A loan against FD for education is a secured overdraft or demand loan from your bank, priced at 1 to 2 percent above your FD rate, with up to 90 percent of the deposit value available the same day you ask. On a ₹10 lakh FD earning 7 percent, you can usually draw up to ₹9 lakh at around 8 to 9 percent interest, with no academic verification, no co-applicant FOIR check, and no moratorium. The FD keeps earning interest in the background. The catch: no Section 80E deduction, shorter tenure, and your deposit stays locked as collateral.

I have seen this product solve real problems three weeks before a semester starts. I have also seen it quietly cost more than a proper education loan would have, because nobody ran the comparison on paper. The branch pitch is always “Your FD is just sitting there.” Convenient framing, not always correct.

This post walks through how a loan against fixed deposit (LAFD) actually works for education funding, what it really costs over a 2 to 4 year window, and where it beats a regular education loan versus where it loses.

More on collateral and how much you can borrow: the education loan for abroad studies without collateral post, the margin money education loan explained post, and the maximum education loan amount india post.

What a loan against FD for education actually is

A loan against FD is the simplest secured loan an Indian bank offers. You pledge a fixed deposit. The bank gives you a credit line or demand loan worth up to 90 percent of the deposit value. The deposit keeps earning its contracted rate. You pay interest on whatever you draw, typically 1 to 2 percent above the FD rate.

Two structures exist. An overdraft (OD) gives a credit limit equal to 90 percent of the FD, and you pay interest only on the amount and days used. A demand loan is a lump-sum with full interest from day one. For education where you draw money across semesters, the overdraft almost always wins. SBI, HDFC Bank and most banks offer both, under the RBI and IBA framework on advances against deposits.

Disbursal is usually same day if the FD is with the same bank. Sign the lien marking, the limit reflects in a few hours. No academic file, no admission letter, no university verification.

Faz's ruleThe price you pay for LAFD speed is that the FD is now frozen as collateral for the life of the loan.

Your ₹10 lakh deposit still shows up on your statement and still earns interest, but you cannot break it, transfer it, or use it for anything else until the loan against it is closed. People forget this and then panic six months later when an emergency hits and the FD they thought was a backup is actually pledged.

The rate math: why LAFD looks cheap and what the real cost is

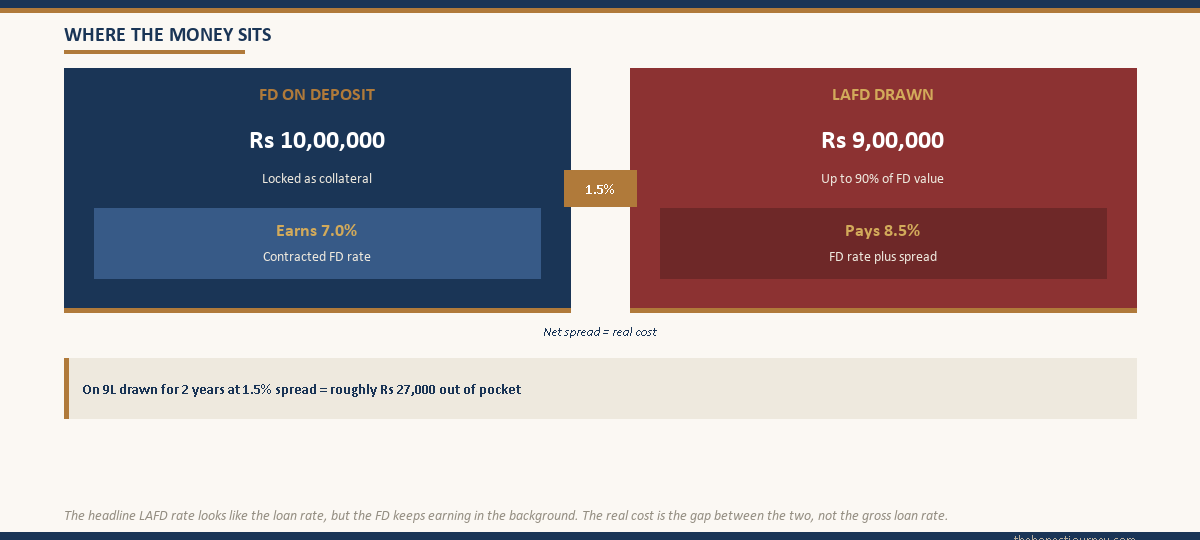

The headline rate on LAFD is genuinely attractive. If your FD earns 7 percent, the loan against it sits at 8 to 9 percent. Compare that to an unsecured NBFC education loan at 11 to 14 percent, or a collateral-backed public sector education loan at 8.5 to 10.5 percent, and LAFD looks like the obvious winner.

But headline rates are not the full picture. The FD is still earning its 7 percent in the background. Your true net cost is the spread, the 1 to 2 percent gap between what the FD earns and what the loan charges, plus the loss of optionality on the deposit.

| Scenario | FD rate | LAFD rate | Net spread cost | On ₹9L drawn for 2 years |

|---|---|---|---|---|

| FD with parent bank, OD | 7.0% | 8.5% | 1.5% | ₹27,000 |

| FD with parent bank, OD | 7.0% | 9.0% | 2.0% | ₹36,000 |

| Senior citizen FD, OD | 7.5% | 9.0% | 1.5% | ₹27,000 |

| Tax-saver FD (locked), demand loan | 6.8% | 8.8% | 2.0% | ₹36,000 |

The “net spread cost” is what you actually pay out of pocket, because the FD keeps earning interest that offsets part of the loan cost. On a ₹9 lakh draw for two years at a 1.5 percent spread, the real net cost is roughly ₹27,000. Genuinely small compared to education loan interest math.

The catch: this assumes you draw close to the full limit. If you take a demand loan of ₹9L upfront and let half sit in savings at 3 percent, you are paying 9 percent on money earning 3 percent. Product structure matters as much as the rate.

LAFD vs regular education loan: side by side

For the loan against FD for education decision, the only honest comparison is against a regular education loan, because that is the alternative most families consider. The rate is part of it. The terms, the tax treatment, and the tenure are the rest.

| Feature | Loan against FD | Education loan (secured) | Education loan (NBFC, unsecured) |

|---|---|---|---|

| Interest rate | FD rate + 1 to 2% | 8.5 to 10.5% | 11 to 14% |

| Max loan | Up to 90% of FD value | Up to ₹1.5 crore (with collateral) | Up to ₹50 to 75 lakh |

| Disbursal time | Same day | 3 to 8 weeks | 2 to 4 weeks |

| Moratorium | None (interest from day 1) | Course + 6 to 12 months | Course + 6 to 12 months |

| Tenure | Linked to FD maturity, usually 1 to 5 years | 10 to 15 years | 10 to 12 years |

| Section 80E benefit | No | Yes | Yes |

| Co-applicant / FOIR check | No | Yes | Yes |

| Processing fee | Nil or nominal | 0.5 to 1% | 1 to 2% |

| Collateral status | FD pledged, locked | Property or FD or deposit pledged | None |

Two rows in that table matter more than the rest. The first is moratorium. A regular education loan lets you defer EMIs until 6 to 12 months after the course ends (the interest still accrues and capitalises, covered in the moratorium period interest post). LAFD has no such grace. Interest is debited monthly from the day you draw the first rupee.

The second is Section 80E, which gives an unlimited deduction on education loan interest for 8 years from repayment start. LAFD interest does not qualify, even if every rupee went to tuition. For a co-applicant in the 30 percent old-regime bracket paying ₹1.5 lakh of interest a year, that deduction is ₹45,000 in tax saved. LAFD does not give you that.

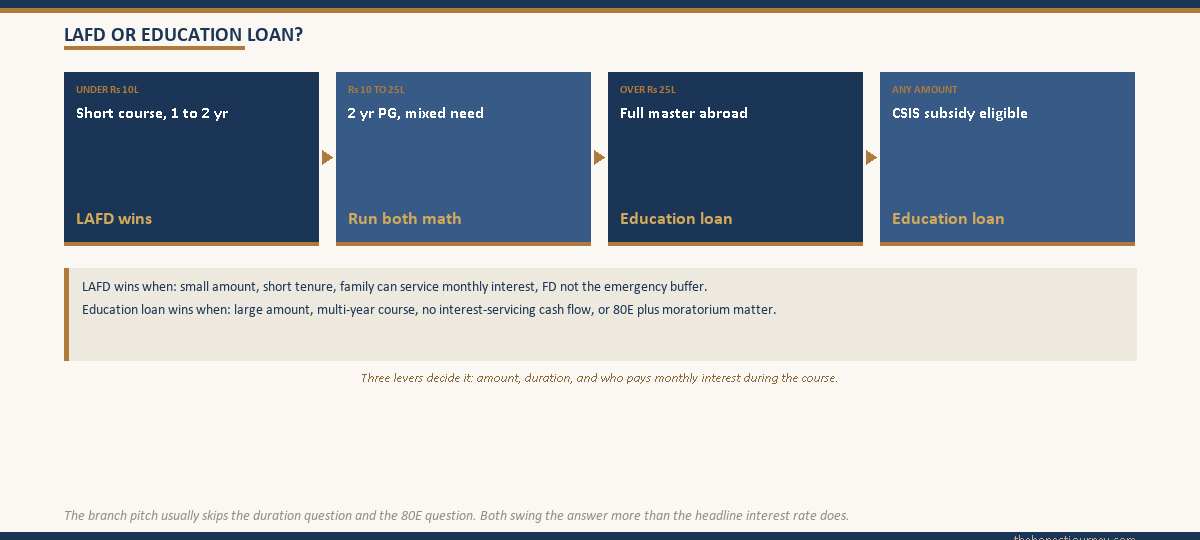

Faz's ruleLAFD wins on rate and speed. Education loan wins on tenure, tax, and breathing room. The right choice depends on how long the money needs to be deployed.

If you need ₹6 lakh for 18 months and you have an existing FD, LAFD almost always wins. If you need ₹25 lakh across a 2-year master’s with no real way to service interest during the course, an education loan with moratorium and 80E is almost always cheaper in net out-of-pocket terms.

When LAFD is the right call

There are specific situations where a loan against FD is genuinely the better instrument. I am going to list them concretely because the branch pitch tends to make it sound right for everything, and it is not.

Short-duration funding needs. If the requirement is ₹3 to 10 lakh for a 12 to 24 month window (a one-year PG diploma, an executive certificate, a short course with bridge funding), LAFD is usually cheaper. The 80E benefit takes years to accumulate, and the moratorium advantage shrinks on a short course because the deferred interest pile stays small.

Bridge funding before disbursal. Education loan sanctions take 3 to 8 weeks for public sector banks. Tuition deadlines, visa fees, blocked account funding for Germany all have their own clocks. An LAFD for 4 to 8 weeks at 8.5 percent costs maybe ₹3,000 to ₹6,000 on a ₹5 lakh draw. That is a rounding error compared to missing an admission deadline.

You were not going to break the FD anyway. If the FD is a long-term family deposit nobody was planning to break, pledging it (with the depositor’s full informed consent) is rationally cheaper than liquidating it. Premature FD break usually costs a 0.5 to 1 percent rate penalty plus loss of the contracted rate, often worse than paying the LAFD spread. For more on the funding-source decision, see education loan vs self funding.

When LAFD is the wrong call

The reverse situations matter more, because this is where the mistake gets expensive.

Large amounts across multi-year programs. A 2-year US or UK master’s with ₹40 to 60 lakh of total need is not an LAFD problem. The FD value required to back that is enormous, the tenure mismatch with the FD maturity gets awkward, and the absence of 80E plus moratorium makes the education loan structurally cheaper in net terms even at a higher headline rate.

You do not have anyone to service monthly interest during the course. Education loan moratoriums exist because students typically do not have income during the course. LAFD interest is debited monthly. If neither the student nor the family has the cash flow to service it while classes are running, the LAFD turns into a slowly compounding overdraft that eats into the FD value itself. This is where people get hurt.

The FD is the family emergency fund. Pledging an emergency fund converts it from a buffer into a frozen asset. If a medical event or job loss hits during the course, the family no longer has the cushion they thought they had. The secured vs unsecured education loan conversation belongs here too.

You qualify for a CSIS subsidy. If parental income is under the CSIS threshold (₹4.5 lakh, being revised under PM Vidyalakshmi), the government pays the moratorium interest on the education loan. LAFD has no such subsidy. Taking LAFD here is forfeiting a benefit you qualify for.

The mechanics: lien marking, FD safety, what happens at default

A few practical points that almost no one explains at the branch.

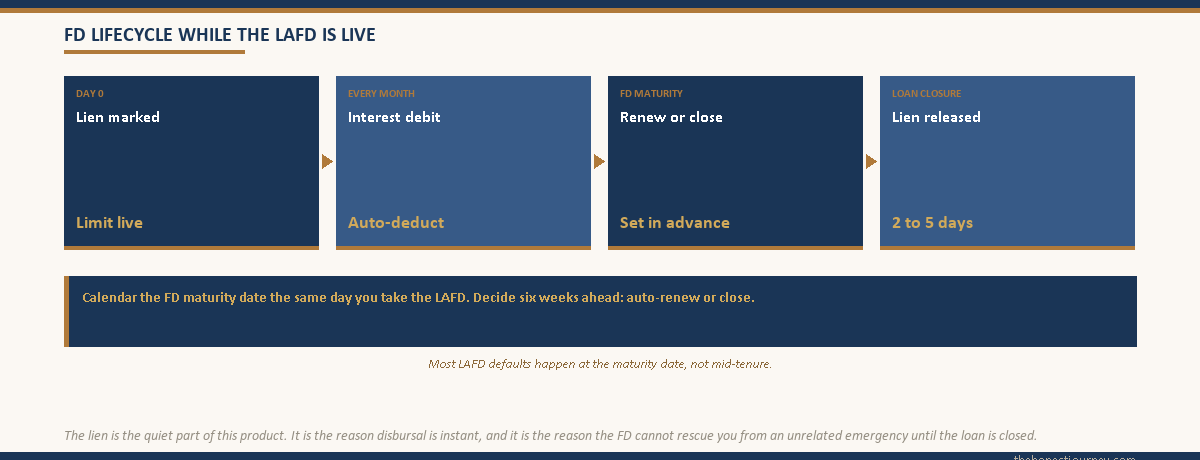

The FD is “lien marked.” It stays in your name and keeps earning its rate, but the bank places a legal hold preventing premature withdrawal, transfer, or use as collateral elsewhere. The lien is released within 2 to 5 working days of full repayment.

If the FD matures while the loan is outstanding, the bank either auto-renews the FD (continuing the lien) or uses the maturity proceeds to close the loan and return the balance. This is set in the loan agreement, not negotiable mid-term. Check the clause before signing.

On default, the bank does not file a recovery suit. It invokes the lien, breaks the FD (with a 0.5 to 1 percent rate penalty), recovers the loan plus accrued interest, and credits the balance back. Faster and cleaner than education loan recovery from the bank’s side. From the borrower’s side, the FD is genuinely at risk if interest servicing stops, and the buffer disappears overnight.

Faz's ruleRead the auto-renewal clause and the maturity-handling clause in the LAFD agreement before signing. Most defaults from this product happen at the FD maturity date when borrowers were not expecting the loan to close in one shot.

Banks do not always send a heads-up before the maturity date triggers the loan closure. Calendar the FD maturity date the same day you take the LAFD, and decide six weeks in advance whether you want renewal or closure.

Tax: the missing 80E and what it actually costs you

Section 80E of the Income Tax Act allows an unlimited deduction on interest paid on an education loan from a scheduled bank or notified financial institution, for up to 8 years from the start of repayment. The loan must be sanctioned as an education loan for higher education. Official text on incometaxindia.gov.in.

An LAFD does not meet that definition. It is a loan against a deposit, not an education loan, and the interest is not deductible even if every rupee went to tuition. For a family in the 30 percent old-regime bracket paying ₹1.2 lakh of education loan interest a year, the 80E saving is ₹36,000 annually, roughly ₹2 to 3 lakh across the 8-year window. That is real money LAFD borrowers never see.

The new tax regime does not offer Section 80E either, so for families on the new regime, this gap closes and LAFD becomes more competitive like-for-like. Whoever pays the interest needs to be on the old regime for 80E to be the deciding factor.

The honest verdict

Loan against FD for education is a precision tool. It is genuinely cheaper than a regular education loan when the amount is small (under ₹10 lakh), the duration is short (under 24 months), the family has income to service monthly interest while the student is in class, and the FD was not the family emergency buffer. In those cases the 1.5 to 2 percent net spread is the cheapest cost of capital in Indian retail banking.

It is the wrong tool when the funding need is large, the duration is multi-year, there is no cash flow to service monthly interest, or the family qualifies for CSIS. The absence of moratorium and 80E quietly makes LAFD more expensive than a proper education loan, even at the higher headline rate.

The branch pitch rarely makes this distinction. The product is profitable for the bank, low-risk, fast to disburse. For the family it is a calculation that needs both columns filled in honestly: rate, tenure, tax, moratorium, FD lock-up, and the use of the money. See also how to fund study abroad and the education loan against property alternative.

FAQ

Can I take a loan against my FD for education expenses?

Yes. Every major Indian bank (SBI, HDFC, ICICI, Axis, PNB, BoB) offers loans against fixed deposits with no restriction on end use, so funds can go to tuition, living expenses, visa fees, or any other education cost. No admission letter, no university verification, no academic documents. The FD is the collateral and up to 90 percent of its value is available, usually same day.

What interest rate applies on a loan against FD?

The rate is typically 1 to 2 percent above the FD rate itself. So if your FD earns 7 percent per annum, the loan against it will be priced between 8 and 9 percent. Public sector banks usually stay at 1 percent above, private banks at 1.5 to 2 percent above. The exact spread depends on whether you opt for an overdraft facility (interest only on amount drawn) or a demand loan (interest on full sanctioned amount). Published spreads are on each bank’s official site.

How much can I borrow against my FD?

Most banks lend up to 90 percent of the FD’s principal value, a few private banks cap at 85 percent. So on a ₹10 lakh deposit, the available credit limit is typically ₹8.5 to ₹9 lakh. Accrued FD interest is not always included. The exact percentage and any minimum FD value requirement (often ₹25,000 or ₹50,000) are bank-specific and listed in the loan against deposit terms on the bank’s website.

Is the interest on a loan against FD tax deductible under Section 80E?

No. Section 80E applies only to interest paid on a loan sanctioned by a scheduled bank or notified financial institution as an education loan. A loan against fixed deposit is classified as a loan against security, not an education loan, even when funds are used entirely for higher education. The interest is not deductible regardless of end use. This is one of the most overlooked cost differences between LAFD and a regular education loan, especially for families in the old tax regime.

How fast can I get a loan against FD disbursed?

If the FD is with the same bank where you hold a savings account, disbursal is typically same day. You visit the branch (or apply online), sign the lien marking authorisation, and the credit limit reflects within a few hours. If the FD is with a different branch of the same bank, it may take 1 to 2 working days for the lien to activate. No external verification, no processing delays.

What happens to my FD when I take a loan against it?

The FD stays in your name and continues to earn its contracted rate until maturity. The bank places a lien on it, so it cannot be prematurely withdrawn, transferred, or used as collateral elsewhere until the loan is fully repaid. The lien is removed within 2 to 5 working days of closure. At FD maturity, the bank either auto-renews the deposit (continuing the lien) or uses the proceeds to close the loan, depending on the loan agreement.

Can I take a loan against a tax-saver FD or senior citizen FD?

Loans against tax-saver FDs (5-year lock-in deposits eligible under Section 80C) are generally not allowed during the lock-in, because Income Tax rules prohibit pledging them. Senior citizen FDs are eligible like any normal FD, and because senior rates are typically 0.5 percent higher, the net spread cost (loan rate minus FD rate) is the same and the math works identically.

What happens if I default on a loan against FD?

The bank does not need to file a recovery suit or go through standard NPA process. It invokes the lien, breaks the deposit (with a 0.5 to 1 percent rate penalty), recovers loan plus accrued interest, and credits the balance back. CIBIL impact is usually limited compared to unsecured loan default, but the FD itself is gone. An LAFD default is contained within the FD, which is both its safety feature for the bank and its real risk for the family losing the deposit.

Faz · The Honest Journey · 2026