The all-in cost of studying in Australia for Indian students in 2026 runs roughly ₹45 lakh to ₹70 lakh for a two-year Master’s, which makes it the second most expensive destination in this cluster after the USA. Tuition is AUD 30,000 to 45,000 a year, and the student visa itself now requires you to prove AUD 29,710 in living funds. At ₹56 to the Australian dollar, a full-freight Master’s in Sydney or Melbourne crosses ₹65 lakh, while a regional or Adelaide program can stay near ₹48 lakh.

The messages I get about Australia have changed tone over the last two years. It used to be “is Australia cheaper than the US?” Now it is “why did the visa savings requirement jump again?” Australia has steadily raised both the visa fee and the funds you must prove, and tuition at the big-city universities keeps climbing. The cost of studying in Australia for Indian students is no longer the budget alternative it once was. It is a premium destination, and the honest planning number reflects that.

This post walks through what tuition actually costs by level and city, the living-fund figure the visa now demands, the Subclass 500 visa fee, health cover, what you can earn part-time, and the honest two-year rupee total in 2026. If you are still mapping the bigger picture, the full guide on studying in Australia for Indian students covers admissions, the visa and timelines end to end.

Once you have the Australia number, the natural next question is how it stacks up against the other big destination for Indians. The best country to study abroad for Indian students comparison puts them side by side.

Tuition: the biggest line, and it varies by level and city

Tuition is by far the largest cost in Australia, the opposite of Germany. For an international student, a postgraduate degree at a Group of Eight university (the research-intensive top tier, including Melbourne, Sydney, UNSW, Monash) sits at the higher end, while regional and mid-tier universities are meaningfully cheaper for a comparable qualification.

| Program level | Annual tuition (AUD) | Rupees per year (at ₹56 per AUD) |

|---|---|---|

| Bachelor’s (3 years) | AUD 22,000 to 40,000 | ₹12.3 lakh to ₹22.4 lakh |

| Master’s, mid-tier / regional | AUD 28,000 to 36,000 | ₹15.7 lakh to ₹20.2 lakh |

| Master’s, Group of Eight | AUD 38,000 to 50,000 | ₹21.3 lakh to ₹28 lakh |

| MBA | AUD 50,000 to 90,000 | ₹28 lakh to ₹50.4 lakh |

The gap between a Group of Eight Master’s and a strong regional one is the single biggest lever on your total. A regional university also carries a real bonus that has nothing to do with cost, which is a longer post-study work window, covered further down. For most Indian students, a mid-tier or regional Master’s is the honest value pick, not the sandstone brand name.

Faz's ruleIn Australia the visa savings figure is not a suggestion. From 2024 the department has actively refused applications where the funds look thin or borrowed at the last minute. Treat AUD 29,710 as a hard floor, fully documented, well before you apply.

Australia tightened the Genuine Student test and the financial checks specifically because of a surge in under-funded applications. Officers now scrutinise where the money came from and how long it has been there. Funds that appeared in the account a few weeks before applying are the fastest route to a refusal.

The living-fund requirement: AUD 29,710 the visa demands

Australia’s version of proof of funds is a fixed living-cost figure you must show on top of tuition and travel. From May 2024 that figure rose to AUD 29,710 for the primary applicant for a year, and it is the number the Subclass 500 visa is assessed against.

| Funds you must demonstrate | Amount (AUD) | Rupees (at ₹56 per AUD) |

|---|---|---|

| Living costs (primary applicant, one year) | AUD 29,710 | ₹16.6 lakh |

| First-year tuition | As per your eCoE | Varies by program |

| Return travel | AUD 2,000 to 2,500 | ₹1.1 lakh to ₹1.4 lakh |

| Spouse (if accompanying) | AUD 10,394 | ₹5.8 lakh |

The important nuance is that AUD 29,710 is a proof-of-funds benchmark, not necessarily what you will actually spend. In a cheaper city you may live on less. In Sydney you will almost certainly spend more. But the visa will not be granted unless you can show at least this amount as genuine, available funds alongside your first-year tuition. A sanctioned education loan letter is accepted as evidence, which is where most Indian students meet the requirement. The full breakdown of what counts is in the proof of funds for student visa guide.

Living costs, city by city

Where you study inside Australia changes your real spend as much as the university you pick. Sydney and Melbourne are among the most expensive student cities in the world. Adelaide, Brisbane and the regional centres are far kinder to a budget.

| City | Rent (shared, per week) | Total monthly living (AUD) | Rupees per month |

|---|---|---|---|

| Sydney, Melbourne (expensive) | AUD 320 to 450 | AUD 2,500 to 3,500 | ₹1.4 lakh to ₹1.96 lakh |

| Brisbane, Perth, Canberra (mid) | AUD 250 to 350 | AUD 2,000 to 2,700 | ₹1.12 lakh to ₹1.51 lakh |

| Adelaide, regional centres (affordable) | AUD 180 to 280 | AUD 1,500 to 2,200 | ₹84,000 to ₹1.23 lakh |

Over a two-year Master’s, choosing Adelaide over Sydney can save AUD 24,000 to 31,000 in living costs alone, which is ₹13 lakh to ₹17 lakh. Combined with lower regional tuition and the longer post-study work window, the regional route is often ₹18 lakh to ₹22 lakh cheaper end to end than a Group of Eight degree in Sydney, for a qualification the Australian job market treats very similarly.

Faz's ruleThe regional university is Australia's best-kept cost secret. Lower tuition, lower rent, and an extra year of post-study work rights. The only thing you give up is the big-city brand name, which your future employer barely weighs.

Indian students gravitate to Sydney and Melbourne for the skyline and the diaspora. But the regional incentives exist precisely because Australia wants to pull students away from those two cities, so it stacks the deck in your favour with cheaper costs and longer work visas. It is the rare case where the cheaper option is also the strategically smarter one.

Visa fee, health cover and the smaller line items

Beyond tuition and living, a handful of mandatory costs apply before and during the program. The Subclass 500 visa fee in particular has risen sharply and is now one of the more expensive student visa fees in the world.

| Fee | Amount | What it is |

|---|---|---|

| Subclass 500 visa application charge | AUD 2,000 | The student visa fee, raised to this level from 1 July 2025. Non-refundable even if refused. Paid to the Department of Home Affairs. |

| Overseas Student Health Cover (OSHC) | AUD 500 to 800 per year | Mandatory health insurance for the full visa duration, arranged before the visa is granted. |

| Genuine Student statement and documents | Nominal | No separate fee, but the GS requirement drives document preparation and sometimes agent costs. |

| Biometrics and medicals | ₹5,000 to 8,000 | Health examination and biometric collection in India. |

OSHC is mandatory for the entire length of your visa and must be arranged before the visa is granted, so it is a genuine upfront cost, not an optional add-on. Single cover runs AUD 500 to 800 a year through providers like Bupa, Medibank and Allianz. The broader picture on cover is in the health insurance for study abroad guide.

Part-time work and the post-study stay

Australia allows international students to work up to 48 hours per fortnight during term and unlimited hours during official breaks. At typical casual rates of AUD 25 to 32 an hour, that comes to roughly AUD 1,000 to 1,300 a fortnight when working the full cap, which materially offsets living costs in the second year. The rules and realistic earnings are in part-time work while studying abroad.

After graduation, the Temporary Graduate visa (Subclass 485) grants two to three years of full work rights, with regional graduates often getting an extra one to two years on top. This post-study window is the return side of Australia’s high cost. A graduate earning an Australian starting salary of AUD 65,000 to 85,000 for two to three years can repay a large part of the loan before returning or transitioning to skilled migration, which is what keeps the premium price defensible.

A worked rupee total: two-year Master’s in a mid-cost city in 2026

The cleanest way to make it concrete is a specific case. A Master’s in IT or Business at a mid-tier university in Brisbane or Adelaide, AUD 33,000 tuition per year, living at the realistic student level rather than the visa benchmark, modest part-time work from the second semester.

| Line item | AUD | Rupees (at ₹56 per AUD) |

|---|---|---|

| Year 1 tuition | AUD 33,000 | ₹18.5 lakh |

| Year 2 tuition | AUD 33,000 | ₹18.5 lakh |

| Year 1 living + rent | AUD 22,000 | ₹12.3 lakh |

| Year 2 living (offset by part-time work) | AUD 17,000 | ₹9.5 lakh |

| OSHC (2 years) | AUD 1,400 | ₹78,000 |

| Subclass 500 visa fee | AUD 2,000 | ₹1.1 lakh |

| Round-trip flights (2 trips home) | AUD 2,600 | ₹1.5 lakh |

| Initial settlement (bond, furniture, setup) | AUD 2,200 | ₹1.2 lakh |

| Forex spread + remittance | AUD 1,300 | ₹73,000 |

| Two-year all-in total | AUD 114,500 | ₹64.1 lakh |

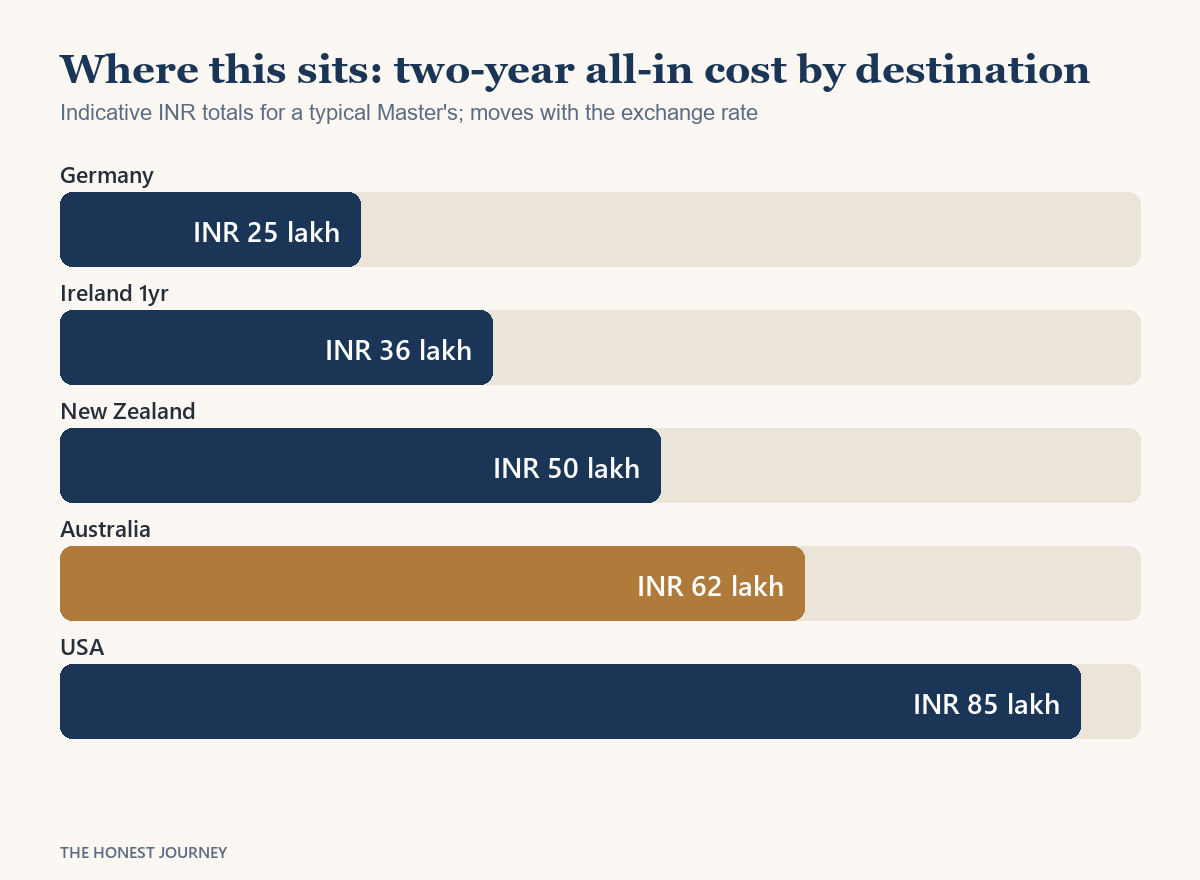

A two-year Master’s in a mid-cost city lands around ₹58 lakh to ₹64 lakh all-in in 2026. Choose Adelaide or a regional university and it drops toward ₹48 lakh to ₹52 lakh. Choose a Group of Eight program in Sydney or Melbourne and it climbs to ₹68 lakh to ₹72 lakh. The number scales with both your university tier and your city, and unlike Germany, tuition is the dominant driver throughout. Forex is small per transfer but adds up across two years, so understand the A2 form and LRS rules for sending money abroad and pick an efficient route. The best forex card for students post covers the options.

Faz's ruleThe honest number for a two-year Master's in Australia in 2026 is ₹55 lakh to ₹65 lakh for most students, not the ₹30 lakh that older forum posts still quote. Australia is now a USA-tier cost, so treat it as one when you plan the loan.

The “Australia is affordable” belief is five years out of date. Rising tuition, a AUD 2,000 visa fee, and a living requirement that keeps climbing have pushed it into premium territory. Plan with the current numbers, because a loan sized on old figures will fall short at exactly the wrong moment.

Funding the gap: loan, savings, or both

At ₹55 lakh to ₹65 lakh, few families fund Australia from savings alone. The standard structure is a sanctioned education loan for Australia studies for the bulk, with family funds covering the visa fee, OSHC, flights and initial settlement. PSU banks sanction up to ₹1.5 crore for reputable Australian universities with collateral at roughly 9.5 to 11 percent, and the sanctioned loan letter doubles as the proof of funds the Subclass 500 visa requires. Unsecured NBFC loans reach ₹75 lakh for select university lists at higher rates. Because Australia’s living requirement is a hard documented figure, a loan that covers first-year tuition plus the AUD 29,710 living benchmark is the cleanest visa evidence. For the full funding picture see the studying abroad from India cost and funding guide and the education loan India complete guide.

The honest closing take

Australia is a premium destination now, and the sooner Indian families internalise that, the better their planning. A two-year Master’s at ₹55 lakh to ₹65 lakh is close to USA territory, and the visa process has become genuinely demanding on both funds and the Genuine Student test. This is not the budget option it was a decade ago.

What Australia still offers in return is a clear and generous post-study pathway. The Subclass 485 visa gives two to four years of full work rights, regional study extends that further, and Australian starting salaries are high enough to repay a large loan within the work window. The country has built its whole international-education model around students who stay, work and often migrate, which is a very different proposition from destinations that expect you to leave on graduation.

The honest decision comes down to two questions. Can you fund ₹55 lakh to ₹65 lakh, and do you intend to use the post-study work rights to earn it back in Australian dollars? If the answer to both is yes, and especially if you choose a regional university, Australia is a defensible premium. If you are simply looking for the cheapest route abroad, Germany or a mid-tier European option will cost a fraction of this.

Once the budget is clear, the visa is the next hurdle. The Subclass 500 fee, funds proof, OSHC and Genuine Student requirements are in the Australia student visa guide.

Cost is only half the question. See is studying in Australia worth it for the salary, payback period and return on this spend.

Ready to fund it? Most Indian students route the loan through the PM Vidyalakshmi portal. That guide covers the step by step application and the 13 banks linked to it.

FAQ

How much does it cost to study in Australia from India in 2026?

A two-year Master’s in Australia typically costs ₹45 lakh to ₹70 lakh all-in for an Indian student, including tuition, living, OSHC, the visa fee, flights and forex. A mid-tier or regional program lands around ₹48 lakh to ₹58 lakh, while a Group of Eight degree in Sydney or Melbourne climbs to ₹68 lakh to ₹72 lakh. Tuition is the dominant cost at AUD 30,000 to 45,000 a year, and the student visa additionally requires you to prove AUD 29,710 in living funds, which is roughly ₹16.6 lakh at ₹56 to the Australian dollar.

How much money do I need to show for an Australian student visa?

For the Subclass 500 student visa in 2026, you must demonstrate living funds of AUD 29,710 for the primary applicant for one year, on top of your first-year tuition as stated on your eCoE and return travel of around AUD 2,000 to 2,500. This is roughly ₹16.6 lakh in living funds alone. A sanctioned Indian education loan letter is accepted as evidence. Australia now scrutinises the source and history of these funds closely under the Genuine Student test, so money that appeared recently or looks borrowed at the last minute risks a refusal.

How much is the Australian student visa fee in 2026?

The Subclass 500 student visa application charge is AUD 2,000 for the primary applicant, having risen to this level from 1 July 2025. That is roughly ₹1.1 lakh at ₹56 to the Australian dollar, and it is one of the most expensive student visa fees in the world. It is non-refundable even if the visa is refused. On top of this you must arrange Overseas Student Health Cover before the visa is granted, at AUD 500 to 800 a year, plus biometric and medical costs in India.

Is Australia cheaper than the USA for Indian students?

Not by much anymore. A two-year Master’s in Australia at ₹55 lakh to ₹65 lakh is close to a US state-university Master’s, which lands around ₹75 lakh to ₹1 crore, so Australia is somewhat cheaper but no longer a budget alternative. Rising tuition, a AUD 2,000 visa fee and a climbing living requirement have pushed Australia into premium territory. The clearer difference is the post-study pathway. Australia offers a more predictable route to work and migration than the US H-1B lottery, which is often the deciding factor rather than cost.

Can Indian students work part-time in Australia?

Yes. International students in Australia can work up to 48 hours per fortnight during term and unlimited hours during official breaks. At casual rates of AUD 25 to 32 an hour, working the full cap earns roughly AUD 1,000 to 1,300 a fortnight, which meaningfully offsets living costs, especially in the second year. After graduation, the Temporary Graduate visa (Subclass 485) grants two to four years of full work rights, with regional graduates typically getting the longest windows.

Which is the cheapest way to study in Australia?

The cheapest route is a mid-tier or regional university in a lower-cost city such as Adelaide, rather than a Group of Eight university in Sydney or Melbourne. Regional study combines lower tuition, cheaper rent and a longer post-study work visa. Choosing Adelaide over Sydney can save ₹13 lakh to ₹17 lakh in living costs alone across a two-year Master’s, and the total end-to-end saving including tuition and the extra work window often reaches ₹18 lakh to ₹22 lakh, for a qualification the Australian job market treats very similarly.

Do I need collateral for an Australia education loan?

Not always. PSU banks sanction secured loans up to ₹1.5 crore for reputable Australian universities with collateral at roughly 9.5 to 11 percent, and the sanctioned letter doubles as the proof of funds the Subclass 500 visa requires. NBFCs offer unsecured loans up to around ₹75 lakh for select university lists at higher rates, without collateral but usually needing a strong co-applicant. Because Australia requires a hard documented living figure of AUD 29,710 plus tuition, a loan sized to cover first-year tuition plus that benchmark is the cleanest visa evidence.

Faz · The Honest Journey · 2026