Yes, an Indian education loan can fund the German blocked account, and most public sector banks now do this routinely. The sanction letter has to mention overseas remittance for blocked account creation, the bank disburses EUR 11,904 (the 2026 figure) directly to Expatrio, Fintiba or Coracle in EUR via SWIFT, and the whole transfer usually clears in 5 to 10 working days. The forex rate the bank uses on transfer day decides how many rupees actually leave your loan account.

The first time I tried to explain the blocked account mechanics to a cousin filing for a Berlin master’s, I realised most of what his study consultant had told him was either outdated or wrong. He thought the loan amount would land in his Indian account and he would forward it to Germany himself. That is not how this works, and getting it wrong delays the visa file by weeks.

This post walks through what actually happens between your Indian bank, the blocked account provider, and the German consulate, in the order it happens.

For the rest of the Germany picture: the cost of studying in Germany breakdown.

What the blocked account is, and why the loan has to go directly to the provider

The Sperrkonto, or blocked account, is a German government requirement that proves you have enough money to cover your first year of living costs. The current minimum (set by the Federal Foreign Office for 2026) is EUR 11,904, which works out to EUR 992 per month you are allowed to withdraw after arrival. Most students top this up to leave a buffer.

The German consulate will not accept a regular Indian bank statement, a fixed deposit receipt or a sanction letter alone as proof of funds. They want to see that the money has been parked with a recognised blocked account provider (the three commonly accepted by Indian students are Expatrio, Fintiba and Coracle) and that a confirmation document has been issued in your name. Until that confirmation is in your visa file, the visa officer will not move your application forward.

This is why the education loan for germany blocked account flow cannot route through your savings account. The bank has to wire the EUR amount directly to the provider’s collection account in Germany, with your reference number on the SWIFT message so the provider can credit it to your Sperrkonto. If the funds land in your INR account first and you try to forward them yourself, you trigger LRS reporting, GST on forex conversion, and an additional layer of TCS that does not apply to a direct disbursement under the education loan TCS exemption.

What the sanction letter must say to be accepted

For a Germany blocked account remittance, the sanction letter wording matters more than people realise. The visa officer does not read it, but the bank’s forex desk does, and a sanction letter that does not explicitly mention overseas remittance will sit in queue while forex raises a query back to your branch.

The four things the sanction letter needs to state:

- The full sanctioned amount in INR.

- The purpose, mentioning “studies in Germany” and the specific university and program.

- An explicit clause permitting overseas remittance for “blocked account creation” or “living expenses in Germany”.

- The disbursement schedule, with the first tranche flagged for blocked account funding.

Public sector banks like SBI and Bank of Baroda have standardised this. The SBI Global Ed-Vantage product handles overseas remittance natively. Some private banks and NBFCs still use older templates that only mention “tuition fees and living expenses payable to the institution”, which the forex desk will flag because a blocked account provider is not the institution. If your sanction letter reads that way, request an amendment in writing before you fund the visa file.

Faz's ruleThe sanction letter has to name the blocked account provider as a permitted beneficiary, or the bank's forex desk will stall the SWIFT for clarification.

Get the amendment in writing before the visa appointment. A two line addendum from your branch manager saves a week of back and forth between the forex team and your relationship manager, which is exactly the week you do not have if your visa slot is locked in.

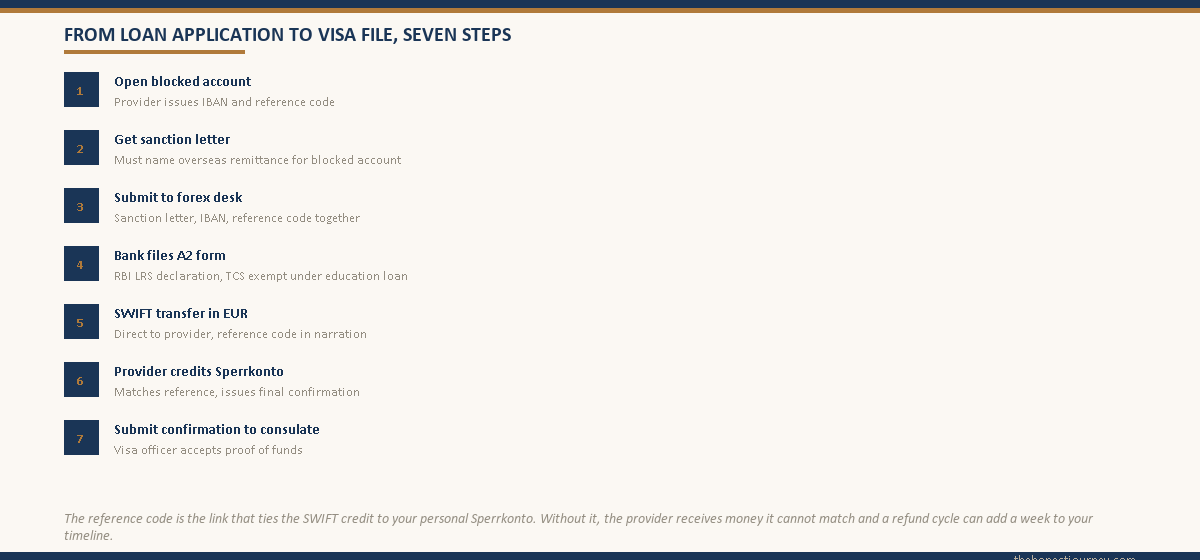

How the disbursement actually moves from your loan account to the blocked account

This is the part nobody walks you through clearly. Here is the actual sequence, in the order it happens.

First, you open the blocked account online with one of the three providers. The application takes 30 to 45 minutes, you upload passport and admission letter, and pay a one time setup fee of around EUR 49 to 99 from your own funds. The provider issues you a personal IBAN and a reference code.

Second, you take the IBAN, reference code and provisional confirmation to your bank’s forex desk along with the sanction letter. The forex team prepares an A2 form, which is the RBI mandated declaration under the Liberalised Remittance Scheme. For education-loan-routed remittance, the A2 is filed under “studies abroad” and is exempt from the 5 percent TCS that applies to other LRS transactions.

Third, the bank converts INR to EUR at the day’s card rate and initiates a SWIFT transfer to the provider’s German collection bank with your reference code in the narration. Without that reference code, the provider receives money it cannot trace, which sometimes triggers a refund and a second round of paperwork.

Fourth, the provider matches the reference code, credits your personal Sperrkonto, and issues the final confirmation document for your visa file.

The whole sequence typically takes 5 to 10 working days. SBI and Bank of Baroda tend to be on the faster end. Smaller branches and unfamiliar private branches have stretched it to 14 working days.

EUR vs INR: the forex angle that costs you ten to forty thousand rupees

The loan amount in your sanction letter is in INR. The blocked account requirement is in EUR. The number of rupees that actually leaves your loan account on disbursement day depends entirely on what rate the bank applies on conversion.

Indian banks use a “card rate” which sits roughly 50 to 150 paise above the inter-bank rate on any given day. On EUR 11,904, a 100 paise spread means an extra ₹11,904 added to your remittance cost. The spread varies by bank and is bigger on currencies with thinner flow at the branch.

| Cost component | Typical range | What it is |

|---|---|---|

| EUR amount disbursed | EUR 11,904 | 2026 blocked account minimum, set by Federal Foreign Office |

| Bank card rate spread over inter-bank | ₹0.50 to ₹1.50 per EUR | Bank’s forex margin, varies by day and by bank |

| SWIFT transfer charge | ₹500 to ₹1,500 | Fixed correspondent bank charge |

| GST on forex conversion | Roughly ₹1,200 to ₹2,000 | 18 percent GST on the forex service fee slab |

| TCS on education loan LRS | Zero | Exempt because remittance is routed through a sanctioned education loan |

The TCS exemption is the part students consistently underestimate. Funding the blocked account from personal savings via LRS attracts 5 percent TCS above the threshold. On EUR 11,904 (roughly ₹10.9 lakh), that is about ₹50,000 locked up as TCS, reclaimable only later through your tax return. Routing through a sanctioned education loan removes this entirely.

Faz's ruleAsk your bank in writing what EUR/INR rate they will apply on disbursement day, or at least what their card rate margin over inter-bank typically is.

The rate the bank uses is not negotiable but it is knowable. If the answer is “we will use the rate on the day,” push for the typical spread. A 50 paise difference on EUR 11,904 is real money and it comes out of your loan principal.

Which Indian banks actually fund the blocked account

Not every Indian bank with an education loan product handles overseas remittance to a blocked account provider smoothly. If you are still deciding which lender to approach, the full guide to an education loan for Germany compares the main options. The pattern from student reports is consistent:

Public sector banks that handle it well: SBI (Global Ed-Vantage), Bank of Baroda (BOB Vidya), Canara Bank, Bank of India. Rates sit around 9 to 10.5 percent and they generally need collateral above ₹7.5 lakh.

Private banks: HDFC Credila and Axis Bank have proper overseas remittance flows. Rates are higher (11 to 13 percent) but processing is often faster.

NBFCs: Avanse, Auxilo and HDFC Credila handle blocked account disbursement through provider tie-ups. Rates are highest (12 to 14 percent typical).

The PM Vidyalakshmi portal is an application channel only. The actual sanction and disbursement happens at the chosen bank’s branch level, so the choice of bank matters more than the application route. For the full funding picture see the study in Germany for Indian students guide.

Timing the disbursement against your visa appointment

German consulate visa slots in major Indian cities are booked months in advance. If disbursement slips by four working days, the confirmation might not be in the file on the appointment date, and rescheduling pushes you back another month.

The working backward calculation:

- Visa appointment: Day 0

- Final blocked account confirmation in hand: Day minus 2

- Provider issues confirmation: Day minus 3 to minus 4

- Bank initiates SWIFT: Day minus 5 to minus 8

- Submit sanction letter and provider details to forex desk: Day minus 10 to minus 14

- Sanction letter in hand: Day minus 14 to minus 21

So once you have the visa appointment date, work backwards three weeks for disbursement and add a one week buffer. Four weeks of lead time is comfortable. Three weeks is tight but workable. Less than two weeks is when people start paying for couriered amendments and weekend forex desk visits.

The DAAD student visa documentation lists the standard proof-of-funds requirements including the blocked account confirmation. The sanction letter alone is not accepted by the consulate as proof of funds because the money has not moved yet. For broader proof of funds options like the parental guarantee, see the proof of funds for student visa post.

Common mistakes I see students make

Three patterns keep showing up.

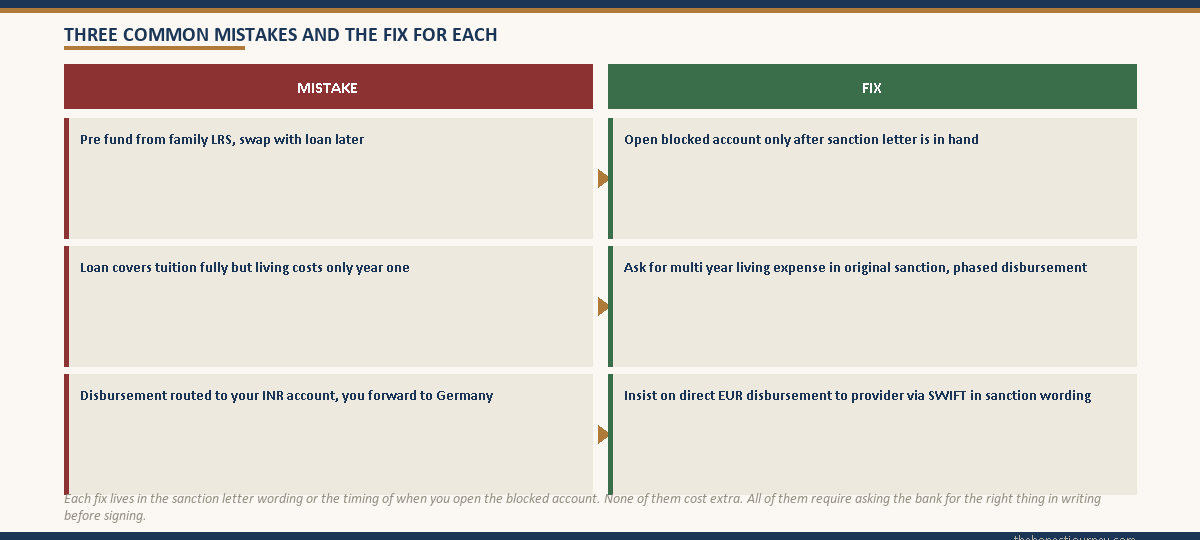

The first is funding the blocked account from a family member’s LRS quota before the loan disburses, then trying to “swap” it with loan funds later. This does not work cleanly. Once the visa is approved, the loan disbursement has nowhere to go and the bank will ask why you are requesting a disbursement when the stated purpose has already been met.

The second is taking a loan amount that covers tuition for the full program but only the first year blocked account requirement. The fix is to ask for the full multi-year living expense coverage in the original sanction with a phased disbursement schedule, so the second year remittance is part of the same sanction.

The third is signing a sanction letter without checking whether disbursement is in EUR direct or in INR with you doing the conversion. The wording you want is “disbursement to be made in EUR directly to the designated blocked account provider via SWIFT”. For more on the sanction letter as proof of funds in its own right, see the education loan sanction letter as proof of funds post.

Faz's ruleIf the bank wants to disburse to your INR account and let you forward to Germany, refuse and ask for direct EUR disbursement. This single line in the sanction letter saves the TCS, the LRS paperwork, and the rate uncertainty.

The bank’s default flow is often the one easiest for them, not cheapest for you. Direct EUR disbursement under the education loan is the protected route. Anything else is you taking on forex and tax exposure that the loan structure was supposed to remove.

What if you do not have collateral

Above ₹7.5 lakh, most public sector banks need collateral, which not every family has. The route then is either an NBFC unsecured loan (Avanse, Auxilo, HDFC Credila) or a private bank’s unsecured product for select universities with a high cut off. The rate trade off is 11 to 14 percent unsecured vs 9 to 10.5 percent secured, and tenure is often 10 years vs 15. For the full breakdown of unsecured options see the education loan for abroad studies without collateral post.

The blocked account disbursement mechanics are identical whether the loan is secured or unsecured. The forex flow, SWIFT process, A2 form and TCS exemption all work the same way. What changes is only the rate and the collateral requirement.

The honest closing take

The Germany blocked account funded by an Indian education loan is one of the cleaner cross-border financial flows available to students, but only if the sanction letter is worded correctly, the forex desk is briefed properly, and the timeline is worked backward from the visa appointment with a buffer built in.

What goes wrong is almost always one of three things. The sanction letter does not name overseas remittance as a permitted purpose, the forex desk is unfamiliar with the provider and stalls, or the disbursement is routed through INR and you lose tens of thousands to forex spread and TCS that would not have applied to a direct EUR disbursement.

The most useful thing you can do the week your sanction letter arrives is confirm two things in the disbursement clause: overseas remittance to a blocked account provider is explicitly named, and the disbursement currency is EUR direct. If either is missing, get a written amendment before booking the visa appointment.

FAQ

Can an Indian education loan fund the German blocked account?

Yes. Public sector banks like SBI (Global Ed-Vantage), Bank of Baroda, Canara and Bank of India routinely fund the German blocked account requirement through direct EUR disbursement to recognised providers like Expatrio, Fintiba and Coracle. Private banks and NBFCs also do this. The sanction letter must explicitly mention overseas remittance for blocked account creation, and the disbursement must be structured as a direct EUR transfer rather than an INR payout to your account.

How does the loan disburse to the blocked account provider?

You first open the blocked account online with Expatrio, Fintiba or Coracle and receive a personal IBAN and reference code. You hand these along with your sanction letter to your bank’s forex desk, which files an A2 form under the RBI LRS framework, converts INR to EUR at the card rate, and initiates a SWIFT transfer to the provider’s German collection bank with your reference code in the narration. The provider matches the code, credits your Sperrkonto, and issues the final confirmation for your visa file.

Does the loan get sent in EUR or INR?

For the protected, exempt route you want it disbursed in EUR directly to the blocked account provider via SWIFT. This avoids the 5 percent TCS that would apply on LRS remittance from your personal account, removes forex rate uncertainty, and keeps the transaction inside the education loan framework. If the bank’s default is INR disbursement to your account followed by you forwarding the funds, request an amendment to the sanction letter for direct EUR disbursement before signing.

Which Indian banks fund the German blocked account?

SBI through Global Ed-Vantage is the most established. Bank of Baroda, Canara Bank and Bank of India also handle it routinely. Among private banks, HDFC Credila and Axis Bank have proper overseas remittance workflows. NBFCs like Avanse and Auxilo handle blocked account disbursement through provider tie-ups. Avoid smaller cooperative banks and unfamiliar private branches where the forex desk has not processed Germany transfers before, because the learning curve gets billed to your visa timeline.

How long does the disbursement take?

From the day you submit the sanction letter and provider details to the forex desk, the typical timeline is 5 to 10 working days for the funds to land at the provider and the final confirmation document to be issued. SBI and Bank of Baroda tend to be on the faster end. Some private banks and unfamiliar branches have stretched to 14 working days. Work backwards three weeks from your visa appointment date and add a one week buffer to be safe.

Does Vidyalakshmi cover the blocked account?

The PM Vidyalakshmi portal is an application channel, not a separate loan product. You can apply through Vidyalakshmi for an education loan that funds the German blocked account, and the chosen bank handles the actual sanction and disbursement at branch level. The selected bank’s overseas remittance capability matters more than the application route.

Is TCS applicable on the blocked account remittance through an education loan?

No. Remittances routed through a sanctioned education loan for studies abroad are exempt from the 5 percent TCS that applies to other LRS transactions above the threshold. This is one of the under appreciated advantages of funding the blocked account through a loan even if your family has the savings to do it directly. Via personal LRS instead, roughly ₹50,000 would be locked up as TCS to be reclaimed later through your tax return.

What if my sanction letter does not mention overseas remittance for the blocked account?

Request a written amendment from your branch before booking the visa appointment. Older sanction templates sometimes only mention “tuition fees and living expenses payable to the institution”, which the forex desk will flag because a blocked account provider is not the institution. A two line addendum naming the provider and the purpose as blocked account creation is enough.

Faz · The Honest Journey · 2026