You repay an education loan in India through monthly EMIs that begin once the moratorium ends, which is typically your course duration plus 6 to 12 months. The EMI uses a reducing-balance formula on the outstanding principal. In my experience the trap is the moratorium interest: if you do not service it during study, it gets capitalised, so you start repaying a balance larger than the original loan.

A friend’s brother, three months into his first job in Bengaluru after a UK master’s, called me last August. His ₹38L education loan moratorium had ended in July. The bank had auto-debited an EMI of ₹52,400 from his salary account on the 5th of August. He had ₹61,000 in that account that morning. After the debit, rent for the new apartment was due on the 7th. He had not understood that the moratorium ending meant the EMI would simply start, on a fixed date, every month, regardless of whether he had moved cities, finished setting up his Indian salary account, or even noticed.

The EMI mechanics of an education loan are not complicated, but they are not explained the way they need to be at sanction stage. Banks tell you the rate and the tenure. They do not walk you through what the actual flow looks like from the moment the moratorium ends through the next 10 years of payments. This post is that walk-through, with the specific things that go wrong and what to do about them.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on managing repayment: the what happens if education loan not paid post and the education loan top UP post.

The 60-second answer

Education loan repayment starts after the moratorium period ends (typically course duration + 6-12 months). EMI is calculated using the standard reducing-balance formula based on the outstanding principal after the moratorium, which includes any interest that accrued and was capitalised during the moratorium itself. Interest typically continues to accrue during the moratorium, meaning the principal you start repaying is higher than the original loan amount unless you serviced interest during studies. Repayment is via auto-debit from a designated savings account, typically on a fixed date each month. Prepayment is allowed with no penalty in most education loans (RBI regulation for floating-rate retail loans). Tenure is typically 7-15 years depending on the loan size and lender.

The moratorium ends differently from how families think it ends

Faz's rule

The moratorium is a period without EMI, not a period without interest.

Interest accrues every month on the disbursed principal. If you don’t service it during studies, it capitalises at moratorium end and your EMI jumps roughly 25%. On a ₹40L loan that’s ₹15,000 a month, or ₹18L over the life of the loan.

The biggest misunderstanding sits here. The “moratorium” is a period where you are not paying EMI. It is not a period where you are not accruing interest. Two distinct things, and most families conflate them.

During a typical education loan moratorium:

- Interest accrues every month on the principal disbursed

- Simple interest is charged in this period (some lenders compound it monthly, the simple-interest treatment is more common)

- You are not required to pay EMI during the moratorium

- You can optionally pay just the interest during the moratorium to prevent capitalisation

- At moratorium end, any unpaid accrued interest is added to the principal, and EMI is calculated on this new, larger amount

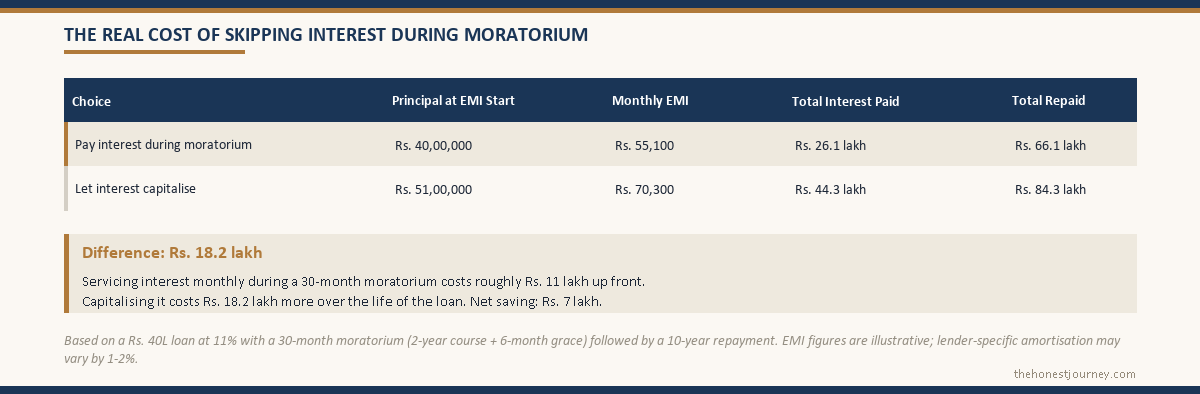

So a ₹40L loan disbursed at 11% with a 30-month moratorium (2-year course + 6-month grace) accrues approximately:

- ₹40L × 11% × 2.5 years = ₹11L of interest during the moratorium

If none of that interest is serviced during the moratorium, the principal at the start of repayment becomes:

- ₹40L + ₹11L = ₹51L

The EMI is calculated on ₹51L, not ₹40L. Over a 10-year repayment tenure at 11%, that becomes an EMI of approximately ₹70,300. If interest had been serviced monthly during the moratorium, the EMI would be approximately ₹55,100, a difference of ₹15,200 per month, or about ₹18.2L over the life of the loan.

We covered the full moratorium math in our moratorium post. The repayment phase is the place where that earlier choice shows up as a number in your monthly bank statement.

When does the EMI actually start

The exact date depends on the loan agreement. Typical scenarios:

Scenario A: Course completion + 6 months. The moratorium ends 6 months after the official course end date. EMI starts the month after moratorium ends. This is the IBA model schedule and applies to most PSU and several private bank loans.

Scenario B: Course completion + 12 months. Some lenders offer a 12-month grace period for the job search. EMI starts after that.

Scenario C: 6 months after first job, or moratorium end, whichever is earlier. A small set of NBFCs use this hybrid trigger. If you find a job 3 months after graduation, EMI starts 9 months after graduation, not after the full 12.

Scenario D: Course completion + no grace. Rare, but some lenders (typically aggressive NBFCs) move directly from course end to EMI start. Check this at sanction stage.

The lender sends a repayment schedule document approximately 30-45 days before the first EMI is due. It lists the EMI amount, the date, the account to debit from, and the full amortisation schedule. If you have not received it 30 days before your expected moratorium end, write to the lender. Do not wait for them.

The mechanics of EMI auto-debit

When the loan is sanctioned, you sign a NACH (National Automated Clearing House) mandate authorising the lender to debit a designated account on a fixed date each month. The default date is usually the 5th, 7th, or 10th of the month. Lenders sometimes let you pick.

What this means in practice:

- On the EMI date, the amount is debited automatically. No action needed from you.

- If the account has insufficient balance, the mandate fails, the lender charges a bounce fee (typically ₹500-750 plus GST), and the bank that holds the savings account may also charge an EMI bounce fee on their side (another ₹500).

- After a failed auto-debit, the lender re-presents the mandate, usually 2-3 working days later. If that also fails, the account is flagged.

- After two consecutive failed auto-debits, the loan account is reported as 30-DPD to CIBIL. We covered the CIBIL impact in detail in our recent CIBIL post.

The defensive setup: Open the designated repayment account at least 30 days before the first EMI is due. Park 2-3 EMIs worth of cushion in it. Set up an alert on every debit. Do not use this account for any other regular outflows (rent, subscriptions) for the first 6 months, keep it isolated and fully funded.

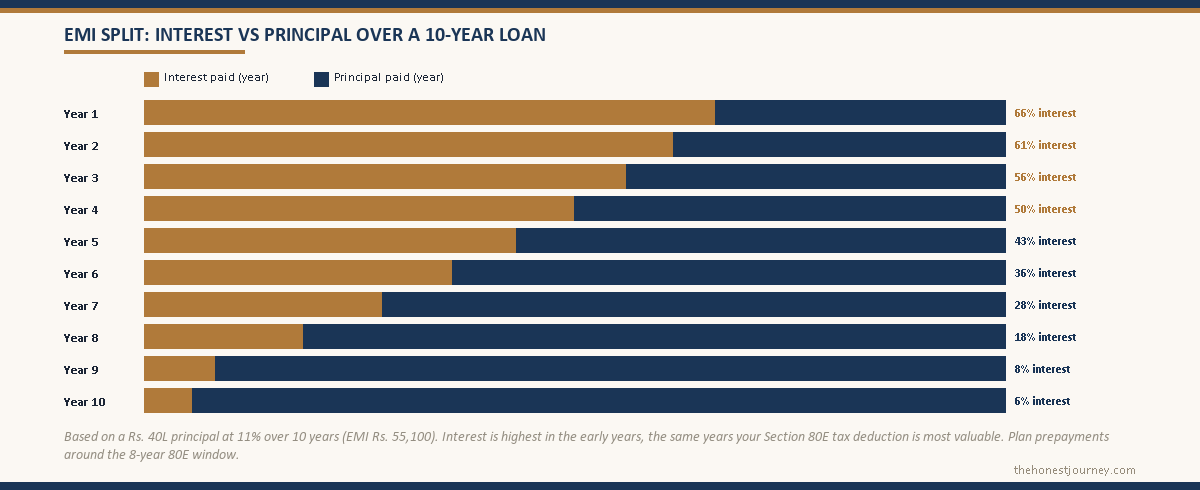

Interest is calculated on reducing balance

Every education loan in India uses the reducing balance method. The EMI stays constant each month, but the split between interest and principal changes over the tenure.

Early in the loan, most of the EMI is interest. Late in the loan, most of it is principal. A worked example on a ₹40L loan at 11% over 10 years:

| Year | EMI/month | Interest paid (year) | Principal paid (year) | Outstanding at year-end |

|---|---|---|---|---|

| Year 1 | ₹55,100 | ₹4,38,000 | ₹2,23,200 | ₹37,76,800 |

| Year 3 | ₹55,100 | ₹3,93,000 | ₹2,68,200 | ₹33,28,500 |

| Year 5 | ₹55,100 | ₹3,32,000 | ₹3,29,200 | ₹27,16,200 |

| Year 7 | ₹55,100 | ₹2,47,000 | ₹4,14,200 | ₹18,75,400 |

| Year 9 | ₹55,100 | ₹1,29,000 | ₹5,32,200 | ₹6,84,500 |

| Year 10 | ₹55,100 | ₹37,000 | ₹6,24,200 | ₹0 |

Total interest paid over the 10-year repayment: approximately ₹26.1L (on top of the ₹40L principal, plus the moratorium interest if it was capitalised). That is the number to plan around, not the headline rate.

This matters for two reasons. First, your Section 80E tax deduction (defined under the Income Tax Act) is on interest, which is highest in early years, meaning the tax benefit is front-loaded and largest when you can least afford to lose it (in years 1-3 of starting a career). Second, prepayment math depends on how early in the tenure you do it.

Prepayment: when it helps, when it does not

Education loans in India are governed by RBI floating-rate retail loan rules. No prepayment penalty is allowed for floating-rate loans, which includes essentially all education loans. You can prepay any amount, any time, with no fee.

Faz's rule

Section 80E ends in Year 8. Plan prepayments around that window.

Interest paid in years 9 and 10 of repayment gets no tax deduction. If you have surplus cash in Year 7 or 8, paying down before the 80E window closes saves you from servicing non-deductible interest at the end of the loan.

But “can prepay” is different from “should prepay.” We covered this in detail in the prepay-or-invest post. The short version for the repayment context:

Early-tenure prepayment is high-impact. Prepaying ₹5L in Year 1 of a 10-year loan at 11% saves approximately ₹4.2L in interest over the life of the loan. Same prepayment in Year 7 saves about ₹85,000.

Section 80E ends in Year 8. Interest paid in years 9-10 is no longer tax-deductible. If you have surplus money in Year 7 or 8, it can make sense to prepay the loan down before the deduction window closes, so you are not paying non-deductible interest unnecessarily.

Partial vs full prepayment. Most lenders allow either. Partial prepayment reduces the EMI (or shortens the tenure, you usually get to choose). Choosing to shorten tenure saves more interest. Choosing to reduce EMI gives more monthly breathing room.

Process for prepayment. Email the lender’s customer service with the loan account number and the prepayment amount. Some lenders need a physical visit or a signed form for amounts above ₹1L. Allow 5-7 working days for the prepayment to be applied. The next EMI date is recalculated automatically.

What happens if you genuinely cannot pay one month

This happens. Job loss, medical emergency, salary delays. The structured options:

- Pre-empt with the lender. If you know an EMI is going to fail (job loss, salary delayed), email the lender’s customer service before the debit date, not after. Most lenders have an internal “EMI deferral” or “rephasement” option that can move one EMI to the end of the tenure if requested in advance. This is discretionary, not a right, and lenders weigh it against your repayment history.

- Use the moratorium extension clause. Some loan agreements have an “additional moratorium” clause for unemployment periods, typically up to 6 months. This needs proof (resignation acceptance, employer letter). Read your sanction letter, this clause is often present but not advertised.

- Restructure to a longer tenure. If the problem is persistent (lower-than-expected salary), some lenders will extend the tenure from 10 years to 12 or 15, which lowers the EMI. This requires a formal restructuring request and typically a small processing fee.

- Single-EMI bounce is recoverable. One bounce, with the EMI made good within 7-14 days, does not get reported to CIBIL. Two consecutive bounces does. The cost of bounce fees (typically ₹1,000-1,500 total) is small compared to the CIBIL damage from a 30-DPD reporting.

- Avoid using a credit card to pay the EMI. This is a common but costly move. Credit card “loan against limit” or paying with a card creates a separate high-interest debt that is harder to clear. The card EMI defeats the purpose of having an education loan with sub-12% rates.

The repayment account setup, end to end

A practical setup for the first 12 months of repayment:

Month before moratorium end:

- Confirm the EMI amount, date, and debit account with the lender

- Open or designate a savings account specifically for EMI debit

- Set up a standing instruction from your salary account to transfer 1.1x the EMI to the debit account on the 1st of every month

- Pre-fund the debit account with 2-3 months of EMI as cushion

Month 1 of repayment:

- Verify the first debit went through cleanly

- Check the loan statement (lender sends a monthly or quarterly statement)

- Confirm the EMI split matches what you expected, there should be a sharp interest skew in this first month

Months 2-12:

- Monitor the salary-account-to-debit-account standing instruction is firing

- Build the debit account cushion gradually to 3-4 EMIs

- If your salary increases, consider raising the standing instruction to allow occasional prepayments

Year 1 close:

- Pull the interest certificate from the lender (needed for Section 80E claim if you are filing in Old Regime)

- Decide whether to make a year-end prepayment or defer until the next financial year

- Reassess: is the EMI sustainable at your current income level, or do you need a tenure extension?

Common mistakes that cost real money

Paying the EMI from a credit card. Defeats the rate advantage. Card interest is 36-42% effective annual rate; loan EMI is 10-13%.

Letting a small balance underfund the debit account. ₹500 short of the EMI triggers a bounce, a fee, and potentially a CIBIL flag. The buffer is worth more than the marginal interest the money would earn elsewhere.

Not claiming Section 80E. Particularly in the first 2-3 years of repayment when interest paid is highest and tax deduction is largest. If the loan is in the parent’s name, the parent claims. We covered the who-claims-what mechanics here.

Continuing to pay the EMI in Year 11 of an 8-year 80E window. Years 9-10 of repayment have interest paid but no tax deduction available. If you have the surplus, prepaying down before Year 9 saves you from paying non-deductible interest.

Not getting the interest certificate. The lender does not always send it automatically. You may need to request it from the loan customer service portal. Without the certificate, the ITR claim under 80E is difficult to defend if challenged.

Mixing repayment account with salary account. The risk is that another large transaction (a rent payment, a card bill) clears just before the EMI date and leaves insufficient balance. Keep the EMI account isolated for the first year at least.

When prepayment from a parent vs from the student matters

If the loan is in the parent’s name with the student as co-applicant, Section 80E goes to the parent as long as the parent is the one paying interest. If the student later starts earning and sends money home to the parent to fund EMI, the deduction stays with the parent (the borrower), but the household tax planning gets cleaner if the parent’s tax slab is higher.

If the loan is in the student’s name, the student is the only one who can claim 80E once they start earning. Parents helping with EMI in early years are paying down a loan they cannot deduct against in their own returns.

The borrower-name decision at sanction stage has a 10-year tax-saving consequence. We laid out the three sub-cases in the 80E post. It is worth re-reading before any major prepayment decisions.

If you want to run your own figures, use the education loan EMI calculator to work out your monthly EMI, total interest and total payable before you sign.

Frequently asked questions

When exactly does my first EMI hit my account?

The first EMI typically debits 1 month after the moratorium ends, on the specific calendar date stated in your loan agreement (usually the 5th, 7th, or 10th of the month). The lender sends a repayment schedule 30-45 days before this date. Confirm with the lender if you have not received it.

Can I change the EMI date after the loan is disbursed?

Sometimes. Lenders allow one or two changes during the tenure for genuine reasons (salary credit date changes). Email the lender’s customer service. Allow 30 days for the change to take effect.

What is the EMI amount on a ₹40L education loan at 11%?

Over a 10-year tenure with interest serviced during moratorium: approximately ₹55,100/month. With moratorium interest capitalised: approximately ₹70,300/month.

How do I prepay my education loan?

Email or call the lender’s customer service with the loan account number and the prepayment amount. Transfer funds to the lender’s specified account. Allow 5-7 working days for the prepayment to be applied. Most lenders allow online prepayment through their portal for amounts under ₹1L; larger amounts may require a physical or signed-form process.

Is there a penalty for prepaying my education loan?

No. RBI rules prohibit prepayment penalties on floating-rate retail loans, which includes essentially all education loans in India.

What happens if I bounce one EMI?

A bounce fee (typically ₹500-1,500 total across the lender and your bank) is charged. If you make good the EMI within 7-14 days, it does not get reported to CIBIL. Two consecutive bounces or any 30+ day delay does get reported and stays on your credit file for 7 years.

Can I switch lenders after disbursement to get a better rate?

Yes, through a “loan takeover” or balance transfer. RBI directions on interest rate on advances require lenders to let floating-rate retail borrowers switch without a foreclosure penalty. Most lenders accept education loan takeovers if the borrower’s credit is clean and the rate differential is meaningful. Processing fees apply (typically 0.5-1% of outstanding balance). Worth doing if the rate improvement is more than 1.5%.

My moratorium is ending but I do not have a job yet. What can I do?

Apply for a moratorium extension before the end date. Most lenders allow a 3-6 month extension on documented evidence of an active job search. Some loan agreements have this clause built in; others require a formal request. Either way, raise it early, not after the first EMI bounces.

If you are at the start of repayment planning, also read the prepay or invest analysis for the question of where to put surplus income (most people get this wrong by either over-prepaying or under-prepaying), the Section 80E post to make sure the tax benefit is claimed correctly, the moratorium post to understand how the choice you made earlier shaped the EMI you are paying now, and the education loan insurance post if you want to know whether a loan-protection policy is worth funding to cover the EMI burden in the worst case.