Education savings versus loan is not a one-way answer, so compare post-tax to post-tax, never headline to headline. A 7 percent FD is closer to 4.9 percent after tax for a 30 percent slab, while a 10.5 percent loan drops to about 7.35 percent effective after Section 80E. On the 30 lakh case in this post, a hybrid of 60 percent loan and 40 percent self-fund beat either extreme by 1 to 2 lakh.

An uncle of mine called me in March, sounding genuinely torn. His daughter had a Master’s admission in Edinburgh, the all-in cost would land somewhere near ₹30 lakh, and he had ₹35 lakh sitting in fixed deposits earning 7 percent. The bank manager he had spoken to that morning had told him plainly: just break the FD, why pay interest on a loan when you have the cash. His CA had said the opposite. He wanted a third opinion.

I told him the honest answer was neither of those two takes. The right call depended on numbers he had not yet looked at, including his own retirement runway, his tax slab, and what the FD was actually doing for him post-tax. We sat down with a spreadsheet that evening. By the end of it, the answer was a hybrid neither the bank manager nor the CA had suggested. This post is that same exercise, written down.

Education savings vs education loan is not a one-way answer. A loan wins when the parents’ savings are doing real work elsewhere, the borrower is in a 20 or 30 percent tax slab, and Section 80E can fully absorb the interest. Savings win when the cost is small, parents are close to retirement with no replacement income, and the FD is just sitting at post-tax 5 percent. For a ₹30L cost, a hybrid (60 percent loan, 40 percent self-fund) often beats either extreme by ₹1 to 2 lakh after tax.

The honest decision frame (without the bank manager’s pitch)

Most of the noise around education savings vs education loan comes from people whose job depends on the answer. Bank relationship managers want you to take the loan because they have targets. Parents in WhatsApp groups want you to self-fund because they think debt is bad. Neither is wrong in the abstract, but both are advice without context.

The honest frame is to look at four things together. The first is the post-tax return your savings are earning right now. A bank FD at 7 percent gross is closer to 4.9 percent post-tax for someone in the 30 percent slab. The second is the effective cost of the education loan after Section 80E. A 10.5 percent loan becomes roughly 7.35 percent effective for the same 30 percent slab borrower. The third is the cash flow stress: can the parent comfortably part with that money without disrupting their own retirement runway. The fourth is the borrower’s earning trajectory: who realistically pays the EMI back.

Stack those four against each other and the answer usually picks itself. The mistake people make is comparing the headline 7 percent FD with the headline 10.5 percent loan and concluding the loan is more expensive. Both numbers are pre-tax, and the tax treatment of each is the exact opposite of what you would assume.

Faz's rule

Compare post-tax numbers to post-tax numbers. Never headline to headline.

Bank FD interest is taxed as ordinary income at your full slab rate. Education loan interest is deductible at your full slab rate. These two work in opposite directions, so the real gap between savings yield and loan cost is much smaller than the headline numbers suggest, and sometimes the loan is mathematically cheaper than the FD it would have replaced.

The ₹30 lakh worked example, both paths to the rupee

Parents have ₹35 lakh in FDs earning 7 percent gross. Daughter has an admission costing ₹30 lakh all-in (tuition plus living for a 1-year UK Master’s). Daughter expects to start earning roughly ₹12 to 15 lakh per year post-graduation in either India or the UK. Parent is 54, retiring at 60, in the 30 percent tax slab. These are realistic 2026 numbers.

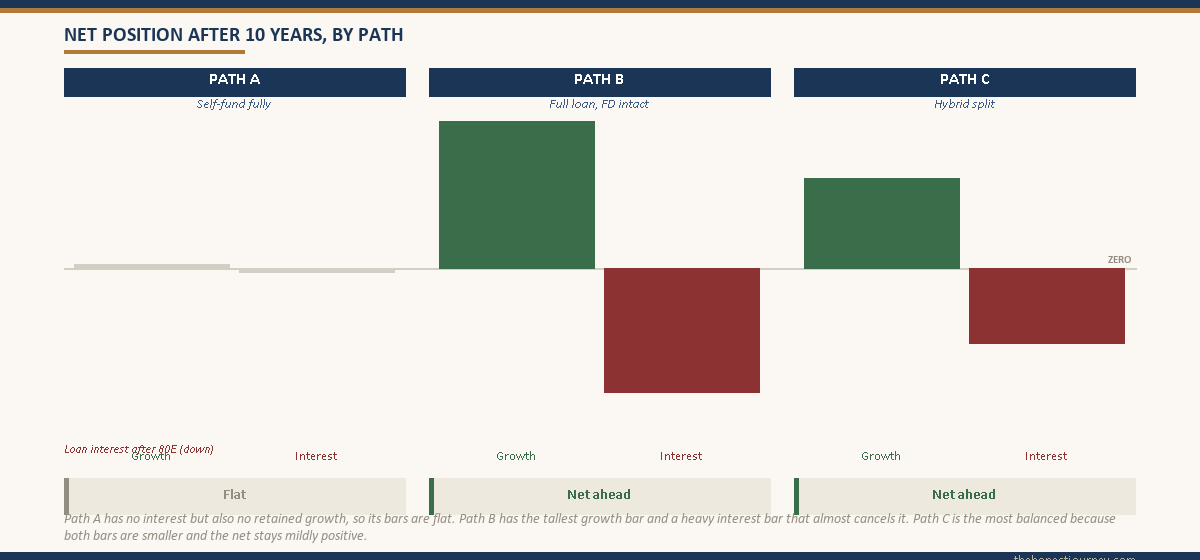

Path A is pure self-fund. Break ₹30 lakh of FDs, pay the university directly via wire, daughter graduates debt-free, parent keeps ₹5 lakh as buffer. Path B is pure loan. Keep all ₹35 lakh in FDs, take a ₹30 lakh education loan at 10.5 percent for 10 years with a 1.5 year moratorium. Path C is the hybrid: parents contribute ₹12 lakh from savings (the part that does not disturb their core retirement corpus), daughter takes an ₹18 lakh loan.

| Parameter | Path A: Self-fund ₹30L | Path B: Full loan ₹30L | Path C: Hybrid (₹12L + ₹18L loan) |

|---|---|---|---|

| Cash paid by parents upfront | ₹30 lakh | ₹0 | ₹12 lakh |

| Loan principal | ₹0 | ₹30 lakh | ₹18 lakh |

| Capitalised interest (moratorium) | ₹0 | ~₹4.7 lakh | ~₹2.8 lakh |

| Loan balance at EMI start | ₹0 | ~₹34.7 lakh | ~₹20.8 lakh |

| Total interest paid (10 yr) | ₹0 | ~₹21.6 lakh | ~₹13.0 lakh |

| 80E tax saving (30 percent slab, 8 yr cap) | ₹0 | ~₹6.0 lakh | ~₹3.6 lakh |

| FD post-tax growth retained (10 yr at 4.9 percent) | ₹0 (FD broken) | ~₹18.4 lakh | ~₹11.3 lakh |

| Net cost (interest minus 80E minus FD growth) | ₹0 cost but ₹30L cash gone | Rs -2.8 lakh (savings beat loan) | Rs -1.9 lakh (savings beat loan) |

Read that bottom row carefully. On a pure cash-cost basis Path A looks “free” because there is no interest. But the parents have given up ₹30 lakh of FDs that would have compounded for the next decade. Once you include the post-tax FD growth they walked away from, Path B and Path C both come out ahead financially. The loan, when 80E is applied and the savings are kept invested, is the cheaper path on paper.

What the table cannot capture is the human side. Path B leaves a 22-year-old with ₹21 lakh of interest to pay, which feels heavy regardless of the math. Path A leaves a 54-year-old with no FD cushion if a medical emergency hits at 58. Path C splits the load and preserves both retirement and the daughter’s manageable EMI. That is why the hybrid often wins in conversation even when Path B wins on a spreadsheet.

When tapping savings genuinely makes sense

The math above leans toward the loan, but there are five real situations where the loan is the worse call. I want to be specific because the bank manager will not tell you these.

The total cost is small. A ₹2 to 5 lakh course in India does not justify the paperwork, the credit check, or the long-term liability of an education loan. The 80E benefit on ₹5 lakh of borrowing over 7 years is roughly ₹50,000 to ₹70,000 in tax saved, which is not enough to compensate for the friction. If the parents have the money sitting at low yield, just pay.

Parents are 5 or fewer years from retirement with no other income. Section 80E only applies to the person who actually pays the interest. If a parent is the primary co-applicant and they retire in 3 years, their tax slab drops to zero in retirement, and the 80E benefit evaporates. In that scenario the loan is at its full headline cost while the savings would have been giving them 4.9 percent post-tax. The math flips.

The savings are in low-yield instruments (savings account, low-rate FD). If the family money is parked in a savings account at 3 to 4 percent or a very old FD at 5 percent, the post-tax return is roughly 2.1 to 3.5 percent. An education loan at 7.35 percent effective after 80E is much more expensive than that. Self-fund the part that is in low-yield parking. The RBI publishes weighted average deposit rates if you want to benchmark what your bank is paying versus the market on the RBI site.

The borrower is not in a taxable slab. 80E only saves tax if the person paying interest is in a tax slab. A graduate earning ₹4 lakh per year is below the basic exemption limit and pays no tax. They get zero benefit from 80E for those years. The deduction is use-it-or-lose-it per year, no carry-forward. The Income Tax India site has the exact wording at incometaxindia.gov.in. If both the student and the parent co-applicant are in low or zero slabs, the loan’s effective cost is the full headline rate.

The course is short and the earning trajectory is uncertain. A 1-year diploma in a field with weak placement statistics is not worth a ₹20 lakh loan that the graduate may struggle to service. If parents have the cash and the course is a calculated bet rather than a high-confidence ROI, self-funding contains the downside. The loan locks in a liability regardless of how the course turns out.

Faz's rule

Self-funding is not the cheap option. It is the simple option.

People say self-funding is free because there is no interest. There is always interest. It is just the interest you could have earned on that money parked somewhere else. Sometimes that opportunity cost is small and the simplicity is worth it. Sometimes it is large and you are quietly paying it without realising.

When a loan is mathematically better

The mirror cases are where the loan structurally wins, and these are more common than people assume. I see four.

The savings are in higher-yield investments that would be expensive to liquidate. Equity mutual funds held for over 1 year are taxed at 12.5 percent LTCG above the ₹1.25 lakh annual exemption. Long-term equity returns have historically averaged around 11 to 13 percent per the data SEBI publishes on registered mutual fund schemes at sebi.gov.in. Pulling out ₹30 lakh from an SIP that has been compounding for 8 years to pay tuition is destroying a compounding engine to replace cheaper debt. The loan at 7.35 percent effective is materially cheaper than the 9.6 percent post-LTCG return you are walking away from.

Parents are mid-career with strong income. A 45-year-old in the 30 percent slab with 15 working years left has both the income to claim 80E fully and the time to rebuild savings even if they did contribute. Keeping the FD intact and taking the loan preserves their liquidity buffer for their own retirement, medical needs, and any other shock. The 80E benefit on a ₹30 lakh loan over 8 years is roughly ₹6 lakh in tax saved, which is real money.

The course has high-confidence post-degree earning. A STEM Master’s at a known US or UK university with strong placement statistics, a CFA or actuarial qualification, an MBA at a top-30 institute: these have predictable salary outcomes. The borrower can comfortably service the EMI from year 2 of employment. The loan structure (moratorium during study, EMI from earning years) maps exactly to the cash flow reality.

The savings are the parents’ only retirement corpus. If the FD is the entire safety net and there is no separate pension, NPS, or second income, draining it for education is a real risk. The loan transfers the financial liability from the retiring parent to the earning child, which is structurally healthier even if it costs more on paper. The IBA model education loan scheme on the Indian Banks’ Association site is built around this principle: the borrower of record is the student, and repayment is from their post-graduation income.

The hybrid path most families end up at (and should consider first)

Almost every honest conversation I have on this topic ends at a hybrid. Pure self-fund leaves parents exposed. Pure loan loads the graduate with a heavy first-job EMI. The middle path uses savings for the portion that does not stress retirement, and a smaller loan covers the rest. Before you size either, shrink the bill itself: chasing scholarships for Indian students to study abroad can cut the principal that savings and a loan then have to split.

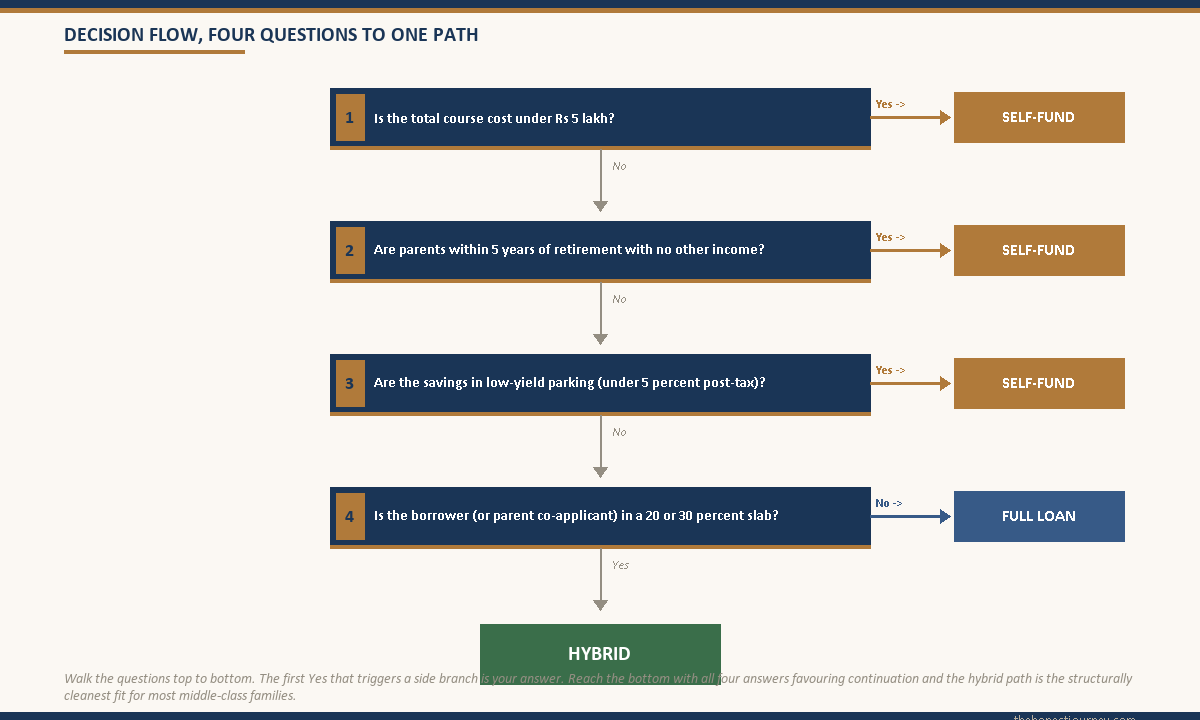

The rule I usually suggest is: parents contribute up to whatever they can without dropping their core retirement corpus below 10x annual expenses. So if their annual living cost is ₹6 lakh, they should not let their retirement corpus drop below ₹60 lakh. Whatever sits above that line is genuinely surplus and can fund education without future damage. The rest comes from a loan.

The other version of the hybrid is to take the loan upfront and prepay aggressively from savings once the moratorium is over. This gives you the tax benefit while interest accrues, then closes the loan faster than the original tenor once you have visibility on the graduate’s salary. Most public sector banks do not charge prepayment penalty on education loans per the IBA model scheme. You get the best of both: the 80E benefit, the savings staying invested during the study years, and a shorter actual repayment.

What the bank manager and the CA each get wrong

The bank manager who said “just break the FD, why pay interest” was looking at the headline numbers and stopping there. He did not factor in that the FD is taxed annually at the parent’s slab, while the loan interest is deductible at the same slab. He did not account for what compounding the ₹30 lakh at post-tax 5 percent over 10 years would do for the parent’s retirement (around ₹18 lakh of foregone growth). He gave the verbally simple answer.

The CA who said “always take the loan, 80E is free money” was right about the deduction but wrong to call it universal. If the parent co-applicant is retiring in 3 years and the student will earn below the taxable threshold for several years, the 80E benefit is largely theoretical. The full tax saving calculation only works when there is a high-slab earner paying the interest throughout the 8-year deduction window.

The honest answer always comes from running both paths for your specific numbers. Your slab, your spouse’s slab, your retirement timeline, your savings instruments, your child’s expected earning trajectory. These vary enough that the same ₹30 lakh decision has a different right answer for a 45-year-old senior engineer than for a 58-year-old shopkeeper, even if both have ₹35 lakh in FDs.

Faz's rule

The right answer is the one your family can live with for 10 years, not the one that wins on a spreadsheet by ₹50,000.

Spreadsheets are useful for showing direction. They do not capture the stress of a 58-year-old parent watching their FD drain or the weight on a 25-year-old of a ₹21 lakh EMI burden. Pick the path you can sleep with, then optimise within it. A slightly suboptimal path you actually follow beats a perfect path that creates family tension every Diwali.

The honest closing take

Education savings vs education loan is not a values question. It is a math question with four inputs: cost size, parents’ runway, savings post-tax yield, and the borrower’s tax slab over the next decade. Plug your numbers in and the answer is usually visible within an hour.

For most middle-class Indian families with a child going for a ₹20 to 40 lakh education abroad, the hybrid wins. Parents contribute the surplus above their core retirement corpus, the rest comes from an education loan with Section 80E claimed against the higher earner’s income, and the savings that stay in FDs or mutual funds keep compounding to support both retirement and any future shocks. The pure self-fund path makes sense for small costs and parents near retirement. The pure loan path makes sense when savings are working hard elsewhere and the borrower has a clear earning trajectory.

If you remember nothing else from this post, remember this: compare post-tax loan cost (after 80E) to post-tax savings yield (after slab tax on the interest). That single comparison, done honestly, gets you 80 percent of the way to the right answer. The rest is judgement about your family’s specific runway and tolerance. For the deeper version of either side, the full education loan guide walks through the loan mechanics, the 80E tax benefit post covers the deduction in detail, and the study abroad funding overview stitches all the routes together. The education loan vs self-funding post is the closest companion to this one.

If the savings are your parents savings, the risk is theirs too. Read how a family should size this bet.

FAQ

Should I use savings or take an education loan?

Use both if the cost is large and your savings are working at decent post-tax yield. The honest comparison is post-tax loan cost (around 7.35 percent for a 30 percent slab borrower after Section 80E) versus post-tax savings yield (around 4.9 percent for a 7 percent FD in the same slab). When savings yield post-tax is higher than the loan cost post-80E, keep savings invested and take the loan. When savings are in low-yield parking and the parent will not claim 80E (low or no income post-retirement), self-fund. For ₹20 lakh plus costs, a hybrid usually beats either extreme by ₹1 to 2 lakh over 10 years.

Is education loan better than withdrawing FD?

Often yes, but not always. A 7 percent FD post-tax for a 30 percent slab holder yields 4.9 percent. A 10.5 percent education loan post-80E for the same slab borrower costs 7.35 percent effective. On those numbers the loan is slightly more expensive than the FD yield, but you also keep the principal compounding and preserve liquidity. Over 10 years the retained FD compounding usually exceeds the net loan cost. If the FD yield is below 6 percent (older instruments) or the borrower is in a low tax slab where 80E does not help much, the calculus reverses and breaking the FD becomes the cleaner answer.

Does Section 80E make a loan cheaper than self-funding?

It makes the loan cheaper relative to the headline rate, not automatically cheaper than self-funding. The effective post-80E cost of a 10.5 percent loan for a 30 percent slab borrower is roughly 7.35 percent. If your savings would have earned more than that post-tax (equity mutual funds historically have, FDs often do not), keeping the savings invested and taking the loan is mathematically better. If your savings are in low-yield parking earning under 5 percent post-tax, self-funding is cheaper than the loan even after 80E. Run the comparison with your specific numbers, not the bank manager’s headline pitch.

Can I do partial loan and partial self-funding?

Yes, and it is what most families end up doing once they look at the math honestly. The common split is parents contribute whatever does not breach their core retirement corpus (typically 10 times annual expenses), and the rest comes from a loan. This preserves the parents’ safety net, gives the family the 80E benefit on the borrowed portion, and keeps the savings that remain in FDs or mutual funds compounding. Most banks process partial loans without issue: you simply tell them the loan amount needed, not the full cost of the course. The sanction letter reflects the loan amount and 80E applies to interest on that portion.

What if parents have enough savings to cover the full cost?

Having the savings does not mean you should use all of them. The question is what those savings are doing for the parents’ own retirement runway. If draining the FD takes the corpus below 10 times annual living expenses, the financial vulnerability that creates often outweighs the loan interest cost. If the parents have 25 times annual expenses saved and are still earning, paying directly is the simpler call. The middle case (15 to 20 times) is where a partial loan often makes sense. The other consideration is the borrower’s earning trajectory: a confident high-salary graduate should be the one carrying the EMI, not the retiring parent.

Does an education loan affect the CIBIL of the parent forever?

It appears on the co-applicant’s CIBIL report for as long as the loan is active and for several years after closure. On-time payments build the parent’s score. Late payments or default damage it. Once the loan is closed and the closure is reported correctly (verify after the final payment), it sits on the report as a closed account with positive history, which is constructive, not negative. The fear that an education loan “ruins” parent CIBIL is mostly misplaced for borrowers who service the EMI on time. The genuine risk is if the EMI gets missed during the graduate’s job-hunt phase, which is why the moratorium and a realistic earning trajectory matter at sanction time.

What happens to the 80E benefit if the parent retires during the repayment period?

The 80E deduction is claimed by whoever actually pays the interest from their taxable income. If a retired parent has no taxable income, they cannot use the deduction even if the loan is in their name. In that case the deduction is wasted for the years the parent is not earning. The fix is to have the loan in the student’s name with the parent as co-applicant, and have the student claim 80E once they are earning in a taxable slab. The 8-year deduction window starts from the year repayment begins, so timing the repayment start (post-moratorium) to coincide with the student’s earning years preserves the benefit.

Is there a rule of thumb for the right loan-to-self-fund split?

No single rule fits every family, but a useful starting frame is: parents contribute up to the surplus above 10 times their annual living expenses, and the loan covers the rest. So if annual living costs are ₹6 lakh and parents have ₹80 lakh saved, the surplus above 10x (₹60 lakh corpus floor) is ₹20 lakh. They can contribute ₹20 lakh comfortably. If the course costs ₹35 lakh, the remaining ₹15 lakh becomes the loan. This protects the retirement runway, lets the family claim 80E on the borrowed portion, and keeps the borrower’s EMI burden manageable from a starting salary.

Faz · The Honest Journey · 2026