An education loan covers tuition and living costs, needs no collateral up to ₹7.5 lakh, and repays in EMIs after a moratorium running through your course plus 6 to 12 months. Rates sit around 8.5% to 10% at public sector banks with collateral, and 11.5% to 14% at NBFCs without. Most offers fail on CIBIL, co-applicant income, and university quality.

An education loan in India is the most under-explained financial product most middle-class families will ever sign. The sanction letter looks like a victory. The relationship manager calls it a benefit. The paperwork uses the word “support.” And then, somewhere between the first disbursement and the first EMI three years later, the actual cost of the thing reveals itself, and the family realises they had been reading the cover page of a much longer document.

I wrote this guide because almost every conversation I have with students and parents about education loans starts in roughly the same place: they know the loan amount, they kind of know the interest rate, and they have almost no idea what happens between those two numbers. This page is the full picture, from eligibility to repayment to what the law actually entitles you to.

An education loan in India is a financing product from a bank or NBFC that covers tuition, living, and related costs, with no collateral required up to ₹7.5 lakh, repayment in EMIs after a moratorium period that runs through your course plus 6 to 12 months, and a tax deduction under Section 80E on the interest you pay. Rates currently sit around 8.5% to 10% at public sector banks with collateral, and 11.5% to 14% at NBFCs without. Most loan offers fall apart on the same three things: CIBIL, co-applicant income, and the quality of the university on the bank’s approved list.

What this guide covers, in order: who actually needs a loan, how much you can borrow and what it really costs, secured versus unsecured options, the CIBIL and eligibility wall, documents, the co-applicant question, loans by course type, government schemes, approval timelines and rejection reasons, the disbursement process, the moratorium and the interest trap, repayment and prepayment, the Section 80E tax angle, insurance and your rights, the abroad-studies specifics, what happens when things go wrong, and the calculators you can use right now.

The loan basics nearby: the education loan EMI calculator math post and the education loan vs personal loan post.

Two government levers can cut the real cost before you even compare lenders: the moratorium interest subsidy under the CSIS scheme, and a fully funded award from our ranked guide to scholarships for Indian students.

Who actually needs an education loan

The honest answer is fewer people than the bank ads suggest, and more than most parents would like to admit. An education loan makes sense in one of three situations. First, the family has the savings to fund the course but the opportunity cost of liquidating them (broken FDs, sold mutual funds at the wrong time, a property mortgage at a worse rate) exceeds the cost of borrowing. Second, the family does not have the savings and the course has a credible payback (a top-ranked MBA, a clinical MBBS, a STEM master’s at a target university with strong placement). Third, the student wants to keep the parents’ retirement corpus intact and treat the loan as a way to pay for their own education out of their future earnings.

The loan does not make sense in two situations that come up just as often. The first is the family treating it as a way to fund a status purchase: a vaguely-ranked overseas master’s chosen for the postcard, not for the placement data, where the post-study salary will not realistically service a ₹30 lakh EMI. The second is the family using a loan to cover a course the student is not committed to, where the dropout risk is real and the bank still wants every rupee back.

Before you walk into any branch, sit with one number: the projected starting monthly take-home after the course, in rupees, in your most likely first job. If your EMI after the moratorium will exceed 35% to 40% of that number, the loan is too big or the course is wrong, not the bank.

How much you can borrow (and what it really costs)

The headline numbers are easy to find. Most lenders cap unsecured education loans at ₹7.5 lakh for domestic studies and ₹40 lakh to ₹75 lakh for abroad studies, with some NBFCs going up to ₹1.5 crore for top-tier universities. With collateral, public sector banks routinely sanction ₹1.5 crore and above. The actual amount you will be offered depends on the course, the university, your co-applicant’s income, and the value of any collateral you bring.

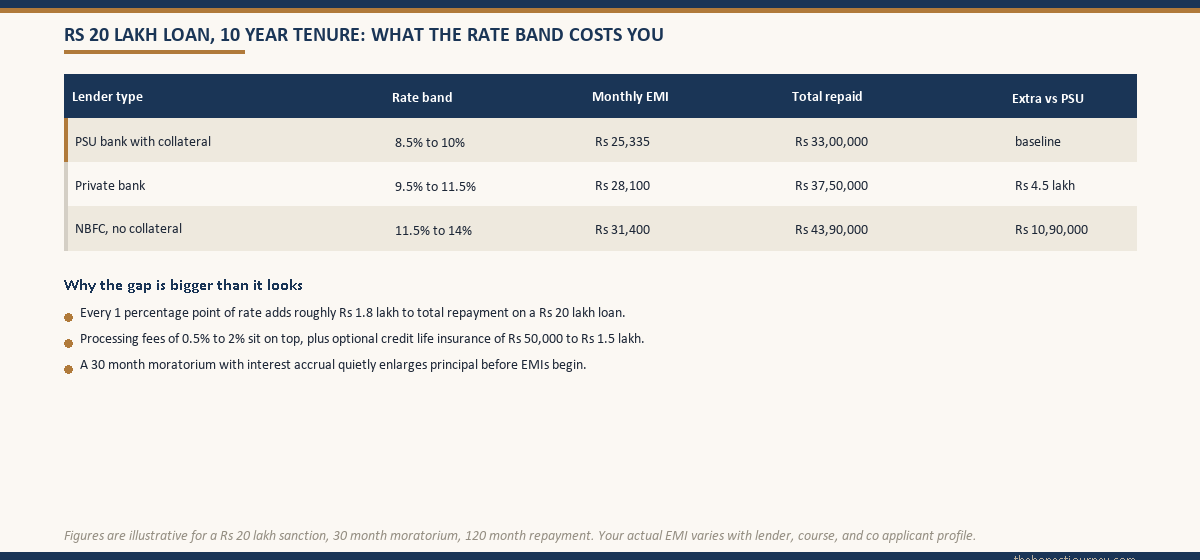

The harder number is the cost. Interest rates in 2026 sit in three rough bands. Public sector banks with collateral, with SBI the largest by volume, are at 8.5% to 10%. Private banks are at 9.5% to 11.5%, depending on the relationship. NBFCs that fund without collateral are at 11.5% to 14%. On a ₹20 lakh loan at 11.5% with a 30-month moratorium and a 10-year repayment, you will repay approximately ₹43.9 lakh in total. On the same loan at 9% from a public sector bank, total repayment drops to roughly ₹33 lakh. The 2.5 percentage points are worth ₹10 lakh over the life of the loan.

Two costs that almost never appear in the sales pitch: processing fees (0.5% to 2% of the sanctioned amount, sometimes capped) and the cost of insurance the lender may bundle in. On a ₹30 lakh loan, a 1% processing fee is ₹30,000, and a credit life policy can add ₹50,000 to ₹1.5 lakh to the principal you eventually pay interest on.

If you want the full details, read Education loan interest rate comparison in India.

Named lender comparison: banks and NBFCs at a glance

Readers always ask for the actual names, so here is the honest version. The table below lists the lenders most of my readers end up shortlisting, with indicative rate ranges and the collateral-free threshold each is known for. Treat every number here as a starting reference, not a quote. Your actual rate depends on the co-applicant’s CIBIL and income, the university, the course, and whether you pledge collateral. If SBI is on your shortlist, our breakdown of how SBI’s overseas education loan works goes deeper into its limits and timelines.

| Lender | Indicative rate range | Collateral-free threshold | Notes |

|---|---|---|---|

| SBI (Global Ed-Vantage) | indicative, ~8.5% to 10.5% | Up to ₹7.5 lakh standard; higher for select institutes | Largest PSU lender by volume. Lowest rates with collateral, longer timeline, the benchmark to beat. |

| Bank of Baroda | indicative, ~8.5% to 11% | Up to ₹7.5 lakh; higher for premier-list institutes | PSU. Sharper rates for students admitted to its list of premier Indian and global institutions. |

| Punjab National Bank | indicative, ~8.5% to 11% | Up to ₹7.5 lakh standard | PSU. Follows the IBA model scheme; rate concessions common for women borrowers. |

| Axis Bank | indicative, ~9.5% to 13% | Up to ₹40 lakh for select profiles and institutes | Private bank. Faster than PSUs, higher collateral-free ceilings for strong profiles. |

| ICICI Bank | indicative, ~9.5% to 13% | Up to ₹50 lakh for premier institutes | Private bank. Quick sanction, higher unsecured limits for top-tier admits. |

| HDFC Credila | indicative, ~11% to 14% | ₹50 lakh to ₹1 crore-plus for premier institutes | NBFC. Fast, collateral-light for strong profiles, at a clear rate premium over PSUs. |

| Avanse | indicative, ~11% to 14% | ₹50 lakh to ₹1 crore-plus for premier institutes | NBFC. Speed and flexibility on university lists, higher rate, common visa-timeline fallback. |

Rates are indicative and change; confirm the current figure on the lender’s official page before you decide. The bands above line up with the picture across this guide: PSU banks with collateral around 8.5% to 10%, private banks roughly 9.5% to 11.5% and higher for unsecured, and NBFCs at 11.5% to 14% for the collateral-light convenience. The cheapest sticker rate is not always the cheapest loan once you price in processing fees, bundled insurance, and the moratorium capitalisation, so run the full number, not the headline. Among the PSUs, it is worth reading the detail on the Bank of Baroda education loan, the Canara Bank education loan, and the PNB education loan, since their premier-institute concessions can beat the table’s indicative bands.

Secured vs unsecured loans

This is the single most consequential choice in the whole process, and most families make it backwards. They walk into the NBFC first because the NBFC sells faster, sanctions in two weeks, and does not ask for property papers, which is exactly how an HDFC Credila education loan wins so many families before they have compared anything. The same pull applies to the other dedicated education-loan NBFCs, like the Auxilo education loan and the InCred education loan, which all sell on speed and a collateral-free pitch. The public sector bank, with its 8.5% rate and 60-day timeline, only gets considered when the visa appointment is six weeks away and the NBFC has already started disbursing.

A secured loan is one where you pledge collateral (typically immovable property, sometimes fixed deposits or LIC policies) for an amount above the unsecured threshold. The rate is lower, the tenure is longer (up to 15 years at most PSBs), and the moratorium math is gentler because the absolute interest accrued is smaller. The downside is the paperwork: valuation, legal opinion, title search, registration of mortgage. It takes time. It also means the property is encumbered until the loan is closed.

An unsecured loan from an NBFC or private bank skips all of that. You get a faster sanction, a cleaner process, no property to pledge, and a much higher rate. For a ₹20 lakh abroad loan, the unsecured route at 12% costs roughly ₹10 lakh more over the tenure than the same loan secured at 9.5%. For some families that premium is worth it because the property is not available to pledge or the timeline does not allow it. For most, it is a default they did not realise they had a choice in, which is why it pays to weigh the PSU bank versus NBFC education loan question deliberately rather than by whoever calls back first.

A middle path that comes up often: an education loan against property taken from a bank that specialises in LAP (loan against property) and uses the proceeds to fund the course. The structure is technically a property loan, not an education loan, which means you lose Section 80E, but the rate can be very competitive.

If you want the full details on the headline tradeoff, read Secured vs unsecured education loan. For the unsecured abroad route specifically, read Education loan for abroad studies without collateral.

The CIBIL and eligibility wall

The bank’s eligibility check has three layers. The first is the student profile: course, university, country, expected outcomes. The second is the co-applicant profile: income, age, existing EMIs, employment stability. The third, and the one that quietly kills the most loan applications, is the CIBIL score of the co-applicant.

Most lenders want a co-applicant CIBIL score of 700 and above. Public sector banks are slightly more flexible at 650 and above for secured loans. NBFCs are more rigid at 720 and above for the better rate cards. A score below 650 does not always mean rejection, but it almost always means a higher rate, a smaller sanction, or a request for additional security. A co-applicant with a recent settled loan, a write-off, or a 90+ day overdue marker on the report will struggle to get the file cleared even if their income is strong.

Faz's rule

Pull the co-applicant's CIBIL report before you start any loan application, not after the first rejection.

A free pull from cibil.com takes ten minutes and shows you exactly what the bank will see. If there is a stale dispute, a settled-not-closed marker, or a wrong overdue entry from a card you cleared years ago, you have time to fix it before the file goes in. Once the bank pulls the report and logs a hard enquiry, the next lender sees that enquiry too.

Income eligibility is the other half. The bank uses a Fixed Obligation to Income Ratio (FOIR), typically capped at 50% to 65%, to decide whether the proposed EMI plus the co-applicant’s existing EMIs will fit inside their take-home. If the co-applicant has an existing home loan EMI of ₹40,000 on a ₹80,000 take-home, the room for a new education loan EMI is small.

For families where the parents do not file ITR (small-business owners, self-employed without proper books, agricultural income), the process is different. Some lenders accept bank statements, GST returns, or land records in lieu of ITR, but the universe of willing lenders shrinks. For the full set of workarounds, read Education loan without ITR. For the CIBIL specifics, read CIBIL score for education loan in India.

Documents you will need

The document list looks long because it is. A typical education loan file has three sections: student documents, co-applicant documents, and course documents. Student documents include identity proof, address proof, passport, all academic mark sheets from Class 10 onwards, the entrance exam scorecard (GRE, GMAT, IELTS, NEET, CAT, depending on the course), and a CV. Co-applicant documents include identity, address, PAN, three years of ITR with computation, six months of bank statements showing salary credit, a Form 16 if salaried, and proof of any existing loans or assets. Course documents include the admission letter, the fee structure on official letterhead, and a year-wise breakup of expected costs.

Two documents catch students out. The first is the gap certificate, required if there is a break of a year or more between your last qualification and the current course. The format is simple but the wording matters. Banks reject loans over poorly drafted gap certificates more often than you would expect. The second, for abroad visa-linked loans, is the sponsorship affidavit, a notarised document the co-applicant signs declaring they will support the student financially. This is a visa requirement, not a bank requirement, but the bank often holds the file until it is in place.

If you want the master checklist with formats, read Documents required for education loan.

The co-applicant question

Almost every education loan in India requires a co-applicant. The exceptions are narrow: some NBFCs offer co-applicant-free loans for students with admission to a handful of pre-approved top-tier universities, usually at a rate premium. For everyone else, the co-applicant is the loan’s actual borrower in the eyes of the bank. The student is the beneficiary. The co-applicant carries the credit risk.

Most families default to “father.” It is rarely the optimal choice. The right co-applicant is the family member with the strongest income, the cleanest credit history, the longest remaining working life, and the lowest existing EMI load. That is sometimes the father. It is also sometimes the mother, an elder sibling who is now earning, an uncle in a stable government job, or a combination of two co-applicants where one provides income and the other provides collateral. The bank’s preference is usually parents first, then siblings, then close relatives, then spouse.

The legal weight of being a co-applicant is real. The co-applicant is jointly and severally liable for the loan, which means the bank can recover the full outstanding from them alone if the student does not pay. This shows up on the co-applicant’s credit report as their own liability and affects their future borrowing capacity. If the loan goes bad, the co-applicant’s salary can be attached, their assets pursued.

If you want the full picture of how to pick a co-applicant and what they are signing up for, read Co-applicant for education loan in India. If you are exploring the co-applicant-free route, read Education loan without co-applicant.

Loans by course type

The bank’s underwriting model is not the same for every course, even at the same university. A two-year MBA at a top-ranked global school is treated as a high-confidence loan: clear placement data, predictable post-study salary, short tenure to EMI start. The bank is comfortable lending ₹60 lakh to a student with a co-applicant earning ₹12 lakh a year. The same co-applicant trying to borrow ₹60 lakh for a four-year MBBS at a private medical college will face a much harder file, because the timeline to EMI start is twice as long, the post-study earnings trajectory is more uncertain, and the absolute capitalised interest is larger.

A few course-specific patterns worth knowing. MBA loans are the easiest to clear, with the most competitive rates, because the bank has good data on outcomes. Read Education loan for MBA. MBBS at a private Indian college is one of the harder loans because the fee structure can run ₹60 lakh to ₹1.5 crore and the seat is not always on the lender’s approved list; read Education loan for MBBS at a private college. MBBS at a government college is the cleanest of all because the fee is small and the seat is gold-plated; read Education loan for MBBS at a government college. MBBS abroad (Russia, Georgia, Kazakhstan, the Philippines) is its own ecosystem with NMC eligibility risk baked in; read Education loan for MBBS abroad.

Specialised courses have their own pockets. Commercial pilot training, which now costs ₹50 lakh to ₹80 lakh end to end, has a small number of specialised lenders; read Education loan for pilot training. CA aspirants pursuing the qualification full-time can access smaller loans; read Education loan for CA students. Working professionals returning for an executive MBA or a full-time master’s can borrow against their own income; read Education loan for working professionals.

Government schemes (PM Vidyalakshmi, CSIS, the 0% myth)

The government has three real interventions in the education loan market and a great deal of marketing noise around all three. The first is the IBA Model Education Loan Scheme, which sets the framework most public sector banks follow. The second is the Central Sector Interest Subsidy (CSIS), which pays the moratorium-period interest for students from families with parental annual income below ₹4.5 lakh. CSIS is genuinely valuable but the income ceiling makes it largely irrelevant for abroad-studies borrowers, who almost always sit above the bracket.

The third, and the one that has reshaped the access landscape since launch, is the PM Vidyalakshmi portal, a single window where students can apply to multiple lenders with one form. The portal does not approve or fund anything itself; it routes applications. The newer version of the scheme also extends an interest subvention to students from families below a higher income threshold, with the central government covering a portion of the moratorium-period interest. The exact numbers are worth re-checking at the time you apply, because the parameters shift.

What does not exist, despite the WhatsApp forwards: a true 0% education loan from the Government of India for general use. The closest equivalents are state-level schemes for specific communities, scholarships that effectively reduce the loan you need, and the moratorium subsidy under CSIS for eligible families. The “zero interest education loan” framing in most ads is either a scholarship being mis-described or an outright misrepresentation. The Ministry of Education maintains the current list of legitimate central schemes.

If you want the full details, read PM Vidyalakshmi portal for education loans and The zero interest education loan myth.

Approval timeline and rejection reasons

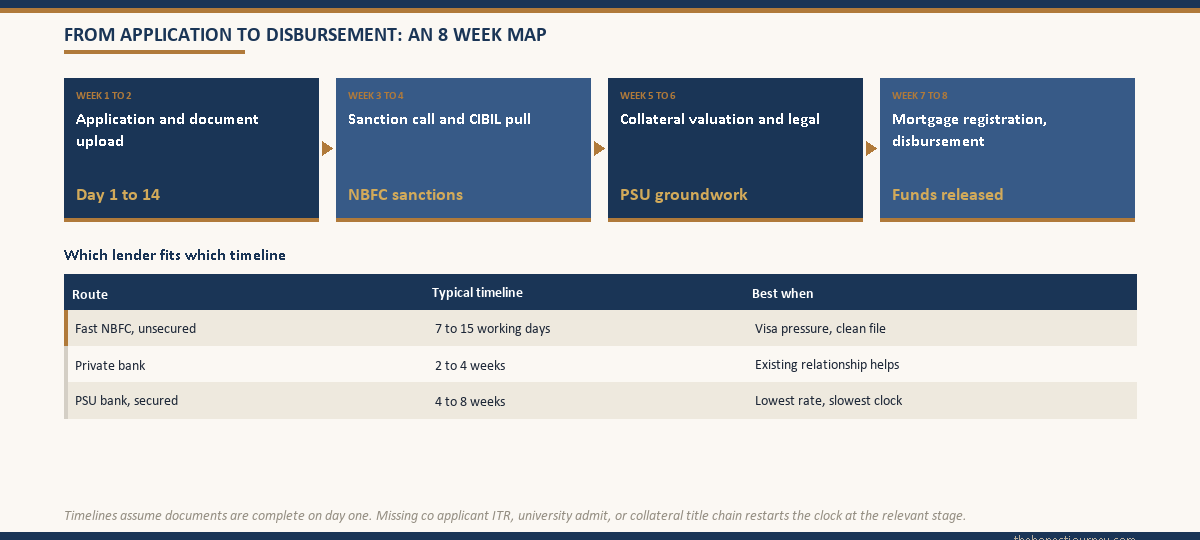

An unsecured loan from a fast NBFC can move from application to sanction in 7 to 15 working days if the file is clean. A secured loan from a public sector bank takes 4 to 8 weeks because the legal opinion, valuation, and mortgage registration add their own clocks. A private bank such as the one behind the Axis Bank education loan sits in the middle at 2 to 4 weeks. The visa timeline often forces students into the NBFC route by default, which is one reason rate-shopping early matters so much.

Rejections cluster around predictable failures. The most common are co-applicant CIBIL below threshold, FOIR exceeded because of existing loans, university not on the lender’s approved list, course not on the lender’s product list, sanctioned-to-cost ratio (the bank wants margin money the family cannot put up), and incomplete or inconsistent documentation. A rejection from one lender does not automatically mean the next will reject, but every hard enquiry adds friction. The best practice is to pre-qualify softly through PM Vidyalakshmi or through informal conversations with relationship managers before formal applications go in.

If you want the full breakdowns, read Education loan approval time in India and Education loan rejection reasons in India.

The disbursement process and what the loan covers

A sanctioned loan is not a disbursed loan. The sanction letter is the bank’s promise to lend a maximum amount. The disbursement is the actual money moving, and it usually happens in tranches tied to the course’s fee schedule. Tuition fees go directly to the university, often in foreign currency for abroad courses. Living expense components may come to the student’s account on a quarterly or semester basis. Books, equipment, and travel may be disbursed against bills.

What the loan covers, in most product designs: tuition fees, examination fees, library fees, hostel and accommodation charges, books, equipment, instruments, uniforms, computer or laptop where required for the course, travel expenses including airfare for abroad studies, study tours and project work fees, and caution deposit refunds. What it usually does not cover or covers only with explicit agreement: pre-admission coaching, accommodation deposits beyond a cap, food and personal expenses beyond the stipulated allowance.

Margin money is the other piece almost no one explains at sanction. For loans above ₹4 lakh for domestic studies and above ₹7.5 lakh for abroad studies, the bank typically requires the borrower to fund 5% to 15% of the total cost themselves. So a ₹50 lakh total cost course might have a ₹42.5 lakh sanction and a ₹7.5 lakh margin money requirement. Families miss this because the loan amount headline does not include it.

If you want the full mechanics, read The education loan disbursement process, What an education loan covers, and Margin money in education loans explained.

The moratorium and the interest trap

The moratorium is the structural feature that catches more families off guard than anything else in the entire product. It is the window during which you are not required to pay EMIs, covering your course duration plus a grace period of 6 to 12 months. The relationship manager describes it as a benefit, and it is, in the sense that you do not have to find EMI money while you are studying. But the interest does not pause.

On a ₹20 lakh loan at 11.5%, the monthly interest accrual is ₹19,167. Across a 30-month moratorium, that is ₹5.75 lakh of interest, which in most loan agreements gets capitalised, meaning added to your principal. You borrowed ₹20 lakh. Before you make a single EMI, you owe ₹25.75 lakh. On a four-year MBBS abroad with a 60-month moratorium, the same loan becomes ₹31.5 lakh at EMI start.

Faz's rule

The single most useful question to ask your bank before signing: what is my outstanding balance at the end of the moratorium period?

Not the EMI, not the rate. The outstanding balance. Any bank that has run the disbursement schedule can produce this number. The gap between what you borrowed and what you owe at EMI start is the most important number in the loan, and almost no one checks it at sanction.

You have one real lever during the moratorium: pay the simple interest. If you, your co-applicant, or a part-time-working student can service the monthly interest, capitalisation is prevented entirely. On the ₹20 lakh example, this drops the EMI from ₹36,587 to ₹28,420 and total repayment by nearly ₹10 lakh.

If you want the full math and the full set of options, read The education loan moratorium period and the interest trap.

Repayment, prepayment, and top-ups

Repayment begins the month after the moratorium ends. The standard tenure is 10 years for unsecured loans and up to 15 years for secured loans. The EMI is calculated on the post-capitalisation principal at the prevailing floating rate. Floating means the rate moves with the lender’s benchmark, which means your EMI can change during the tenure. Some lenders keep the EMI fixed and adjust the tenure; others adjust both.

Prepayment is where families who took the loan correctly recover ground. As per RBI guidelines, no penalty can be charged on prepayment of a floating-rate education loan to an individual borrower. You can pay extra at any time, partially or fully, and the bank cannot charge a foreclosure fee. The interest savings on early prepayment are large because the front-loaded structure of an EMI means most of the early payments are interest. A ₹5 lakh prepayment in year 2 of a 10-year tenure can save ₹8 lakh to ₹10 lakh in total interest, depending on the rate.

Top-ups are the opposite case. If the course extends, costs rise, or a new semester adds an unfunded gap, most lenders allow a top-up to the existing facility rather than a new loan, subject to fresh credit checks and within the original product cap.

For the full repayment playbook, read How to repay an education loan in India. For the prepayment math specifically, read Should you prepay your education loan in India. For top-ups, read Education loan top-ups.

Section 80E and the tax angle

Section 80E of the Income Tax Act gives a deduction for the entire interest paid on an education loan, with no upper cap on the deduction amount. It is one of the few uncapped deductions in the tax code. The deduction is available for a maximum of 8 years from the year you start repayment, or until the interest is fully paid, whichever is earlier. It applies to loans taken for higher education for the borrower, their spouse, children, or a student for whom the borrower is a legal guardian.

Two practical realities. First, the deduction is on the person who actually pays the interest. If the co-applicant (parent) is paying the EMI, the parent claims the deduction. If the student takes over the loan after employment and pays from their own salary, the student claims it. The bank’s interest certificate, issued annually, names the payer. Second, the deduction is only useful in the old tax regime. The new regime, which is now the default for individual filers, does not allow Section 80E. For a family in the 30% bracket, choosing the old regime and using 80E on a ₹20 lakh loan can save ₹1.5 lakh to ₹2 lakh in tax over the moratorium-plus-EMI cycle.

| Loan amount | Interest rate | Tenure (post-moratorium) | Total interest paid | Approx 80E benefit (30% bracket) |

|---|---|---|---|---|

| ₹10 lakh | 10% | 10 years | ₹5.9 lakh | ₹1.77 lakh |

| ₹20 lakh | 11.5% | 10 years | ₹18.1 lakh | ₹5.4 lakh |

| ₹40 lakh | 12% | 10 years | ₹37 lakh | ₹11.1 lakh |

If you want the full rule book, read Education loan tax benefit under Section 80E. The official source on the deduction sits at incometax.gov.in.

Insurance and the rights you actually have

Most lenders bundle credit life insurance with the loan, premium added to the principal. The pitch is that if the borrower dies during the loan, the insurance pays off the outstanding balance and the family is not left with the liability. That is a real protection. What is not always disclosed is that the premium can be ₹50,000 to ₹1.5 lakh on a large loan, that you are paying interest on the premium for the full tenure, and that in many cases the insurance is optional, not mandatory, despite how it is presented. Always ask, in writing, whether the insurance is a condition of sanction or an opt-in.

Your rights as a borrower are clearer than most lenders admit. Under the RBI’s master directions and Fair Practices Code, you are entitled to: a copy of the sanction letter and loan agreement, a copy of all signed documents, advance notice of any change in interest rate, a clear annual statement showing principal and interest paid, no penalty for prepayment on floating-rate loans, transparent disclosure of all fees, and access to the Banking Ombudsman for unresolved grievances.

Faz's rule

If the bank refuses to share the loan agreement, the sanction letter, or the interest-rate-change communication in writing, escalate immediately.

The Banking Ombudsman scheme is genuinely effective. Most disputes that get formally filed are resolved in the borrower’s favour within 60 days. The threat of an ombudsman complaint is often enough to unlock documents the branch was sitting on for months.

The insurance angle and the rights framework are covered in full in Education loan insurance and RBI guidelines for education loans.

Loans for abroad studies: TCS, GIC, approved universities

Abroad-studies loans live in their own world because of three things: tax collected at source on foreign remittances, country-specific funding requirements like the Canadian GIC, and the bank’s approved-university list. The TCS on foreign remittances under the Liberalised Remittance Scheme is currently 5% on remittances above ₹7 lakh in a financial year for education funded through a loan from a notified financial institution, and 20% otherwise. The TCS is not a tax. It is an advance collection that can be adjusted against your final tax liability or refunded. On a ₹50 lakh remittance for tuition, that is potentially ₹2.5 lakh sitting with the government until your return is filed.

The Canadian GIC (Guaranteed Investment Certificate) is a one-time deposit of around CAD 20,635 (roughly ₹12.5 lakh) that the student parks with a Canadian bank as proof of first-year living expenses. The deposit is released monthly to the student after arrival. Some Indian lenders fund the GIC as part of the education loan; others do not. Confirming this at sanction matters because finding ₹12.5 lakh of additional liquid funds two weeks before visa filing is not a problem you want to discover. If Canada is your destination, our guide to the best education loan for Canada walks through which banks fund the GIC and tuition together.

Almost every lender maintains an approved-university list. Funding for institutions on the list is faster, cheaper, and at higher loan-to-cost ratios. Funding for institutions off the list is either declined or available only at premium rates with additional collateral. The list shifts and is rarely public. Asking your shortlisted lender for the list, in writing, before you commit to a university is a step most families skip and almost all later wish they had taken.

The sanction letter itself doubles as proof of funds for the visa application in most countries, which is why timing the sanction before the visa appointment matters.

For the full set of abroad-loan specifics, read TCS on education loans in India, GIC Canada and the education loan from India, Approved foreign universities for education loans, and Using the education loan sanction letter as proof of funds. Destination-specific funding rules vary widely, so if you are headed to a high-cost Asian hub, see how the numbers work in our guide to the education loan for Singapore.

What happens if it goes wrong

The loan does not have to go wrong for the question to matter. Knowing what the bank can and cannot do if you miss EMIs, fail a course, or hit a career setback is part of taking the loan honestly. A missed EMI generates a late fee and an entry on the credit report after 30 days overdue. Three consecutive missed EMIs (90 days) is the point at which the account becomes a non-performing asset on the bank’s books and the recovery machinery activates: calls, notices, and eventually legal action.

The bank’s recovery options depend on whether the loan is secured. On a secured loan, the bank can invoke the SARFAESI Act to take possession of the pledged property after due notice and process. On an unsecured loan, recovery is through civil suit and court decree, which is slower but real. The co-applicant is jointly liable throughout, so the bank can pursue their assets and income alongside the student’s.

What does not happen, despite what aggressive recovery agents sometimes imply: the bank cannot stop the student from leaving the country, cannot withhold the passport, cannot pursue criminal cases for non-payment of a civil debt unless fraud is alleged. Threats outside the law are themselves grounds for a complaint to the Banking Ombudsman.

The other scenario worth knowing is backlogs and course-extension cases. A semester backlog typically does not trigger any loan action. A pattern of backlogs that delays course completion can lead the bank to reassess, sometimes extending the moratorium and sometimes triggering early EMI start on the disbursed portion.

For the full picture, read What happens if the education loan is not paid and Education loans with backlogs in India.

Calculators you can use right now

The math in this post is the kind that should not be done by hand once you have your actual numbers. Three calculators on the site do the work cleanly. The Education loan EMI calculator takes the principal, rate, and tenure and produces the EMI and the amortisation schedule. The Education loan moratorium calculator takes the moratorium length and shows the capitalised balance and the post-moratorium EMI side by side with the no-moratorium case, so you see exactly what the trap costs you. The Prepay vs invest calculator answers the most common post-employment question: should the next bonus go into prepaying the loan or into an SIP.

Run the three calculators in that order before you sign any sanction letter. The output of the moratorium calculator is the number to fight the relationship manager on. The output of the prepay calculator is the discipline you will need three years into repayment.

Where to go next

If you are at the early stage and trying to decide whether to take a loan at all, start with the secured versus unsecured tradeoff and the CIBIL eligibility check. If you are mid-process with a sanction in hand, the moratorium piece and the disbursement piece are the two that matter most. If you have already started repayment, the prepayment math and the Section 80E filing are where the money is.

- Just exploring: Secured vs unsecured education loan, then CIBIL score for education loan.

- Sanction in hand: The moratorium and interest trap, then The disbursement process.

- Studying abroad: TCS on education loans and Approved foreign universities.

- Already repaying: Should you prepay your loan and Section 80E tax benefit.

- Something went wrong: What happens if the loan is not paid.

Faz's rule

The education loan is a 12 to 15 year relationship with a bank. Treat the sanction letter like a marriage contract, not a credit card.

Read every clause. Ask for the moratorium balance projection in writing. Confirm whether insurance is optional. Pull the co-applicant CIBIL before applying, not after rejection. Most loan problems are sanction-time problems that become visible only at EMI start.

FAQ

What is the maximum education loan amount available in India?

For unsecured loans, most lenders cap at ₹7.5 lakh for domestic studies and ₹40 lakh to ₹75 lakh for abroad studies. Some NBFCs sanction up to ₹1.5 crore for top-tier overseas universities without collateral. With collateral, public sector banks routinely sanction ₹1.5 crore and above, with the limit set by the value of the pledged security and the co-applicant’s income rather than a product cap. The actual sanction depends on the course, the university, the co-applicant’s FOIR, and the lender’s appetite for the country and institution.

What is the current interest rate on education loans in India?

Rates in 2026 sit in three bands. Public sector banks with collateral offer 8.5% to 10%, private banks offer 9.5% to 11.5%, and NBFCs without collateral offer 11.5% to 14%. Floating rates are tied to the lender’s external benchmark, typically the repo rate, with a spread. Women borrowers often get a 0.25% to 0.5% concession at public sector banks. The rate gap between secured and unsecured is the single biggest cost driver in the loan, often worth ₹5 lakh to ₹10 lakh over the tenure on a ₹20 lakh principal.

Is collateral mandatory for an education loan?

No. Loans up to ₹7.5 lakh for domestic studies are unsecured by RBI guideline and require only the parent or guardian as co-applicant. For larger amounts, lenders typically ask for collateral, but specialised NBFCs and some private banks offer collateral-free loans for higher amounts, particularly for students with admission to top-tier universities. The trade-off is the rate: collateral-free loans carry interest rates 2 to 4 percentage points higher than secured loans, which compounds into a significant total cost difference.

Who can be a co-applicant for an education loan?

Most lenders accept parents, spouse, siblings, or close relatives as co-applicants. The co-applicant must have a stable income, an acceptable CIBIL score (700 and above for most lenders), and sufficient FOIR headroom to absorb the proposed EMI. The co-applicant is jointly and severally liable for the loan, which means the bank can recover the full outstanding from them if the student does not pay. Some NBFCs offer loans without a co-applicant for students with admission to a small list of pre-approved top-tier universities, usually at a rate premium.

What is the moratorium period and how does it work?

The moratorium is the period during which you are not required to pay EMIs, typically covering your course duration plus a grace period of 6 to 12 months. Interest accrues every month from the date of first disbursement and, in most loan agreements, gets capitalised (added to principal) at the end of the moratorium. So on a ₹20 lakh loan at 11.5% with a 30-month moratorium, you start EMIs on a balance of approximately ₹25.75 lakh, not ₹20 lakh. Paying simple interest during the moratorium prevents capitalisation and is the single most effective cost-saving move available.

How long does it take to get an education loan approved?

An unsecured loan from a fast NBFC can sanction in 7 to 15 working days if documentation is complete. A private bank takes 2 to 4 weeks. A secured loan from a public sector bank takes 4 to 8 weeks because property valuation, legal opinion, and mortgage registration add their own timelines. Visa-linked abroad applications often push families into the NBFC route by default because of the timeline pressure. Pre-qualifying through PM Vidyalakshmi or through informal lender conversations before formal application can reduce friction.

What documents are required for an education loan application?

Standard documents include student KYC (identity, address, PAN, passport), all academic mark sheets from Class 10 onwards, the entrance exam scorecard, the admission letter, the official fee structure, co-applicant KYC and income proof (three years of ITR, six months of bank statements, Form 16 if salaried), and proof of existing loans or assets. For students with an academic gap, a gap certificate is required. For abroad studies with a visa application, a sponsorship affidavit may be needed. Collateral-backed loans add valuation report, legal opinion, and title documents.

Can I get an education loan with a low CIBIL score?

The bank evaluates the co-applicant’s CIBIL, not the student’s. A co-applicant CIBIL below 650 is hard to clear with most lenders. Public sector banks with collateral are slightly more flexible because the security reduces credit risk. NBFCs are stricter, often demanding 720 and above for the better rate cards. If the primary co-applicant has weak credit, adding a second co-applicant with stronger credit can sometimes unlock the file. Resolving stale or incorrect entries on the report before applying is the first step, not the last.

What is Section 80E and how much can I save?

Section 80E of the Income Tax Act allows a deduction for the entire interest paid on an education loan, with no upper limit on the deduction amount, available for up to 8 years from the year repayment starts. The deduction is claimed by whoever actually pays the interest, which is usually the co-applicant during the moratorium and EMI years. The benefit is meaningful only under the old tax regime; the new regime does not allow it. For a family in the 30% bracket on a ₹20 lakh loan, the tax saving over the loan tenure can exceed ₹5 lakh.

Can I prepay the education loan without penalty?

Yes, on floating-rate education loans to individual borrowers, RBI guidelines prohibit prepayment penalties. You can prepay partially or in full at any time, including during the moratorium. The interest savings on early prepayment are large because EMIs are front-loaded with interest. A ₹5 lakh prepayment in year 2 of a 10-year tenure can save ₹8 lakh to ₹10 lakh in total interest. Always get a fresh amortisation schedule from the bank after each prepayment to confirm the principal reduction has been applied.

What happens if I cannot repay the education loan?

A missed EMI generates a late fee and, after 30 days overdue, an entry on the credit report. Three consecutive missed EMIs make the account a non-performing asset, triggering formal recovery action. The bank’s options depend on whether the loan is secured. On a secured loan, the bank can invoke SARFAESI to take possession of the pledged property. On an unsecured loan, recovery is through civil suit. The co-applicant is liable throughout. The bank cannot stop you from travelling, cannot withhold the passport, and cannot pursue criminal cases for civil non-payment unless fraud is alleged.

Is the PM Vidyalakshmi portal the same as a government loan?

No. PM Vidyalakshmi is a single-window application portal where students can apply to multiple banks with one form. The portal does not lend or approve anything itself. It routes the application to participating lenders, who underwrite by their own criteria and offer at their own rates. The newer version of the scheme adds an interest subvention for students from families below a defined income threshold, with the central government covering part of the moratorium-period interest. The subvention is real but the loan itself is a regular commercial product from the chosen bank or NBFC.

Faz · The Honest Journey · 2026