Prepay your education loan if the post-tax interest rate (typically 8 to 9 percent after Section 80E) is higher than the realistic after-tax return you can earn on a long-horizon SIP, otherwise invest. For most Indian salaried borrowers in the 30 percent slab, an 11 to 12 percent loan costs around 8 percent net, which beats a debt fund but loses to a 12 to 13 percent equity SIP over 7 plus years. Cash-flow comfort decides the rest.

You just got your first salary credit. The education loan EMI hits your account on the 5th. And somewhere in the back of your head, a question keeps surfacing: should you throw every spare rupee at the loan, or invest it instead?

This is the most common financial question I hear from Indian students who studied abroad or took a large domestic education loan. The honest answer is: it depends on the math, your tax situation, and one thing that no spreadsheet captures well. Let us work through all three.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on managing repayment: the education loan balance transfer india post, the RBI education loan repayment rules post, and the what happens if education loan not paid post.

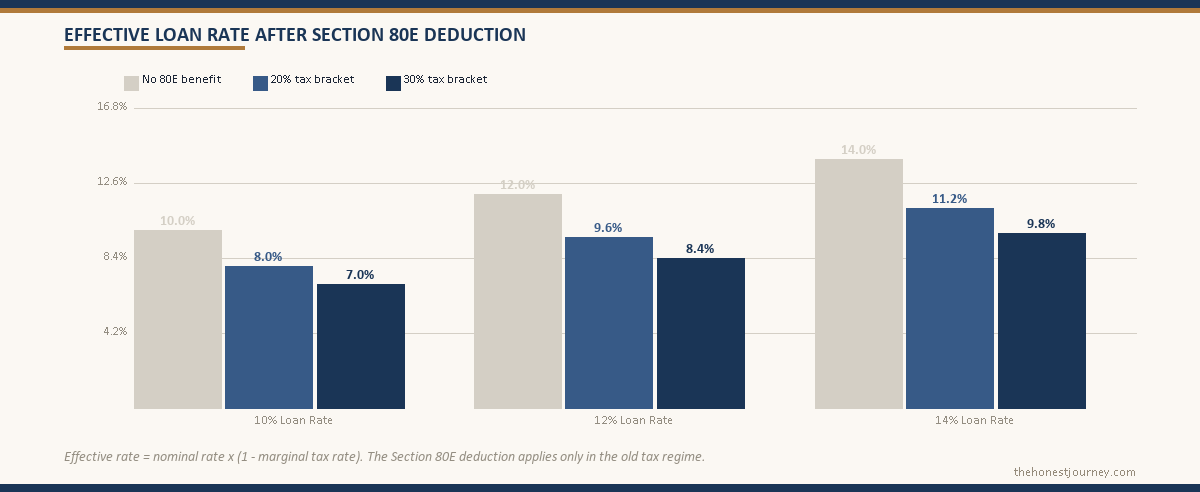

First, know exactly what your loan is costing you

Most education loans in India sit between 10.5% and 13.5% per annum. Some public sector banks offer slightly lower rates for top-tier institutions; NBFCs tend to charge closer to 13 to 14 percent, a gap broken down in the bank vs NBFC interest rate comparison. Before you do anything, pull your loan statement and find the actual interest rate, not the marketing number, the one printed on your sanction letter.

Now calculate the real cost after tax. Under Section 80E of the Income Tax Act, you can deduct the entire interest paid on an education loan from your taxable income. The deduction runs for up to 8 years from the year you start repaying. There is no rupee cap, the full interest amount is deductible.

If you are in the 30% slab plus 4% cess, your effective tax rate on income is 31.2%. A loan at 12% interest becomes:

Effective cost = 12% x (1 – 0.312) = 8.26%

At a 20% slab: 12% x (1 – 0.208) = 9.5%

That number, 8.26% or 9.5%, is what you should compare against investment alternatives. Not the headline loan rate.

The interest rate arbitrage question

Here is where most personal finance advice gets lazy. People say “invest instead of prepaying” without telling you what investment actually beats the loan rate.

Faz's ruleAfter-tax effective rate matters, not nominal rate.

A 12% loan rate becomes effectively 8.4% in a 30% slab with 80E, lower than the after-tax return on most Indian equity over a 10-year horizon. The prepay-or-invest decision needs both numbers, not just the headline loan rate.

Let us be specific.

| Investment option | Expected return (pre-tax) | Post-tax return (30% slab) |

|---|---|---|

| Fixed deposit (1-3 year) | 7.0 to 7.5% | 4.8 to 5.2% (income tax on interest) |

| Debt mutual fund | 7.5 to 8.5% | ~7.5% (indexation benefit gone post-2023) |

| ELSS / equity MF (10+ yr horizon) | 11 to 13% (long-run historical) | ~10.5 to 11.5% (10% LTCG above ₹1.25L) |

| PPF | 7.1% (current) | 7.1% (exempt) |

| NPS Tier 1 (aggressive) | 10 to 12% (long-run) | Partially deferred, partial exemption |

Compare these numbers against your effective loan cost from above. If your loan after 80E benefit costs you 8.26%, a debt fund returning 7.5% post-tax is a losing trade. You are better off prepaying. But an equity mutual fund running 10.5-11.5% post-tax over a long horizon does beat the loan rate, in theory.

The “in theory” matters. Equity returns are not guaranteed. In any 3-5 year window, equities can underperform dramatically. If your loan tenure is 5-7 years, you are taking on sequence-of-returns risk that a 30-year retirement portfolio does not face in the same way.

Faz's ruleCompare your effective loan rate (after 80E), not the headline rate, against investments.

The 30% slab taxpayer on a 12% loan faces an effective cost of about 8.3%. Fixed deposits and debt funds lose that comparison easily. Only equity mutual funds held long enough have a realistic shot at beating it.

Section 80E: the full picture

Section 80E is one of the cleanest deductions in the Income Tax Act. No cap. No form 16 confusion. You claim the actual interest paid during the financial year (whatever it is) and it reduces your gross total income directly.

A few things people miss:

- The 8-year clock starts from the year you begin repayment, not from the year you took the loan or graduated. If you had a 2-year moratorium period, the clock starts after the moratorium ends.

- The deduction is available only to the individual who took the loan, not a parent co-applicant unless they are the primary borrower. The full rules sit in the Section 80E tax benefit post.

- It covers loans taken for any higher education (domestic or abroad) from a financial institution or approved charitable institution. Loans from friends or family do not qualify.

- If you prepay the entire loan in year 3, you lose 5 years of 80E benefit. That is real money.

Here is a concrete example. Suppose your education loan outstanding is ₹20L at 12%, and you are in the 30% slab. In year 3 of repayment, you are paying roughly ₹1.8-2.0L in interest annually. That interest claim saves you around ₹56,000-62,000 in tax. If you foreclose the loan this year, you lose that saving for years 4, 5, 6, 7, 8. That is a cumulative tax benefit of ₹2-3L you are walking away from, depending on how fast your balance amortises.

Part-prepayment vs full foreclosure: they are not the same decision

Most people treat “should I prepay?” as a binary. It is not.

Faz's rulePrepayment is highest-impact in years 1-3, lowest in years 9-10.

₹5L prepaid in Year 1 saves ₹4.2L of interest over the life of the loan. The same ₹5L in Year 7 saves ₹85,000. The 80E window also closes in Year 8. Time prepayments around both signals.

Full foreclosure means clearing the entire outstanding. It ends your EMI obligation and eliminates all future interest. It also ends your 80E benefit immediately and frees up your CIBIL profile for other credit.

Part-prepayment means paying a lump sum toward the principal while keeping the loan alive. Most banks allow this without a prepayment penalty for floating rate loans (RBI mandates no prepayment charges on floating rate loans). Fixed rate loans may have a 1-2% charge, check your sanction letter.

Part-prepayment has an underrated advantage: you can choose to either reduce the EMI or reduce the tenure. Almost always, choose to reduce the tenure, not the EMI. Reducing tenure cuts your total interest outgo more aggressively because the outstanding principal falls faster.

Faz's rulePart-prepay to cut tenure, not EMI, the math works in your favour.

On a ₹20L loan at 12% over 10 years, paying ₹2L extra in year 2 toward principal and choosing tenure reduction can save you ₹3-4L in total interest compared to the same ₹2L invested in a fixed deposit. Run the numbers before defaulting to the FD.

The psychological argument for clearing debt

I am not dismissing this. Some people genuinely cannot invest well while carrying debt anxiety. They lose sleep, make reactive decisions, and under-save in other ways. For those people, the psychological premium of being debt-free is worth taking a slightly suboptimal financial position.

But be honest with yourself about whether you are in that category. If you are someone who can comfortably ignore the loan notification and run a disciplined SIP every month, the arithmetic case for investing over prepaying (especially in the early years when 80E saves you the most) is solid.

If your loan hangs over every financial decision you make, clearing it might unlock better behaviour across the board, and that is worth something real.

A framework for the actual decision

Here is how I would approach it, given the numbers above:

Years 1-3 of repayment: Lean toward investing over aggressive prepayment. Your outstanding is highest, so your 80E benefit is highest. The interest deduction is doing the most work here. Direct surplus into equity mutual funds via SIP if you have a 7+ year horizon. Always check that the fund and your distributor are registered with SEBI before committing. Build your emergency fund first, 3 to 6 months of expenses minimum.

Years 4-6: Reassess. If your effective investment return has been tracking ahead of your effective loan cost, continue. If your loan is a floating rate loan and rates have risen, or if your income has not grown as expected, consider part-prepayment to reduce tenure.

After year 8 of repayment: The 80E window closes. Your effective loan cost jumps back to the full headline rate. This is when prepayment or foreclosure becomes clearly attractive for most people, because you no longer have the tax offset working for you.

Faz's ruleAfter year 8, the 80E shield is gone, that is when prepayment math flips clearly.

Pre-year 8, the tax deduction reduces your true borrowing cost significantly. Post-year 8, every rupee of interest hits you at full cost. If you have not cleared the loan by then, attack it aggressively.

One thing the models miss: your loan is in rupees, your salary might not be

If you are earning in a foreign currency (common for students who studied abroad and took up international roles), your rupee loan becomes cheaper every year if the rupee depreciates against your earning currency. A ₹25L loan looks very different in year 5 when you are earning in GBP or USD. This is an argument against aggressive prepayment if you are in that situation, let currency movement do part of the work. Conversely, if you returned to India and earn in rupees, this does not apply.

The short version

Prepay aggressively only when: your loan rate after 80E still exceeds what your investments are realistically returning, you are past year 8 of repayment (80E window closed), or the debt is causing genuine financial anxiety that is impairing your decision-making.

Invest instead when: you are in the 80E window and your effective loan cost is below 9%, you have a genuine long-horizon equity strategy and the discipline to stick to it, and your emergency fund is already solid.

Part-prepay as a middle path: pay lump sums against principal every year to reduce tenure, keep the loan alive for 80E purposes, and continue a parallel equity SIP. This is the least dramatic but often the most sensible path for someone in the ₹15-30L loan range in the first 5-6 years of their career.

A worked example: ₹5 lakh, prepay or invest, over the full loan life

Abstract percentages only get you so far. Let me run one concrete case end to end so you can see the gap.

Assume a ₹20 lakh loan at 12 percent over 10 years. Your EMI is roughly ₹28,700. In year 2 of repayment, a relative gifts you ₹5 lakh and you have to decide what to do with it.

Option A, prepay ₹5 lakh toward principal and reduce tenure. The outstanding drops sharply, and at 12 percent that ₹5 lakh of principal you cleared early would otherwise have generated roughly ₹4.1 lakh of interest across the remaining years. You also shave close to 30 months off the tenure. The catch: you lose the 80E deduction on that ₹4.1 lakh of interest, which at a 30 percent slab is about ₹1.28 lakh of tax benefit forgone over those years.

Option B, invest ₹5 lakh in an equity mutual fund for 8 years. At a realistic 11 percent compounded, ₹5 lakh becomes about ₹11.5 lakh before tax. After 10 percent LTCG on the ₹6.5 lakh gain (above the ₹1.25 lakh exemption), you keep roughly ₹10.9 lakh. Meanwhile you keep paying the loan and claiming 80E each year.

Net comparison. Option A saves about ₹4.1 lakh of interest but costs ₹1.28 lakh of lost tax shield, a net benefit near ₹2.8 lakh, and it is certain. Option B turns ₹5 lakh into a ₹5.9 lakh gain, but only if equities deliver 11 percent across that window, which they may not. In an honest read, Option B wins on expected value, Option A wins on certainty. If you cannot tolerate the variance, prepayment is not the wrong answer. It is just the more expensive kind of peace of mind.

What changes if your loan was self-funded instead of bank-financed

This whole article assumes you have a formal education loan from a recognised lender. A meaningful share of families instead fund studies from savings, a property loan, or a loan against a fixed deposit. If that is you, the prepay-or-invest framing shifts in two ways.

First, there is no 80E deduction. Section 80E applies only to loans from banks, recognised financial institutions, or approved charitable institutions taken specifically for higher education. A general personal loan or a loan against property used for fees does not qualify, even if every rupee went to tuition. That removes the tax shield entirely, so your effective borrowing cost equals the headline rate.

Second, the rate you are comparing against is usually different. A loan against property might sit at 9 to 10.5 percent, a personal loan at 14 percent or higher. Without 80E softening it, a 14 percent personal loan is almost always worth clearing before any equity investment, because no realistic post-tax equity return reliably beats 14 percent. If you are still at the decision stage and weighing whether to borrow formally at all, the education loan vs self-funding comparison walks through the tradeoff in full. The short version: a formal education loan with 80E often costs less in real terms than draining savings that could compound, which is exactly why the prepay question is worth this much thought.

Building the prepayment into a yearly review habit

The single most useful change is to stop treating prepayment as a one-time dramatic decision and start treating it as a yearly checkpoint. Once a year, ideally when you file your income tax return, pull three numbers.

One, your loan’s current outstanding and the interest you paid last financial year. Two, your effective loan cost after the 80E deduction at your current tax slab. Three, the actual post-tax return your investments delivered over the last 12 months, not the long-run assumption, the real figure.

If your investments outpaced your effective loan cost, stay the course and keep the SIP running. If they trailed it, or if you have crossed year 8 and the 80E shield is gone, redirect that year’s surplus into a tenure-reducing part-prepayment. This keeps you from making the decision once at age 26 and then never revisiting it while rates, slabs, and markets all move. Floating rate education loans in particular reprice when the RBI changes the repo rate, and you can confirm the current rate environment from the RBI press releases. A yearly review costs you 20 minutes and routinely beats a fixed rule applied blindly for a decade. If the mechanics of how part-prepayment is applied to your account are unclear, the education loan repayment guide covers exactly how lenders process a lump sum against principal.

If you want to run your own figures, use the prepay or invest calculator to compare your after-tax loan cost against your expected investment return on your own numbers.

FAQ

Is there a prepayment penalty on education loans in India?

For floating rate education loans, the RBI prohibits lenders from charging a prepayment penalty. For fixed rate loans, lenders can charge a prepayment fee, typically 1-2% of the prepaid amount. Check your original sanction letter under the foreclosure or prepayment clause before making a lump-sum payment.

Can I claim Section 80E if my parents are the primary borrower?

Section 80E allows the deduction for the individual who took the loan for their own higher education, or for a relative (which includes a spouse, children, or a student for whom you are a legal guardian). If your parents are the primary borrowers and you are repaying the loan, the deduction is available to the person who actually pays, but the loan must have been taken for the student’s education. Consult a chartered accountant for your specific loan structure before filing.

Should I prepay the education loan or start investing for retirement first?

These are not mutually exclusive, but if you must choose, the priority order is: (1) build a 3-month emergency fund, (2) contribute enough to NPS or EPF to capture any employer match if applicable, (3) then split between loan prepayment and equity SIP based on the rate arbitrage discussed in this article. Waiting 10 years to start investing while clearing the loan fully is too conservative for most people in their late 20s.

My loan tenure is 10 years. Is it better to extend it to stretch the 80E benefit?

The 80E clock runs for 8 years from when you start repaying, not from when you took the loan. Extending the tenure does not extend the 80E window. If your loan runs for 10 years but the 80E window is 8 years, you pay full-rate interest in years 9 and 10 with no deduction. That is usually not a good trade unless your investment returns are very high and consistent.

What if I have multiple education loans, one from a public sector bank at 10.5% and one from an NBFC at 13.5%?

Clear the NBFC loan first. The after-80E effective rate on the NBFC loan at 13.5% (30% slab) is approximately 9.3%, and the public sector loan at 10.5% works out to about 7.2% effective. The gap is wide enough that the NBFC loan is almost always the right target for any prepayment surplus, regardless of tenure.

Does foreclosing the education loan affect my CIBIL score?

Closing a loan in good standing (no defaults, no missed EMIs) has a modest positive effect on your credit profile, it demonstrates successful credit repayment. The main thing to watch is that closing a credit account reduces your total credit history depth slightly, a nuance covered in the CIBIL score and education loan post. This matters most if you are planning to apply for a home loan within 6-12 months. In that case, time the foreclosure after your home loan is sanctioned, not before.