The maximum education loan amount in India depends on collateral, course, and co-applicant strength, not on a single official ceiling. Under the IBA model scheme, PSU banks lend up to ₹10 lakh unsecured for domestic study and ₹20 lakh unsecured for abroad. With tangible collateral, PSU caps stretch to ₹40 lakh domestic and ₹1.5 crore abroad. NBFCs like Avanse, Credila and Auxilo can go to ₹1 crore or more unsecured for premier institutes. What you actually get is usually well below the bank’s theoretical ceiling.

I have watched parents walk into a PSU branch convinced they qualify for ₹50 lakh because a friend got ₹50 lakh. They walk out with a ₹18 lakh sanction. Nothing in the rule book changed between those two cases. The co-applicant’s income, the institute on the offer letter, and the collateral on the table did.

This post breaks down the maximum education loan amount in India by lender type, by collateral status, and by the variables that actually decide your sanction. The bank’s brochure ceiling is the easy number. The real number is a different calculation.

More on collateral and how much you can borrow: the loan against FD for education post and the margin money education loan explained post.

The IBA model scheme caps and where they come from

The maximum education loan amount in India for PSU banks is governed by the Indian Banks’ Association (IBA) model education loan scheme, which most public sector banks adopt with small variations. The IBA framework sets two unsecured ceilings: ₹10 lakh for studies inside India and ₹20 lakh for studies abroad. These are the numbers you can borrow without pledging property, FD, or other tangible security, against a co-applicant guarantee alone.

Above those caps the loan becomes secured. With tangible collateral (residential property, commercial property, FD, LIC policy with surrender value), PSU banks lend up to ₹40 lakh for domestic study and ₹1.5 crore for abroad. Some banks (the SBI Global Ed-Vantage scheme in particular) publish higher abroad ceilings up to ₹1.5 crore for premier institutes with strong collateral. The full SBI scheme detail is on sbi.co.in.

The RBI sets the priority-sector classification thresholds (₹20 lakh for individuals) and the broad prudential rules, but does not cap the maximum education loan amount in India directly. The cap comes from the IBA scheme and each bank’s board-approved policy.

| Bank category | Unsecured cap (domestic) | Unsecured cap (abroad) | With collateral (domestic) | With collateral (abroad) |

|---|---|---|---|---|

| PSU bank (IBA scheme) | ₹10 lakh | ₹20 lakh | Up to ₹40 lakh | Up to ₹1.5 crore |

| SBI Global Ed-Vantage | Not applicable | ₹7.5 lakh threshold (then secured) | Not applicable | Up to ₹1.5 crore |

| Private bank (Axis, ICICI) | ₹40 lakh (varies by institute) | ₹50 to 75 lakh (premier institute) | Up to ₹1 crore | Up to ₹2 crore |

| NBFC (Avanse, Credila, Auxilo) | ₹50 to 75 lakh | ₹1 crore or higher (premier institute) | Up to ₹1.5 crore | Up to ₹3 crore |

Two things to read from that table. First, the secured cap is roughly 5 to 8 times the unsecured cap across every category. Collateral is the single biggest lever on the maximum education loan amount in India. Second, NBFC numbers look generous, but they come with interest rates of 11 to 14 percent against PSU rates of 8.5 to 10.5 percent. The “higher max” is partly priced into the rate.

Faz's ruleThe brochure number is the ceiling, not the sanction. Banks sanction what your co-applicant's income and collateral support, not what the scheme allows.

I tell families to ignore the headline cap and run the actual numbers: monthly EMI affordable by the co-applicant, FOIR check, collateral valuation. The sanction that comes out of that math is almost always lower than the scheme cap. Use the cap as the upper bound, never as the expectation.

What actually decides the number you get

The bank applies three filters before it agrees to a loan amount. Each one can pull the maximum education loan amount in India down to a fraction of the scheme ceiling. The course cost is just the starting input.

Co-applicant income and FOIR. The bank calculates a Fixed Obligations to Income Ratio (FOIR), usually capped at 50 to 65 percent for the co-applicant. The proposed EMI plus existing EMIs cannot exceed that share of monthly income. For a ₹30 lakh loan at 10.5 percent over 10 years, the EMI is roughly ₹40,500. The co-applicant needs net monthly income of roughly ₹70,000 to 90,000 just to clear FOIR after the existing EMIs. Lower income, lower sanction.

CIBIL score. PSU banks usually look for a co-applicant CIBIL of 650 and above, private banks and NBFCs prefer 700 and above. Below 650 the file is either rejected or the sanctioned amount is cut sharply, sometimes by half. The student’s own CIBIL (if any) matters less for first-time borrowers but matters for working students. See the detailed treatment in our education loan India complete guide.

Collateral valuation. If you pledge property, the bank conducts an independent valuation. The loan amount is capped at 70 to 80 percent of the valuation, not the market price you think the property is worth. A property you believe is worth ₹1 crore might value at ₹80 lakh by the bank’s valuer, supporting only ₹60 lakh of loan. Detail in education loan against property.

Sanction matrix by course type and institute tier

This is the table I wish someone had handed me on day one. It maps how the course you pick and the tier of your institute move the typical sanction, and what collateral you should expect to pledge. These are indicative ranges, not quotes. They shift with every lender revision, your co-applicant income, and your profile, so confirm the live numbers officially before you plan around them.

| Course type and institute tier | Typical sanction range (domestic) | Typical sanction range (abroad) | Collateral expectation |

|---|---|---|---|

| General degree (non-premier institute) | Up to ₹10 to 15 lakh | Up to ₹20 to 30 lakh | Collateral usually needed above the unsecured cap (₹7.5 to 10 lakh) |

| Professional course (MBA, MBBS, engineering) | ₹15 to 30 lakh | ₹30 to 60 lakh | Collateral-free slice first, security for the balance |

| Premier institute (top-ranked, strong placements) | Up to ₹30 lakh (domestic fees rarely cross this) | ₹60 lakh to ₹1 crore for full cost of attendance | Higher unsecured limits, ₹40 to 50 lakh possible for strong profiles, balance secured |

Read it the honest way. A premier institute lifts your unsecured slice, but it does not erase the collateral conversation once your total crosses what the lender will give without security. Plan from the collateral-free figure up, not from the headline maximum down.

The premier institute exception

The single biggest jump in the maximum education loan amount in India comes from the institute on your offer letter. PSU banks, private banks, and NBFCs all publish a list of “premier institutes” (sometimes labelled List A, AA, or Tier 1). Admission to a premier institute is treated as collateral in itself, because the placement record statistically de-risks the loan.

For premier institutes, the unsecured cap commonly stretches from ₹20 lakh to ₹50 to 75 lakh on PSU banks, and ₹1 crore plus on NBFCs. The list is bank-specific and updated periodically. IIM A/B/C, IIT/IIM/NIT, AIIMS, ISB, top US Ivy League and select UK Russell Group universities are on most premier lists. A second-tier university in the same country usually is not. More on the funded list mechanics in our education loan for abroad studies without collateral post.

| Institute tier | PSU unsecured cap (abroad) | NBFC unsecured cap (abroad) | Typical sanction range |

|---|---|---|---|

| Premier (e.g. MIT, Stanford, Oxford, Cambridge, Wharton) | ₹50 lakh plus | ₹1 crore or higher | ₹60 lakh to ₹1 crore |

| Top tier (e.g. Imperial, UCL, NYU, USC) | ₹30 to 40 lakh | ₹60 to 75 lakh | ₹35 to 55 lakh |

| Mid tier (e.g. typical state university Master’s) | ₹20 lakh | ₹40 to 50 lakh | ₹20 to 35 lakh |

| Not on list / unranked | Often case-by-case, may be declined | ₹25 to 40 lakh max | ₹15 to 25 lakh |

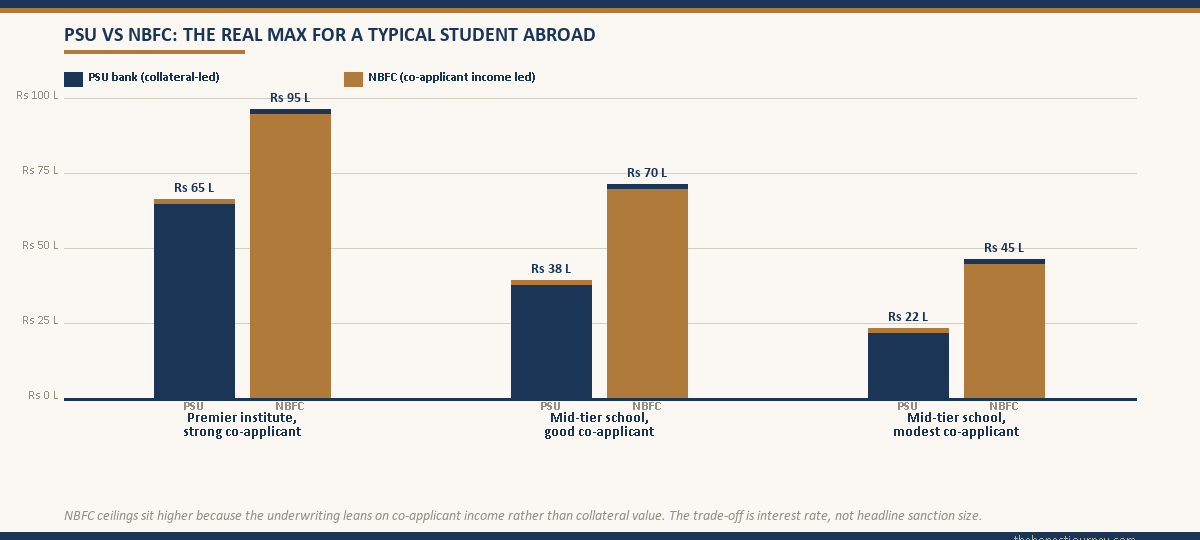

The honest read: the same student with the same co-applicant and the same collateral can get a 3 to 4x larger sanction by enrolling at a premier institute versus a mid-tier one. This is not a fairness statement. It is what the lending models actually do.

NBFC ceilings: what the high numbers really mean

NBFC publicity often quotes ₹1 crore, ₹1.5 crore, even ₹2 crore as the maximum education loan amount in India for abroad study. The numbers are technically accurate. They obscure three real-world points.

First, NBFC rates run 11 to 14 percent against PSU 8.5 to 10.5 percent. On a ₹50 lakh loan over 12 years, the rate difference alone is roughly ₹12 to 18 lakh of extra interest. The “higher max” comes at a meaningful cost.

Second, NBFC sanctions still apply the FOIR and CIBIL filters. The brochure cap of ₹1 crore is realisable only with a co-applicant earning ₹1.5 to 2 lakh net per month plus collateral or premier-institute backing. The student walking in with a ₹60,000 income parent and a mid-tier US university offer will get nowhere near ₹1 crore from an NBFC either.

Third, NBFCs market and disburse faster than PSU banks but are not bound by the IBA scheme’s borrower protections (CSIS subsidy eligibility, IBA tenure rules, RBI priority sector classification benefits). The trade is speed and higher cap for higher cost and weaker structural protection.

Faz's ruleAn NBFC ₹1 crore sanction is not a free upgrade over a PSU ₹30 lakh sanction. The higher cap is paid for in interest, in 80E ceiling utility, and in the absence of subsidy eligibility.

I have seen families pick the bigger NBFC number and ship ₹15 lakh extra interest over 12 years because nobody compared the two paths in full. Always run the total cost calculation, not the headline sanction. The PSU loan plus self-funding the gap is often the cheaper combined path.

The course-cost cap and what counts as “expense”

The other ceiling on the maximum education loan amount in India is the documented total cost of the course. Banks fund a defined set of heads: tuition, hostel, examination/library/laboratory fees, books, equipment, uniforms, two-way travel, study tours/project work/thesis, deposit/refundable caution money, and reasonable living expenses for abroad study.

The cost is captured from the offer letter, the I-20 (USA), the CAS for a UK education loan, the COE for an Australia education loan, or the LOA + tuition invoice. The bank funds up to 100 percent of these documented heads. It does not fund discretionary spend (luxury travel, premium accommodation above the institute’s standard, personal electronics beyond a reasonable laptop). For abroad study the bank usually treats the I-20 / CAS cost-of-attendance figure as the upper bound.

So a USD 80,000 tuition + USD 25,000 living = USD 105,000 (roughly ₹87 to 90 lakh at current rates) Master’s in the US on an education loan would in theory support a ₹87 lakh loan ask. Whether you get the full ₹87 lakh still depends on the FOIR, collateral, and institute tier filters above. The course cost is the cap, not the sanction. See our secured vs unsecured education loan post for how the secured route changes the conversation.

Faz's ruleCourse cost is the ceiling, not a target. Borrowing the full I-20 number because the bank will fund it is the most expensive habit I see in education-loan files.

I have watched students borrow the full cost-of-attendance figure on the I-20, then sit on ₹6 to 8 lakh of unspent living-expense headroom that accrued interest for two years. Borrow what you actually need, not what the document says you can. Every lakh trimmed at sanction saves roughly ₹90,000 over a 12 year tenure.

The PM Vidyalakshmi portal and the central scheme route

The PM Vidyalakshmi portal is the government’s single-window application platform for education loans, where students can apply to multiple banks simultaneously. The portal itself does not increase the maximum education loan amount in India, but the underlying PM Vidyalakshmi scheme (notified November 2024) adds two things worth knowing for the cap conversation.

One, a 3 percent interest subsidy during moratorium for students with family income up to ₹8 lakh per year, for loans up to ₹10 lakh studying in 902 quality higher education institutions in India. Two, a credit guarantee of 75 percent on collateral-free loans up to ₹7.5 lakh for the same institute list. The guarantee helps PSU banks sanction the ₹10 lakh unsecured cap with less friction, but does not raise it.

For abroad study and amounts above ₹10 lakh, the PM Vidyalakshmi scheme does not change the cap structure. The IBA model scheme caps and bank-specific policies remain the operating rules. State governments run their own interest-subsidy and credit-guarantee programmes on top of this, so it is worth checking the state education loan schemes in Maharashtra, Bengal, and UP if you are domiciled there.

The honest verdict on the maximum education loan amount in India

The honest answer to “what is the maximum education loan amount in India” is: between ₹4 lakh (the IBA model scheme floor below which no collateral is needed) and ₹3 crore (the highest NBFC sanction on record for a premier-institute abroad Master’s with substantial collateral). That is a 75x range. Where your specific case lands inside it depends on three things, in order of weight.

The co-applicant’s net monthly income and CIBIL. The institute on the offer letter. The collateral available. The course you are doing and the country you are going to matter, but they matter mostly through how those three filters apply to your file. A high-cost Tier-1 destination pushes the sanction toward the top of that range, which is exactly why our guide to the education loan for Singapore walks through how much these premier-hub courses actually fund.

Run the math before you pick a lender. A PSU bank ₹30 lakh sanction at 9 percent over 12 years costs roughly ₹22 lakh in interest. An NBFC ₹50 lakh sanction at 12.5 percent over 12 years costs roughly ₹49 lakh in interest. The ₹20 lakh extra capital costs you ₹27 lakh extra interest over the loan life. Sometimes worth it, often not. The maximum education loan amount in India is a useful upper bound, never a recommendation.

FAQ

What is the maximum education loan amount in India?

Under the IBA model scheme followed by most PSU banks, the unsecured cap is ₹10 lakh for domestic study and ₹20 lakh for studies abroad. With tangible collateral, PSU caps stretch to ₹40 lakh domestic and ₹1.5 crore abroad. Private banks and NBFCs can go higher: up to ₹1 crore or more unsecured for premier institutes, and ₹2 to 3 crore with collateral. The actual sanction depends on co-applicant income, CIBIL, the institute on the offer letter, and collateral valuation.

Can I get a ₹1 crore education loan?

Yes, but only under specific conditions. NBFCs like Avanse, Credila, and Auxilo regularly sanction ₹1 crore plus for abroad Master’s at premier institutes (MIT, Stanford, Oxford, Wharton and similar). The co-applicant typically needs net monthly income of ₹1.5 lakh or higher, a CIBIL of 750 plus, and either substantial collateral or a premier-institute admission. PSU banks rarely cross ₹1 crore even with collateral. The interest rate on a ₹1 crore NBFC loan is usually 11 to 13 percent, against 8.5 to 10.5 percent on a smaller PSU loan.

What is the unsecured education loan cap in India?

The IBA model scheme sets unsecured caps of ₹10 lakh for domestic study and ₹20 lakh for abroad. PSU banks adhere to these for standard institutes. For premier institutes the unsecured cap can stretch to ₹50 lakh or higher at SBI (Global Ed-Vantage) and other PSUs. NBFCs offer ₹50 lakh to ₹1 crore unsecured for premier institutes. Above the unsecured cap, tangible collateral (property, FD, LIC policy) is mandatory and the loan-to-value ratio is typically 70 to 80 percent of the bank’s valuation.

Does premier institute admission mean a higher loan?

Yes, materially so. Banks and NBFCs maintain published lists of premier institutes where the placement record statistically lowers the default risk. For premier institutes the unsecured cap commonly stretches 3 to 5x: from ₹20 lakh to ₹50 to 100 lakh on a like-for-like co-applicant profile. The lists vary by lender. IIT, IIM, NIT, AIIMS, ISB, and select global universities (Ivy League, Oxbridge, top Russell Group) feature on most premier lists. A mid-tier or unranked institute on the offer letter caps the sanction well below the scheme ceiling.

What is the IBA scheme ceiling for education loans?

The Indian Banks’ Association (IBA) model education loan scheme, adopted by most PSU banks, caps unsecured loans at ₹10 lakh for domestic study and ₹20 lakh for studies abroad. With tangible collateral, the cap goes up to ₹40 lakh domestic and ₹1.5 crore abroad. The scheme covers tuition, hostel, examination fees, books, equipment, two-way travel, and reasonable living expenses for abroad study. The IBA scheme is periodically revised. The current text is on iba.org.in.

How much can I borrow for an MBA abroad?

For an MBA at a top global business school (Wharton, Harvard, INSEAD, LBS), the total cost is typically USD 150,000 to 230,000 (₹1.25 to 1.95 crore). NBFCs like Credila and Avanse regularly sanction ₹1 crore plus unsecured for these programs given the strong placement record. PSU banks sanction up to ₹1.5 crore with collateral. The actual sanction still depends on co-applicant income and CIBIL. For a mid-tier MBA abroad (regional US programs, mid-tier UK schools), sanctions typically land in the ₹35 to 60 lakh range.

Does the loan amount depend on the course?

Indirectly, yes. The maximum education loan amount in India is capped at the documented total cost of the course (tuition + hostel + permitted heads). A two-year MBA at IIM A funds up to roughly ₹30 lakh, the course cost. A four-year engineering degree at a state college funds up to roughly ₹8 lakh, again the course cost. A long-haul medical degree pushes the ceiling far higher, which is why borrowers compare an education loan for MBBS in the Philippines, Bangladesh, or Nepal against the cost of a domestic seat. A vocational course like commercial flying behaves the same way, where the documented training cost sets the cap, as the education loan for pilot training post lays out. The cap is the course cost. Above that the bank does not fund regardless of co-applicant strength. Within that cap the FOIR, CIBIL, institute tier and collateral decide the actual sanction.

Can I take more than one education loan?

Yes, with conditions. A second loan for a second course (e.g. one loan for a bachelor’s, a separate loan for a master’s later) is routinely sanctioned, subject to repayment record on the first loan and the co-applicant’s current FOIR. Two simultaneous loans for the same course are not normally allowed, but a top-up loan on an existing education loan for a fee revision or course extension is possible at the same lender. NBFCs sometimes refinance existing PSU education loans, called a balance transfer, but this is not the same as a fresh second loan.

Faz · The Honest Journey · 2026