Studying abroad from India typically costs 25 to 60 lakh per year all-in, covering tuition, living, forex, insurance, and one-time fees, not just the tuition a consultancy quotes. Most families fund it with an education loan at 60 to 75 percent, family savings at 15 to 30 percent, and a scholarship at 5 to 15 percent where you actually win one. Your destination and course set the exact mix.

Once your funding is sorted, plan the move with our pre-departure checklist for Indian students.

Every Indian family I have spoken to about studying abroad eventually asks the same question, and it is almost never the one they opened with. They start with “which country is best” or “which university gives scholarships.” Within twenty minutes, the real question surfaces: can we actually afford this, and if we borrow, will the EMI break us. The honest answer depends on numbers most families never see laid out in one place before they sign a sanction letter or wire a deposit.

This guide is that one place. Real costs, real funding mixes, real forex rules, real scholarship odds, and what each destination actually demands of an Indian student before the visa officer stamps the page. If you are at the stage of building a number on paper before you commit, read this first.

Studying abroad from India typically costs ₹25 to 60 lakh per year all-in, covering tuition, living, forex, insurance, and one-time costs. Most families fund it with a mix of education loan (60 to 75 percent), family savings (15 to 30 percent), scholarship (5 to 15 percent where you actually win one), and part-time work that covers living expenses but rarely tuition. The exact mix is set by your destination, your course, and your family’s income band.

What this guide covers, section by section. We start with what “cost” really means once you add the line items most agents skip. Then the tuition vs living vs one-time split, the genuinely cheaper destinations and their catch, country-by-country numbers for Canada, Germany, Australia, Ireland, and the Netherlands, how to rank your funding sources, the realistic scholarship list, visa proof of funds country by country, forex and TCS, part-time work limits, and the two calculators that will save you the most time.

What “cost of studying abroad” actually means (the four-line bill)

The number a consultancy quotes you is almost always just tuition for year one. It is the cleanest line, the easiest to compare, and the most misleading. The real bill has four lines, and three of them are bigger than families expect.

Line one is tuition. For a master’s in the UK, that ranges from GBP 18,000 to GBP 38,000 per year. In Canada, CAD 25,000 to CAD 55,000. In Australia, AUD 35,000 to AUD 55,000. In Germany at a public university, often zero, though semester contributions of EUR 150 to EUR 350 still apply. Tuition is the headline, but for a two-year US MS or MBA it can be the smaller half of the total.

Line two is living. Rent, food, transport, utilities, phone, internet. London is GBP 1,300 to GBP 1,800 a month outside zone one. Toronto is CAD 1,800 to CAD 2,400. Sydney is AUD 2,000 to AUD 2,800. Berlin is EUR 1,100 to EUR 1,500. Multiply by 12 and you usually find living equals or beats tuition.

Line three is the one-time bill. Application fees (USD 75 to USD 150 each, across 6 to 10 universities). GRE or GMAT (USD 220 to USD 275). IELTS or TOEFL (₹17,000 to ₹19,500). Visa fee (GBP 524 for the UK, CAD 235 for Canada, AUD 1,840 for Australia). SEVIS or IHS health surcharge (USD 350 for the US, GBP 776 per year for the UK). Flight, initial deposit on housing, laptop, winter clothing, first-month groceries. This stack lands between ₹3 to 6 lakh before you have attended a single class.

Line four is the forex and tax cost. TCS on foreign remittances above ₹7 lakh in a financial year, currency conversion margins on your forex card, wire transfer fees, and the slow bleed of remitting living expenses every quarter at whatever the bank’s spread happens to be that day. On a ₹40 lakh annual outflow, this can easily run ₹1 to 2 lakh that nobody itemises in advance.

Add the four lines and a UK master’s that started at GBP 25,000 tuition becomes a ₹45 to 55 lakh year. That is the bill you need to fund. If you want the full deep-dive on building this number for your specific course, read how to fund study abroad from India.

All-country cost comparison at a glance

Before the country-by-country detail, here is the whole field in one place. These are indicative ranges for an Indian student, not quotes, and they move with the exchange rate, your city, your university tier, and your course. Use them to shortlist, then read the country section for the real detail. The annual figure combines tuition and living. The USD column uses a rough rate near 83 rupees to the dollar, so treat it as a guide and not a precise conversion.

| Country | Tuition per year (INR) | Living per year (INR) | Total per year (INR) | Total per year (USD) |

|---|---|---|---|---|

| USA | 23 to 57 lakh | 10 to 23 lakh | 36 to 80 lakh | 43k to 96k |

| UK | 17 to 42 lakh | 10 to 20 lakh | 35 to 65 lakh | 42k to 78k |

| Canada | 13 to 33 lakh | 9 to 17 lakh | 22 to 45 lakh | 27k to 54k |

| Australia | 16 to 30 lakh | 11 to 18 lakh | 32 to 65 lakh | 39k to 78k |

| Ireland | 16 to 25 lakh | 10 to 16 lakh | 30 to 45 lakh | 36k to 54k |

| Germany | little to none (public) | 9 to 13 lakh | 13 to 22 lakh (full degree) | 16k to 27k |

| Netherlands | 13 to 20 lakh | 10 to 15 lakh | 25 to 40 lakh | 30k to 48k |

Tuition vs living vs one-time costs (the breakdown most families miss)

Once you have the four-line frame, the ratios matter more than the headline. Two students at the same Canadian university, one in a one-year postgraduate diploma at a college and one in a two-year master’s at the same city’s university, end up with completely different totals because the tuition-to-living ratio flips.

| Course type | Tuition share | Living share | One-time + forex | Typical 1-year total (INR) |

|---|---|---|---|---|

| UK 1-year master’s | 55 to 65 percent | 30 to 40 percent | 5 to 8 percent | ₹40 to 55 lakh |

| US 2-year MS | 60 to 70 percent | 25 to 35 percent | 5 to 8 percent | ₹50 to 75 lakh per year |

| Canada master’s at university | 50 to 60 percent | 35 to 45 percent | 5 to 8 percent | ₹30 to 45 lakh |

| Canada PG diploma at college | 35 to 45 percent | 45 to 55 percent | 8 to 12 percent | ₹22 to 32 lakh |

| Germany public university master’s | 2 to 8 percent | 75 to 85 percent | 10 to 15 percent | ₹13 to 18 lakh |

| Australia master’s | 55 to 65 percent | 30 to 40 percent | 5 to 8 percent | ₹40 to 55 lakh |

Two things to notice. First, Germany flips the ratio because tuition is near zero, so the cost is almost entirely your living expenses for two years. That is why a German master’s totals ₹25 to 35 lakh across the full degree while a UK master’s runs ₹45 to 55 lakh in one year. Second, the Canada college route works financially not because tuition is much lower, but because rent in smaller cities like Kitchener or Cape Breton is half of what Toronto or Vancouver charge.

Faz's ruleThe headline tuition number is the smallest lie a brochure tells you. The real bill is four lines, and three of them are not on the brochure.

Build your own version of the four-line bill before you talk to any consultancy or bank. Tuition, living, one-time, forex. The bank will lend against the total. Your family will fund the gap. The bigger your underestimate at this stage, the messier the second-year scramble.

If you want the full deep-dive on building this breakdown for your specific destination and course, read the funding plan guide for Indian students.

Cheapest destinations (and the honest catch)

Cheap is a real lever. Germany, Norway, France public universities (the cost of studying in France for Indian students shows just how low the public route runs), and parts of Eastern Europe (Poland, Hungary, Czechia for medicine) offer total degree costs that are a fraction of what the US or Australia charge. A two-year German master’s totals ₹25 to 35 lakh across the entire program, not per year. Norwegian public universities until recently charged no tuition even for non-EU students, though that has tightened post 2023 for non-EEA students.

The catch is rarely tuition. It is everything around it. Language is the first wall. Most truly free German programs are in German. The English-taught master’s options exist (around 1,800 across Germany) but you compete with a global applicant pool for limited seats, and your post-study employment ceiling is much lower without German B2 or C1.

The second wall is post-study work and residency. Cheap European destinations vary widely on this. Germany gives 18 months of post-study work and a relatively clean path to permanent residency after 21 to 33 months of qualified employment. Norway and France are also generous. Eastern European countries with cheap medical degrees often do not lead to local jobs at all, and the Indian student returns to write FMGE or NExT for license back home.

The third wall is brand and salary. A German Fachhochschule degree is a perfectly good qualification, but it does not carry the same recruiter recognition in India as a US-top-30 master’s. If your goal is a leadership track in India after the degree, cheap-and-good is real, but cheap-and-prestigious is rare.

If you want the full deep-dive on the genuinely affordable destinations and what each demands of you, read the cheapest country to study abroad for Indian students breakdown.

Country-by-country cost: Canada

Canada has been the default mass-market destination for Indian students for nearly a decade, and the cost structure reflects that. Tuition at universities runs CAD 25,000 to CAD 55,000 per year for a master’s. Colleges (which run postgraduate diplomas) are CAD 16,000 to CAD 22,000 per year. Living costs vary sharply by city: Toronto and Vancouver demand CAD 1,800 to CAD 2,400 a month, while Halifax, Winnipeg, or Regina sit closer to CAD 1,200 to CAD 1,600.

The Canada-specific cost line that catches many families off guard is the GIC. The Guaranteed Investment Certificate is a CAD 20,635 (2024 onwards from CAD 10,000) lump sum that you wire to a Canadian bank before applying for the study permit. It is your money, returned to you in monthly instalments after you land. But it is a one-time forex outflow that needs to happen before the visa, and it counts toward your TCS calculation for the year. Refer to the official guidance on studying in Canada for the current GIC threshold.

The post-study work permit (PGWP) is what makes the Canada math work for most Indian students. A two-year program qualifies for a three-year PGWP, which is long enough to gain Canadian work experience and apply for permanent residency through Express Entry or a provincial nominee program. The 2024 changes to PGWP eligibility (linking it more tightly to programs aligned with labour market needs) tightened this, so verify your specific program qualifies before you commit.

Total one-year all-in: ₹22 to 45 lakh depending on city and university tier. Two-year programs roughly double that, with the catch that the GIC is a one-time, not annual, requirement. If you want the full deep-dive on Canada costs, work permits, and the GIC mechanics, read study in Canada for Indian students and the dedicated GIC Canada education loan guide.

Country-by-country cost: Germany

Germany is the destination that breaks the cost-of-studying-abroad mental model. Public universities, which include most of the well-regarded technical universities (TU Munich, TU Berlin, RWTH Aachen, KIT), charge no tuition for master’s programs even for non-EU students. Semester contributions cover student services and a local transport pass, typically EUR 150 to EUR 350 per semester. Some states (notably Baden-Wurttemberg) charge non-EU students EUR 1,500 per semester, but most do not.

Living costs are the real expense. The official blocked account requirement (the funds you must prove for your visa) is EUR 11,904 per year as of 2024, which works out to roughly ₹10.7 lakh per year. Real spending varies: Munich and Frankfurt are at the top end (EUR 1,200 to EUR 1,500 a month), while smaller university towns like Karlsruhe, Dresden, or Magdeburg sit closer to EUR 800 to EUR 1,000.

The Indian student in Germany is funding two things: living expenses for two years, and the blocked account (which is your own money returned monthly). Total degree cost: ₹13 to 22 lakh across the full two-year master’s, depending on city, with the complete cost of studying in Germany for Indian students itemised separately. That is less than one year of a comparable US or UK master’s.

The trade-offs: most undergraduate programs and many master’s are in German, so plan for a parallel language investment if you want broad program access and employability. The official German Academic Exchange Service (DAAD) is the cleanest source for program search and scholarship options. Post-study, Germany gives an 18-month job-seeker visa and a relatively quick path to permanent residency for qualified workers. If you want the full deep-dive on costs, blocked account mechanics, and program search in Germany, read study in Germany for Indian students.

Country-by-country cost: Australia

Australia has tightened sharply since late 2023, and the cost reflects both currency strength and post-COVID policy shifts. Tuition for a master’s at a Group of Eight university (Melbourne, Sydney, ANU, UNSW, Monash, UQ, UWA, Adelaide) runs AUD 38,000 to AUD 55,000 per year. Regional and lower-tier universities are AUD 30,000 to AUD 38,000.

Living costs are now the largest line for many students. Sydney rents have spiked to AUD 2,200 to AUD 2,800 a month for a shared apartment in a decent suburb. Melbourne is slightly cheaper at AUD 1,800 to AUD 2,400. Brisbane, Adelaide, and Perth run AUD 1,500 to AUD 2,000. The official Department of Home Affairs financial requirement for a student visa is AUD 24,505 per year for the student, which sets the floor for what the visa officer expects you to be able to fund.

The 2024 changes to the Genuine Student requirement (replacing the older Genuine Temporary Entrant rule) and the higher financial requirement have made the visa more selective, and the post-study work rights for some courses were cut back. The Temporary Graduate visa (subclass 485) still applies to most master’s by coursework graduates but the duration depends on your qualification and field.

Total one-year all-in for a Go8 master’s in Sydney or Melbourne: ₹50 to 65 lakh, and the full cost of studying in Australia for Indian students breaks this down city by city. For a regional university in a smaller city, ₹32 to 45 lakh. If you want the full deep-dive on costs, visa rules, and post-study work in Australia, read study in Australia for Indian students.

Country-by-country cost: Ireland

Ireland has quietly become one of the more attractive destinations for Indian students in business, tech, and pharma, largely because of the two-year post-study work permit (Stay Back Option) and the cluster of multinational employers around Dublin. Tuition for a master’s at the major universities (Trinity College Dublin, UCD, UCC, NUI Galway) runs EUR 18,000 to EUR 28,000 per year for taught master’s programs, with business and computer science at the higher end.

Living costs in Dublin are the major constraint. Rent has surged to EUR 800 to EUR 1,200 a month for a single room in a shared house, with the city centre well above that. Cork, Galway, and Limerick are EUR 600 to EUR 900. Total monthly living budget for Dublin: EUR 1,400 to EUR 1,800 including everything.

The Irish Naturalisation and Immigration Service requires proof of EUR 10,000 in funds available for the visa. Tuition is paid up front (typically before visa application) and the post-study Stay Back is currently two years for level 9 (master’s) graduates, which is generous compared to the UK Graduate Route’s two years but with arguably stronger employer demand in Dublin’s tech and pharma clusters.

Total one-year all-in: ₹30 to 45 lakh. The Ireland math works particularly well for students targeting Dublin’s multinational employers (Google, Meta, Pfizer, Stripe, Accenture) where a strong post-study trajectory can repay the loan within the Stay Back period itself. If you want the full deep-dive on costs, visa, and post-study work in Ireland, read study in Ireland for Indian students, and for the numbers alone the cost of studying in Ireland for Indian students goes line by line.

Country-by-country cost: Netherlands

The Netherlands sits in an interesting middle ground: high-quality English-taught programs at internationally ranked universities (Delft, Amsterdam, Erasmus Rotterdam, Eindhoven, Utrecht, Leiden), tuition that is well below the UK or US, and a post-study orientation year (zoekjaar) for skilled migrants. Tuition for a master’s runs EUR 15,000 to EUR 22,000 per year at the major research universities, with engineering, business, and computer science at the higher end.

Living costs are real. Amsterdam is the most expensive, with single rooms now EUR 800 to EUR 1,200 per month in a shared apartment. Eindhoven, Delft, and Groningen are EUR 500 to EUR 800. Total monthly living budget: EUR 1,200 to EUR 1,700 in Amsterdam, EUR 900 to EUR 1,300 in smaller cities.

The Dutch immigration service (IND) requires proof of EUR 14,000 to EUR 16,000 per year for the visa, transferred to the university or a blocked account before residence permit issuance. After graduation, the orientation year visa gives you 12 months to find a qualifying skilled migrant job, and the salary threshold for the highly skilled migrant scheme (around EUR 2,800 per month gross for recent graduates under 30) is well below what Indian tech and business master’s graduates typically command in Dutch starting salaries.

Total one-year all-in: ₹25 to 40 lakh. The Netherlands math has become more attractive as the UK and Australia have tightened, and the cluster of tech and engineering employers (ASML, Booking, Adyen, Philips, Shell) supports a strong post-study pathway. If you want the full deep-dive on costs, residence permit, and post-study work in the Netherlands, read study in Netherlands for Indian students, and the dedicated cost of studying in the Netherlands for Indian students breaks the budget down in full.

Country-by-country cost: USA

The USA has the widest cost range of any destination, and the I-20 your university issues is the only number that matters. It is the cost of attendance the school estimates, and it doubles as the figure the consulate uses for your F1 proof of funds. Tuition and mandatory fees run roughly ₹23 to 35 lakh a year at a state university and ₹44 to 57 lakh a year at a private one. Living plus insurance adds another ₹10 to 18 lakh a year depending on the city. A typical STEM Master’s at a mid-tier state school sits around USD 38,000 to 55,000 a year all-in.

During study, F1 students can work up to 20 hours a week on campus in term time and full-time in official breaks, which barely covers groceries and never touches tuition. The real return comes after. OPT gives you 12 months of work authorisation on graduation, and a STEM-designated degree adds a further 24 months of STEM-OPT, for up to three years in total. That post-study window is what lets a US Master’s pay for itself, which is why the funding plan matters more here than anywhere else.

Total all-in for a two-year STEM Master’s at a state university lands around ₹75 to 85 lakh in 2026, and ₹1.2 to 1.5 crore at a private university. For the full breakdown of the I-20, fees, work rights, and the worked rupee total, read cost of studying in USA for Indian students.

Country-by-country cost: UK

The UK stays popular with Indian students because a taught Master’s is one year, which keeps the total degree cost lower than most countries even though the annual numbers look high. Tuition runs roughly ₹17 to 24 lakh a year at wider post-92 universities, ₹24 to 31 lakh at mid-tier non-London universities, and ₹27 to 42 lakh at a Russell Group university, with Oxbridge and Imperial higher still. Living costs add ₹10 to 15 lakh a year outside London and ₹15 to 20 lakh a year in London.

You can work up to 20 hours a week during term and full-time during official vacations. After you finish, the Graduate Route lets you stay and work for two years after a bachelor’s or master’s, and three years after a PhD, with no employer sponsor required. Because the degree is a single year, the all-in cost of a one-year Master’s for an Indian student in 2026 lands between roughly ₹35 lakh and ₹65 lakh, with a Russell Group Master’s in London coming to around ₹55 lakh.

For the full picture on tuition tiers, the Immigration Health Surcharge, living costs, and the Graduate Route, read cost of studying in UK for Indian students.

Funding sources, ranked

Most families build their funding stack in the wrong order. They start with “how much loan can we get” and back into the destination. The correct order is reverse: pick the destination and course where the post-degree outcome justifies the bill, then assemble funding from the cheapest source to the most expensive.

Rank one is scholarship. It is free money. Even a partial tuition waiver of 25 to 50 percent at a US or UK university can change your loan size by ₹15 to 30 lakh over the program. The realistic odds are low (most named scholarships have single-digit acceptance rates for Indian students), but the time investment is small relative to the payoff if you win.

Rank two is family savings. Money that is not borrowed has no interest cost. The instinct to “preserve savings and take the full loan” is almost always wrong if the loan is at 11 to 14 percent and your savings are sitting in an FD at 6 to 7 percent. Use savings first, borrow the gap.

Rank three is secured education loan from a public sector bank. Collateral-backed loans from SBI, BoB, Canara, and PNB run 8.5 to 10.5 percent. The collateral can be property, FD, or LIC policy. The catch is processing time (4 to 8 weeks) and paperwork weight, but the rate difference vs an unsecured NBFC loan (which runs 11.5 to 14 percent) is meaningful.

Rank four is unsecured education loan from an NBFC or private bank. Faster processing, no collateral, but higher rates. This is what most students at major foreign universities default to because the loan amount needed (₹30 to 60 lakh) exceeds what they can secure with property.

Rank five is part-time work during studies. This funds living expenses (or part of them) but never tuition. Treat it as a way to reduce your monthly forex outflow, not as a primary funding source.

Rank six is the last-resort credit (top-up education loan, personal loan, gold loan from family). High cost. Use only to bridge a one-off gap. If your funding plan requires this at sanction time, the plan is undersized.

If you want the full deep-dive on stacking these in the right order, read how to fund study abroad and the specific tradeoff post on education loan vs self-funding.

Faz's ruleBorrow the gap, not the maximum. The bank's sanction limit is what they will lend you, not what you should take.

Every ₹5 lakh you do not borrow is roughly ₹8 to 9 lakh you do not repay over 10 years at 11.5 percent. Use family savings first, scholarships where they land, and the loan only for the genuine gap. The instinct to “preserve savings, take the full loan” is almost always wrong when the loan rate is double your savings yield.

Scholarships: the realistic short list

Scholarships are a real funding source for a small percentage of Indian students. The challenge is filtering the long list of “available” scholarships to the ones with a non-trivial Indian acceptance rate and an application window that fits your timeline.

For UK master’s, the Chevening Scholarship (FCDO-funded, fully covers tuition, living, flights for a one-year master’s) is the gold standard. Around 60 to 80 Indian students win it annually. The Commonwealth Scholarship is similar in scale but tighter in eligibility. Both require strong work experience and a clear leadership story.

For US master’s, the Fulbright-Nehru and Inlaks Shivdasani are the named scholarships with consistent Indian intake. Most US funding for international master’s students comes from university-internal merit aid, which is generally a 10 to 50 percent tuition waiver baked into your admission decision. Apply to schools that are known to offer this, and apply early in the cycle when the financial aid pool is fresh.

For Germany, the DAAD scholarship database is the official source and covers a wide range of stipends from short-term research to full master’s funding. Awards are competitive but realistic for strong academic profiles.

For Canada and Australia, named scholarships exist but are smaller in number. Most funding comes from university-internal awards and is admission-linked. Apply early.

The general filter: if a scholarship is advertised on a consultancy website with no link to an official .gov, .edu, or .ac.uk source, it is almost always a small token award (₹50,000 to ₹2 lakh) being marketed as if it were a major win. Apply to the named, government-backed, or university-internal scholarships first. Skip the rest.

Faz's ruleScholarships are real, but they are not a funding plan. Apply seriously to the top 5 to 10 named awards in your destination. Build your loan and savings plan as if you will win none.

The student who builds a plan assuming a Chevening or Fulbright will land and is wrong has a ₹30 to 40 lakh gap to scramble for in May or June. The student who builds a plan as if scholarships will not land and then wins one has ₹30 lakh of breathing room. Plan from the harder case.

If you want the full deep-dive on scholarships for Indian students, including the realistic acceptance odds and application timelines, read scholarships for Indian students to study abroad after 12th.

Visa funds: proof of funds country by country

Every country requires you to prove, before the visa is granted, that you can fund the first year of tuition plus living. The amounts and the acceptable forms of proof vary, and getting this wrong is one of the most common visa refusal reasons for Indian students.

| Country | Proof of funds required (year 1) | Acceptable forms | Common refusal reason |

|---|---|---|---|

| UK | Tuition + GBP 1,334/month (London) or GBP 1,023/month (outside) for 9 months | Bank statement (28 days mature), education loan sanction letter, official sponsor letter | Funds held for less than 28 consecutive days |

| Canada | Tuition + CAD 20,635 GIC + CAD 10,000 (or more, varies by province) | GIC certificate, education loan sanction, bank statements, sponsorship | GIC not in place at application time |

| Australia | AUD 24,505 living + tuition + travel | Bank statement, education loan sanction, sponsorship affidavit | Funds not satisfying Genuine Student criteria |

| Germany | EUR 11,904 blocked account per year | Blocked account confirmation from approved provider (Expatrio, Fintiba, Coracle, Deutsche Bank) | Blocked account not opened at application |

| Ireland | EUR 10,000 + tuition (typically paid up front) | Bank statement, education loan sanction, paid tuition receipt | Tuition not paid prior to visa application |

| Netherlands | EUR 14,000 to EUR 16,000 per year | Transferred to university or blocked account before residence permit | Funds transferred after deadline |

The education loan sanction letter is accepted as proof of funds in every major destination, but the wording matters. The visa officer is looking for an unconditional sanction (not “in principle”), a clear disbursement schedule, and the lender on the approved list (most major Indian banks and the recognised NBFCs qualify). For the deep mechanics of getting the sanction letter to satisfy visa requirements, read the education loan sanction letter as proof of funds guide and the specific proof of funds for student visa breakdown.

If part of your funding comes from a family member who is not a co-applicant on the loan, you will need a notarised sponsorship affidavit. The format and notarisation requirements vary by country. The dedicated sponsorship affidavit for student visa guide covers the country-specific templates.

For the official rules, refer to the destination embassy’s own pages: UK student visa guidance, study in Canada, and the foreign service guidance on studying abroad from the Ministry of External Affairs.

Forex and money abroad

The forex and tax line is the one most families discover only after it has hit them. Three rules to internalise before the first transfer.

Rule one is the Liberalised Remittance Scheme. The RBI’s LRS allows resident Indians to remit up to USD 250,000 per financial year per person for permitted purposes, including education. The full LRS framework is on the Reserve Bank of India site. For most undergraduate or master’s costs, USD 250,000 per remitter is well above what you need. If the total bill exceeds this, parents can each use their LRS limit (married couple, two limits).

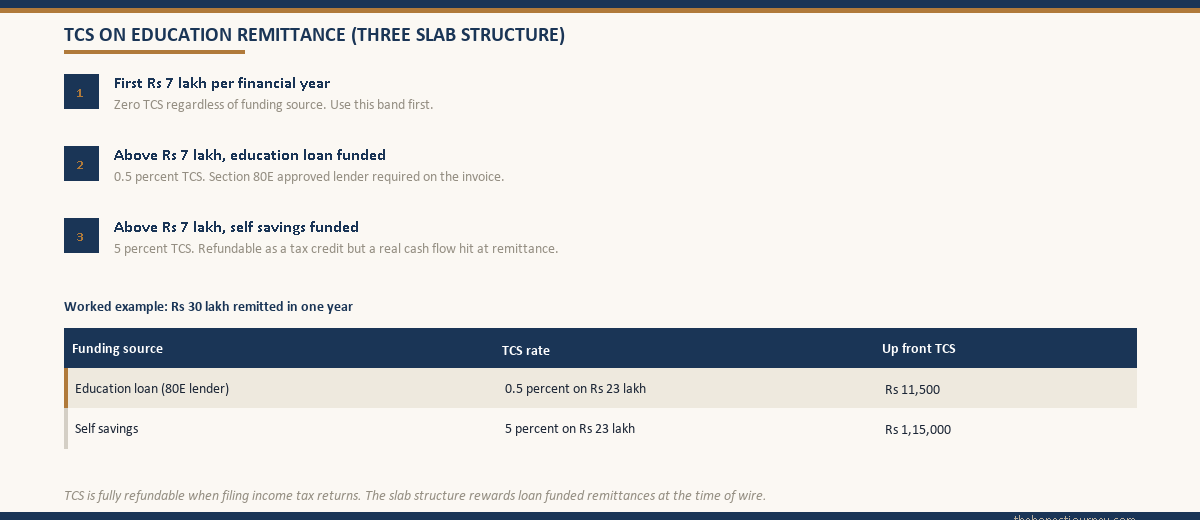

Rule two is TCS. Tax Collected at Source on foreign remittances for education works in three layers. Up to ₹7 lakh in a financial year, no TCS. Above ₹7 lakh, if the remittance is funded by an education loan from a Section 80E approved lender, TCS is 0.5 percent. If funded from self-savings, TCS is 5 percent. The detailed rules are in the Income Tax Department circulars. TCS is fully refundable as a credit against your tax liability when filing returns, but it is a real cash-flow hit at the time of remittance. For the full deep-dive on TCS mechanics, including how to structure remittances to minimise the up-front bleed, read TCS on education loan in India.

Rule three is which money instrument to carry. The clean stack for most Indian students is: forex card (loaded once or twice a semester for predictable monthly spending), a small amount of USD or destination currency cash for the first 72 hours, an international debit card from your Indian bank as backup, and within the first week of landing, a local bank account opened on a student account scheme. For the comparison of major forex card options and how much cash to carry vs load, read how much money to carry abroad as a student and the dedicated best forex card for students review.

Part-time work: what it really covers

Every Indian student family has heard the “she will work part-time and cover her own expenses” story. Some of it is true. Most of it is overstated. The honest math by destination is below.

UK: 20 hours per week during term, full-time during vacations. Minimum wage at GBP 11.44/hour (April 2024) means roughly GBP 220 per week, or GBP 880 per month before tax. After tax and the realistic reality that hospitality and retail are the dominant sectors hiring students, expect GBP 600 to GBP 800 net per month. That covers about half of London rent or most of living costs outside London. It does not touch tuition.

Canada: 24 hours per week during term as of late 2024 (was 20, then briefly unlimited, now 24). Minimum wage varies by province, around CAD 16 to CAD 17/hour. Expect CAD 1,200 to CAD 1,600 per month net. Covers most of living costs in smaller cities, half of living costs in Toronto/Vancouver.

Australia: 24 hours per week during term (was 20, then 48, now 24). AUD 24/hour minimum wage. Expect AUD 1,500 to AUD 2,000 per month net. Covers most of living costs outside Sydney.

Germany: Limited to 140 full days or 280 half days per year for non-EU students. At EUR 12 to EUR 15/hour for typical student jobs, expect EUR 400 to EUR 800 per month net during the active periods. Combined with the lower cost base, this can cover most of living costs.

Ireland: 20 hours per week during term, 40 during holidays. EUR 13.70 minimum wage. Expect EUR 800 to EUR 1,100 per month net. Covers about half of Dublin living costs.

Netherlands: Non-EU students can work 16 hours per week during term or full-time in summer, with a separate work permit required from the employer. EUR 13 to EUR 14/hour for typical student work. Expect EUR 700 to EUR 1,000 per month net.

The honest pattern: part-time work covers some-to-most of living, almost never tuition, and only after you have settled in (usually month 2 or 3, not week 1). Plan your loan and savings as if the part-time income is zero, and treat any earnings as reduced loan top-ups or living buffer. For the full deep-dive on country-by-country work rules and the realistic earnings vs spend ratio, read part-time work while studying abroad.

Faz's rulePart-time work covers living expenses, not tuition. If your funding plan needs part-time earnings to cover tuition, the plan is broken before you land.

The first three months abroad are the most expensive (deposit, setup, no income yet) and the hardest to find a stable part-time role. Build your loan and savings to fund the first semester completely. Treat any part-time income as a buffer, not a budget line.

Calculators you should use

Two calculators on this site will save you the most time at the planning stage, and they are the ones I would use first if I were starting from scratch.

The first is the cost of studying abroad calculator. You enter destination, course type, city tier, and duration, and it gives you the full four-line bill (tuition, living, one-time, forex) in INR for the full program. It is the fastest way to compare two destinations on like-for-like terms (a UK one-year master’s vs a German two-year master’s, or Canada college vs Australia regional university). Use it before you fix on a destination.

The second is the TCS on foreign remittance calculator. Enter your annual remittance total and your funding source split (loan vs self), and it gives you the TCS hit per remittance and per year. This is the calculator most families never run, which is why the TCS line lands as a surprise at the first wire. Run it before the first remittance, and structure your transfers across the financial year if it makes sense for cash flow.

If you want to use them now, the cost of studying abroad calculator and the TCS on foreign remittance calculator are both free, no sign-up, and the math is shown so you can verify it yourself.

Where to go next

You arrived at this guide with a question. The next step depends on which question is still open.

If you are still picking a destination, start with the cost comparison and work backward to what your funding can support. The cheapest country to study abroad for Indian students post is the clearest decision tree if budget is the main constraint. If you are weighing the destinations that fewer agents push but that we rate highly on cost to outcome, read our guides to studying in Italy for Indian students, studying in Dubai and the UAE for Indian students, and studying in Sweden for Indian students.

If you have a destination in mind and need to build the funding stack, read how to fund study abroad for the order-of-sources framework, then the education loan vs self-funding deep-dive for the loan-vs-savings call.

If your visa application is the next milestone, the proof of funds for student visa guide and the destination-specific posts on Canada, Germany, Australia, Ireland, and the Netherlands have the embassy-by-embassy checklists.

If you are at the forex and remittance stage, the forex card comparison and the TCS on education loan guide are the two pieces most students wish they had read before the first transfer.

Budget sorted, the visa is the next real hurdle, and each country runs its own process, fee and funds rule. The full walkthrough per destination is in our student visa guides for Canada, the USA, the UK, Australia, Germany, New Zealand, Ireland, France, the Netherlands and Singapore.

FAQ

What is the total cost of studying abroad for Indian students in 2026?

The all-in cost ranges from ₹13 lakh (Germany public university, full two-year master’s) to ₹75 lakh per year (US top-tier MS or MBA). Mid-range destinations like Canada, Ireland, and the Netherlands sit between ₹25 and ₹45 lakh per year all-in, and New Zealand lands in a similar band, as the cost of studying in New Zealand for Indian students sets out. The total includes tuition, living, one-time costs (visa, applications, tests, flight, deposits) and forex and TCS overhead. The single biggest variable is destination and city tier, not university tier within a country.

Which is the cheapest country to study abroad for Indian students?

Germany is the cheapest for a high-quality, internationally recognised master’s degree at roughly ₹13 to 22 lakh for the full two-year program at a public university. Norway, France public universities, and parts of Eastern Europe are also low-cost, though they vary on language requirements and post-study work rights. Cheap and well-recognised globally narrows the list quickly. The DAAD scholarship search is the cleanest entry point if Germany is on your shortlist.

How much education loan can I get to study abroad?

Indian banks and NBFCs sanction education loans up to ₹1.5 crore for studies abroad, with most students borrowing ₹25 to 60 lakh based on destination and course. Public sector banks (SBI, BoB, Canara, PNB) typically require collateral above ₹7.5 lakh. NBFCs (HDFC Credila, Avanse, Auxilo, InCred) offer unsecured loans up to ₹50 to 75 lakh but at higher rates (11.5 to 14 percent) compared to secured public bank loans (8.5 to 10.5 percent). Your sanction limit depends on co-applicant income, collateral, and the university’s recognition status with the lender.

What is TCS on foreign remittance for education?

TCS on foreign remittances for education works in three slabs. The first ₹7 lakh per financial year per remitter has no TCS. Above ₹7 lakh, remittances funded from a Section 80E approved education loan attract 0.5 percent TCS. Remittances funded from self-savings attract 5 percent TCS. TCS is fully refundable as a tax credit when filing returns, but it is collected up front at the time of remittance and is a cash-flow consideration. The Income Tax Department publishes the current rates and exemption details.

What is the proof of funds required for a UK student visa?

The UK student visa requires you to show tuition for the first year plus living costs of GBP 1,334 per month for nine months if studying in London, or GBP 1,023 per month for nine months elsewhere. Funds must be held in an acceptable account for at least 28 consecutive days before application, with the statement dated within 31 days of submission. An unconditional education loan sanction letter from a recognised Indian lender is accepted as proof. The official UK government student visa page lists the current amounts and acceptable forms.

What is the GIC for Canada and how does it work?

The Guaranteed Investment Certificate (GIC) is a mandatory upfront deposit of CAD 20,635 (as of 2024) that Indian students applying for a Canadian study permit through the Student Direct Stream must wire to a participating Canadian bank before visa application. The funds are returned to you in monthly instalments of roughly CAD 1,700 after you land, covering your living expenses for the first year. The GIC is your own money, but it is a one-time forex outflow and counts toward your TCS calculation in the year it is remitted.

Can I work part-time while studying abroad and cover my living costs?

In most major destinations, yes, you can cover most of your living costs through part-time work. The UK allows 20 hours per week during term, Canada and Australia allow 24 hours per week, Ireland 20 hours, the Netherlands 16 hours, and Germany 140 full days per year for non-EU students. Net earnings typically run EUR 600 to AUD 2,000 per month depending on country and minimum wage. Part-time work does not realistically cover tuition. Build your funding plan as if part-time income is zero, and treat any earnings as buffer.

Which forex card is best for Indian students going abroad?

The best forex card depends on destination currency, monthly spend pattern, and reload frequency. Major Indian banks (SBI, HDFC, Axis, ICICI) and platforms like Niyo Global and BookMyForex offer multi-currency cards with varying markups, ATM withdrawal fees, and reload charges. The general rule: prefer zero or low-markup cards for predictable monthly living spend, and open a local bank account in your destination country within the first two weeks to handle ongoing expenses with lower friction.

Are scholarships realistic for Indian students studying abroad?

Yes, but selectively. Named scholarships like Chevening (UK), Fulbright-Nehru (US), DAAD (Germany), and Commonwealth typically intake 50 to 200 Indian students per year across all destinations. University-internal merit aid is more common (often 10 to 50 percent tuition waivers, baked into your admission offer). Treat scholarships as a serious but uncertain funding source. Apply to the top 5 to 10 named awards in your destination, and build your loan and savings plan assuming you will win none of them.

How much money should I carry abroad when I first land?

The clean stack for most Indian students is: USD 300 to USD 500 in destination currency cash for the first 72 hours (taxi, sim card, meals before you set up a local card), a forex card loaded with one to two months of living expenses, an Indian bank international debit card as backup, and instructions to open a local student bank account in the first week. Avoid carrying large amounts of cash. Most countries require declaration of cash above USD 10,000 at customs.

What is the difference between LRS and TCS for education remittances?

LRS (Liberalised Remittance Scheme) is the RBI’s framework that allows a resident Indian to remit up to USD 250,000 per financial year per person for permitted purposes including education. It is the limit on how much you can send out. TCS (Tax Collected at Source) is a separate income tax provision that collects a small percentage (0.5 percent on loan-funded, 5 percent on self-funded education remittances above ₹7 lakh) at the time of remittance. LRS sets the ceiling. TCS is the friction layer applied within that ceiling. Both are set centrally by the RBI and the Income Tax Department respectively.

Is an education loan sanction letter accepted as proof of funds for student visas?

Yes, in every major destination (UK, Canada, Australia, Germany, Ireland, Netherlands, US), an unconditional education loan sanction letter from a recognised Indian lender is accepted as proof of funds. The conditions: the sanction must be unconditional (not “in principle”), it must clearly state the total sanctioned amount, the disbursement schedule must align with your tuition and living needs, and the lender must be on the destination embassy’s list of recognised institutions. Most major Indian banks and the established NBFCs qualify. Always request the loan sanction letter in the format your destination embassy accepts.

Faz · The Honest Journey · 2026