Ratio) is the percentage of the co-applicant’s monthly income that already goes toward existing EMIs, rent commitments, and other fixed obligations. Most banks cap total FOIR including the new education loan EMI at 50 to 65 percent of net monthly income. DSCR (Debt Service Coverage Ratio) is the inverse framing used more often for self-employed co-applicants, comparing total annual debt servicing to annual net income.

The simple version. Take the co-applicant’s net monthly income. Subtract every existing EMI and committed obligation. The remainder must comfortably cover the projected post-moratorium EMI of the education loan, with cushion. If the co-applicant’s net income is ₹60,000 per month, existing EMIs are ₹20,000, and the projected education loan EMI is ₹18,000, the FOIR sits at (20,000 + 18,000) / 60,000 = 63 percent. That is borderline and many PSU banks will push back.

The capitalised moratorium interest is what makes this calculation trickier than it looks. On a ₹25 lakh loan at 10.5 percent with a 4-year moratorium, the principal at EMI start grows to roughly ₹35 lakh, and the post-moratorium EMI on a 10-year tenure is around ₹47,000 per month. If the bank uses the post-moratorium EMI for FOIR calculation (most do), the co-applicant needs net monthly income of at least ₹80,000 to ₹90,000 to stay under a 55 percent FOIR with no other major obligations. I have a longer breakdown of why this matters in the education loan India complete guide.

Faz's ruleFOIR is where good income and bad timing collide.

I have seen co-applicants with ₹1 lakh monthly income get refused because they had a recent home loan EMI of ₹45,000 and a car loan of ₹12,000 running. The bank looked at the FOIR with the proposed education loan EMI and said no. Income alone does not save you. Free cash flow after existing obligations is what the bank actually lends against.

CIBIL score thresholds for co-applicants in 2026

The co-applicant’s CIBIL score matters more than the student’s score for education loans, because the student typically has no credit history. CIBIL maintains the standard score range of 300 to 900, with 750+ considered excellent. Banks use the co-applicant’s score as a primary signal of repayment intent. The free CIBIL report check sits at cibil.com and you should pull it before applying, not after.

The thresholds I see consistently applied across lenders in 2026.

| Lender type | Minimum CIBIL | Comfortable CIBIL | What happens below minimum |

|---|---|---|---|

| PSU bank (SBI, BoB, Canara, PNB) | 650 | 720+ | Branch can escalate to regional office with justification, or ask for collateral |

| Private bank (HDFC, ICICI, Axis) | 700 | 750+ | Typically refused at credit team level, hard to escalate |

| NBFC (Credila, Avanse, Auxilo, InCred) | 680 to 700 | 740+ | Higher rate offered (12 to 14 percent vs 11 to 12 percent), or refused |

Below 600 the application is effectively closed at most lenders for unsecured exposure. The honest path then is either fixing the CIBIL (closing dispute accounts, settling defaults, waiting 12 to 18 months for old delinquencies to age) or switching to a different co-applicant. The CIBIL score education loan post walks through the repair process in detail.

Recent settlements (the “Settled” status on a CIBIL report) hurt more than people realise. A settled credit card from three years ago can knock a co-applicant out of contention for unsecured education loan exposure above ₹7.5 lakh, even if the current score is 720. The bank’s underwriter sees “Settled” and reads it as “did not pay in full.” Sometimes a written explanation and the closure letter from the earlier lender helps. Sometimes it does not.

Age limits and the moratorium math

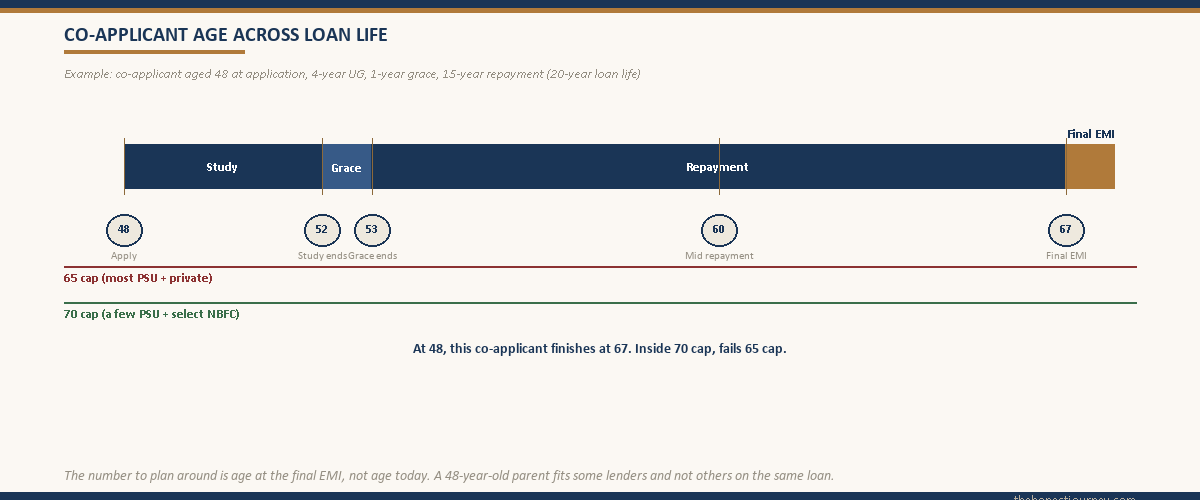

Banks cap the co-applicant’s age at loan maturity, not at application. The cap is typically 65 or 70 depending on the lender. The reason is straightforward. The bank wants the co-applicant to be earning, or to have realisable assets, throughout the loan tenure including the post-moratorium repayment years.

The arithmetic matters more than the headline number. Take a 4-year undergraduate degree, 12-month grace, 15-year repayment tenure. Total loan life from disbursement to final EMI is 20 years. If the bank caps co-applicant age at 65 at maturity, the co-applicant must be 45 or younger at application. For a parent of a 17 or 18-year-old undergraduate student, this is usually fine. For a parent of a 24-year-old applying for a 3-year PG abroad with a 10-year repayment plan, total loan life is 14 years, so the co-applicant can be up to 56 at application against a 70-year cap.

For retired co-applicants the bank looks at pension income, rental income, and investment income, not just age. A retired government employee with a ₹50,000 monthly pension and a clean CIBIL can still qualify, though the bank may shorten the tenure or ask for collateral. A retired private sector employee with only investment income but no regular pension faces tougher questions.

What disqualifies a co-applicant outright

Some flags close the file regardless of income or relationship. Knowing them upfront saves weeks of back-and-forth.

Active default or write-off on CIBIL. Any current “Default,” “Doubtful,” “Loss,” or “Write-off” tag on the co-applicant’s CIBIL report is a near-certain rejection. Closed and settled accounts can sometimes be explained. Active defaults cannot.

NPA classification on any existing loan. If the co-applicant has any loan currently classified as a Non-Performing Asset under RBI guidelines (90+ days overdue), no bank will sanction a new loan, education or otherwise. RBI’s prudential norms are documented on the RBI site.

Pending legal cases on financial matters. Active suits filed by a bank or financial institution against the co-applicant for recovery, cheque bounce cases under Section 138, or income tax prosecution. The bank’s legal review will flag these.

Bankruptcy or insolvency proceedings. Self-explanatory. Co-applicant cannot be undergoing or recently emerged from IBC proceedings.

Income that cannot be documented. Cash-only income with no ITR history, unreported rental income, or business income shown only in personal bank statements with no proprietorship or partnership filings. Banks need ITRs, Form 16, salary slips, or audited financials. Anything else is treated as zero income for FOIR purposes.

Co-applicant who is themselves the guarantor or co-applicant on another large existing loan that is borderline. If your mother has already co-signed your sibling’s education loan and that loan is performing but not stellar, she may be excluded as co-applicant on yours. Banks check joint exposure.

PSU bank vs NBFC: what changes for the co-applicant

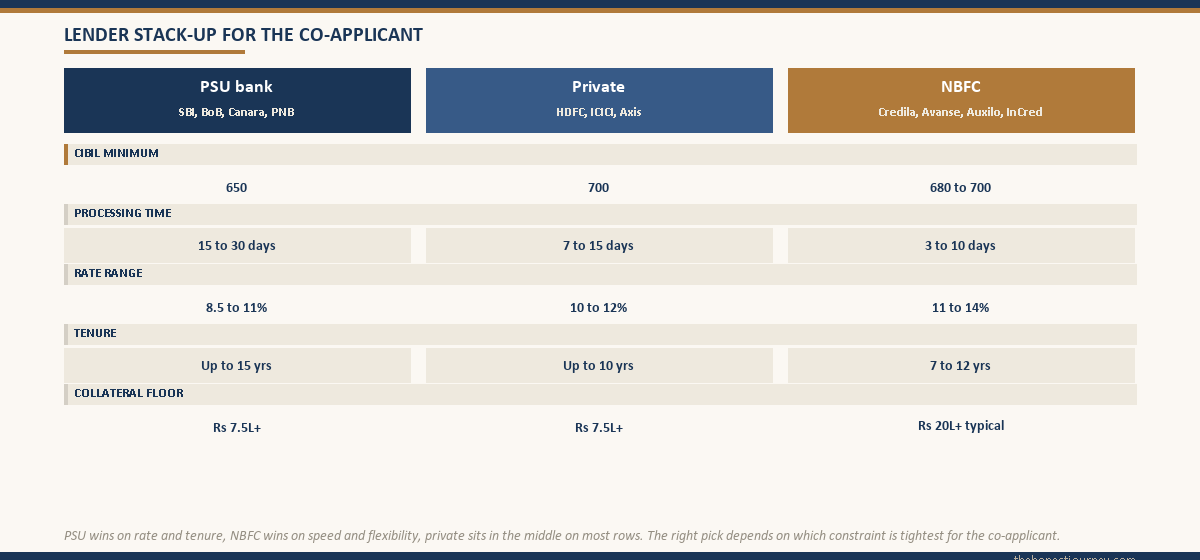

The choice of lender changes what the bank looks for. PSU banks follow the IBA model scheme closely and tend to be stricter on documentation but more flexible on CIBIL thresholds (650 vs 700) and rates (8.5 to 11 percent vs 11 to 14 percent). NBFCs are more flexible on co-applicant relationship (a wider range of relatives accepted) and faster on processing, but compensate with higher rates and tighter CIBIL cutoffs.

Key differences for the co-applicant.

PSU banks. Insist on parent or spouse where possible. Strict on income documentation (last 2 to 3 years ITR mandatory for amounts above ₹4 lakh). CIBIL threshold typically 650. Tenure up to 15 years per IBA scheme. Lower rates. Slower processing (15 to 30 days typical). Often require collateral for amounts above ₹7.5 lakh, though the unsecured ceiling is being relaxed at SBI for IBA-approved courses.

Private banks. CIBIL threshold typically 700 to 720. Strict income proof. Faster processing than PSU (7 to 15 days). Rates 10 to 12 percent. Tenure usually up to 10 years.

NBFCs (HDFC Credila, Avanse, Auxilo, InCred, others). CIBIL threshold 680 to 720. Wider relationship acceptance (uncle, aunt with documentation more often allowed). Fastest processing (3 to 10 days). Rates 11 to 14 percent. Tenure 7 to 12 years typically. Useful when PSU has refused for relationship or marginal CIBIL reasons. The trade-off is total cost.

For students without a viable co-applicant at all, the education loan without co-applicant post covers the narrow set of NBFC products that lend on the student’s own profile, the merit and target-institute conditions, and the rate premium that applies.

Common fixes when the co-applicant profile is borderline

Before resubmitting with a different co-applicant or switching lenders, there are several practical moves that strengthen a borderline file.

Add a second co-applicant. Most PSU banks accept both parents as joint co-applicants. Combined income, combined repayment capacity, both CIBIL scores in the assessment. If one parent’s income is thin and the other has any documented income (even ₹15,000 to ₹20,000 monthly), adding them often gets the file over the line.

Reduce existing EMIs before applying. If the co-applicant has a personal loan or car loan that can be prepaid in part or full, doing it before the application improves FOIR meaningfully. A ₹15,000 EMI prepaid frees that whole amount in the FOIR calculation.

Offer collateral to reduce the unsecured portion. A fixed deposit, an LIC policy with surrender value, or property pledged against the loan reduces the unsecured exposure and lowers the income threshold the bank applies. This shifts the conversation from “your income is thin” to “we have security.”

Reduce the loan ask. If the ask is ₹25 lakh and the co-applicant profile fits ₹18 lakh, take ₹18 lakh and fund the difference via family savings, a part-time job during studies, or a top-up applied for later once income starts. Banks rarely volunteer this option but will accept a lower ask without re-running the whole process.

Pull the CIBIL report and clean up errors. Roughly one in five reports I have seen has a stale account marked as active, a closed loan still showing balance, or a paid credit card showing overdue. CIBIL has a dispute mechanism and corrections take 30 to 45 days. A clean-up can move a score 20 to 50 points.

Switch lender, not file. If a PSU bank has refused on relationship or borderline CIBIL grounds, the same file at an NBFC with a different relationship policy or a slightly lower CIBIL cutoff can sanction. The rate premium is real, but a sanctioned loan at 13 percent beats a refused loan at 10.5 percent.

The honest closing take

The co-applicant is the centre of gravity for an Indian education loan. The student’s profile (course, institute, future earning potential) is the lens through which the bank looks at the file, but the co-applicant’s income, CIBIL, age, and FOIR are what actually decide whether the loan moves to sanction. Treating the co-applicant choice as a formality is the single most common reason families spend weeks watching an application sit “under review” with no clear answer.

Before you submit, pull the co-applicant’s CIBIL, list out every existing EMI honestly, calculate the rough FOIR against the projected post-moratorium EMI of the loan you are asking for, and compare against the lender’s published thresholds. If the math is tight, fix the file (add a second co-applicant, prepay an EMI, offer collateral, lower the ask) before you submit. Fixing it after a refusal is harder, slower, and the rejection itself sits on the CIBIL pull as a hard inquiry for two years.

For the broader documentation checklist that the co-applicant has to bring to the application, the documents required for education loan post goes through every item. The two posts together cover what the bank is looking at on the co-applicant side, end to end.

Faz's ruleThe co-applicant is not a formality. The co-applicant is the loan.

Banks lend against the co-applicant’s ability to repay, dressed up as a loan for the student’s future. Once you internalise that, the entire process makes sense. Choosing the right co-applicant, fixing the file before submitting, and being honest about FOIR are the three moves that determine whether the loan sanctions or sits in limbo.

FAQ

Who can be a co-applicant for an education loan in India?

The IBA model scheme allows a parent, spouse, or parent-in-law (for married female students). In practice most PSU and private banks also accept siblings if the parent is unavailable or has insufficient income, and NBFCs often accept uncles, aunts, grandparents, and legal guardians with documented relationship proof and a written explanation. The further the relationship from the immediate family, the more likely the bank is to ask for additional documentation, an affidavit, or escalation to a regional credit team. A non-relative cannot be a co-applicant on an Indian education loan.

What is the minimum income for a co-applicant on an education loan?

There is no IBA-mandated minimum. Each bank sets thresholds based on loan amount. For unsecured loans up to ₹4 lakh, most PSU banks accept ₹15,000 to ₹20,000 monthly. For ₹4 to 7.5 lakh, the floor moves to ₹20,000 to ₹30,000. For ₹7.5 to 20 lakh unsecured, expect ₹30,000 to ₹50,000 minimum at PSU banks and ₹50,000 to ₹75,000 at private banks and NBFCs. Above ₹20 lakh, collateral is usually required and the income threshold rises accordingly. Self-employed income is averaged across the last 2 to 3 ITRs.

Can a sibling be a co-applicant for an education loan?

Yes, at most PSU banks and several NBFCs, with conditions. The sibling must be an adult with documented income, a satisfactory CIBIL score, and acceptable FOIR. Banks typically ask for a written explanation of why the parent is not the primary co-applicant (parent deceased, retired with no pension, NRI with no Indian income, or insufficient income). Sibling co-applicants work best when the sibling is salaried with stable employment for 2+ years and clean credit history. Marriage certificates are not required for sibling relationship, but birth certificate or family ration card proof is usually asked for.

Does the co-applicant’s CIBIL score matter for an education loan?

Yes, significantly. The co-applicant’s CIBIL score is typically the primary credit signal in the bank’s underwriting because the student usually has no credit history. PSU banks generally accept 650+, with 720+ being comfortable. Private banks typically need 700+. NBFCs need 680 to 700 minimum and may charge a higher rate (12 to 14 percent vs 11 percent) if the score is borderline. Active defaults, settled accounts, or NPA tags on the co-applicant’s CIBIL usually result in outright refusal regardless of current score. Pull the report at cibil.com before applying.

Can I change the co-applicant on an education loan later?

Substituting the co-applicant after disbursement is technically possible but operationally difficult. It requires a fresh sanction process: the new co-applicant submits full documentation, the bank re-runs underwriting, and the original co-applicant is released only after the new one is approved and the loan is technically re-sanctioned. Most banks treat this as a closure and fresh disbursement. The more common (and easier) move is adding a second co-applicant during the loan life, which strengthens the file without releasing the original. Both routes require formal application and bank approval.

What if my parent has a low CIBIL score for the education loan?

Several options. First, pull the report and look for errors (closed accounts showing as active, paid loans with stale balances). CIBIL has a dispute mechanism that can lift a score 20 to 50 points in 30 to 45 days. Second, add the other parent or a sibling as a second co-applicant if their CIBIL is cleaner. Third, offer collateral to reduce the unsecured exposure, which makes lenders less score-sensitive. Fourth, approach an NBFC with a lower CIBIL cutoff, accepting a higher rate. Fifth, if the score reflects a real past default, allow 12 to 18 months of clean repayment on existing loans before reapplying.

Is the co-applicant liable to repay the education loan if the student defaults?

Yes, fully. Co-applicants on Indian education loans sign joint liability, which means they are legally on the hook for the entire outstanding amount, EMIs, and any penalties or interest from the day the loan is disbursed. If the student does not pay, the bank can recover from the co-applicant via salary attachment, lien on assets, or legal action under the SARFAESI Act for secured loans above ₹1 lakh. This is why banks underwrite the co-applicant’s profile so carefully. The student’s signature is on the loan, but the co-applicant carries the same legal weight.

Can I take an education loan without a co-applicant in India?

For most loans above ₹4 lakh, no. PSU banks following the IBA scheme require a co-applicant for any loan above ₹4 lakh, and below that for non-collateralised exposure. A handful of NBFCs (Prodigy Finance, MPower Financing, and select others for premier-institute admits) offer education loans on the student’s own profile without an Indian co-applicant, but these are typically restricted to top-tier overseas universities and STEM or MBA courses with strong employment outcomes. The rate is meaningfully higher (12 to 16 percent), there is usually no collateral but tight institution and course conditions apply, and the loan is sanctioned in foreign currency for overseas study.

Faz · The Honest Journey · 2026