Studying in the UK as an Indian student means a one-year taught Master’s that lands all-in at roughly ₹35 to 55 lakh, made up of tuition near GBP 18,000 to 30,000, living costs, the Immigration Health Surcharge, and the student visa. You apply through the university (or UCAS for undergraduate), get a CAS, prove 28 days of held funds, then stay on the two-year Graduate Route to work after you finish. The single-year degree is what makes the UK ticket smaller than a two-year US one, and the Graduate Route is the work runway that decides whether the math repays.

A friend’s younger sister finished a one-year MSc in Data Science at a Russell Group university in 2024. She had the offer by January, the CAS by May, the visa by July, and was in halls by late September. The part that nearly tripped her was the 28-day funds rule. She moved money into her account two weeks before the visa application, which was too late, and had to delay the application by a fortnight until the balance had sat for the full 28 days. Nobody had told her the money has to be held, not just present.

This post is the honest end-to-end picture of going to the UK: admissions, the student visa, the real all-in cost, the work runway after you graduate, and how scholarships and loans fit. It is the overview, not the deep cost breakdown and not the loan-product detail, both of which already live on their own pages I link below.

Applying without IELTS? Over 80 UK universities waive it, but UKVI rejects Duolingo and the waiver must be on your CAS. See UK universities without IELTS.

Applying to the UK? September and January both work, but a one-year master’s finishes at very different points for graduate hiring. See UK intakes explained.

Why the UK appeals to Indian students, honestly

The UK pulls Indian students for three concrete reasons, and it is worth being honest about each rather than repeating the brochure.

First, the one-year taught Master’s. A UK MSc or MA is usually 12 months of intensive study, against two years for a comparable US Master’s. That single fact roughly halves your tuition and living bill versus the US, and it gets you back to earning a year sooner. For a loan-funded student that compounding of one saved year is the strongest financial argument the UK has.

Second, the Graduate Route. Since 2021 a student who completes an eligible degree can stay and work, or look for work, for two years (three for a PhD) with no employer sponsorship needed. That is the repayment runway, and I treat it as the single most important number for a loan-funded student after tuition itself.

Third, the names. Many UK universities sit high in global rankings, and a Russell Group degree carries weight with Indian employers if you return. None of this means the UK is automatically worth it. It means the UK is worth it when the program, the post-study work plan and the funding line up, which is the same honest test I apply to every destination.

Faz's ruleThe one-year Master's is the UK's real financial edge, not the prestige. A 12-month degree halves the tuition and living bill versus a two-year US program and gets you earning a year sooner.

Treat the saved year as money, because it is. One fewer year of tuition, one fewer year of living costs abroad, and one extra year of salary all land on the same side of the ledger. That is what makes a UK loan smaller and easier to repay than a US one, before you even look at the rate.

Admissions: UCAS for undergraduate, direct for postgraduate

How you apply depends on the level, and Indian students often confuse the two routes.

For an undergraduate degree, you apply through UCAS, the central application service. UCAS lets you apply to up to five courses with one application and one personal statement, on a published annual cycle with set deadlines. The official portal is ucas.com, and it is the only route for most UK undergraduate admissions.

For a postgraduate taught Master’s, which is what most Indian students go for, you apply directly to each university’s own portal, not through UCAS. There is no single Master’s deadline; each program runs rolling admissions and closes when full, so applying early genuinely matters for popular courses and for scholarship consideration.

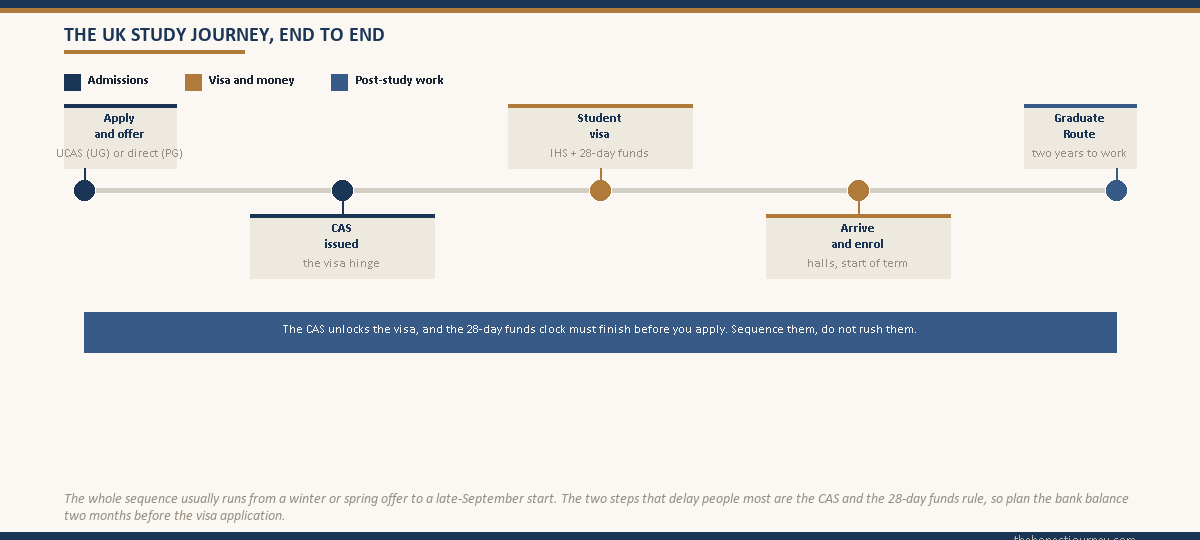

Either way, once a university decides to admit you and you accept and meet the conditions, the university issues a CAS, the Confirmation of Acceptance for Studies. The CAS is a reference number, not a paper certificate, and it is the document you need to apply for the student visa. No CAS, no visa application, so the CAS is the hinge between admission and immigration.

| Level | How you apply | Deadline pattern |

|---|---|---|

| Undergraduate | UCAS (up to five courses, one application) | Fixed annual cycle with set deadlines |

| Postgraduate taught | Direct to each university portal | Rolling, closes when full, apply early |

| After acceptance | University issues a CAS | Needed before the visa application |

The Student visa, the IHS, and the 28-day funds rule

The UK study visa for over-18s is the Student visa, applied for online before you travel. The official rules and the application sit on gov.uk, and the independent guidance for international students is on ukcisa.org.uk. Three things on this visa cost real money and trip up Indian applicants, so I will take each plainly.

The Immigration Health Surcharge (IHS) is a charge that gives you access to the National Health Service for the length of your visa. It is paid upfront, per year of the visa, when you apply. For a one-year Master’s with the usual few extra months of visa validity, the IHS runs to a few thousand pounds, and it is a real line in your budget, not an afterthought. You pay it in full at application, so it has to be in your funds.

The visa application fee itself is separate from the IHS and also paid at application. Together the visa fee and the IHS are the two upfront UK government charges, and both are out of pocket, not loan-funded as a tranche, in most cases.

The financial requirement is the one that delayed my friend’s sister. You must show you have enough money to cover your course fees for the first year plus a set monthly living amount, and crucially that money must have been held in your account for at least 28 consecutive days ending no more than 31 days before you apply. Moving money in at the last minute does not count. The funds have to sit for the full 28 days, which means planning the bank balance two months before you intend to apply.

Faz's rulePark your visa funds 28 days before you apply, not the week of. The money must sit held in the account for 28 consecutive days, so plan the balance two months ahead of the application.

This is the most common avoidable delay I see for UK applicants. The bank balance has to be held, not just present on the day. If you are funding the visa from a loan disbursement or a family transfer, time it so the money lands at least 28 days before you click submit, or you lose weeks waiting for the clock to run.

The real all-in cost in INR, summarised

The full breakdown lives on the dedicated cost of studying in the UK for Indian students post, so here I will give the summary picture a loan applicant needs to size the borrowing. For a one-year taught Master’s at a mainstream UK university, the all-in number for most Indian students lands somewhere between ₹35 lakh and ₹55 lakh, depending heavily on the university, the city, and the exchange rate.

| Cost layer | Typical range (GBP) | INR (at 106) |

|---|---|---|

| Tuition (one-year Master’s) | 18,000 to 30,000 | ~19,08,000 to 31,80,000 |

| Living costs (12 months) | 12,000 to 15,000 | ~12,72,000 to 15,90,000 |

| IHS (health surcharge) | ~1,200 to 1,500 | ~1,27,000 to 1,59,000 |

| Visa fee | ~500 | ~53,000 |

| Indicative all-in | ~32,000 to 47,000 | ~33,90,000 to 49,80,000 |

The honest caveat on this table: London is materially more expensive on living costs than the rest of the country, and the rupee-pound rate has drifted enough in recent years that a one-rupee move on the exchange rate shifts a GBP 40,000 ticket by several thousand rupees. Treat these as indicative bands, confirm the exact tuition on your offer letter, and use the live rate, not last year’s. The funding side of this, the loan that covers it, is the subject of the education loan for UK post.

One structural point matters for funding. Because a UK Master’s is a single year, the bank or NBFC sanctions against a one-year cost of attendance, not two. That makes the UK loan structurally smaller than the equivalent US loan, which in turn means more UK students fit under collateral thresholds or qualify for unsecured loans more comfortably. It is the same point I keep coming back to: the one-year degree is the financial edge.

The Graduate Route: two years to work after you finish

The Graduate Route is the post-study work visa, and for a loan-funded student it is the repayment runway, so it deserves a clear-eyed look. After you complete an eligible UK degree, you can apply to stay for two years to work or look for work, with no job offer and no employer sponsorship required. PhD graduates get three years.

What makes the Graduate Route honest as a repayment plan, more than the US OPT, is that it needs no lottery and no employer to sponsor you upfront. You finish, you apply, you get the two years. That certainty is worth a lot when you are modelling whether a loan repays.

The catch is on the other side. Two years of UK salary is a shorter runway than the US STEM OPT’s three years, and UK starting salaries for many fields are lower than US ones in dollar terms. So the UK math works on a smaller loan repaid over a tighter, lower-paid window, while the US math works on a larger loan against a longer, higher-paid one. Neither is automatically better. The UK suits the student who wants a smaller bet and a near-certain two-year work window; the comparison with the US route is laid out in the is studying abroad worth it post. The day-to-day reality of working part-time during the course, which helps with living costs, is covered in the part-time work while studying abroad post.

Faz's ruleThe Graduate Route is two near-certain years, the US STEM OPT is three lottery-shadowed ones. Model your loan on the runway you actually get, not the one you hope for.

The UK’s two-year Graduate Route needs no lottery and no sponsor to start, which makes it a more dependable repayment window than the US OPT-to-H-1B path, even though it is a year shorter. If your loan repays comfortably across two years of a realistic UK starting salary, the UK is a sound bet. If it only works assuming you land a top-tier role, shrink the loan.

Scholarships and funding for the UK

Scholarships will rarely fund a UK Master’s end to end, but the right one can knock a meaningful chunk off the loan, so they are worth chasing early. The two that Indian students should know by name are government schemes.

Chevening is the UK government’s flagship scholarship, fully funded, covering tuition, a living stipend, and travel for a one-year Master’s. It is highly competitive and aimed at students with leadership potential and work experience, with a fixed annual application window. The Commonwealth Scholarships are a parallel UK-government funded route for students from Commonwealth countries, including India, for Master’s and PhD study. Both are merit and need driven, both close early, and both expect a strong application built over weeks, not days.

Beyond these, most UK universities offer their own partial scholarships and India-specific bursaries, often applied for as part of, or just after, the admission application. The broad landscape of what is available and how to stack it sits in the scholarships for Indian students to study abroad post.

For the part of the cost that scholarships do not cover, which is most of it for most students, the funding is an education loan. The visa requires you to prove the held funds regardless of source, and a loan sanction letter is accepted proof of funds, which is why the loan and the visa timelines have to be sequenced together. The standard of proof and the documents are in the proof of funds for student visa post.

The honest take on studying in the UK

The UK works as a loan-funded destination when the one-year Master’s is from a program that gives you real employability, and when you treat the two-year Graduate Route as your repayment window with eyes open. The smaller, single-year ticket and the no-lottery work runway are genuine advantages over the US for Indian students for a cost-conscious, risk-aware student. If Canada is also on your shortlist, our UK vs Canada comparison weighs the one-year ticket against the longer Canadian work pathway.

What does not work is treating the UK as a cheaper US, applying to a weak program just because the degree is one year, then expecting a UK salary to clear a loan sized for a stronger outcome. The two-year runway is shorter and the salaries lower than the US, so the program quality has to carry more weight, not less.

Run the math against the one-year cost of attendance on your offer letter, at the live exchange rate, and against a realistic two-year UK starting salary. If it repays on those honest numbers, the UK is one of the most efficient education bets an Indian student can make. If it only repays on hopeful ones, change the program or shrink the loan before you sign.

Sorting the visa is the step most people underestimate. The full process, fees and funds proof for the UK sit in the UK student visa guide.

Before you commit, weigh the payback: read is studying in the UK worth it for the honest ROI and years-to-repay math.

FAQ

How much does it cost to study in the UK for Indian students?

For a one-year taught Master’s at a mainstream UK university, the all-in cost for most Indian students lands between ₹35 lakh and ₹55 lakh. That covers tuition of roughly GBP 18,000 to 30,000, twelve months of living costs, the Immigration Health Surcharge, and the visa fee. London is materially more expensive than the rest of the country, and the rupee-pound rate moves the total significantly, so confirm tuition on your offer letter and use the live exchange rate rather than an old one.

How do Indian students apply to UK universities?

For an undergraduate degree you apply through UCAS, the central service, which lets you apply to up to five courses with one application. For a postgraduate taught Master’s you apply directly to each university’s own portal, with rolling admissions that close when full, so applying early matters. Once a university admits you and you accept and meet the conditions, it issues a CAS, the Confirmation of Acceptance for Studies, which is the reference number you need to apply for the student visa.

What is the CAS and why do I need it?

The CAS, or Confirmation of Acceptance for Studies, is a reference number a UK university issues once it has decided to admit you and you have accepted and met the offer conditions. It is not a paper certificate, just a number tied to your record. You cannot apply for the UK student visa without a CAS, so it is the hinge between admission and immigration. Get the CAS, then apply for the visa, which is why the admission and visa timelines have to be sequenced.

What is the 28-day funds rule for the UK student visa?

To get a UK student visa you must show enough money for your first year of fees plus a set monthly living amount, and that money must have been held in your account for at least 28 consecutive days ending no more than 31 days before you apply. Moving money in at the last minute does not count, because the funds have to sit held for the full 28 days. Plan your bank balance roughly two months before you intend to apply so the clock has run.

What is the Immigration Health Surcharge?

The Immigration Health Surcharge, or IHS, is a charge paid upfront when you apply for the UK student visa, giving you access to the National Health Service for the length of your visa. It is charged per year of the visa, so for a one-year Master’s with the usual extra months of validity it runs to a few thousand pounds. You pay it in full at application alongside the visa fee, both out of pocket, so budget for both as real upfront costs.

What is the UK Graduate Route?

The Graduate Route is the UK post-study work visa. After you complete an eligible UK degree, you can stay for two years to work or look for work, three years for a PhD, with no job offer and no employer sponsorship needed to apply. It needs no lottery, unlike the US H-1B path, which makes it a dependable repayment runway for a loan-funded student. The runway is a year shorter than US STEM OPT, and UK salaries are often lower, so size the loan accordingly.

Are there scholarships for Indian students in the UK?

Yes. The two government schemes to know are Chevening, the UK government’s fully funded flagship covering tuition, a living stipend and travel for a one-year Master’s, and the Commonwealth Scholarships for students from Commonwealth countries including India. Both are highly competitive, merit and need driven, and close early. Most UK universities also offer partial scholarships and India-specific bursaries applied for around the admission stage. Scholarships rarely fund a degree end to end but can meaningfully reduce the loan.

Is a UK Master’s worth it compared to the US?

It depends on your risk appetite and the program. A UK Master’s is one year against two for the US, which roughly halves tuition and living costs and gets you earning sooner, and the two-year Graduate Route needs no lottery. The trade-off is a shorter work runway and generally lower salaries than the US STEM OPT route. The UK suits a smaller, lower-risk bet; the US suits a larger one with a longer, higher-paid window. Run both against realistic salaries before deciding.

Faz · The Honest Journey · 2026