Yes, an education loan sanction letter works as proof of funds for a student visa in most countries, provided it is on the lender’s official letterhead, names you as the borrower, and states the full sanctioned amount in figures and words. The catch I see most often: the disbursement schedule on the letter has to match the cost of attendance the university quoted, or the visa officer reads the difference as a funding gap and refuses the file.

The bank gave you a sanction letter and your father exhaled like the hard part was over. Then the university asked for proof of funds, the visa checklist asked for proof of funds, and suddenly nobody was sure whether one piece of paper from an Indian bank actually counts. It usually does. But only if the letter says the right things, and only if the numbers on it line up with the number the embassy is looking for.

This is the post that sits between your loan file and your visa file. If you have a sanction letter in hand and you are about to submit it as proof of funds, read this first so you do not find out at the worst possible moment that it was missing a line.

An education loan sanction letter works as proof of funds for a student visa when it is on the lender’s letterhead, names you as the borrower, states the sanctioned amount, and confirms the money covers your tuition and living costs. Most countries accept it. The catch is that the disbursement schedule must match the cost of attendance the university quoted, or the visa officer treats it as a gap.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The other paperwork that sits in the loan file: the bonafide certificate education loan post, the education loan interest certificate post, and the gap certificate for education loan post.

The sanction letter is only as clean as the file behind it. See the documents and eligibility checklist for what a bank actually needs.

What an education loan sanction letter must actually state

A sanction letter is the bank’s formal commitment that it has approved a specific loan amount for you. It is not the same as a disbursement, and it is not the same as a loan agreement. For proof-of-funds purposes, the visa officer is reading it as evidence that the money is committed and waiting. So the letter has to remove every reasonable doubt about that.

Here is what a sanction letter has to contain before you submit it anywhere as proof of funds:

| Element | Why the visa officer wants it |

|---|---|

| Your full name as the borrower | Confirms the funds are committed to you, not a relative |

| Sanctioned loan amount (in figures and words) | The number that gets compared against cost of attendance |

| Purpose: education abroad, named course and university | Ties the money to this specific application, not a general loan |

| Coverage: tuition and living expenses | Shows the loan is meant for the full cost, not tuition alone |

| Lender’s name, letterhead, stamp, and signatory | Confirms it came from a recognised financial institution |

| Date of sanction and validity period | Proves the commitment is current, not a stale approval |

A sanction letter that says only “we have approved a loan of ₹25 lakh” with no named course, no coverage breakdown, and no validity date is a weak document. It is technically a sanction letter, but it leaves the officer guessing, and guessing is exactly what you do not want a visa officer doing with your file. If your letter is thin, go back to the branch and ask for a detailed sanction letter that names the university and confirms it covers tuition plus living expenses. Banks issue these routinely. They just default to the short version unless you ask.

Faz's ruleA sanction letter for proof of funds must name your university and confirm it covers living costs, not just tuition.

The short one-line version every branch prints by default is not enough for a visa file. Ask for the detailed sanction letter that names the course, the institution, and confirms coverage of tuition and living expenses. It is the same loan, just a stronger piece of paper.

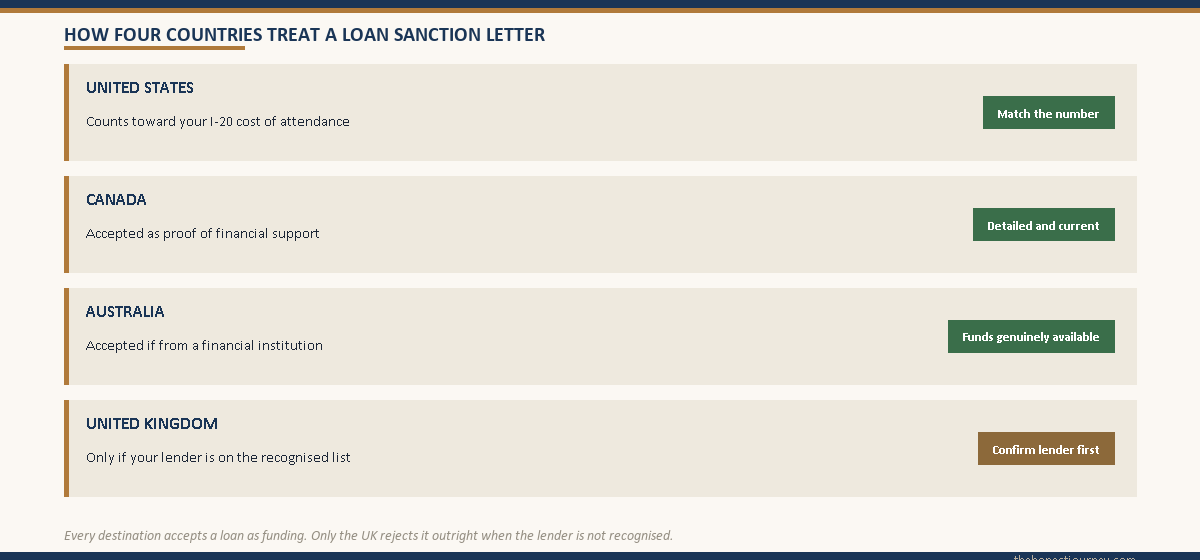

How each country treats a loan sanction letter

Every country accepts the idea of a loan as funding, but they wrap it in different rules. Some want the loan from a recognised list of lenders. Some fold it straight into the document the university issues. Knowing the specific rule for your country is the difference between a clean submission and a request for more documents.

United States (I-20 alignment). The US does not ask for a fixed bank balance. It asks the university to issue an I-20 form that states your total cost of attendance, and you must show funding that matches or exceeds that number. A loan sanction letter is one of the accepted funding sources, and many universities let you list it directly on the financial documentation form before they issue the I-20. The key is alignment: if the I-20 says your first-year cost is USD 55,000, your sanction letter (plus any other funds) needs to cover at least that. At the visa interview the consular officer is checking that your funding is credible and sufficient, not that it sits in a savings account.

United Kingdom (recognised-lender rule). The UK is the strictest here. A loan counts as proof of funds only if the lender is on the UK government’s list of recognised institutions, the loan is for tuition and living costs, and the funds will be available before you travel or are paid directly to the university. The official UK student visa money rules spell this out. An Indian public sector bank or a recognised NBFC generally qualifies, but you should confirm your specific lender before you rely on the loan letter. If your lender is not recognised, the UK will not count the loan, and you fall back to the maintenance balance held for 28 consecutive days.

Canada. Canada accepts a loan sanction letter as part of your proof of financial support for a study permit, alongside or instead of the GIC and first-year tuition payment. The sanction letter has to clearly show the loan is approved and available for your studies. Canada’s published list of acceptable proof of financial support includes a bank loan, so an education loan from an Indian bank fits, provided the letter is detailed and current.

Australia. Australia’s Genuine Student requirement asks you to demonstrate you can cover course fees, travel, and living costs. A loan is accepted, but Australia specifically requires that an education loan come from a financial institution and that the funds be genuinely available to you. A sanction letter that is conditional on documents you have not yet produced is weaker than an unconditional one. The official immigration guidance for each country is the source of truth, and it does shift, so check the current wording when you apply.

Faz's ruleFor the UK, confirm your lender is on the recognised list before you count the loan as funds.

The UK is the one country that will reject a perfectly valid Indian loan if the lender is not recognised. Most major banks and large NBFCs are fine, but a smaller regional lender may not be. Check first, because there is no fixing this at the visa stage.

The validity window: why a sanction letter goes stale

A sanction letter is not valid forever. Most Indian lenders issue a sanction letter with a validity window of 3 to 6 months. After that, the sanction lapses and the bank may require fresh income documents, an updated co-applicant statement, or a revised credit check before it reissues the commitment. For proof of funds, this matters because visa officers want a current commitment, not one that expired two months before you applied.

The timing trap looks like this. A student gets a sanction letter in December to support a January university application. The visa interview lands in May. By May the original sanction letter is past its validity window, and the officer sees a document that the bank itself no longer stands behind. The fix is simple but you have to plan for it: line up your sanction letter close to your visa submission, not at the earliest possible moment. If it is going stale, ask the bank for a fresh letter or a revalidation. Banks reissue routinely and it usually takes a few days.

| Stage | What you submit the sanction letter for | Timing note |

|---|---|---|

| University application | Financial documentation, to trigger the I-20 or CAS or offer | Earliest use, can be months before the visa |

| Visa application | Proof of funds in the visa file | Must be within the 3 to 6 month validity window |

| Disbursement | Bank releases funds to the university or your account | Usually after visa approval and admission confirmation |

Notice that the sanction letter does its proof-of-funds work before any money actually moves. That is by design. You do not need the loan disbursed to use the sanction letter as proof of funds. What you need is for the commitment to be live and the numbers to be right.

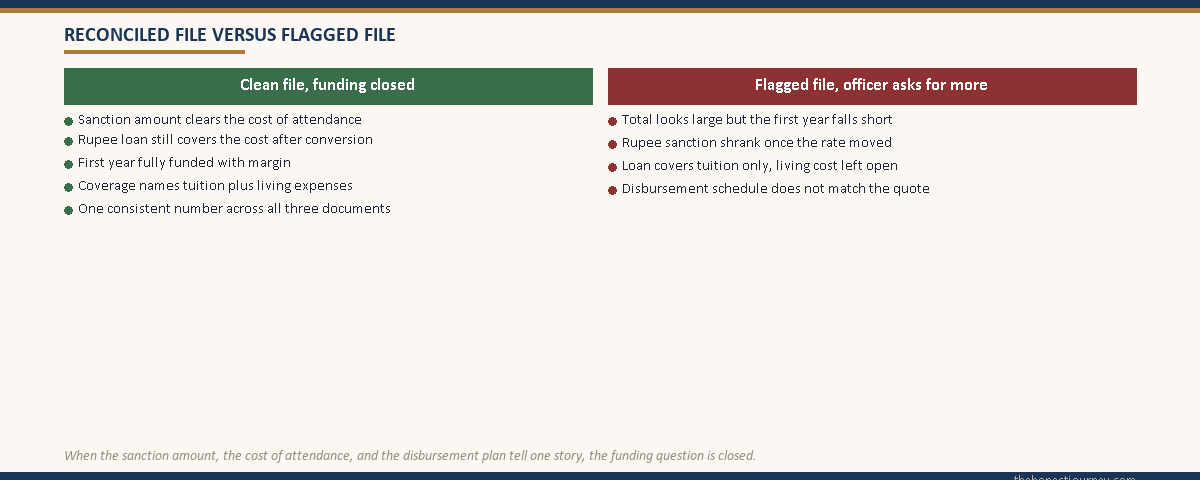

The gotcha: disbursement schedule must match cost of attendance

This is the line that catches the most files, and it is the reason this post exists. A sanction letter does not just need a big enough total. The way the money is scheduled to come out has to match how the cost of attendance is structured.

Cost of attendance is usually quoted per year. A US I-20 might state USD 55,000 for the first year. A two-year master’s degree means roughly USD 110,000 total. If your sanction letter is for the full USD 110,000 equivalent but the disbursement schedule releases it in tranches tied to each semester, that is normal and fine. The problem starts when the totals do not reconcile. If the university wants proof you can fund the first year and your sanction letter, after currency conversion, falls short of that first-year number, the officer treats it as a funding gap, even though your total loan looks large.

Three reconciliation checks before you submit:

- Currency. Your loan is sanctioned in rupees. The cost of attendance is in dollars, pounds, or Canadian dollars. Convert at a realistic rate and confirm the rupee sanction still clears the foreign-currency cost after conversion. A sanction that looked comfortable can shrink once the rupee moves.

- First-year coverage. Many countries care most about the first year being fully funded. Make sure the sanction amount, plus any savings or scholarship you are also showing, covers the first-year cost of attendance with margin, not exactly to the rupee.

- Tuition plus living. Cost of attendance includes living expenses, not just tuition. A sanction letter that covers tuition only, while the I-20 or offer letter includes a living-cost figure, leaves a visible gap. Your loan coverage and the university’s cost figure must describe the same total.

The cleanest files are the ones where the sanction letter, the university cost document, and the disbursement plan all tell the same financial story. When an officer can read three documents and see one consistent number, the funding question is closed. When the numbers disagree, even by a plausible margin, the officer has a reason to ask for more, and that is where avoidable delays and refusals come from. The financial mismatch is one of the most common student visa rejection reasons, and it is entirely preventable at the document stage.

Faz's ruleReconcile three numbers before you submit: sanction amount, cost of attendance, and disbursement schedule.

Convert your rupee sanction to the foreign currency at a realistic rate and confirm it still covers the first-year cost of attendance, tuition plus living. If those three documents tell one consistent story, the funding question is closed. If they disagree, the officer has a reason to ask for more.

How the sanction letter fits the rest of your funds file

A loan sanction letter is one of the strongest proof-of-funds documents you can submit, but it rarely travels alone. The full picture of what each country accepts is in the proof of funds for a student visa post, and the sanction letter slots into that picture as the committed-funding piece. Where it sits next to savings, FDs, or a scholarship depends on whether your loan covers the full cost or only part of it.

If the loan covers your full cost of attendance, the sanction letter can stand as your primary proof, with the rest of your file supporting it. If the loan covers only part, say tuition but not the full living-cost margin, you pair it with a bank balance or an FD that fills the gap, and the two together have to clear the cost of attendance. The documents that the bank needed to issue the sanction in the first place, covered in the documents required for an education loan post, are largely the same documents that strengthen your visa file, so the work is not duplicated.

One structural note for students on an unsecured loan. An education loan for abroad studies without collateral is sanctioned on the strength of your co-applicant’s income and your admission, not on a pledged asset. That does not weaken it as proof of funds. A recognised lender’s sanction letter is a recognised lender’s sanction letter, whether or not collateral backs it. What matters to the visa officer is the lender, the amount, the coverage, and the validity, not the security structure behind the loan.

From sanction to disbursement: what happens after the visa

The sanction letter does its proof-of-funds job before the visa is granted. The actual money moves later, through the disbursement process, and the timing is usually disbursement after admission confirmation and visa approval, not before. This trips up students who assume they need cash in a foreign account to apply. You do not. You need the commitment, evidenced by the sanction letter, to be live and sufficient.

When disbursement does happen, it is often staged. The bank releases tuition directly to the university each semester, usually against a fee demand letter from the institution, and may release living expenses to you or to a forex arrangement. This staged release is exactly why the disbursement schedule has to reconcile with the cost of attendance, the point from two sections ago. The mechanics of how and when the money actually leaves the bank are covered in the education loan disbursement process post, and it is worth understanding before you travel, because a mismatch between the disbursement timeline and a university fee deadline is its own headache. The Reserve Bank of India’s guidelines govern how these education loans and outward remittances are structured, and the major lenders publish their own education loan terms, such as SBI’s education loan pages, which are worth reading for the disbursement and repayment specifics.

The honest closing take

A loan sanction letter is one of the most accepted, most reliable proof-of-funds documents available to an Indian student. It is also one of the most commonly mishandled, not because students are careless, but because nobody tells them that the letter has to say specific things and the numbers have to reconcile across three documents. The bank issues the short version. The university quotes a cost. The visa officer reads both and looks for daylight between them.

Your job is to close that daylight before you submit. Get the detailed sanction letter that names your course and confirms living-cost coverage. Confirm your lender is recognised if you are headed to the UK. Check the validity window so the letter is not stale at the visa stage. And reconcile the sanction amount against the cost of attendance in the right currency, with the first year fully covered. Do those four things and the loan letter does its job quietly, which is exactly what you want a proof-of-funds document to do.

FAQ

Can I use an education loan sanction letter as proof of funds?

Yes. A loan sanction letter is one of the most widely accepted proof-of-funds documents for a student visa. It works because it is the lender’s formal commitment that an approved amount is reserved for your studies. To count, it must be on the lender’s letterhead, name you as the borrower, state the sanctioned amount, confirm the loan covers tuition and living costs, and be within its validity window. Most countries accept it, though the UK requires the lender to be on a recognised list.

What should the sanction letter mention for proof of funds?

It should mention your full name as the borrower, the sanctioned amount in figures and words, the purpose stated as education abroad with the named course and university, confirmation that it covers tuition and living expenses, the lender’s name and letterhead with stamp and signatory, and the date of sanction with a validity period. The short one-line approval that branches print by default is too thin for a visa file. Ask for the detailed version that names the institution and confirms living-cost coverage.

Is a loan sanction letter accepted for a US student visa?

Yes. The US does not require a fixed bank balance. It requires funding that matches or exceeds the cost of attendance stated on your I-20 form. A loan sanction letter is an accepted funding source, and many universities let you list it on the financial documentation before they issue the I-20. The key is alignment: your sanctioned amount, after currency conversion and combined with any other funds, must cover the I-20 cost figure. At the visa interview the officer checks that the funding is credible and sufficient.

How long is an education loan sanction letter valid?

Most Indian lenders issue a sanction letter with a validity window of 3 to 6 months. After that, the sanction can lapse and the bank may ask for fresh income documents or an updated credit check before reissuing it. For proof of funds, the letter must be current at the time you submit your visa application, not expired. If your interview is months after the sanction, ask the bank for a fresh letter or revalidation. Lenders reissue routinely and it usually takes only a few days.

Do all countries accept an education loan as proof of funds?

Most do, but the rules differ. The US folds it into I-20 cost-of-attendance alignment. Canada accepts it as part of proof of financial support alongside or instead of a GIC. Australia accepts it if the loan is from a financial institution and the funds are genuinely available. The UK is the strictest: it counts a loan only if the lender is on its recognised-institution list and the loan covers tuition and living costs. Always check the current official immigration guidance for your destination, as the wording can change.

Does the loan need to be disbursed before the visa?

No. The sanction letter does its proof-of-funds work before any money moves. You do not need the loan disbursed, or cash sitting in a foreign account, to use the sanction letter as proof of funds. What you need is for the commitment to be live, within its validity window, and large enough to cover the cost of attendance. Disbursement typically happens later, after admission confirmation and visa approval, often in staged tranches paid directly to the university each semester.

What is the disbursement-must-match-cost gotcha?

It is the requirement that your sanction amount and disbursement schedule reconcile with the cost of attendance the university quoted. Your loan is in rupees and the cost is in foreign currency, so you must convert at a realistic rate and confirm the sanction still clears the cost, especially the first year, after conversion. The loan must also cover tuition plus living, matching the university’s full cost figure. If the numbers disagree, the officer treats it as a funding gap even when the total loan looks large.

Can a sanction letter alone be enough proof of funds?

If the loan covers your full cost of attendance, the sanction letter can stand as your primary proof, with the rest of your file supporting it. If the loan covers only part, such as tuition but not the full living-cost margin, you pair it with a bank balance, an FD, or a scholarship that fills the gap, and the documents together must clear the cost of attendance. What matters to the visa officer is that the combined funding is credible, sufficient, and reconciles with the university’s quoted cost in the correct currency.

Faz · The Honest Journey · 2026