Proof of funds for a student visa is documentary evidence that you can cover one full year of tuition and living costs without working illegally. The amount is country specific: the US asks for your full I-20 cost of attendance, the UK wants tuition plus roughly GBP 1,023 a month held for 28 days, and Canada requires first year tuition plus a CAD 20,635 GIC. The money must be seasoned, not freshly parked.

The first student I met who had been refused a visa lost it not on grades or intentions, but on a fixed deposit her uncle wired in eleven days before she filed. To her it proved she could afford the course. To the officer it looked like borrowed money, parked for show, that would vanish the day the stamp landed. That one deposit cost her a four-month delay and a refusal on her record.

Proof of funds is the part of a study-abroad file families get wrong most often, because they think it is about having the money. It is not. It is about proving the money is real, yours, and stable. This post lays out how much each country wants, what counts, and what quietly gets your file rejected.

Proof of funds for a student visa is documentary evidence that you can cover your tuition and living costs for at least the first year. Each country sets its own amount: the US wants your full I-20 cost of attendance, the UK wants tuition plus a fixed monthly maintenance figure held for 28 days, Canada wants first-year tuition plus a GIC, and Australia and New Zealand publish their own annual living thresholds. The money must be available and seasoned, not freshly parked.

For the full guide, read Studying Abroad From India: Cost and Funding Guide.

What proof of funds actually proves

A visa officer is not asking whether your family is wealthy. They are asking one narrow question: will this student run out of money halfway through and either drop out or work illegally? Everything in the funds section of your file exists to answer that question with a yes, the money is there, and it is stable.

That is why the amount alone never settles it. A balance that appeared last week tells the officer nothing about stability. A balance that has sat for six months, or a loan formally sanctioned by a recognised bank, tells them a great deal. The document is not the point. The story it tells is.

Get this framing right and the rest is detail. You are assembling a file that says: here is the money, here is where it came from, and here is the proof it will still be there when I land. Miss any one of those three and the strongest balance can still draw a refusal. That credibility gap is one of the most common financial refusal grounds, which is why I covered it in the student visa rejection reasons post.

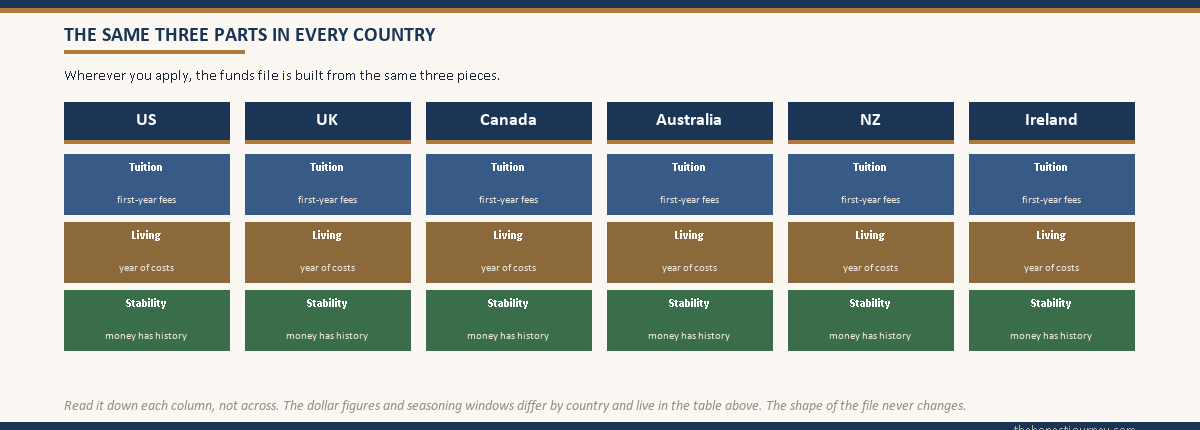

How much each country wants, country by country

Here is the grid families ask me for first. These are the first-year figures each immigration authority works to. Living-cost numbers move with policy and inflation, so treat them as the working baseline and always confirm against the official source before you file: the Canadian IRCC proof of financial support page and the Australian Home Affairs site publish their current numbers.

| Country | What you must show | Approximate first-year amount | Seasoning rule |

|---|---|---|---|

| United States (F-1) | Full cost of attendance on your I-20 (tuition plus living, minus any scholarship) | USD 30,000 to 75,000+ depending on the school | No fixed window, but recent large deposits draw scrutiny at interview |

| United Kingdom (Student route) | One year tuition plus monthly maintenance (£1,023/month outside London, £1,334/month in London) for up to 9 months | Tuition plus roughly £9,207 to £12,006 living | Funds held for 28 consecutive days, ending within 31 days of applying |

| Canada (study permit) | First-year tuition plus a Guaranteed Investment Certificate (GIC) for living costs | GIC of CAD 20,635 plus first-year tuition | GIC funds locked with the bank; balance history expected |

| Australia (subclass 500) | One year tuition plus published living costs, plus travel | Living cost benchmark around AUD 29,710 plus tuition | Genuine access to funds; sudden deposits questioned under the genuine student test |

| New Zealand | Tuition plus living funds for the stay | NZD 20,000 per year of living costs plus tuition | Funds shown as genuinely available, not borrowed for display |

| Ireland | Tuition plus proof of living funds for the year | Around €10,000 living per year plus tuition | Recent transfers explained; stable balance preferred |

Notice the pattern. Every country wants tuition plus a living figure, and every country has some version of a stability test. The UK simply writes its test into a hard rule, the 28-day requirement, while the others apply it through officer judgement. That difference matters more than it looks, so the UK gets its own section below.

Faz's ruleThe amount is the easy half. The stability of that amount is the half that gets people refused.

Families spend weeks arranging the balance and almost no time thinking about how the balance looks on paper. A visa officer reads the second half first. Money that appeared last week reads as money that will disappear next week.

The UK 28-day rule, explained properly

The UK is the country that turns the stability principle into a precise, unforgiving rule, and it is the single most common reason Indian students get refused on funds for a UK Student visa. So it is worth slowing down on.

The rule is this: the required money must sit in your account, or your parent’s account, for 28 consecutive days. On every one of those 28 days, the balance must not drop below the required amount, not even once, not even for a day. The 28-day period must end no more than 31 days before the date you submit your application. And the closing balance on your statement, the most recent figure, must show the full required amount.

Where people fall: they assemble the money on day 20, so the balance only crosses the threshold partway through. Or the account dipped below the line on day 14 because a regular EMI went out. Either resets the clock, and you cannot file until a fresh, clean 28-day window has passed with the balance held above the line throughout.

If you are using an education loan for the UK, the rule is different and easier: a loan sanction letter from a recognised lender does not need the 28-day seasoning at all, because the funds are committed by the bank rather than parked in your account. That is one of several reasons a loan letter is often the cleaner route, which I cover in the loan sanction letter as proof of funds post. Always read the current numbers and method on the official UK Student visa money page before you lock your filing date.

Faz's ruleFor the UK, the date you assemble the money matters as much as the amount. Build the balance, then wait 28 clean days, then file.

I have seen perfectly funded students refused because they filed on day 22 of the window instead of day 29. The money was real. The timing was wrong. Plan the 28 days into your calendar before you book the visa appointment.

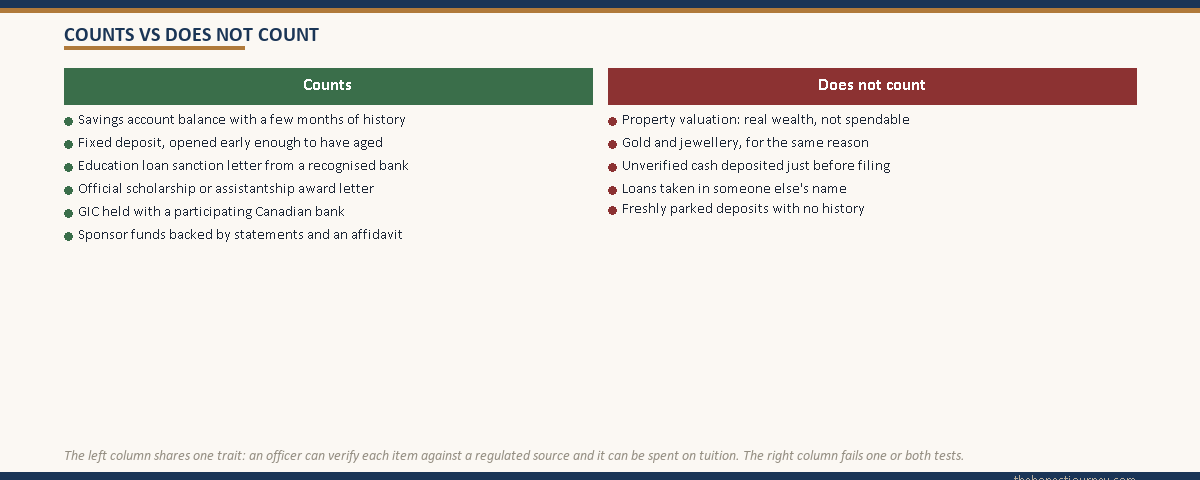

What counts as proof of funds

This is the list that actually works across the major destinations. None of these is exotic. The reason they count is that each one is verifiable by the officer and tied to a regulated institution.

- Savings account balance. The simplest proof, and the one most exposed to the seasoning test. A statement showing a stable balance over several months is far stronger than a single recent screenshot.

- Fixed deposits (FDs). Widely accepted. An FD certificate plus the bank statement showing when it was created. An FD opened months ago is excellent. An FD created the week before you file invites the same suspicion as a fresh deposit.

- Education loan sanction letter. One of the strongest documents you can submit, because a bank has formally committed the money. Most countries accept it; the UK explicitly recognises loans from recognised financial institutions. It must state the sanctioned amount, the disbursement coverage, and your name as borrower.

- Scholarship or assistantship letter. An official award letter reduces the amount you must otherwise show by exactly that figure. A USD 20,000 scholarship on your I-20 lowers the cost of attendance you need to cover.

- GIC (Canada). A Guaranteed Investment Certificate is purpose-built proof for the Canadian study permit. You deposit the living-cost amount with a participating bank, and it is released to you in instalments after you arrive.

- Sponsor’s funds with an affidavit. A parent or close relative can sponsor you, but the money must be backed by their bank statements, income proof, and a notarised affidavit of support, which I break down in the sponsorship affidavit post.

Across all of these, the common thread is verifiability. The officer can pick up the phone, or check the document against a regulated source, and confirm it is real. That is what separates proof from a number on a page.

What does not count, and why

This is where most avoidable refusals happen, because the rejected items feel like wealth. They are wealth. They are just not liquid, verifiable proof of funds in the way a visa officer needs.

- Property. A house worth ₹2 crore is not proof of funds. You cannot pay a tuition invoice with a flat. A property valuation tells the officer you have assets, not that you have spendable money for the course. It can support a loan application; it does not stand alone as visa proof.

- Gold and jewellery. Same logic. Real value, not liquid, not accepted as standalone proof.

- Unverified cash. Cash deposited into an account just before filing is the single biggest red flag. The officer cannot trace where it came from, so they treat it as borrowed money parked for the application.

- Loans not in your name. A personal loan your uncle took to lend you the money does not work as your proof of funds. It is his liability, not your committed education funding.

- Freshly parked deposits. Money that appeared days before you filed, even if it is genuinely yours, fails the stability test in every country and outright breaks the UK 28-day rule.

The fix for almost all of these is the same: plan the funds early. If the money needs to move between accounts or come in from a sale, do it months ahead, keep the paper trail, and let the balance settle so the officer sees stability instead of a last-minute scramble.

Faz's ruleProperty and gold are wealth. They are not proof of funds. Do not build your file on assets you cannot spend on tuition.

I meet families every year who assume a property worth crores settles the funds question. It does not. The officer needs money that can pay an invoice this year, not an asset that takes months to sell. Convert early or use a loan, but never lead with the house.

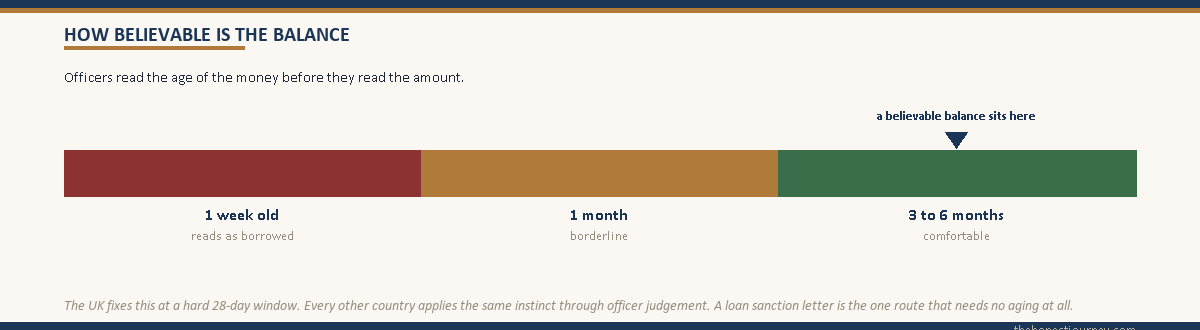

How seasoning works everywhere except the loan route

Seasoning is the idea that money should have a history. The UK fixes it at 28 days. Canada, Australia, New Zealand, Ireland, and the US do not publish a single magic number, but every officer in those systems is trained to ask the same question: has this money been here long enough to be believable?

In practice, that means a balance with three to six months of history is comfortable, a balance one month old is borderline, and a balance one week old is a problem. Bank statements covering the recent months, not a single-day snapshot, are what demonstrate seasoning. The remittance you eventually send abroad is also governed by the RBI’s Liberalised Remittance Scheme, which caps outward remittance at USD 250,000 per financial year, worth knowing as you plan the actual transfer (the RBI publishes the current rules on the RBI site).

Faz's ruleA small loan can buy you a clean funds file. Some families with the cash take one purely to skip the seasoning test.

It sounds backwards, but a sanction letter needs no history while parked cash does. If your money only came together recently and your filing date is close, a loan letter can be the calmer route than racing the seasoning clock.

The one clean exception is the education loan. A sanctioned loan needs no seasoning because the funds are committed by a regulated bank and disbursed against your fee schedule rather than parked in your account. That is why a loan letter so often makes the file simpler than a self-funded balance. If you go that route, the bank’s own paperwork is listed in the documents required for education loan post, and for Canada the GIC and loan interact in a way I covered in the GIC Canada education loan post.

The honest closing take

If you remember one thing from this post, make it this: proof of funds is a credibility exercise, not an accounting one. The officer is not impressed by a large number. They are reassured by a believable one. A modest balance with six months of clean history beats a huge balance that landed last Tuesday, every single time.

So plan backwards from your filing date. Decide your funding mix early, whether that is savings, an FD, a loan sanction letter, a scholarship, or a sponsor. Get the money into the right account in the right name with enough runway that it has a history by the time you apply. For the UK, count the 28 days deliberately. For everyone else, give the balance a few months to settle. And never, ever fund the application on assets you cannot spend or cash you cannot trace.

Do that and the funds section, the part that refuses more honest students than any other, becomes the easiest part of your file instead of the one that derails it. With the money settled, turn to the other moving parts of the application: a tight statement of purpose for your student visa and education loan, and the medical test required for your student visa so nothing stalls in the final weeks.

Funds proof is where most student visa refusals actually start, and the exact amount and format shift with the country. The country-by-country breakdown sits in our student visa guides for Canada, the USA, the UK, Australia, Germany, New Zealand, Ireland, France, the Netherlands and Singapore.

Bringing a spouse or children raises the amount you must show, sometimes substantially, and the rules differ by country. The dependants comparison sets out the extra funds required for each.

FAQ

How much money do I need to show for a student visa?

It depends entirely on the country and your school. The US wants your full I-20 cost of attendance, often USD 30,000 to 75,000 or more. The UK wants one year of tuition plus monthly maintenance of £1,023 outside London or £1,334 inside London. Canada wants first-year tuition plus a GIC of around CAD 20,635. Australia works to a living benchmark near AUD 29,710 plus tuition. Always cover at least the first full year, and confirm the current figure on the official immigration page before you file.

What counts as proof of funds for a student visa?

Verifiable, liquid evidence tied to a regulated institution. That includes savings account balances, fixed deposits, an education loan sanction letter from a recognised bank, an official scholarship or assistantship letter, a Canadian GIC, and a sponsor’s funds backed by their bank statements and a notarised affidavit. The common thread is that an officer can check each one against a real source. Anything the officer cannot independently verify, or cannot be spent directly on tuition, generally does not count on its own.

Does an education loan count as proof of funds?

Yes, and it is one of the strongest documents you can submit. Because a bank has formally committed the money, a sanction letter often makes the funds file cleaner than a self-funded balance, and crucially it does not require the seasoning that a fresh deposit does. The letter must state your name as borrower, the sanctioned amount, and that it covers your tuition and living costs. The UK explicitly recognises loans from recognised financial institutions, and most other countries accept them too.

What is the 28-day rule for UK student visa funds?

The required money must sit in your account, or your parent’s account, for 28 consecutive days without ever dropping below the threshold on any of those days. The 28-day window must end within 31 days of the date you submit your application, and the closing balance on your statement must show the full amount. If the balance dips below the line even once during the window, the clock resets and you must wait for a fresh clean period before filing. Loan sanction letters are exempt from this rule.

How much bank balance do I need for a Canada student visa?

For a Canadian study permit you must show first-year tuition plus living costs, and the standard way to prove living costs is a Guaranteed Investment Certificate (GIC) of around CAD 20,635. You deposit that amount with a participating bank, and it is released back to you in instalments after you arrive in Canada. On top of the GIC you show that first-year tuition is paid or arranged. Check the current required figure on the official IRCC proof-of-financial-support page before you apply, as the amount is reviewed periodically.

Can I show a fixed deposit as proof of funds?

Yes. A fixed deposit is widely accepted, provided you submit the FD certificate alongside the bank statement showing when it was opened. An FD created several months ago is excellent proof because it demonstrates both the amount and the stability an officer wants to see. The catch is timing: an FD opened the week before you file looks exactly like a freshly parked deposit and invites the same suspicion. If you are going to use an FD, create it early so it has a believable history by your filing date.

Why does property not count as proof of funds?

Because you cannot pay a tuition invoice with a house. Proof of funds must be liquid, money that can be spent on the course this year. A property valuation shows the officer you hold assets, not that you have spendable funds available for the program. Property can support an education loan application, where it serves as collateral, but it does not stand alone as visa proof. The same logic applies to gold and jewellery: real value, but not the liquid, verifiable money a visa officer is required to confirm.

Why do freshly deposited funds get rejected?

Because an officer cannot tell whether the money is genuinely yours or borrowed and parked just to pass the application, with plans to return it the moment the visa is granted. A large deposit that appears days before you file fails the stability test in every country and outright breaks the UK 28-day rule. The money may be completely legitimate, but if it has no history the officer treats it as a risk. The fix is simple: move funds into place months ahead and keep the paper trail clean.

Faz · The Honest Journey · 2026