An education loan for Germany is structurally smaller than one for the US or Canada, because public universities charge near-zero tuition, only a semester contribution of around EUR 150 to 350. The loan mostly funds the blocked account, the Sperrkonto of EUR 11,904 for 2024 to 2025, plus living. At ₹90 per euro that blocked account is roughly ₹10.7 lakh, so a public-university student often needs a sanction of only ₹15 lakh to 20 lakh, which can fit inside a PSU bank’s unsecured line.

A girl from my old apartment block got into a fully taught-in-English Master’s at a public university in Bavaria. Her father walked into the bank ready to pledge property, the way he had heard every abroad loan works, and the officer told him the tuition was effectively zero and the real money was a blocked account he had never heard of. He had over-prepared on collateral and under-prepared on the one cash line that actually mattered, the Sperrkonto, which had to be funded and sitting in a German account before the visa interview.

This post is the loan-product picture for Germany, the funding angle. Germany is the destination where the loan logic flips: there is barely any tuition to fund at a public university, so the lender’s job is to fund the blocked account and living, and the sanction is smaller than families expect. I stay in the loan lane here and link the cost side and the study side below.

For the wider picture on Germany beyond the borrowing: the cost of studying in Germany breakdown.

Why a Germany loan is structured differently

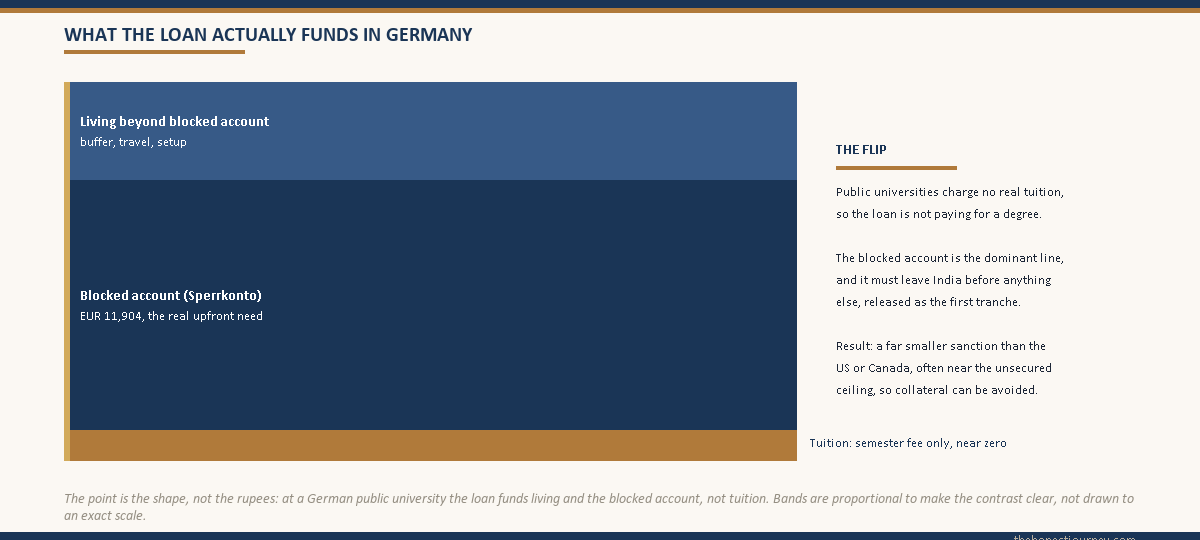

Most German public universities abolished tuition fees years ago. What remains is a semester contribution, the Semesterbeitrag, of roughly EUR 150 to 350 per semester, which often includes a public transport pass. That is a few thousand rupees a semester, not a tuition bill. So for a public-university student, the loan is not paying for a degree in the way a US or UK loan does. It is funding the cost of living, with the blocked account as the centrepiece.

That changes the whole shape of the sanction. Where a US Master’s pushes families into the collateral tier because the ticket is ₹50 lakh, a German public-university Master’s may need only ₹15 lakh to 20 lakh total, most of it the blocked account and living. That can sit at or near a PSU bank’s unsecured ceiling, which is a very different conversation from the one most families brace for. The general ceiling picture across destinations is in the maximum education loan amount in India post.

- Up to ₹4 lakh: no margin, no collateral, no guarantee. The semester contribution alone fits here, but nobody borrows just that.

- Above ₹4 lakh to ₹7.5 lakh: parent co-applicant and usually a guarantee, no tangible collateral. The blocked account alone can nearly fit here.

- Above ₹7.5 lakh to around ₹1.5 crore: tangible collateral mandatory at PSU banks. A public-university Germany case that includes living and a buffer often lands just above the line.

The blocked account, the heart of a Germany loan

The blocked account, the Sperrkonto, is the German version of the proof-of-funds requirement. You deposit a set sum in a German account before you arrive, and it is released to you in monthly installments to cover living costs, so the embassy knows you can support yourself for a year. For 2024 to 2025 the required amount rose to EUR 11,904, which is one year at EUR 992 per month. At ₹90 per euro, that is roughly ₹10.7 lakh, sitting in Germany before your course begins.

The official guidance on studying in Germany, including the financing proof, is published by the DAAD, the German Academic Exchange Service. The honest implication for your loan is the same as the GIC in Canada: the blocked account is a large upfront cash line that has to leave India before tuition or anything else, and a good lender funds it as the first tranche. The detailed mechanics of funding the Sperrkonto sit in the dedicated education loan for the German blocked account post, so I keep it brief here and focus on how it shapes the sanction.

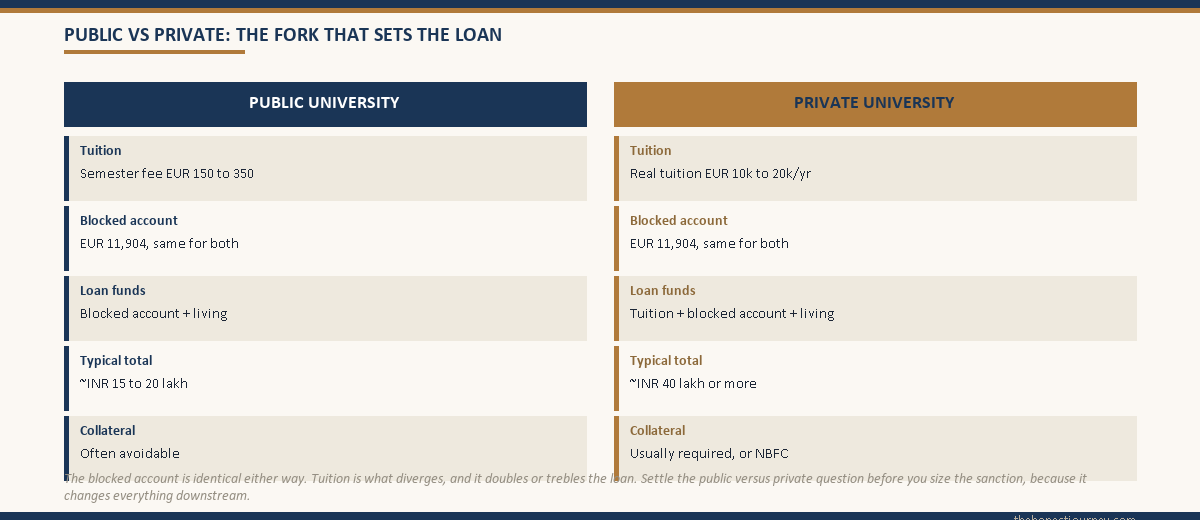

Public versus private, the fork that decides the sanction size

The big distinction in Germany is public versus private. Public universities, where the great majority of Indian students go, charge the small semester contribution and nothing more. Private universities and some specialised programs do charge real tuition, often EUR 10,000 to 20,000 a year, comparable to other destinations. The two cases produce very different loans.

For a public-university Master’s, the loan funds the blocked account plus living, and the sanction is small enough that many families avoid collateral entirely. For a private-university program, the loan looks like a normal abroad loan: tuition plus the blocked account plus living, often ₹30 lakh or more, back in collateral or NBFC territory. So the first question any honest lender should ask is which kind of institution you are joining, because it changes the sanction by a factor of two or more.

Faz's ruleTell the bank whether your university is public or private before anything else. A public-university Germany loan is a fraction of a private one, and the wrong assumption sends a family pledging property it never needed to pledge.

The single biggest mistake I see on Germany files is treating it like the US, assuming a big tuition-led ticket and lining up collateral. At a public university there is no real tuition. The money is the blocked account and living, often small enough to stay unsecured. Confirm your university type in writing, then size the loan to the blocked account plus living, not to an imagined tuition bill.

The worked INR sanction example for a public-university Master’s

Take a realistic public-university case. A student admitted to a two-year, taught-in-English Master’s at a public university. Tuition is effectively zero beyond a semester contribution of about EUR 300 each semester. The student needs the blocked account of EUR 11,904 for the first year, plus a living buffer beyond what the blocked account releases. At ₹90 per euro, the blocked account alone is ₹10.7 lakh.

| Item | EUR | INR (at 90) |

|---|---|---|

| Semester contribution (two years, four semesters) | ~1,200 | 1,08,000 |

| Blocked account (year-one living proof) | 11,904 | 10,71,360 |

| Additional living buffer, travel, insurance, setup | ~4,000 | 3,60,000 |

| Total funding need | ~17,104 | ~15,39,360 |

This student goes to a PSU bank for an overseas education loan of roughly ₹15.4 lakh. Because the amount is above ₹7.5 lakh, tangible collateral is technically required at the PSU bank, so the family pledges a fixed deposit or a small property. But notice how close this is to the unsecured line: a leaner Germany case, with a smaller living buffer, can land at or under ₹7.5 lakh and avoid collateral altogether, which almost never happens for the US or Canada.

Now the margin money. For studies abroad, PSU banks ask for 10 to 15 percent margin on amounts above ₹4 lakh, contributed alongside each disbursement. On a ₹15.4 lakh loan at 15 percent, the family puts in roughly ₹2.3 lakh across the schedule, and the bank funds the balance, with the blocked account released first.

| Funding layer | INR | Notes |

|---|---|---|

| Total funding need | 15,39,360 | The sanction basis |

| Family margin (15 percent) | ~2,30,904 | Paid alongside disbursements |

| Bank-funded loan | ~13,08,456 | Blocked account released first |

| Collateral | FD or small property, after haircut | Needed only because total tops ₹7.5 lakh |

If the same student were at a private university charging EUR 15,000 a year, the picture changes entirely. Tuition over two years would add roughly ₹27 lakh, pushing the total past ₹40 lakh, firmly into collateral or NBFC territory. The honest economics of the unsecured route, when you do need a larger sum, sit in the education loan for abroad studies without collateral post.

How banks handle a low-tuition destination

Banks are used to tuition-led loans, where the sanction tracks a large fee bill. Germany breaks that habit, and a branch that has funded few German files can get it wrong in two directions. It can over-size the loan, assuming a tuition bill that does not exist, or it can under-fund the blocked account because it does not understand the Sperrkonto is the real upfront need.

The correct handling is straightforward once you name it. The lender sizes the loan to the blocked account plus living plus the small semester contribution, releases the blocked-account amount as the first tranche so the visa proof is ready, and then releases the modest living top-ups as the year progresses. SBI’s overseas product details are on the SBI education loans page, and Bank of Baroda’s on the Bank of Baroda education loan page. Both can fund a Germany case cleanly when you tell them upfront that the blocked account is the priority line.

Faz's ruleFund the blocked account first, then living. The Sperrkonto has to sit in a German account before your visa interview, so the disbursement order must put it ahead of everything else.

The blocked account is your proof of funds for the visa, and it has to be in place before the interview, not after you arrive. Ask the bank explicitly to release the EUR 11,904 as the first tranche. If they queue it behind living top-ups or a tuition tranche that does not even exist, your visa proof will not be ready, and you will be back at the branch losing weeks you cannot spare.

What banks check on Germany-specific paperwork at sanction

Beyond the standard income and KYC documents, a Germany sanction file leans on a few destination-specific items.

- The admission letter or confirmation of enrolment from the university, stating the program and whether it is public or private.

- The semester contribution figure and, for a private university, the actual tuition schedule.

- The blocked-account requirement, so the lender funds the EUR 11,904 as the first disbursement to a recognised provider.

- Co-applicant income proof, since even a small Germany loan rests on the parent’s repayment capacity.

- For any amount above ₹7.5 lakh, the collateral documents and a valuation, though many lean Germany cases stay below that line.

The thing banks should get right, and the thing inexperienced branches miss, is that the blocked account is the upfront priority, not tuition. A clean Germany file releases the Sperrkonto first so the visa proof is ready. If you are carrying cash alongside, the sensible amount is covered in the how much money to carry abroad post.

The honest take on a Germany education loan

Germany is the value destination, and the loan reflects that. At a public university there is no real tuition, so the loan funds the blocked account and living, and the sanction is often half or less of a US or Canada loan. Many public-university students can keep the loan near or under the unsecured line and avoid pledging collateral, which is a genuine advantage you do not get elsewhere.

What goes wrong is treating Germany like any other destination. Over-preparing on collateral for a tuition bill that does not exist, or under-funding the blocked account because nobody explained it, are the two failure modes. And a private university changes everything: real tuition pushes the ticket back into collateral territory, so the public-versus-private question has to be settled before the loan is sized.

Germany rewards a student who understands its loan logic. Size the sanction to the blocked account plus living, fund the Sperrkonto first, and confirm your university type before anything else. If you want the full living-cost picture, the study in Germany guide covers the academic and arrival side, and this page stays in the loan lane.

Your loan sanction feeds straight into the visa funds proof. The whole visa process for Germany is in the Germany student visa guide.

FAQ

Can I get an education loan for Germany from Indian banks?

Yes. PSU banks like SBI and Bank of Baroda, and NBFCs, all fund studies in Germany. The difference from other destinations is the loan is usually smaller, because public universities charge near-zero tuition. The loan funds the blocked account of EUR 11,904 and living rather than a large tuition bill, so a public-university student often needs only ₹15 lakh to 20 lakh, sometimes near or under the PSU unsecured ceiling of ₹7.5 lakh.

Does the loan cover the blocked account for Germany?

It should, and the blocked account is the most important line to fund. The Sperrkonto requirement for 2024 to 2025 is EUR 11,904, roughly ₹10.7 lakh, deposited in a German account before you travel and released monthly for living. A good lender funds it as the first tranche so your visa proof of funds is ready for the interview. Ask the bank explicitly to release the blocked-account amount first, ahead of any living top-ups.

Is tuition really free in Germany?

At most public universities, yes, in the sense that there is no real tuition fee. What remains is a semester contribution of roughly EUR 150 to 350, which often includes a transport pass, a few thousand rupees a semester rather than a tuition bill. Private universities and some specialised programs do charge real tuition, often EUR 10,000 to 20,000 a year. So whether tuition is effectively free depends entirely on whether your university is public or private.

How much loan do I need for a public university in Germany?

For a public-university Master’s, the loan funds the blocked account of EUR 11,904 plus living plus the small semester contribution, so a typical total funding need is around ₹15 lakh to 20 lakh at ₹90 per euro. A leaner case can land at or under the PSU unsecured ceiling of ₹7.5 lakh and avoid collateral. A private university, with real tuition, pushes the total past ₹40 lakh and back into collateral or NBFC territory.

Do I need collateral for a Germany education loan?

Often not, which is unusual. Because a public-university loan can stay near or under the ₹7.5 lakh unsecured ceiling, many Germany students avoid pledging collateral entirely, something that almost never happens for the US or Canada. If your total need, including a living buffer, tops ₹7.5 lakh at a PSU bank, you will need a fixed deposit or small property as security. A private-university program with real tuition will need collateral or an NBFC.

How does the bank handle a low-tuition destination like Germany?

The lender sizes the loan to the blocked account plus living plus the semester contribution, not to a tuition bill, and releases the blocked-account amount first so the visa proof is ready. An inexperienced branch can get this wrong, either over-sizing the loan for tuition that does not exist or under-funding the Sperrkonto. Tell the branch on day one that your university is public and the blocked account is the priority line, and the file goes smoothly.

How much margin money is needed for a Germany loan?

For studies abroad, PSU banks ask for 10 to 15 percent margin money on the loan amount above ₹4 lakh, paid alongside each disbursement rather than upfront. On a ₹15.4 lakh loan at 15 percent, the family contributes roughly ₹2.3 lakh across the tranches. Because Germany loans are smaller, the margin in rupee terms is correspondingly smaller. Confirm at the branch exactly how your margin is computed, since a scholarship can sometimes be folded into it.

Is a Germany loan worth it compared to other destinations?

For value, Germany is hard to beat. A public-university Master’s funds at a fraction of a US or Canada ticket, because there is no real tuition, and many students avoid collateral altogether. The repayment runway depends on the post-study job market and German-language ability for some roles, so weigh that honestly. A private-university program loses much of the cost advantage. Settle the public-versus-private question first, then judge whether the smaller loan and the runway line up.

Faz · The Honest Journey · 2026