RBI guidelines under the Model Education Loan Scheme entitle every Indian student to apply for up to ₹50 lakh for domestic study and ₹1.5 crore for abroad, with no collateral required up to ₹7.5 lakh. The rules also cap processing fees, mandate a moratorium covering course duration plus 12 months, and forbid prepayment penalties on floating rates. Banks cannot reject you on the basis of address or branch service area alone.

The bank officer told a family I know that their daughter’s loan could not go through because their permanent address fell outside the branch’s “service area.” They were ready to give up. They had already been turned away once, and a second rejection felt like a verdict. It was not a verdict. It was a branch officer either misreading the rules or hoping the family would not push back.

Most students treat an education loan as a favour the bank is doing them. It is not. It is a regulated product, and the RBI guidelines for education loan sit behind it like a rulebook most borrowers never read. This post is that rulebook, in plain language, framed as what it actually is: your rights.

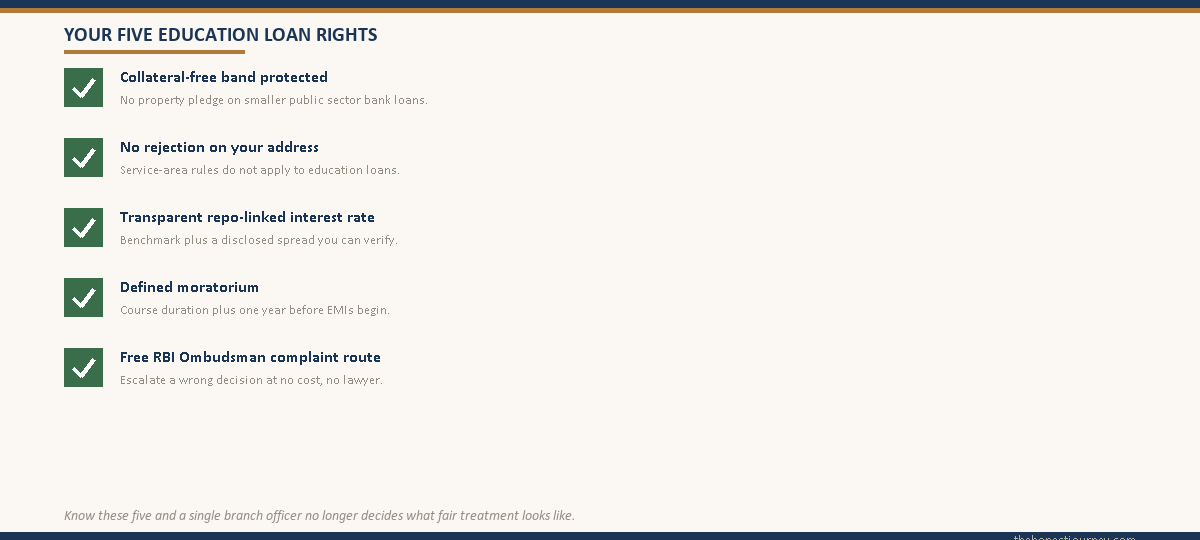

The RBI guidelines for education loan do not set one fixed interest rate or guarantee approval. What they do is define a floor of fair treatment: collateral-free lending up to a set limit, transparent repo-linked pricing, a defined moratorium, an ethical recovery process, and a free grievance route through the RBI Integrated Ombudsman Scheme. Know these five and you stop being at the mercy of one officer’s mood.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The loan basics nearby: the what education loan covers post, the education loan EMI calculator math post, and the education loan vs personal loan post.

Where the RBI guidelines for education loan actually come from

There is a common confusion worth clearing up first. The RBI does not write the education loan scheme line by line. The actual scheme template is the Model Education Loan Scheme (MELS), framed by the Indian Banks’ Association (IBA) and adopted by member banks. The RBI’s role is the regulator’s role: it issues master directions on lending, pricing, fair practices, and grievance handling that every bank must follow, and the IBA scheme is built to sit inside those rules.

So in practice, two documents govern your loan. The IBA Model Education Loan Scheme decides things like loan limits, the collateral-free ceiling, and the moratorium structure. The RBI master directions decide how the loan is priced, how you are treated, and where you complain when a bank gets it wrong. A bank’s own product brochure is a third layer, and it can be stricter than both, but it can never be looser. When a brochure contradicts the regulator, the regulator wins.

The reason this matters: when an officer quotes you a “rule,” you are allowed to ask which document it comes from. A genuine rule traces back to the IBA scheme or an RBI direction. A branch-level preference does not, and you can push on it.

Right one: collateral-free lending up to a defined limit

This is the single most useful thing for a student to know. Under the IBA Model Education Loan Scheme, banks cannot demand collateral for smaller loans.

The structure runs in three bands. For a loan up to ₹4 lakh, no collateral and no third-party guarantee can be insisted on. The parent simply joins as co-applicant. For a loan above ₹4 lakh and up to ₹7.5 lakh, the bank can ask for a third-party guarantee but still cannot demand tangible collateral like property. Above ₹7.5 lakh, the bank is allowed to ask for collateral.

| Loan amount | Collateral | What the bank can ask for |

|---|---|---|

| Up to ₹4 lakh | Not allowed | Parent or guardian as co-applicant only |

| Above ₹4 lakh to ₹7.5 lakh | Not allowed | A third-party guarantee, plus co-applicant |

| Above ₹7.5 lakh | Allowed | Tangible collateral, co-applicant, sometimes a guarantee |

There is a second layer that students rarely hear about. The Credit Guarantee Fund Scheme for Education Loans (CGFSEL), backed by the central government and administered alongside the schemes listed by the Ministry of Education, provides a guarantee cover to banks on collateral-free loans up to ₹7.5 lakh. In plain terms, the government partly insures the bank against default on these loans. So a bank that tells you it “cannot do collateral-free above ₹4 lakh” is not just bending the IBA scheme, it is also ignoring a guarantee fund built specifically so it can say yes.

The honest caveat: this collateral-free protection is firmest for public sector banks following the IBA scheme. Private banks and NBFCs run their own products. They often lend collateral-free well above ₹7.5 lakh, but they price that risk into a higher interest rate, and they are not bound by the IBA bands in the same way. If you want to understand how unsecured abroad loans actually work in practice, the education loan for abroad studies without collateral post walks through the real numbers.

Faz's ruleA loan up to ₹7.5 lakh from a public sector bank should not need property as collateral. If a branch insists, ask which rule says so.

The IBA Model Education Loan Scheme and the CGFSEL guarantee fund both exist to make collateral-free lending up to ₹7.5 lakh possible. A branch officer asking for a property mortgage on a ₹6 lakh loan is going past the scheme. You are within your rights to ask for that demand in writing, then escalate.

Right two: a bank cannot reject you over your address or service area

This is the rule the family in the opening was never told. Banks operate with branch service areas for many product categories. Education loans were specifically carved out of that constraint. A bank cannot refuse an education loan application simply because the applicant’s residence falls outside the branch’s service area, and it cannot insist you apply only at a branch near your home town.

The reason the rule exists is obvious once you see it. A student from a small town might have a parent co-applicant there, a university across the country, and the only convenient branch near the campus. If service-area rules applied, that student would be stuck. So the guideline is clear: an education loan application has to be considered on the merits of the course, the institution, the co-applicant’s repayment capacity, and the academic record. Not the pin code.

If you are refused on service-area grounds, do not accept it as final. Ask for the rejection in writing with the specific reason stated. A bank that is genuinely declining on merit will give you a real reason. A bank hiding behind “service area” usually goes quiet the moment you ask for it on paper, because the officer knows it does not hold up. Address-based rejection is one of the most common informal refusals, and it is also one of the easiest to overturn. For the full picture on why loans actually get declined, see the education loan rejection reasons post.

Right three: a transparent, repo-linked interest rate

Years ago, banks priced loans off an internal “base rate” that customers could not see or verify. The RBI ended that for retail loans. Education loans from banks are now linked to an external benchmark, in most cases the RBI repo rate. The bank’s lending rate is published as the External Benchmark Lending Rate (EBLR), which is the repo rate plus a fixed spread the bank discloses.

What this gives you as a borrower is real transparency. You can see the benchmark, you can see the spread, and you can verify the math. When the RBI changes the repo rate, your floating-rate education loan should move in step within the reset cycle defined in your agreement, usually every three months. The bank cannot quietly hold your rate high while the benchmark falls.

Three things you are entitled to check before signing. First, ask whether the rate is repo-linked or marginal-cost based, and ask for the spread in writing. Second, ask for the reset frequency. Third, confirm that there is no prepayment or foreclosure penalty. RBI guidelines bar prepayment charges on floating-rate loans given to individual borrowers, which covers most education loans. If a lender mentions a foreclosure fee on a floating-rate education loan, ask them to point to the clause and the regulation behind it.

NBFC pricing works differently. NBFCs are regulated, but they are not bound to the EBLR framework the way banks are, so an NBFC rate is set by the lender’s own policy. It is still disclosed, and you are still entitled to the full schedule of charges, but the repo-linked transparency above applies cleanly to banks.

Right four: a defined moratorium period

The moratorium is the window when you are not required to pay EMIs. Under the IBA Model Education Loan Scheme, the standard moratorium is the course duration plus one year. So a two-year master’s abroad typically carries a moratorium of three years before the EMI clock starts.

The point worth being precise about: a moratorium is a holiday from EMIs, not a holiday from interest. Interest accrues through the moratorium, and in most loans it is capitalized, meaning it is added to your principal at the end. The RBI’s contribution here is not to stop the interest, it is to require that the bank communicate clearly how moratorium interest is treated and what your outstanding balance will be when repayment begins. You are entitled to ask for that figure in writing at sanction time. This single number, the balance at EMI start, is the most under-checked figure in any education loan, and the education loan moratorium period and interest post runs the full math on what it costs.

You also have the right to know your repayment tenure, which under the scheme typically runs up to 15 years after the moratorium, and the right to make partial payments during the moratorium to reduce capitalization. No lender can stop you from servicing interest early.

Faz's ruleThe moratorium is course duration plus one year, and interest runs through all of it.

Treat the moratorium as a defined right, not a vague favour. You are entitled to know, in writing, the exact moratorium length and your projected balance when EMIs start. A bank that cannot produce that number at sanction time is telling you something about how it handles transparency.

Right five: ethical recovery and a free grievance route

This is the right that matters most if something goes wrong, and it is the one borrowers know least about. Two parts.

First, recovery has to be ethical. RBI’s fair practices code binds every bank and NBFC. If a borrower defaults, the lender can pursue recovery, but it cannot harass. No calls before 8 am or after 7 pm, no contacting your relatives and neighbours to shame you, no abusive language, no threats, no use of muscle. Recovery agents must identify themselves and follow the code. An education loan default is a serious financial event, but it does not strip you of the protection of the fair practices code. If a recovery agent crosses that line, that is itself a complaint.

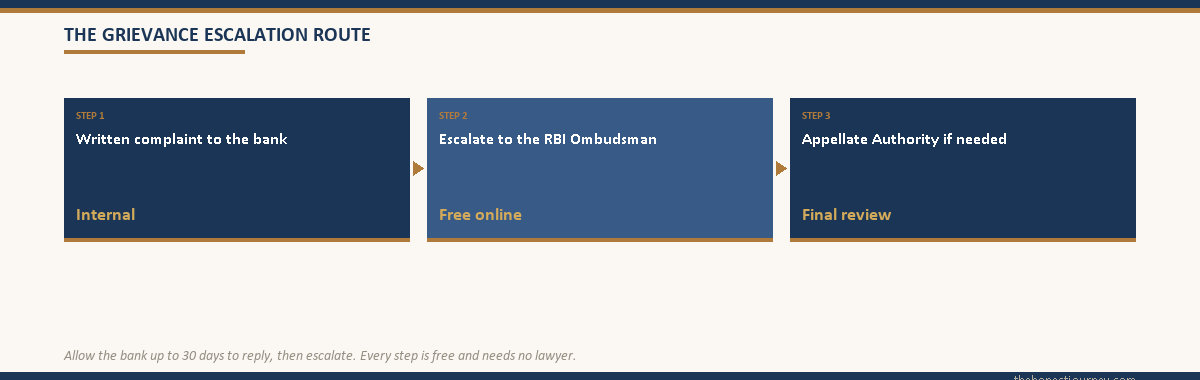

Second, the grievance route. The path runs in three steps. Step one, complain in writing to the bank’s own grievance redressal officer and keep the acknowledgement. Step two, if the bank does not resolve it within 30 days, or gives a reply you are not satisfied with, escalate to the RBI under the Reserve Bank Integrated Ombudsman Scheme. This is the single nationwide ombudsman that replaced the older separate banking, NBFC, and digital ombudsmen. Filing is free. You can file online through the RBI’s complaint portal, by email, or by post, and the scheme covers banks and the larger NBFCs.

| Step | Where to go | Cost and timeline |

|---|---|---|

| 1. Internal complaint | The bank or NBFC grievance redressal officer, in writing | Free. Allow up to 30 days for a reply |

| 2. RBI Ombudsman | Reserve Bank Integrated Ombudsman Scheme, via RBI complaint portal | Free. Escalate after 30 days or an unsatisfactory reply |

| 3. Appellate authority | The Appellate Authority named in the scheme | Free. If you disagree with the Ombudsman’s decision |

The thing to internalise: this route is free and it is real. A bank that wrongly rejects you on service-area grounds, charges a foreclosure penalty it should not, or lets a recovery agent harass your family is exposed to an ombudsman complaint, and banks treat those complaints seriously because the RBI tracks them. You do not need a lawyer to file. You need a written paper trail and 30 days of patience.

What the RBI guidelines do not promise

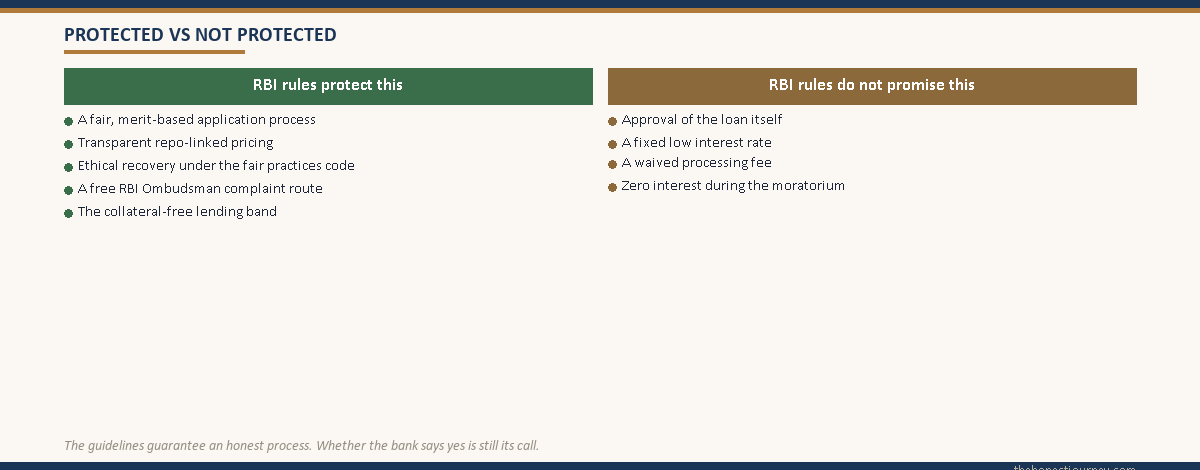

Honesty cuts both ways, so here is the other side. The guidelines protect the process. They do not guarantee an outcome.

They do not guarantee approval. A bank can still decline your loan on genuine merit grounds: a co-applicant whose income does not support the EMI under the bank’s debt-to-income checks, a course or institution the bank does not consider employable, a poor academic record, or an existing credit default in the family. Those are legitimate reasons, and no RBI rule overrides a bank’s right to assess repayment capacity.

They do not fix one interest rate. Within the transparency rules, banks compete, and rates vary by lender, by collateral, and by co-applicant profile.

They do not cap the processing fee universally. Many public sector banks waive the processing fee on education loans, and that is a policy choice by the bank, often a genuine zero. Private banks and NBFCs commonly charge a processing fee, typically around 1 percent of the loan amount, sometimes more. There is no RBI rule that forces a free processing fee. What you are entitled to is full disclosure of every charge before you sign, with nothing added afterward. So the right question is not “is the processing fee waived,” it is “show me the complete schedule of charges in writing.”

And they do not stop interest during the moratorium. That is built into the product. The guidelines only force the bank to be clear about it.

How to use these rights in practice

Knowing the rights is half of it. Using them is the other half, and it comes down to a few habits.

Get everything in writing. A verbal rejection is not a rejection you can act on. Ask for the reason on the bank’s letterhead. A verbal rate quote is not binding. Ask for the sanction letter with the rate, spread, reset frequency, and full charge schedule spelled out.

Compare at least three lenders before you sign. One public sector bank, one private bank, and one NBFC is a sensible spread, because the collateral bands, rates, and fees genuinely differ. The guidelines protect you at each one, but they do not make the lenders identical.

Keep a paper trail from day one. Every email, every acknowledgement, every letter. If you ever need the ombudsman route, that file is your case.

And once the loan is running, your rights continue. You can prepay a floating-rate education loan without penalty, you can question a rate that has not moved when the repo rate has, and you can claim the Section 80E income tax deduction on the interest. How to actually clear the loan efficiently, including prepayment timing, is covered in the how to repay an education loan post.

Faz's ruleThe RBI guidelines protect the process, not the result. Use them to demand fairness, not to expect a yes.

A bank can still decline you for real reasons, and that is the system working. What the rules guarantee is that the decline is honest, the pricing is transparent, the recovery is ethical, and you have a free route to complain when it is not. That is a strong floor. It is not a ceiling.

The honest closing take

Most students lose ground on an education loan not because the rules are stacked against them, but because they never knew the rules existed. They accept a service-area rejection that should not stand. They pledge a property on a ₹6 lakh loan that did not need collateral. They never ask for the spread or the charge schedule in writing. They assume a recovery call is something they must simply endure.

None of that is the borrower’s fault in a moral sense. The information is not handed to you. But the moment you read these five rights, the dynamic changes. You are no longer asking a bank for a favour. You are using a regulated product, and you know what fair treatment looks like.

The guidelines will not make a bad loan good. If the amount is wrong for your earning potential, no RBI rule fixes that, and you still have to run your own math. What the guidelines do is make sure the deal you sign is an honest one. Whether to sign it at all is still your call, and it always was.

FAQ

What are the RBI guidelines for education loans?

The RBI guidelines for education loan are a set of protections that govern how banks lend, price, and recover education loans. The core ones: collateral-free lending up to ₹7.5 lakh under the IBA Model Education Loan Scheme, transparent repo-linked interest rates, a defined moratorium of course duration plus one year, an ethical recovery process under the fair practices code, and a free grievance route through the RBI Integrated Ombudsman Scheme. They protect the process, not approval itself.

Can a bank reject an education loan based on my address?

No. Education loans were specifically carved out of branch service-area restrictions. A bank cannot refuse your application simply because your residence falls outside the branch’s service area. The loan must be assessed on the course, the institution, the co-applicant’s repayment capacity, and the academic record. If you are refused on address grounds, ask for the rejection in writing with the specific reason stated, then escalate. Informal address-based refusals rarely survive a written request.

Is there a processing fee on education loans under RBI rules?

There is no RBI rule that forces a free processing fee. Many public sector banks waive it on education loans as a policy choice, often a genuine zero. Private banks and NBFCs commonly charge a processing fee, typically around 1 percent of the loan amount. What you are entitled to is full written disclosure of every charge before you sign, with nothing added afterward. So ask for the complete schedule of charges, not just whether the fee is waived.

What is the RBI moratorium rule for education loans?

Under the IBA Model Education Loan Scheme, the moratorium runs for the course duration plus one year. During this window you are not required to pay EMIs. The moratorium is a holiday from EMIs, not from interest: interest accrues throughout and is usually capitalized into your principal at the end. The RBI’s contribution is to require the bank to communicate clearly how moratorium interest is treated and what your balance will be when repayment starts.

Can I complain about a bank to the RBI?

Yes, and it is free. First file a written complaint with the bank’s grievance redressal officer and keep the acknowledgement. If the bank does not resolve it within 30 days, or gives an unsatisfactory reply, escalate to the RBI under the Reserve Bank Integrated Ombudsman Scheme. You can file online through the RBI complaint portal, by email, or by post. The scheme covers banks and larger NBFCs. You do not need a lawyer to file.

What is the Model Education Loan Scheme?

The Model Education Loan Scheme (MELS) is the template framed by the Indian Banks’ Association and adopted by member banks. It defines the practical terms of an education loan: the collateral-free bands, loan limits, the moratorium structure, and repayment tenure. It sits inside the RBI’s master directions on lending and fair practices. Together, the IBA scheme and the RBI directions form the rulebook behind a bank education loan, and a bank’s own brochure cannot be looser than either.

Is collateral always required for an education loan?

No. Under the IBA Model Education Loan Scheme, a loan up to ₹4 lakh needs no collateral and no third-party guarantee. A loan above ₹4 lakh and up to ₹7.5 lakh can require a third-party guarantee but not tangible collateral like property. Only above ₹7.5 lakh can a bank ask for collateral. The CGFSEL government guarantee fund covers collateral-free loans up to ₹7.5 lakh, so a public sector bank demanding property below that limit is going past the scheme.

Can a bank harass me to recover an education loan?

No. RBI’s fair practices code binds every bank and NBFC. A lender can pursue recovery on a default, but it cannot harass. No calls before 8 am or after 7 pm, no contacting your relatives and neighbours to shame you, no abusive language, no threats, no muscle. Recovery agents must identify themselves and follow the code. If an agent crosses that line, that is itself a valid complaint you can file with the bank and escalate to the RBI Ombudsman.

Faz · The Honest Journey · 2026