Most Indian students fund study abroad with a mix, not one source. An education loan usually covers 60 to 80 percent, family savings or a sponsor close the gap, and a scholarship trims tuition by 10 to 30 percent if you win one. A two-year master’s runs ₹40 lakh to ₹80 lakh, so build the stack backwards from an EMI you can survive.

The first real shock of studying abroad is not the visa interview or the entrance exam. It is the number on the cost-of-attendance sheet. A two-year master’s in the US or UK lands somewhere between ₹40 lakh and ₹80 lakh once you stack tuition, living costs, flights, and insurance. Almost nobody pays that from one source. The families I have seen do it well are the ones who stopped looking for the single answer and built a mix instead.

So this post is the honest map of how to fund study abroad. Every source, how much it realistically covers, and the catch that the brochures skip. No upsell. Just the version I would give a younger cousin.

Here is a tight answer first, then the detail.

Most Indian students fund study abroad with a mix: an education loan covers the bulk (often 60 to 80 percent), family savings or a sponsor closes the gap and proves intent, a scholarship trims tuition by 10 to 30 percent if you win one, and part-time work covers daily living once you land. No single source carries the whole cost for most families.

For the full guide, read Studying Abroad From India: Cost and Funding Guide.

The realistic funding mix (start here)

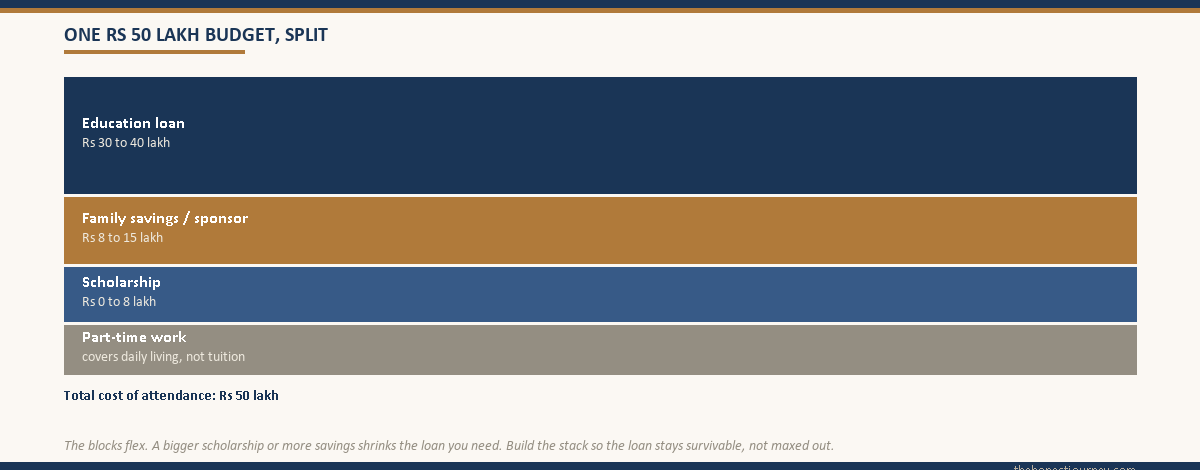

Before we go source by source, hold this picture in your head: funding study abroad is a stack, not a switch. The typical Indian family budget for a two-year overseas master’s costing ₹50 lakh looks roughly like this in practice.

| Source | Typical share of total cost | What it usually covers |

|---|---|---|

| Education loan | 60 to 80 percent | Tuition and a large slice of living costs |

| Family savings or sponsor | 15 to 30 percent | Margin money, the gap the bank will not fund, visa proof of funds |

| Scholarship or assistantship | 0 to 30 percent | Tuition discount, sometimes a stipend |

| Part-time work | Living costs after arrival | Rent, groceries, phone, transport (not tuition) |

Notice that the shares do not add up to a fixed 100 percent. They flex. A bigger scholarship shrinks the loan you need. A part-time job does not reduce the loan you sanction, but it changes how much of your living costs you draw from it. The skill is balancing the stack so the loan stays survivable, which is the decision I will keep pointing back to.

Faz's rule

Fund study abroad as a stack, not a single source. The goal is a survivable loan, not a maxed-out one.

Every rupee a scholarship or your savings covers is a rupee you do not borrow at 11 percent for ten years. Build the mix backwards from the EMI you can live with, not forwards from the cost sheet.

Education loan: the workhorse (60 to 80 percent)

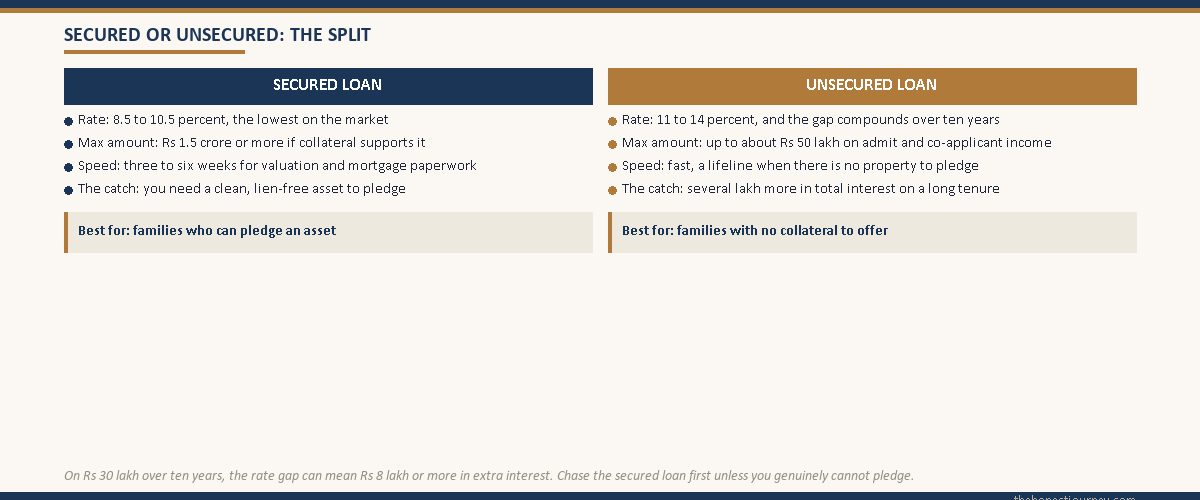

For most families, the education loan does the heavy lifting. Indian banks and NBFCs split loans into two kinds, and the difference shapes everything else in your plan.

Secured loans are backed by collateral: property, an FD, or other pledgeable assets. Public sector banks lead here. The rates are the lowest on the market, typically 8.5 to 10.5 percent, and the sanctioned amount can run to ₹1.5 crore or more if the collateral supports it. Margin money (the share you fund yourself) is usually 10 to 15 percent for abroad studies. The catch is time and friction: property valuation, legal verification, and mortgage paperwork can take three to six weeks, and not every family has a clean, lien-free asset to pledge.

Unsecured loans need no collateral. NBFCs and some private banks dominate this space, lending up to ₹50 lakh or so on the strength of your admit, the university’s ranking, and a co-applicant’s income. They are faster and a lifeline for families without property to pledge. The catch is the rate, usually 11 to 14 percent, and that gap compounds brutally over a ten-year tenure. On ₹20 lakh, the difference between 9.5 percent and 13 percent is several lakh in total interest.

Two things to lock in early. First, the interest you pay on an education loan qualifies for a deduction under Section 80E of the Income Tax Act, with no cap on the amount, for up to eight years from when repayment starts. If your co-applicant is on the old tax regime, that is real money back. Second, the loan sanction letter is also one of the strongest documents you can show for visa proof of funds, so the loan does double duty.

For the full secured-versus-unsecured breakdown, see the deeper page on education loans without collateral.

Faz's rule

A secured loan saves you lakhs in interest. Chase one before you settle for unsecured, unless you genuinely cannot pledge an asset.

The 3 percent rate gap between a public sector secured loan and an NBFC unsecured loan is not small. Over ten years on ₹30 lakh it can mean ₹8 lakh or more in extra interest. The collateral paperwork is worth the wait.

Scholarships and assistantships (0 to 30 percent)

Scholarships are the best money in the entire stack because you never repay them. They are also the most oversold. The honest framing: treat a scholarship as a discount you might win, not a plan you can count on. Build your loan as if you will get nothing, then celebrate and reduce the loan if you do.

The realistic categories are merit scholarships from the university (often a 10 to 50 percent tuition waiver, awarded with admission), external and government-linked schemes, and, in the US especially, teaching or research assistantships that pair a tuition waiver with a small stipend. Assistantships are gold but competitive and usually offered after you arrive, not before, so you cannot bank on them for your visa funds.

India’s National Scholarship Portal lists central and state schemes worth checking, though most are aimed at domestic or specific-category students. For abroad studies, your single highest-yield move is applying to universities that publish automatic merit awards, because that money is decided by your existing profile rather than a separate essay marathon.

The catch nobody mentions: a tuition-only scholarship does not cover living costs, and living costs are often half the total bill. A 30 percent tuition waiver on a ₹50 lakh budget might only shave ₹7 to 8 lakh off the real number once you account for rent and food being untouched. Useful, not transformative. For where to look first, see the guide to scholarships for Indian students to study abroad.

Family savings (15 to 30 percent)

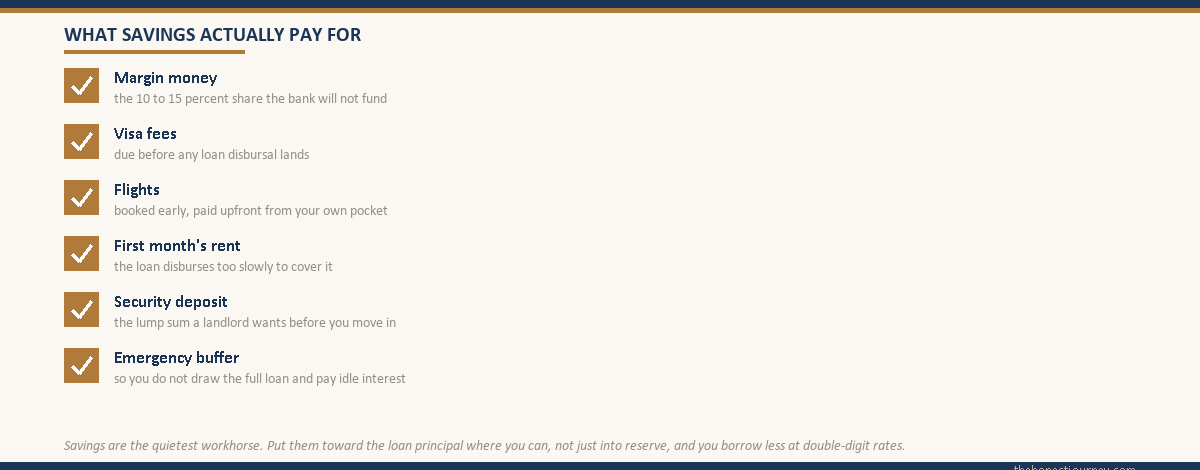

Savings are the quietest workhorse in the stack and the one most families underestimate. Even when you take a loan, you almost always need savings for the margin money the bank will not fund, the upfront costs the loan disburses too slowly to cover (visa fees, flights, first month’s rent, the security deposit on a flat), and the buffer that keeps you from drawing the full loan and paying interest on money sitting idle.

The smart move is to use savings to reduce the loan, not just to supplement it. Every rupee of your own money that goes toward tuition is a rupee you do not borrow at double-digit interest for a decade. If your family has ₹15 lakh available against a ₹50 lakh cost, putting it into the principal rather than holding it in reserve can cut your total repayment by several lakh.

There is also a remittance rule worth knowing. When you send your own money abroad under the Reserve Bank of India’s Liberalised Remittance Scheme, you can remit up to USD 250,000 per financial year per person, and education-related remittances funded by a loan get more favourable TCS treatment than self-funded ones. That tax angle quietly nudges some families to route more through the loan than they first planned.

Sponsor (closes the gap and proves intent)

A sponsor is usually a parent, but it can be a sibling, an uncle, or another close relative with the income and willingness to back you. In funding terms, a sponsor plays two roles. First, as a loan co-applicant whose income and credit profile is what actually gets your unsecured loan sanctioned, the bank lends against their FOIR, not yours. Second, as the named source in your visa proof of funds, where a sponsorship affidavit plus their bank statements and income proof tells the embassy who is paying.

The catch is that a sponsor is only as strong as their documentation. An affidavit on stamp paper means nothing on its own. The embassy and the bank both want to see the sponsor’s income tax returns, bank statements showing seasoned funds (not a sudden large deposit days before you apply), and a clear relationship proof. A weak or undocumented sponsor is one of the more common reasons a funding plan that looked fine on paper falls apart at the visa stage.

Part-time work (covers living, never tuition)

Part-time work is the source students overestimate the most. The honest rule: budget for your degree as if you will earn nothing from a job, then treat any part-time income as a way to ease living costs, not as a tuition source.

Most student visas cap work at around 20 hours per week during term, with full-time allowed in vacations. At a typical student wage, that covers groceries, a phone bill, transport, and maybe a slice of rent. It does not touch tuition, and it cannot, because the hours are capped precisely so study comes first. Counting on a part-time job to fund a meaningful chunk of a ₹50 lakh degree is the single most common funding miscalculation I see, and it is the kind that leaves students taking on extra debt mid-course when the maths does not hold.

There is an exception worth naming. A formal assistantship (the teaching or research role mentioned earlier) is different from a casual part-time job because it often comes with a tuition waiver attached. That is structural funding, not pocket money. For the practical limits and what is realistic, see the guide to part-time work while studying abroad.

Faz's rule

Plan your degree as if a part-time job earns you nothing. Anything it brings in is a bonus, not a budget line.

Twenty hours a week at a student wage covers your groceries and phone, not your fees. Families who count on part-time income to pay tuition almost always end up borrowing more midway. Treat it as relief, never as a plan.

How to pick the right mix for you

This is an overview, not a decision page, so I will keep this short and point you to the deeper read. The big strategic question is how much to borrow versus how much to fund yourself, and that genuinely deserves its own analysis of your numbers, your risk appetite, and your expected starting salary. I have written that out in full on the education loan versus self-funding page, and I will not re-argue it here.

The one principle that ties the whole stack together: build your mix backwards from the EMI you can survive, not forwards from the cost sheet. Start with the monthly repayment your likely first salary can carry at, say, 35 to 40 percent of take-home. Work back to the loan that produces. Then fill everything above that line with savings, scholarship, and sponsor support. If the gap is still too large, the honest answer is sometimes a cheaper destination rather than a bigger loan. The list of cheapest countries to study abroad for Indian students exists for exactly this reason.

The honest closing take

There is no clever single source that makes study abroad cheap. The loan is the workhorse, savings and a sponsor close the gap and prove your funds to the embassy, a scholarship is a discount you chase but never assume, and a part-time job keeps the lights on once you land. Anyone selling you one magic route, a guaranteed scholarship, a no-collateral loan with no catch, a job that pays your fees, is selling, not advising.

The families who get this right are unglamorous about it. They run the numbers, pledge an asset if they can to get the cheaper loan, put their savings into the principal instead of hoarding it, and size the loan to a repayment they can actually carry. Do that, and the cost sheet stops being a shock and becomes a plan. Read the loan-versus-self-funding page next, because that is where the real decision lives.

FAQ

How do Indian students fund studying abroad?

Most fund it with a mix rather than one source. An education loan typically covers 60 to 80 percent of the cost, family savings or a sponsor close the remaining gap and serve as visa proof of funds, a scholarship may trim tuition by 10 to 30 percent if won, and a part-time job covers daily living costs after arrival. The right blend depends on what assets you can pledge, your co-applicant’s income, and the loan EMI your expected salary can carry.

What is the cheapest way to fund study abroad?

The cheapest funding is money you do not repay or repay at the lowest rate. In order: a scholarship or assistantship (free), your own savings put toward principal (no interest), then a secured loan from a public sector bank at 8.5 to 10.5 percent rather than an unsecured loan at 11 to 14 percent. Choosing a more affordable destination also lowers the total you need to fund, which is often a bigger saving than any single source decision.

Can I study abroad without a loan?

Yes, if your savings, a sponsor, and a scholarship together cover the full cost, but this is uncommon for the ₹40 lakh to ₹80 lakh budgets typical of a Western master’s. Fully scholarship-funded routes exist (a full assistantship in the US, for example) but are highly competitive and usually confirmed after arrival, so you still need provable funds for the visa first. For most families, a partial loan is part of the plan even when savings are strong.

How much can a part-time job cover while studying abroad?

Realistically, it covers living costs, not tuition. Most student visas cap work at around 20 hours a week during term, which at a typical student wage covers groceries, phone, transport, and perhaps part of your rent. It cannot fund a meaningful share of a large tuition bill. The exception is a formal teaching or research assistantship, which often pairs a stipend with a tuition waiver and is genuine structural funding rather than casual work.

What funding mix do most families use?

A common pattern for a ₹50 lakh two-year master’s is a loan covering 60 to 80 percent, family savings or a sponsor covering 15 to 30 percent (including the bank’s margin money and upfront costs the loan disburses too slowly to cover), and a scholarship reducing the loan further if won. Part-time work then covers living costs after arrival. The exact split flexes with each family’s assets and the scholarships secured.

Do I need to show all the funding upfront for a visa?

You need to prove you can cover the full cost of attendance, which usually means showing tuition plus living costs for at least the first year. A loan sanction letter, seasoned bank balances or fixed deposits, and a sponsor’s documented income all count. What does not count is unverified cash or a sudden large deposit made just before applying, since most countries require funds to be seasoned. The sources differ in form, but together they must add up to the required amount.

Is a scholarship enough to study abroad on its own?

Rarely. Most merit scholarships are partial tuition waivers of 10 to 50 percent and leave living costs untouched, and living costs are often half the total bill. A 30 percent tuition waiver on a ₹50 lakh budget might only reduce the real cost by ₹7 to 8 lakh. Full-ride scholarships and funded assistantships do exist but are scarce and competitive. Treat any scholarship as a discount that reduces your loan, not as a complete funding plan.

How much money can I send abroad to fund my studies?

Under the Reserve Bank of India’s Liberalised Remittance Scheme, you can remit up to USD 250,000 per financial year per person, which is well above what most students need. Education-related remittances funded by an education loan also receive more favourable tax-collected-at-source treatment than self-funded remittances above the threshold. This tax difference is one reason some families route a larger share through the loan than they originally intended. Check the current TCS rates at the time you remit.

Faz · The Honest Journey · 2026