An education loan for the UK from an Indian PSU bank typically sanctions up to ₹1.5 crore for a one-year Master’s, but the unsecured ceiling without collateral stays around ₹7.5 lakh at PSU banks and ₹50 to 75 lakh at NBFCs for ranked universities. A taught UK Master’s runs GBP 20K to 35K in tuition plus living, which at 1 GBP equals 106 INR works out to roughly ₹21 lakh to ₹50 lakh all in. Because the program is one year, the total ticket is smaller than a two-year US or Canada Master’s, so the loan stays tighter, but almost any UK sanction above ₹7.5 lakh needs either collateral or an NBFC co-applicant route.

A cousin of mine finished a one-year MSc in Management at a Russell Group university last autumn. He picked the UK over a two-year Canada program for one blunt reason: the math. One year of tuition and rent instead of two meant a loan that was almost half the size, and a degree in hand twelve months sooner. What surprised him was not the tuition. It was how the CAS, the 28-day bank statement and the IHS payment all collided in the same three weeks, and how his sanctioned amount lined up against the year’s real cost.

This post is the loan-side picture I wish he had read in May, before he accepted the offer and before he paid the deposit. It is the loan-product view, distinct from the broader cost of studying in the UK post, which covers the spending side in detail, and from the full guide to studying in the UK for Indian students, which walks through admissions and the visa from scratch.

Why a UK Master’s is the Indian loan sweet spot

The single biggest reason an education loan for the UK works cleanly is the program length. A taught Master’s in the UK is twelve months. A US Master’s is usually two years, a Canada Master’s one to two. That one detail halves the rent bill, halves the living-expense tranche, and shrinks the total loan you carry into repayment.

Concretely: a two-year US Master’s might total USD 80K to 100K, which is ₹67 lakh to ₹84 lakh, almost always above the PSU unsecured ceiling and usually needing collateral. A one-year UK Master’s at GBP 30K total is ₹31.8 lakh. Still above ₹7.5 lakh, still collateral territory at a PSU bank, but a much smaller absolute number, a shorter repayment tail, and a faster route to earning. For a family weighing how much debt to take on, the UK’s one-year structure is the quiet advantage that does not show up in tuition-only comparisons.

PSU banks read the UK as Tier-1: their flagship overseas products cover it without question, the Russell Group and most other recognised universities sit on every approved list, and the documentation is well-trodden. That predictability is worth something when you are racing a visa deadline.

What an education loan for the UK actually covers

PSU banks treat the UK under their flagship overseas products. The two most relevant are SBI Global Ed-Vantage and Bank of Baroda’s Baroda Vidya overseas education loan, with Canara Bank’s IBA Premier and Union Bank’s special education loan as the usual alternatives.

The covered heads on a Tier-1 UK sanction usually include:

- Full tuition for the entire program, paid directly to the university.

- Living expenses up to a stated annual cap, often a fixed amount or a percentage of tuition.

- The Immigration Health Surcharge (IHS), which is mandatory and paid up front for the whole visa duration.

- The student visa application fee.

- One return economy airfare per year.

- Laptop and study material against bills, capped.

- Examination, library and lab fees where the university charges them separately.

The IHS is a UK-specific item worth flagging. It is not optional and it is not small. For a student visa it is charged per year of leave granted, and a one-year Master’s visa (with the extra few months the UK adds on either side) usually means paying for two years of surcharge. At the 2025 rate of GBP 776 per year for students, that is roughly GBP 1,552, which is ₹1.65 lakh, due in full before the visa is granted. Good banks fold this into the sanction; thinner ones leave the family to front it.

The CAS and university offer as the sanction basis

For most destinations the bank sanctions against the admission letter. For the UK the document that anchors everything is the CAS, the Confirmation of Acceptance for Studies. The university issues the CAS only after you have accepted the offer and usually after you have paid a tuition deposit. It carries a unique CAS number, the course details, the tuition figure, and any deposit already paid. You cannot apply for the student visa without it.

Banks have learned to read the CAS as the binding cost basis. The tuition line on the CAS is what the bank disburses against, and the deposit-paid figure tells the bank how much tuition is already settled. The official rules for what the CAS must contain and how the visa uses it are on the UK government’s student visa pages, and the student-facing explainer at UKCISA is the cleanest neutral source for what the visa actually requires.

The practical timing knot is this. The university wants a deposit before it issues the CAS. The bank often wants the CAS before final disbursement of the tuition tranche. So families usually pay the deposit themselves (or via an early partial disbursement), the university issues the CAS, and the bank then releases the balance of tuition directly to the university. Sequence the deposit early so the CAS is not held up.

Faz's ruleGet your CAS sorted before you obsess over the visa date. The CAS is the gate. No CAS, no visa application, no final disbursement. Everything downstream waits on it.

The order that actually works: accept the offer, pay the tuition deposit (from savings or an early loan tranche), receive the CAS, then apply for the visa with the CAS number, then have the bank release the tuition balance to the university. Students who try to do these in parallel end up with a sanctioned loan and no CAS to apply against.

The 28-day rule, IHS and disbursement timing

Two UK requirements interact with your loan disbursement in ways that catch families off guard.

First, the 28-day rule on funds. The UK student visa requires you to show the maintenance funds (money for living costs, on top of tuition) held in an eligible account for 28 consecutive days, ending no more than 31 days before you apply. The maintenance amount is set by the Home Office: for study in London it is GBP 1,483 per month for up to nine months (so up to GBP 13,347), and outside London GBP 1,136 per month for up to nine months (up to GBP 10,224). Any tuition deposit already paid is deducted from the tuition you still need to evidence, but the maintenance money is separate.

This is where loan timing bites. An education loan disbursed straight to the university does not sit in your account for 28 days, so it does not by itself satisfy the maintenance evidence. Families handle this one of two ways: either the maintenance amount is parked in the student’s own account for the full 28 days (often arranged by the bank as a maintenance tranche released early to the student), or the bank issues a sanction letter on letterhead confirming the loan covers both tuition and living expenses. The UK accepts an approved loan letter from a recognised financial institution as evidence of maintenance funds, which sidesteps the 28-day account-balance requirement entirely. Confirm with your bank that they will issue this letter in the Home Office format.

Second, the IHS is paid as part of the visa application itself, before the decision, in one lump sum. So the sequence of money leaving is: tuition deposit, then IHS plus visa fee at application, then the tuition balance to the university, then the living-expense tranche to you. The IHS and visa fee land before any living-expense tranche arrives, so the family needs that GBP 2,000-ish ready up front regardless of how the loan is structured. The general flow is covered in the education loan disbursement process post.

PSU sanction limits and where the math breaks

The PSU education loan products that cover the UK follow the IBA framework on collateral and ceiling:

| Loan tier | Terms | Collateral required |

|---|---|---|

| Up to ₹4 lakh | Nil margin, no collateral, no third-party guarantee | None |

| Above ₹4 lakh to ₹7.5 lakh | Parent co-applicant, third-party guarantee | Often no tangible collateral |

| Above ₹7.5 lakh to ₹1.5 crore (Global Ed-Vantage tier) | Tangible collateral mandatory (property, FD, LIC) | Yes, near 100 percent of loan after haircut |

The wall most UK-bound students hit sits right at ₹7.5 lakh. A GBP 30K total UK Master’s is ₹31.8 lakh, well above the unsecured PSU ceiling. So you either bring tangible collateral (typically property valued enough to clear the loan after the bank’s haircut) or you split the funding between a PSU loan up to ₹7.5 lakh and family contribution, or you go the NBFC unsecured route.

NBFCs (Avanse, HDFC Credila, Auxilo, InCred) sanction unsecured loans up to ₹50 to 75 lakh for ranked UK universities against parent co-applicant income, but at interest rates 200 to 400 basis points higher than PSU floating rates, and without the CSIS subsidy. NBFCs also tier their rates by university ranking: a Russell Group offer gets a finer rate than a lesser-known institution. The honest economics of PSU versus NBFC are in the education loan for abroad studies without collateral post, and the overall ceilings in the maximum education loan amount in India post.

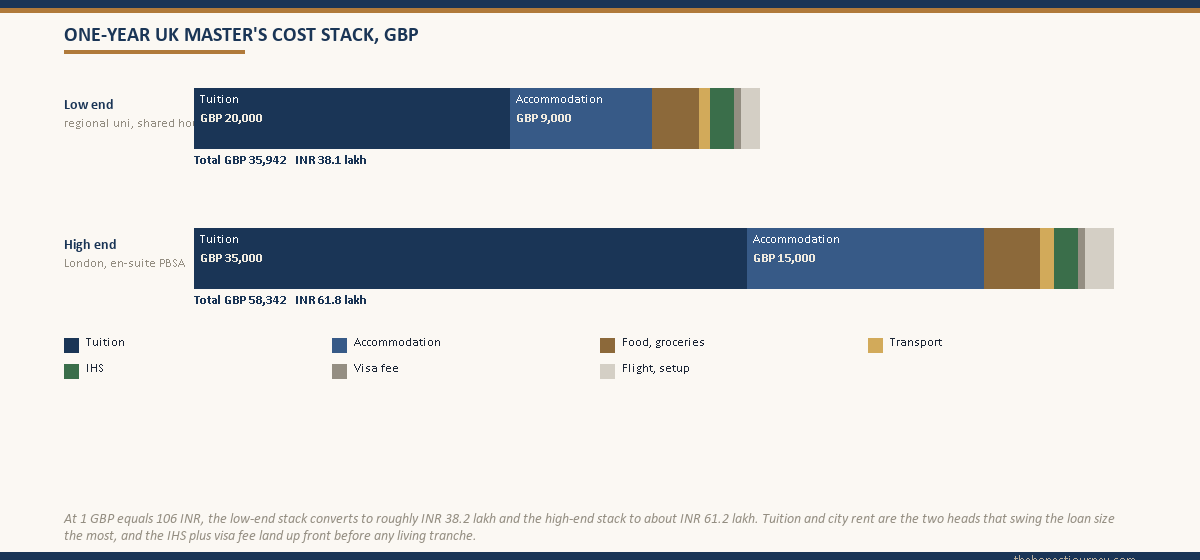

Worked example: a GBP 30K UK Master’s against a PSU sanction

Take a real-shaped case. Student admitted to a one-year MSc at a Russell Group university outside London for September 2025. Tuition GBP 24,000. Estimated total one-year cost GBP 30,000.

| Item | GBP | INR (at 106) |

|---|---|---|

| Tuition (MSc, one year) | 24,000 | 25,44,000 |

| Accommodation (outside London, 12 months) | 9,600 | 10,17,600 |

| Food and groceries | 3,000 | 3,18,000 |

| Transport and local travel | 700 | 74,200 |

| IHS (two years at GBP 776) | 1,552 | 1,64,512 |

| Visa application fee | 490 | 51,940 |

| Flight and setup | 1,200 | 1,27,200 |

| Total cost | 40,542 | 42,97,452 |

Note the gap between the GBP 30K headline (tuition plus rough living) and the GBP 40.5K all-in figure once IHS, visa fee, food, transport and setup are added. The headline number families quote is almost always the tuition-plus-rent figure. The real sanction needs to cover the full ₹43 lakh.

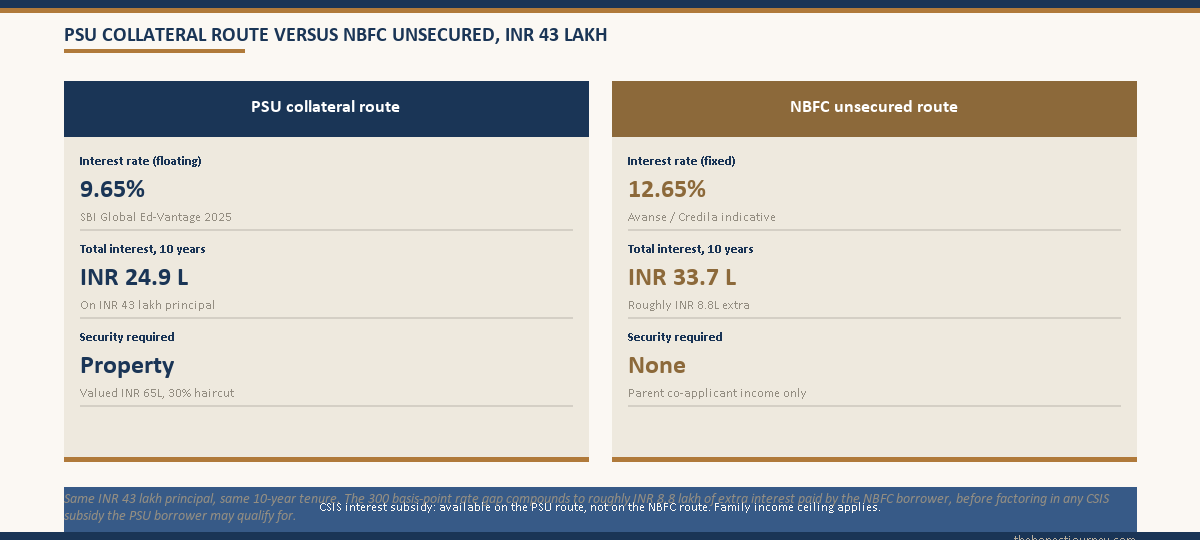

This student goes to SBI for a Global Ed-Vantage loan. SBI sanctions the full ₹43 lakh, but because the amount is far above ₹7.5 lakh, collateral is mandatory. The family pledges a residential property valued at ₹65 lakh. SBI applies its haircut (commonly around 25 to 30 percent on residential property), so the security value the bank counts is roughly ₹45.5 to 48.75 lakh, comfortably above the loan.

Tuition is wired GBP 24,000 to the university in line with its fee schedule, after the deposit already paid is netted off. The maintenance evidence for the visa is handled by SBI issuing a loan-sanction letter confirming the loan covers living expenses, accepted by the Home Office in place of the 28-day account balance. The IHS and visa fee are paid by the family up front and reimbursed from the loan’s covered heads after disbursement.

If the family had no property to pledge, the same case at an NBFC would mean an unsecured sanction of around ₹43 lakh against the parent’s income, typically needing CTC of ₹15 to 18 lakh and a clean CIBIL above 750, at an interest rate of 11.5 to 13.5 percent versus SBI’s floating rate near 9.65 percent. Over a 10-year repayment, that roughly 300 basis point gap on ₹43 lakh is in the region of ₹8 to 9 lakh of extra interest. That is the real price of skipping collateral, and it is worth modelling before you sign.

The narrowed Graduate Route and your repayment runway

Here is the part that has changed, and the part your loan plan has to absorb honestly. The UK Graduate Route is the post-study work visa that lets you stay and work after the degree. It still exists. But it has been narrowed. From 2024 the route was reviewed and tightened, dependents were barred for most taught Master’s students, and the standing position is that the post-study stay for Master’s graduates is now two years on the Graduate Route (down from the wider expectations of a few years ago, and with PhD graduates getting three).

Two years sounds fine until you map it against a ₹43 lakh loan. Repayment usually begins after a moratorium covering the course plus six months to a year. So your earning runway in the UK to make a dent in the loan, before either switching to a Skilled Worker visa or returning home, is roughly those two Graduate Route years. The Skilled Worker route requires an employer sponsor and a salary above the threshold, which not every graduate lands inside two years.

What this means in plain terms: do not model your UK loan on the assumption of five comfortable years of UK salary paying it down. Model it on two years of Graduate Route earning, a realistic UK starting salary after tax and rent, and a clear fallback of either securing sponsorship or repaying from an Indian salary if you return. If the loan only makes sense assuming you stay and earn in pounds indefinitely, the narrowed route has quietly broken that assumption. Run the numbers for the case where you come back after two years.

Faz's ruleTreat the two Graduate Route years as your real ROI window, not a relaxed buffer. The loan does not care which country pays it back, but pounds repay faster than rupees, and you only have two pound-earning years guaranteed.

A UK graduate salary outside London after tax and rent leaves a real surplus, but two years of it will not clear a ₹43 lakh loan. It will dent it. Plan for the partial-repayment-then-Skilled-Worker-or-return reality, and make sure the loan is survivable on an Indian salary if the sponsorship does not come through.

What banks check on UK-specific paperwork at sanction

For a UK Master’s, the documents that go into the sanction file beyond the standard ones include:

- The unconditional offer letter from the university, on letterhead, with the course, duration and tuition clearly stated.

- The CAS, or confirmation that the CAS will be issued on deposit payment, showing the CAS number, tuition figure and any deposit paid.

- The fee structure or invoice showing tuition for the program year and the deposit already settled.

- Evidence the institution is a licensed student sponsor on the Home Office register (banks check the university appears on the official sponsor list).

- The IHS and visa fee estimate, so the covered-heads total reflects the real up-front cost.

- For collateralised loans, the property documents and the valuation signed off by the bank’s empanelled valuer.

The point banks scrutinise most is the alignment between the CAS tuition figure, the deposit paid, and the amount they are being asked to disburse. If the deposit was paid from family funds, the bank disburses the balance to the university. If the bank funds the deposit too, it wants the CAS to follow promptly. Keep the deposit receipt, the CAS and the fee invoice consistent to the rupee, because any mismatch between them stalls the file. The Reserve Bank’s framework that governs how these overseas remittances move sits on the RBI site, and the disbursement mechanics are in the disbursement process post.

The honest take on the UK as a loan-funded destination

The UK works well as a one-year, focused, English-taught Master’s destination for an Indian student with PSU loan funding, provided two things hold. One, the family can either pledge collateral for amounts above ₹7.5 lakh or accept the higher NBFC rate with eyes open. Two, the student treats the narrowed two-year Graduate Route as the real ROI window and builds a repayment plan that survives a return to India after it.

The one-year structure is the genuine advantage. A smaller total loan, a shorter repayment tail, a degree in twelve months, and the right to work alongside study within visa limits all make the UK math tighter than a two-year North American Master’s. The CAS-anchored process is predictable, PSU banks know it cold, and the maintenance-funds requirement is cleanly solved by a loan-sanction letter.

What does not work is funding a UK Master’s on the old assumption of an open-ended post-study runway. That assumption is gone. The route is two years for Master’s graduates, dependents are largely barred, and the Skilled Worker bridge is not guaranteed. If your loan only pencils out because you assumed many years of UK earnings, redo the math against the two-year reality and an Indian-salary fallback before you sign the sanction letter. Funded honestly, against the real numbers, a one-year UK Master’s is one of the cleaner loan-funded routes out there. Funded on the old story, it is a stretch.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for the UK is in the UK student visa guide.

FAQ

What is the maximum education loan for a UK Master’s from Indian banks?

SBI Global Ed-Vantage and BoB’s overseas product both sanction up to ₹1.5 crore for Tier-1 destinations including the UK, provided collateral and co-applicant income support the amount. The unsecured ceiling at PSU banks stays at ₹7.5 lakh; anything above needs tangible security such as property, FD or LIC. NBFCs like Avanse and HDFC Credila sanction unsecured loans up to ₹50 to 75 lakh for ranked UK universities against parent income, but at higher interest rates than PSU banks and without the CSIS subsidy.

Do Indian banks sanction loans on the CAS?

Yes, the CAS is the anchor document for a UK loan. The Confirmation of Acceptance for Studies carries the course details, tuition figure and any deposit paid, and banks disburse tuition against it. Practically, you accept the offer, pay the deposit, receive the CAS, then the bank releases the tuition balance to the university. You cannot apply for the student visa without a CAS, so banks treat it as the binding cost basis for the sanction file.

How much margin money is needed for a UK education loan?

For overseas studies, PSU banks usually apply a margin of around 10 to 15 percent on the loan, meaning the family funds that share and the bank funds the rest. Loans up to ₹4 lakh carry nil margin. On a large UK sanction the margin is often met by the tuition deposit and early living costs the family pays before disbursement. NBFCs sometimes offer lower or zero margin for premier programs but price it into a higher interest rate, so the margin saving is rarely a real saving.

Is collateral needed for a UK Master’s loan?

Above ₹7.5 lakh at a PSU bank, yes. Since almost any UK Master’s totals more than that, most students pledging through SBI or BoB need tangible collateral such as residential property, an FD or an LIC policy valued enough to clear the loan after the bank’s haircut. If you have no collateral, the alternative is an NBFC unsecured loan against parent income, which goes up to ₹50 to 75 lakh for ranked universities but costs 200 to 400 basis points more in interest.

How does the 28-day rule interact with my education loan?

The UK requires maintenance funds held in an account for 28 consecutive days before you apply, separate from tuition. A loan disbursed to the university does not sit in your account, so it does not satisfy this by itself. The fix is a loan-sanction letter from your bank in the Home Office format, which the UK accepts as evidence of maintenance funds and sidesteps the 28-day balance requirement. Confirm your bank will issue this letter before you apply.

What is the Graduate Route now, after the narrowing?

The Graduate Route is the post-study work visa that lets you stay and work after a UK degree. Following the 2024 review it was tightened: dependents are barred for most taught Master’s students, and the stay for Master’s graduates is now two years (PhD graduates get three). It requires no employer sponsor for those two years. After that you need a Skilled Worker visa with a sponsoring employer and a qualifying salary, which is not guaranteed, so plan your repayment around the two-year window.

What is the total cost of a one-year UK Master’s for an Indian student?

A one-year UK Master’s typically totals GBP 30,000 to GBP 45,000 all in, depending on university and city. Tuition runs GBP 20,000 to 35,000, accommodation GBP 9,000 to 15,000 (London higher), food GBP 3,000, transport GBP 700, IHS around GBP 1,552 for two years, visa fee GBP 490, plus flight and setup. At 1 GBP equals 106 INR, that is roughly ₹31.8 lakh to ₹47.7 lakh. London adds materially to rent; cities outside London run cheaper.

Can a UK education loan cover the IHS and visa fee?

Yes, good PSU products include the Immigration Health Surcharge and visa application fee among the covered heads, so they form part of the sanctioned amount. The catch is timing: both are paid up front at the visa application stage, before any living-expense tranche reaches you, so the family fronts roughly GBP 2,000 and is reimbursed from the loan after disbursement. Make sure your sanction letter lists IHS and visa fee explicitly, because thinner products quietly leave them out.

Faz · The Honest Journey · 2026