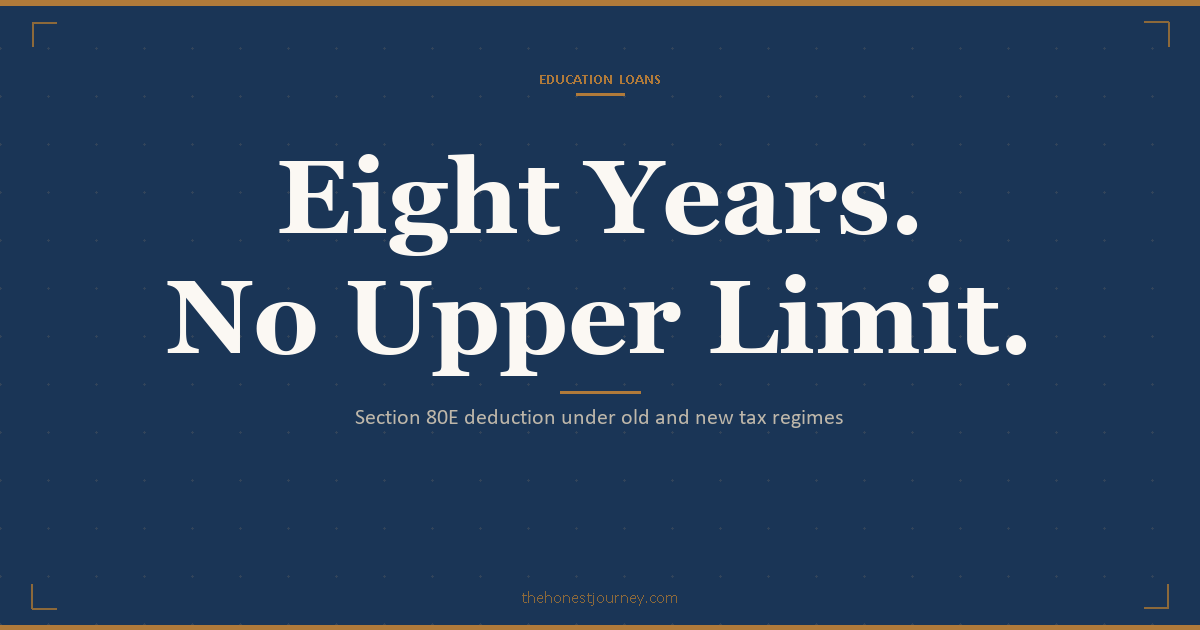

I’ll be direct: you can only claim Section 80E in the Old Tax Regime, never the New. It deducts education loan interest with no upper cap, for up to 8 assessment years from when you start paying. One family I know lost roughly ₹1.3L in relief on a ₹38L loan simply by filing under the New Regime. Decide the regime first.

A friend’s father called me last March, two weeks before the ITR deadline. His son had been paying EMI on a ₹38L education loan for a year, and a chartered accountant friend at a barbecue had told him “claim 80E and you’ll get back at least a lakh.” The father had filed under the New Tax Regime (default, lower headline rates, looked attractive). He wanted to know how to add the 80E deduction now.

The honest answer was: you can’t. Not in the New Regime. He had already filed. The 80E claim worth roughly ₹1.3L in tax relief was gone for that year. Not because the loan was wrong. Not because the interest wasn’t paid. Because of one regime checkbox most people tick without understanding what it switches off.

This post is the thing I wish someone had told that family before they filed. Section 80E, who actually claims it, the real math on a typical ₹40L abroad-studies loan, and the regime decision that has to happen first. Three scenarios across three different families. No “consult your CA” hand-wave.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The 60-second answer

Section 80E is a deduction on the interest paid on an education loan, with no upper cap on the amount. It only applies in the Old Tax Regime. In the New Tax Regime (the default since FY2023-24, and made even more attractive in Budget 2025 with higher rebates and flatter slabs), 80E is unavailable. You can claim 80E for a maximum of 8 assessment years from the year you start paying interest, or until the interest is fully paid, whichever is earlier. The deduction goes to whoever is the primary borrower on the loan (parent or student, not both). Foreign education loans qualify. Principal repayment does not.

What Section 80E actually covers, and what it doesn’t

Section 80E of the Income Tax Act, 1961 (full text on the income tax department site) allows a deduction on interest paid on a loan taken for higher education. “Higher education” here is broad: any course pursued after passing the Senior Secondary Examination, from any school, board, or university recognised by the central or state government, or a local authority. That includes UG, PG, vocational, professional courses, and crucially, studies abroad. The income tax act does not restrict the course location to India.

Three things 80E does not cover that people routinely get wrong:

- Principal repayment. Section 80E is interest-only. The principal you pay back gets no deduction. There is no 80C-style benefit for education loan principal.

- Loans from informal lenders. The loan must be from a scheduled bank, notified financial institution, or an approved charitable institution. Loans from relatives, friends, employer, or unregulated NBFCs do not qualify. Most major NBFCs (HDFC Credila, Avanse, Auxilo, InCred) are notified and qualify; double-check the lender’s status before assuming.

- Tuition fees paid directly without a loan. 80E is tied to a loan. If you paid the fees from savings, there is no 80E to claim. (That cash payment doesn’t get a 80C deduction either; tuition fees under 80C apply only to school-stage tuition for up to two children, not higher education.)

The deduction window runs for 8 consecutive assessment years, starting from the year you begin repaying interest, or until the interest is fully repaid, whichever comes first. The 8 years count from the first year of interest payment, not from when the course ends. If your loan has a moratorium and you start paying interest in 2027, your 8-year window is FY2027-28 through FY2034-35.

The regime decision, with real numbers

Here is the calculation that should happen before anyone files. A 23-year-old engineer’s father, salaried, ₹26 LPA gross. Son took a ₹40L education loan for a UK MS at 11% (typical no-collateral rate from a Credila / Avanse-style lender, see my no-collateral loan post for the rate landscape). Loan tenure 10 years, 1-year moratorium, repayment started April 2025.

Faz's rule

Section 80E only works in the Old Tax Regime.

The New Regime, default since 2023-24 and sweetened in Budget 2025, doesn’t allow the 80E deduction. Most families tick the regime checkbox without realising what they’re switching off.

Faz's rule

Eighty percent of households claiming 80E should be on the Old Regime. The other twenty percent are giving up cash by claiming it.

The break-even is decided by total deductions, not by 80E in isolation. Run both filings side by side once a year; do not assume.

Year 1 interest paid: approximately ₹4,38,000. (₹40L principal × 11% for the bulk of the year, slightly less than a flat 11% because of small principal reductions in the back half.)

In the Old Regime, with 80E:

– Tax slab at ₹26L: 30% marginal.

– 80E deduction: ₹4,38,000 (full interest, no cap).

– Tax saved Year 1: ₹4,38,000 × 30% = ₹1,31,400.

– Add 4% cess: total tax saved ≈ ₹1,36,656.

In the New Regime, no 80E:

– Tax saved Year 1: ₹0.

But the New Regime has lower headline rates. So the comparison is not 80E vs nothing; it is (Old Regime rate + 80E + other deductions) vs (New Regime lower rate + nothing). Let me run the full comparison on this father’s ₹26L gross.

Old Regime (FY2025-26 slabs):

– Gross: ₹26,00,000

– Standard deduction: ₹50,000

– 80C (PF + insurance + ELSS): ₹1,50,000

– 80D (health insurance): ₹25,000

– 80E (education loan interest): ₹4,38,000

– HRA exemption (assume): ₹2,40,000

– Taxable: ₹16,97,000

– Tax (Old slabs): ₹3,21,600 + cess = ₹3,34,464

New Regime (FY2025-26 slabs, post Budget 2025):

– Gross: ₹26,00,000

– Standard deduction: ₹75,000

– No 80C, 80D, 80E, HRA

– Taxable: ₹25,25,000

– Tax (New slabs): ₹3,07,500 + cess = ₹3,19,800

For this profile, Old Regime saves ₹14,664 over New Regime. The 80E deduction is doing heavy lifting; without it, New Regime would win by about ₹1.2L. The verdict: 80E often tips the regime decision in favour of Old, but only when other Old-regime deductions (HRA, 80C, home loan interest) are also stacked up. If the parent doesn’t have HRA, doesn’t have a home loan, and 80C is half-empty, the New Regime can still win even with 80E available.

This is the math that gets skipped. Run it on your actual numbers before checking the regime box in the employer’s investment declaration in April. Use the income tax department’s tax calculator on the e-filing portal for your exact figures. ClearTax also has a the Income Tax Department’s portal for cross-reference.

Total 80E benefit over the 8-year deduction window

Interest paid declines each year as principal reduces. On a ₹40L loan @ 11% over 10 years, the rough interest-paid schedule:

- Year 1: ₹4,38,000

- Year 2: ₹4,06,000

- Year 3: ₹3,70,000

- Year 4: ₹3,30,000

- Year 5: ₹2,86,000

- Year 6: ₹2,37,000

- Year 7: ₹1,83,000

- Year 8: ₹1,22,000

Total interest paid in years 1-8: approximately ₹23,72,000.

At 30% slab: tax saved over 8 years ≈ ₹7,11,600 (plus cess, ≈ ₹7.4L).

At 20% slab: tax saved over 8 years ≈ ₹4,74,400 (plus cess, ≈ ₹4.93L).

Years 9 and 10 of the loan have interest paid but no 80E claim available (window expired). That’s roughly ₹65,000 of interest in years 9-10 that gets no deduction. Plan for it, and if cash allows, our note on whether to prepay an education loan covers the trade-off of closing the loan inside the deduction window.

Who in the family should claim, and why this is the single most-botched detail

80E goes to the person who took the loan and is paying the interest from their taxed income. Not “the family.” Not “whoever has the higher tax slab.” The primary borrower on the loan agreement.

Faz's rule

80E follows the primary borrower, not the household.

Parent in 30% slab as primary saves the household ₹6-8L over the 8-year window. Student as primary with early-career 10% slab saves ₹2-4L. Get the borrower-name decision right at sanction stage, it’s hard to change post-disbursement.

Faz's rule

The wrong family member claiming 80E can erase the entire benefit. Whoever is on the loan is the only one who can claim. This is decided at sanction, not at filing.

If the parent will be paying the EMI but the loan is in the student’s name, the parent cannot claim. Restructure at sanction, not later.

Three sub-cases I see constantly:

Case A: Loan is in the parent’s name, student is co-borrower or just the “beneficiary.” Parent claims 80E. Even if the student later gets a job and “helps repay,” the deduction belongs to the parent. The student cannot claim.

Case B: Loan is in the student’s name, parent is co-applicant for income/collateral. Student claims 80E. Once the student starts earning, the deduction reduces their tax. The parent, despite being the co-applicant who actually signed the cheques during moratorium, cannot claim. This trips up families regularly.

Case C: Loan is in the student’s name, but parents are paying the EMI from their account during the student’s foreign studies. Technically, only the borrower (student) can claim, and only if the interest is paid from income chargeable to tax in the student’s hands. If the student has no Indian income, there is nothing to deduct against, and the 80E benefit is effectively wasted that year. The parent paying from their account does not get to claim either, because they are not the borrower.

The planning move that matters at loan application stage: if the parent is salaried, in a 30% slab, and intends to repay the loan from their post-tax income anyway, take the loan in the parent’s name with the student as co-applicant. The maximum tax benefit accrues to the household. This needs to be discussed with the lender at the documentation stage (see my documents required post). Once the loan is sanctioned, the borrower’s name is hard to change.

A counter-case where student-as-primary makes sense: if the parent is retiring within 2-3 years (no more salary income to deduct against), or if the parent is already in the New Regime by choice for other reasons (very low deductions otherwise), then the deduction is better preserved for the student who will start earning soon.

Three real-numbers scenarios

Scenario 1: The household where 80E paid off cleanly

Profile: Father, age 52, IT manager in Hyderabad, ₹32 LPA gross, has HRA (rents in Hyderabad while owning a house in Vijayawada), maxes 80C, has 80D for parents. Son did MS at a US public university, ₹50L loan from SBI at 9.65% (collateralised against the Vijayawada house). Father is primary borrower.

Year 1 interest: ₹4,82,500. 80E deduction at 30% slab saves ₹1,44,750 (plus cess ≈ ₹1,50,540).

Stacked with HRA + 80C + 80D, Old Regime tax bill is ₹2.8L lower than New Regime would have been. Over 8 years, total 80E benefit alone is roughly ₹8.4L. Father chose Old Regime cleanly. Son graduated, returned to India in 2024, took a ₹22 LPA job, and now repays a chunk of the EMI from his own account into the father’s loan account (no tax implication; he is not the borrower so he does not claim, but he reduces the household burden). Clean win.

Scenario 2: The household where 80E barely mattered

Profile: Mother, age 47, central-government clerk, ₹9.5 LPA gross, no HRA (lives in govt quarters), modest 80C of ₹80K. Daughter did a 2-year MA in Ireland, ₹18L loan from Avanse at 12.5%, mother as primary borrower.

Year 1 interest: ₹2,16,000. At 20% slab, tax saved is ₹43,200. Add cess: ₹44,928.

Old vs New Regime for this profile (after deductions): Old saves about ₹38,000/year vs New. 80E contributes the bulk of that. Over 8 years, total 80E benefit is roughly ₹2.9L, mostly worth-it but not life-changing. The household budgeted assuming zero tax benefit and treated the ₹40-45K/year as found money. The daughter, now working in Dublin and not an Indian tax resident, can’t claim anything herself even after she starts repaying. Fine outcome; nobody was depending on the deduction to make the loan affordable in the first place.

Scenario 3: The household where 80E became a footnote on a much bigger problem

Profile: Father, age 56, retired PSU officer, ₹6 LPA pension. Son took a ₹65L loan in his own name (father retired and didn’t qualify as primary borrower) for a US MS, lender Credila at 11.75%. Course finished 2023, son got placed at a low-tier US employer at $58K, lost the job in mid-2024, returned to India in early 2025, currently job-hunting at ₹12 LPA target.

Year 1 interest after moratorium: ₹7,15,000. Son is the borrower. Son has no Indian income for FY2024-25 (was abroad most of year). 80E is technically available to him but with no taxable income, the deduction is dead weight. Father is not the borrower so cannot claim. The deduction worth ₹2L+ at face value generates ₹0 of actual tax relief that year.

This isn’t an 80E failure; the loan was structurally wrong for the household’s income profile from day one. But it illustrates the rule: 80E is only worth what the borrower’s marginal tax rate makes it worth in the year the interest is paid. Defer the analysis to year 8 and you may discover the entire deduction window passed with the borrower in tax-zero territory.

The 7-question decision framework

Run these in order. If you can’t answer “yes” or “doesn’t matter” to all, the 80E planning isn’t done yet.

- Have I picked the regime deliberately? Run the Old vs New comparison on actual numbers using the e-filing portal calculator, not on vibes. New Regime kills 80E. Default isn’t a decision.

- Is the loan from a notified lender? Scheduled bank or notified financial institution. Confirm before assuming. Loans from relatives, employers, or unregulated lenders don’t qualify.

- Is the primary borrower the person with the higher marginal slab and ongoing taxable income? If parent at 30% slab is paying anyway, make them the primary borrower at sanction stage, not after, and read up on co-applicant rules before you finalise whose name goes where.

- Will the primary borrower have taxable income through the 8-year window? If they retire in year 3, the deduction dies with their tax liability.

- Does the household have enough other Old-Regime deductions (HRA, 80C, home loan interest, 80D) for Old Regime to win once 80E is added? Sometimes New still wins even with 80E.

- Am I tracking the interest-paid certificate from the lender every March? You need Form 26AS reconciliation and a lender-issued interest certificate to claim.

- Do I have a plan for years 9 and 10 (or beyond) when the 8-year window has expired? The interest still gets paid; just no deduction.

Profile correlation: which households actually win on 80E

Maximum benefit:

– One parent in 30% slab, salaried, with the loan in their name.

– Old Regime makes sense anyway because of HRA + 80C + home loan stacking.

– Loan tenure of 8-10 years (matches the deduction window).

– Indian-resident borrower throughout.

Moderate benefit:

– Parent at 20% slab, loan in their name.

– Most other Old Regime deductions thin but present.

– Net Old-vs-New gap is small but positive.

Marginal or zero benefit:

– Student is the primary borrower, but spends most of repayment years abroad with no Indian taxable income.

– Parent is the primary borrower but retires within 2-3 years of repayment starting.

– Both parents are in the New Regime by choice because their other deductions are too thin to justify Old.

Course-specific note: For high-tuition Indian courses, the regime decision is sharper because the interest amounts are larger and the 80E deduction is bigger in absolute terms. A ₹50L MBA loan at a top IIM at 9.5% generates roughly ₹4.75L of year-1 interest, worth ₹1.42L of tax saved at 30% slab. A ₹80L private MBBS loan at 11% generates ₹8.8L of year-1 interest, worth ₹2.64L of tax saved at 30% slab. In both cases, the regime decision is best made jointly with whoever in the household has the higher slab, since the deduction follows the borrower.

Don’t optimise for 80E if any of these apply

- You’re choosing between a needed loan and no loan. 80E is a discount on a cost; it does not make a bad loan good. If the EMI math doesn’t work on a 0%-benefit basis, the loan doesn’t work.

- The borrower’s income is volatile or about to drop. No income, no tax, no deduction. The full face value of 80E is a fiction in those years.

- You’re picking a more expensive lender for an irrelevant reason like loyalty or marketing, and using “but I’ll save tax” to justify it. The interest you don’t pay beats the interest you deduct, every time, which is exactly why our bank vs NBFC interest rate comparison should come before any tax planning.

- The course or institution doesn’t qualify for the loan in the first place. Some lenders won’t fund certain abroad colleges. Solve eligibility before tax planning.

- You’re a parent considering taking the loan in your name purely for the deduction, but you don’t actually intend to repay from your income. The deduction follows the cheque; structurally misrepresenting this can cause issues at tax assessment.

How to claim 80E in your ITR

The mechanics are simple once the structural decisions above are right. Four steps, in order.

- Get the interest certificate from your lender. Ask your bank or NBFC for the education loan interest certificate for the financial year. Most issue it in March or April. It shows the interest paid during the year, which is the only figure that matters for 80E. If the lender gives a combined principal and interest certificate, use the interest line alone, since principal repayment gets no deduction.

- Opt into the Old Regime first. 80E only works in the Old Tax Regime, so this has to be your selected regime before anything else. Ideally you also flagged Old Regime in the investment declaration you gave your employer in April, to avoid a TDS mismatch at filing time. If you let the New Regime stay as the default, there is no 80E field to fill.

- Enter the interest under the 80E deduction. In the return, the interest amount goes into the Chapter VI-A deductions, in the row for Section 80E (interest on loan for higher education). It reduces your gross total income with no upper cap, so the full interest you paid that year is deductible. You do not attach the certificate to the ITR; keep it on file and be ready to produce it if the return is picked for scrutiny. The figure should reconcile with your loan account statement.

- Repeat each year, within the 8-year window. You can claim for a maximum of 8 consecutive assessment years from the year you start paying interest, or until the interest is fully repaid, whichever comes first. Pull a fresh interest certificate every year and claim again. Once the window closes, the interest still gets paid but the deduction is no longer available.

The honest close

Section 80E is a useful, fair deduction that the government left uncapped on purpose. It can return ₹1.3-1.5L per year to the right household in the right regime for 8 years. Or it can return ₹0 if any of three things go wrong: wrong regime, wrong borrower, wrong income year.

Faz's rule

If your total interest deduction will be less than one lakh per year, the Old Regime cost may exceed the 80E benefit. Run both regimes before you opt in.

80E is a benefit, not a destination. Optimise the whole tax bill, not the deduction in isolation.

The article you read on a lender’s blog won’t run your numbers. Your CA might, if you ask the right question (which is “what’s the Old vs New regime delta for me, including 80E?” not “should I claim 80E?”). The decision belongs to you and the household members whose names go on the loan papers. Whatever you decide, decide it before you tick the regime checkbox at the start of the financial year, not at filing time when most options are already gone.

Frequently asked questions

Is 80E available in the New Tax Regime?

No. Section 80E is one of the deductions disallowed under the New Tax Regime. Since FY2023-24, the New Regime is the default, and Budget 2025 further sweetened it with higher rebates and revised slabs. To claim 80E, you must actively opt into the Old Tax Regime when filing (and ideally also when submitting your investment declaration to your employer at the start of the year, to avoid TDS mismatch).

Can parents claim 80E for an education loan taken in the child’s name?

No. The deduction goes to the primary borrower on the loan, not to whoever pays the EMI. If the loan is in the student’s name and the parent is only a co-applicant, the parent cannot claim 80E even if they are paying every rupee. This is why the borrower-naming decision at sanction stage matters more than people realise. Get this right when the loan is being structured, not after.

Is there any upper limit on the 80E deduction amount?

No. 80E has no upper cap on the deduction. Whatever interest you pay on an eligible education loan in a financial year is fully deductible from your gross total income. This is unusual; most income tax deductions have a cap (80C is ₹1.5L, 80D is ₹25-75K). The 80E uncapped design is deliberate, intended to make higher education loans more affordable. Principal repayment, however, gets no deduction at all.

Can I claim 80E for a foreign education loan?

Yes. 80E covers loans for higher education pursued anywhere, not just in India. UG and PG abroad both qualify, provided the loan is from a notified Indian lender (scheduled bank or approved financial institution). Loans from foreign lenders like Prodigy Finance or MPOWER Financing do not qualify because they are not notified Indian financial institutions. If you’re considering those USD-denominated loans, factor the lost 80E benefit into the comparison. And if you plan to work overseas after graduating, read up on how the DTAA protects Indian students abroad from being taxed twice on the same income.

For how many years can I claim 80E?

For a maximum of 8 consecutive assessment years from the year you start paying interest, or until the interest is fully repaid, whichever is earlier. The 8-year count starts from the first year of interest payment, including any interest paid during the moratorium if you chose to service it. If your loan tenure is 10 years, you get the deduction for years 1-8; years 9 and 10 have interest paid but no 80E claim available.

Is principal repayment covered under Section 80E?

No. 80E covers interest only. The principal portion of your EMI gets no deduction under any section. There is no education-loan-principal equivalent of the 80C home loan principal deduction. Plan your math on this basis: of a typical EMI in the early years, roughly 30-40% is interest (deductible) and 60-70% is principal (not deductible). The interest portion shrinks each year as the loan amortises, a mechanic we walk through in our guide on how to repay an education loan.

Do I need any specific document to claim 80E?

You need an interest certificate from the lender showing the interest paid during the financial year. Most banks issue this in March-April. Some lenders also issue a combined principal-and-interest certificate; only the interest figure matters for 80E. Keep the certificate on file (don’t submit it with your ITR, but be ready to produce it during scrutiny). The interest figure should reconcile with your loan account statement.

Can a student claim 80E if they’re paying the EMI but the loan is in their parent’s name?

No. The student can pay the parent informally from their post-tax income, but the 80E deduction stays with the parent because the parent is the borrower on the loan. The student gets no tax benefit from such payments. If you anticipate this arrangement, factor it into the borrower-naming decision at the loan application stage. Once the loan is sanctioned, restructuring the borrower’s name is bureaucratically painful and often not allowed.

Faz · The Honest Journey · 2026