An education loan usually beats self-funding for study abroad when your investments earn more than the post-tax loan rate of roughly 7 to 8 percent and you qualify for the Section 80E interest deduction. For most middle-class families with a ₹40 lakh shortfall, taking the loan and keeping the FD or mutual fund corpus intact preserves liquidity and tax efficiency. Self-funding wins only if you have idle cash earning under 5 percent.

You have the money. Not all of it, but enough. The fixed deposits, the matured LIC policy, a chunk of the retirement corpus, maybe a plot that could be sold. The bank manager says you qualify for a loan, but the math in your head says why pay interest when you already have the cash sitting there earning 7%. So you are stuck on one question: education loan vs self funding, and which one is actually the smarter call for sending your child abroad.

This post does not sell you a loan and does not sell you the idea of staying debt-free either. It runs the real comparison, shows you three families who chose differently, and ends with a six-gate yes or no framework you can answer in ten minutes.

The honest answer to education loan vs self funding is that it depends on three things: whether your savings are genuinely surplus or are someone’s retirement, whether the after-tax cost of the EMI is higher or lower than what your money currently earns, and whether you need a loan sanction letter to strengthen a visa file. Get those three right and the decision makes itself.

For the full guide, read Should I Study Abroad? The Honest Decision Guide.

What the comparison actually is

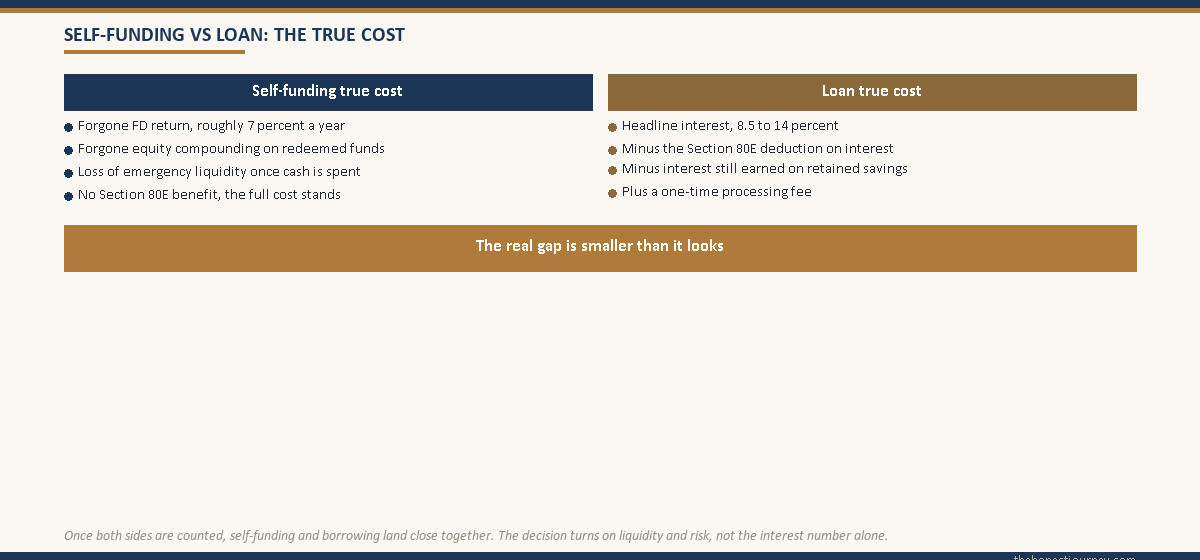

Most people frame this as cash versus debt, as if paying interest is automatically a loss. That framing is wrong. The real comparison is opportunity cost on both sides.

If you self-fund, you give up whatever your money was earning. A fixed deposit at 7%, a mutual fund SIP that has been compounding for a decade, an EPF or PPF balance, the appreciation on a property. That is the cost of self-funding. It is invisible because no EMI lands in your account, but it is real.

If you take a loan, you pay interest, currently around 8.5% to 10.5% on a collateral-secured loan from a public sector bank and 10.5% to 14% on an unsecured loan from an NBFC, a spread the interest rate comparison post breaks down lender by lender. Public sector bank loans follow the Indian Banks’ Association Model Education Loan Scheme, the framework published on the IBA site. But the interest on an education loan qualifies for a deduction under Section 80E of the Income Tax Act, with no cap on the amount, for eight years from the year repayment starts. If the co-applicant is in the 30% tax slab, a 10% headline rate costs roughly 7% after tax. The full mechanics are in the Section 80E tax benefit post.

So the honest comparison is not 7% versus 0%. It is closer to 7% (what your FD earns) versus 7% (the after-tax cost of a loan), and at that point the decision turns on liquidity, risk, and the visa angle, not on the interest number alone.

The numbers behind a typical decision

Take a two-year master’s in Canada or the UK with a total funding need of ₹35 lakh covering tuition, living costs, and forex. Assume the family has ₹40 lakh in reachable assets: ₹15 lakh in FDs, ₹15 lakh in equity mutual funds, ₹10 lakh in a parent’s retirement corpus.

| Factor | Self-fund the full ₹35 lakh | Loan the full ₹35 lakh |

|---|---|---|

| Cash out of pocket now | ₹35 lakh | ₹0 (margin money aside) |

| Headline cost over 10 years | Forgone return on ₹35 lakh | Approx ₹21 lakh interest at 10% |

| Section 80E benefit (30% slab) | None | Approx ₹6.3 lakh tax saved |

| Effective net cost of the money | Roughly 7% forgone, often higher on equity | Roughly 7% after tax |

| Emergency liquidity retained | ₹5 lakh left | ₹40 lakh intact |

| Visa file strength | Needs large proof of funds | Sanction letter is accepted proof |

Look at the bottom three rows, because that is where the decision really lives. The interest cost and the forgone return roughly cancel out. What does not cancel is liquidity and visa strength. Self-funding the full amount leaves this family with ₹5 lakh of cushion against a job loss, a medical event, or a forex swing that pushes the real cost past ₹35 lakh. Taking the loan keeps the ₹40 lakh intact and hands the visa officer a clean sanction letter.

There is also a third path that most families miss: a partial split. Self-fund the ₹15 lakh that sits in low-yield FDs, and loan the ₹20 lakh balance. You keep the equity compounding, you keep the retirement corpus untouched, you still get a sanction letter for the visa, and you claim 80E on the smaller loan. For a lot of families this hybrid is the smartest answer of the three.

Faz's rule

The interest you pay and the return you give up usually cancel out. The decision is really about liquidity and risk.

Stop comparing 10% interest to 0%. Compare the after-tax loan cost to what your money actually earns, and you will see the gap is small. Once the cost is roughly even, the question becomes simple: can you afford to be cash-poor for the next two years, and what happens if something goes wrong.

Three families, three different right answers

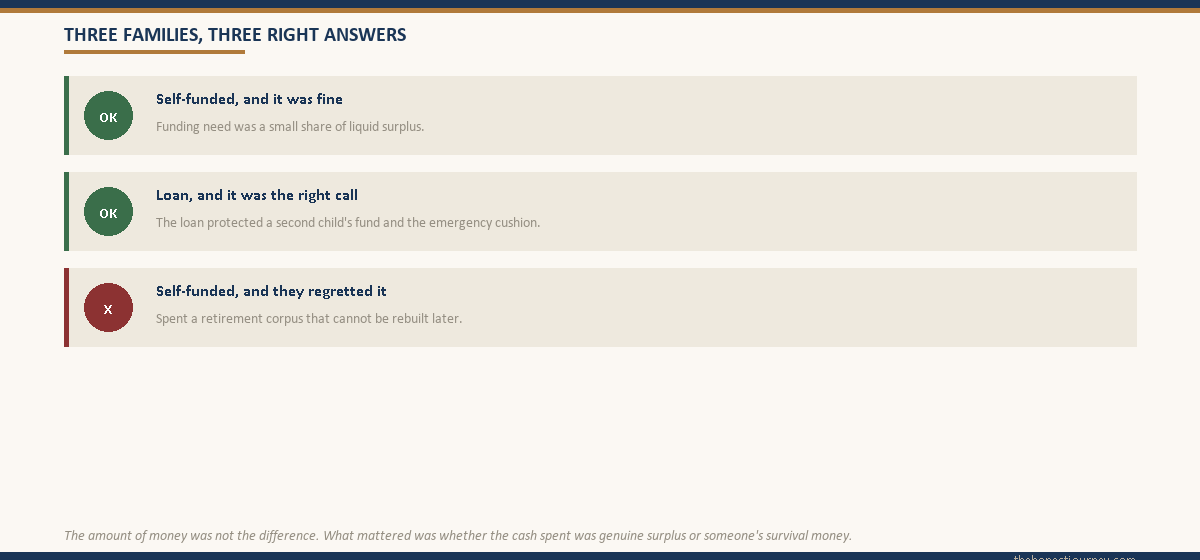

These are anonymised from real situations. The point is not that one path won. It is that each family read its own position correctly, or did not.

The family that self-funded and was fine. A Hyderabad couple, both working, sending their daughter to a one-year master’s in the UK costing ₹28 lakh. Their reachable assets were close to ₹1.1 crore, mostly in equity and FDs built over 25 years, with both parents still five to eight years from retirement and a stable combined income of ₹32 LPA. They paid the ₹28 lakh from FDs and a partial equity redemption. It moved the needle on their net worth by about a quarter and changed nothing about their lives. Their emergency fund stayed full, their retirement plan stayed on track, and there was no EMI to service. For a family where the funding need is a small fraction of liquid surplus, self-funding is the clean answer. There is nothing to optimise.

The family where the loan was the right call. A Pune family, single earner, a father at ₹18 LPA sending his son to a two-year master’s in Germany and Canada totalling ₹30 lakh. They had about ₹22 lakh saved, of which ₹8 lakh was a genuine emergency fund and the rest was earmarked for a younger daughter’s education three years out. Self-funding would have meant draining the daughter’s fund and most of the cushion. They took a ₹30 lakh collateral-secured loan at 9.25% against a residential property, kept their savings intact, serviced the simple interest during the moratorium from monthly income (the way the education loan moratorium post recommends), and the son cleared the EMI himself within a year of starting work in Canada. The loan here was not a compromise. It was the tool that let one child study abroad without robbing the other.

The family that liquidated a retirement corpus and regretted it. A Jaipur father, 56, took voluntary retirement and used roughly ₹42 lakh of his ₹55 lakh retirement payout to fully fund his son’s two-year master’s in the US, reasoning that a loan at 12% from an NBFC was throwing money away when he had cash. The son graduated into a slow hiring market, took 14 months to land a steady job, and during that gap there was no EMI to default on but also no salary coming in, no loan moratorium structure, and a father with ₹13 lakh left and no monthly income. Had he borrowed, the family could have weighed an early payoff later through the route the prepay an education loan post walks through. A medical expense for the mother ate into that further. Two years on, the father is doing consulting work he had planned to stop. The loan he avoided would have cost roughly 8.5% after the 80E deduction. The retirement security he spent cannot be borrowed back.

The difference between family one and family three was not the amount of money. It was what kind of money it was. Family one spent surplus. Family three spent survival. Education loan vs self funding is decided less by arithmetic than by honestly labelling which bucket your cash is sitting in.

Faz's rule

Never fund education by spending money you cannot rebuild.

A retirement corpus, a sole emergency fund, a younger sibling’s education money: these are not surplus, no matter how large the number looks. If self-funding means draining one of these, the loan is not the expensive option. It is the safer one, and the interest is the price of keeping your floor intact.

The visa angle most people underestimate

For several major destinations, a sanctioned education loan is treated as valid proof of funds in the visa file. For a US F-1 interview, a UK Student visa, a Canada study permit, or an Australian student visa, the question the officer is answering is whether the money to complete the course actually exists. A loan sanction letter from a recognised bank answers that cleanly.

If you self-fund, you still have to demonstrate funds, and that means showing liquid balances, FD certificates, and often a paper trail proving the money is not freshly parked. Recently transferred lump sums can invite questions about source. A bank’s sanction letter sidesteps a lot of that scrutiny because the bank has already done the diligence.

This does not mean self-funded students fail visas. Plenty do not. But if your funds are spread across assets that are awkward to show as clean liquid proof, a partial loan purely to generate a sanction letter can be a rational move even if you intend to prepay it quickly. Just confirm there is no prepayment penalty, which RBI norms generally prohibit on floating-rate loans, and check the position with your specific lender before signing. The remittance side is also worth understanding: study-abroad spending falls under the RBI Liberalised Remittance Scheme, and a TCS applies on foreign education remittances, with a lower rate on amounts funded by an education loan from a recognised institution. The TCS on education loan post covers the exact rates, and that TCS treatment is one more quiet point in the loan column.

The six-gate decision framework

Answer these in order. They are designed so the first clear “loan” answer can stop you, because the gates earlier in the list protect against the most expensive mistakes.

| Gate | Question | If the honest answer points to a loan |

|---|---|---|

| 1. The bucket test | Is the money you would spend genuine surplus, not a retirement corpus, sole emergency fund, or another child’s education fund? | If it is not surplus, take the loan. This gate alone overrides the rest. |

| 2. The cushion test | After self-funding, would you still hold six months of household expenses in reachable cash? | If self-funding wipes the cushion, take the loan or split. |

| 3. The yield test | Does your money earn more, after tax, than the loan costs after the 80E deduction? | If your investments out-earn the after-tax loan cost, lean toward a loan and keep the money invested. |

| 4. The visa test | Are your funds easy to present as clean, liquid proof of funds? | If proof of funds is awkward, a partial loan for the sanction letter helps. |

| 5. The income test | Can the family service simple interest during the moratorium from current income, without strain? | If yes, a loan is very manageable. If no, size the loan smaller or self-fund more. |

| 6. The repayment test | Is the expected post-study salary realistically able to carry the EMI at under 40% of take-home? | If the EMI math does not survive a realistic salary, shrink the loan, not the honesty. |

Read the framework this way. Gates 1 and 2 are veto gates: if either points to a loan, you take a loan (or at least a partial one), and the cost comparison no longer matters, because protecting your floor is worth more than saving two points of interest. Gates 3 and 4 decide between a full loan and a partial split. Gates 5 and 6 are sizing gates: they do not decide loan versus no loan, they decide how big the loan can responsibly be. A loan that fails gate 6 is not an argument for self-funding. It is an argument for a smaller loan and a more honest look at expected earnings.

If every gate points to self-funding, which usually means a family with deep surplus and easy liquid proof, then self-fund and do not feel you missed a tax trick. The 80E benefit is real, but manufacturing debt purely to harvest a deduction is rarely worth the EMI discipline it demands. If you want to read the official scheme framework that governs education lending, the Ministry of Education publishes it.

Faz's rule

A failed repayment test means borrow less, not self-fund more from money you do not have.

If the EMI cannot survive a realistic starting salary, the answer is to right-size the loan and rethink the destination or course budget. Draining survival money to dodge an EMI you genuinely cannot afford does not solve the problem. It hides it.

The honest closing take

Education loan vs self funding is not a contest between smart money and lazy money. Both are legitimate. The families who got it wrong were not the ones who chose debt or the ones who chose cash. They were the ones who misread what their money was for.

If you have genuine surplus, easy proof of funds, and the funding need is a modest share of your liquid wealth, self-fund and move on. If your savings are doing a job already, retirement, a second child, the household floor, then a loan is not the expensive choice, it is the responsible one, and the after-tax cost is far closer to your FD return than the headline rate suggests. And for a large number of families in the middle, the partial split, self-funding the lazy low-yield cash and borrowing the rest, is quietly the best of both.

Run the six gates honestly. The framework will not tell you what to want. It will only tell you which money is safe to spend, and that is the part most families get wrong. The decision, in the end, is yours to make.

Whichever way you fund it, someone carries the downside. If it is your parents, read the family financial decision before you sign.

FAQ

Should I take an education loan or self-fund studies abroad?

Take an education loan if self-funding would mean spending a retirement corpus, a sole emergency fund, or another child’s education money, or if you cannot keep six months of expenses in reserve afterward. Self-fund if the cost is a small share of genuine surplus and your funds are easy to present as proof of funds. For many families a partial split, self-funding low-yield cash and borrowing the rest, works best.

Is it better to self-finance studies abroad?

Self-financing is better only when the money is genuine surplus that is not earmarked for retirement, emergencies, or a sibling’s education. It avoids interest and EMI discipline. But it removes liquidity and the protection of a moratorium structure if something goes wrong. If self-funding drains your safety net, a loan is the safer choice even though it carries interest, because the interest is far cheaper than rebuilding a lost retirement corpus.

Does an education loan help with visa approval?

Yes. A sanctioned education loan from a recognised bank is accepted as valid proof of funds for US, UK, Canada, and Australia student visas. The sanction letter shows the visa officer that the money to complete the course exists and has passed bank diligence. Self-funded students must instead show liquid balances and FD certificates, and recently parked lump sums can invite questions about source.

Is an education loan worth it for study abroad?

An education loan is worth it when the after-tax interest cost, roughly 7% to 9% after the Section 80E deduction, is close to or below what your savings earn, and when borrowing protects your liquidity. It is not worth it if the expected post-study salary cannot carry the EMI under 40% of take-home pay. In that case the answer is a smaller loan and a more realistic budget, not a larger one.

Should I break my FD to fund studies abroad?

Breaking a fixed deposit can make sense because FDs are usually low-yield, around 7%, and after tax the return is modest. If that FD is not your emergency fund, using it instead of borrowing at a similar after-tax cost is reasonable. But keep equity investments and any retirement corpus untouched, since those compound faster, and never empty your last cushion. A partial approach, spending FD money and loaning the balance, often works well.

What are the downsides of self-funding?

Self-funding removes liquidity, so a job loss, a medical event, or a forex swing leaves you with no cushion and no EMI moratorium to fall back on. You give up the Section 80E tax deduction, which has no cap and runs for eight years. You also lose the compounding on whatever you liquidated. The biggest risk is spending money meant for retirement or a sibling, which cannot be borrowed back later.

How does Section 80E change the loan-versus-cash math?

Section 80E of the Income Tax Act lets you deduct the full education loan interest, with no upper limit, for eight years from the year repayment starts. For a co-applicant in the 30% tax slab, this cuts the effective interest cost by nearly a third, so a 10% headline rate costs around 7% after tax. That deduction is what brings the loan’s true cost close to a typical FD return and makes the comparison far more even than it first appears.

Is a partial loan plus partial self-funding a good idea?

Often it is the smartest option. You self-fund the low-yield cash, such as FDs, and borrow the rest, which keeps equity and retirement money compounding untouched. You still receive a loan sanction letter for the visa file and you claim Section 80E on the borrowed portion. The EMI is smaller and easier to service, and you keep an emergency cushion. For families in the middle, neither cash-rich nor cash-poor, this hybrid usually beats either extreme.

Faz · The Honest Journey · 2026