The Liberalised Remittance Scheme (LRS) lets any resident Indian send up to USD 250,000 per individual per financial year abroad, and the A2 form is the declaration you sign to authorise each outward forex remittance. For education funded by an education loan, TCS is just 0.5 percent on the amount above ₹7 lakh in a financial year, far below the 20 percent that applies to most other LRS spending. The bank files the actual remittance using your A2 declaration, the admission letter, and the university fee demand. The biggest hidden cost is rarely the wire charge. It is the forex spread the bank quietly builds into the exchange rate.

The first time I sent tuition abroad, I assumed the hard part would be the paperwork. It was not. The paperwork took twenty minutes at a bank counter. The part nobody warned me about was the exchange rate. The bank quoted a rate that looked fine until I checked the live USD to INR rate on my phone and realised they had baked in close to a rupee of margin on every dollar. On a USD 30,000 wire, that is roughly ₹30,000 vanishing into a spread I never saw itemised.

The LRS limit for students is the same USD 250,000 every resident gets, and almost no student gets anywhere near it in a year. The real story of sending money abroad for education is not the cap. It is understanding who files the A2 form, how a SWIFT wire differs from a forex card or a demand draft, and where the hidden markups live. This post walks through all of it.

What LRS is and the USD 250,000 limit

The Liberalised Remittance Scheme is the RBI framework that lets a resident individual remit foreign currency abroad without prior RBI approval, up to USD 250,000 per individual per financial year. It covers a defined list of permissible current and capital account transactions, and education is one of the cleanest permitted purposes. The full master direction sits on rbi.org.in, and the plain-language version is in the RBI’s LRS FAQ.

The limit is per individual, not per family. A student, a father, and a mother are three separate residents, so a family can collectively move up to USD 750,000 in a financial year if each remits within their own USD 250,000 ceiling. For education this is almost never a constraint. A full year of US tuition plus living costs rarely crosses USD 80,000, well inside one person’s limit.

The financial year for LRS runs April to March, matching the Indian tax year. The limit resets every 1 April. So tuition wired in March and tuition wired in April fall in two different LRS years, which matters when you are pacing large payments across an academic year that straddles the reset.

Faz's ruleThe USD 250,000 LRS limit is per person per financial year, and it resets on 1 April. Students almost never hit it. The constraint is your funding, not the regulation.

People worry about the LRS cap far more than they should. I have never met a student who exhausted USD 250,000 in a single year on education. The cap exists to stop large-scale capital flight, not to limit a genuine tuition payment. If your annual ask is USD 60,000 or USD 80,000, the limit is irrelevant to you. Spend your energy on the exchange rate instead, because that is where money actually leaks.

The A2 form: who files it and what it declares

The A2 form is the application-cum-declaration you submit for any outward forex remittance under FEMA. It tells the bank the amount, the currency, the beneficiary, and the purpose code for the remittance. For education, the purpose code identifies the wire as tuition or living expenses, which is what lets the bank apply the correct TCS rate and report the transaction correctly to the RBI under the FEMA reporting framework on fema.rbi.org.in.

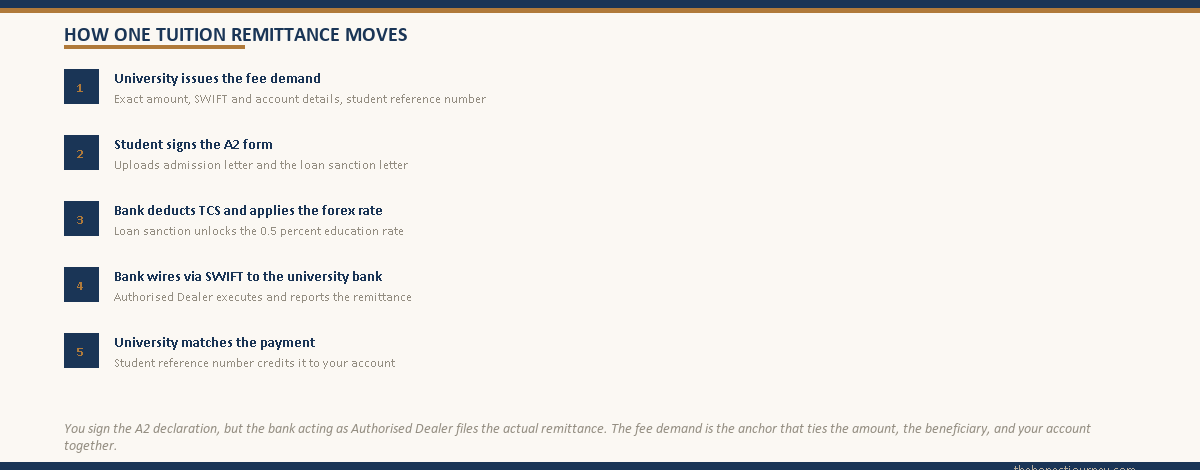

Here is the part that confuses people. You sign the A2 form, but the bank files the remittance. The A2 is your declaration that the money is genuine, within your LRS limit, and for a permitted purpose. The bank, acting as an Authorised Dealer, then executes the wire and handles the regulatory reporting. So the honest answer to who files the A2 form is: you complete and sign it, the bank processes and acts on it. Many banks now offer a fully online A2 submission, where you fill the declaration in net banking and upload the supporting documents, with no branch visit.

The supporting documents the bank wants alongside the A2 are predictable:

- The university admission or offer letter, confirming you are an enrolled student.

- The university fee demand or invoice, stating the exact amount and the beneficiary bank details.

- Your PAN, since TCS is reported against it.

- For loan-funded wires, the education loan sanction letter, so the bank applies the 0.5 percent TCS rate rather than 5 percent.

The fee demand is the document that ties everything together. It states the precise sum the university expects, the SWIFT and IBAN or account details of the university’s bank, and often a student reference number that must travel with the wire so the university can match the payment to your account. Without it, the bank has nothing concrete to remit against. My separate demand letter for education loan post covers what a clean fee demand should contain.

TCS on the education remittance: the 0.5 percent rate

When the bank processes your A2, it also collects Tax Collected at Source under Section 206C(1G) of the Income Tax Act. TCS is not a tax. It is a prepayment adjusted against your final income tax liability, and if you owe nothing, it comes back as a refund through your ITR on incometax.gov.in.

For education remittances funded by an education loan from a notified financial institution, the rate is 0.5 percent on the amount exceeding ₹7 lakh in a financial year. Below ₹7 lakh per FY, there is no TCS at all. For self-funded education remittances (paid from savings, an FD break, or a gift) the rate is 5 percent above ₹7 lakh. Everything else under LRS, the non-education spending, attracts 20 percent above the threshold.

| Remittance type | Up to ₹7 lakh / FY | Above ₹7 lakh / FY |

|---|---|---|

| Education funded by an education loan | Nil | 0.5% |

| Education funded from own savings | Nil | 5% |

| Overseas tour package | 5% | 20% |

| Other LRS spending (investments, gifts) | Nil | 20% |

This is exactly why the loan sanction letter belongs in your A2 file. It is the document that proves the wire is loan-funded, which is what unlocks the 0.5 percent rate instead of 5 percent. On a ₹20 lakh tuition wire that is ₹13 lakh above the threshold, the difference is ₹6,500 at 0.5 percent versus ₹65,000 at 5 percent. The fuller breakdown of how to reclaim that TCS sits in my TCS refund on education loan post.

Faz's ruleCarry the loan sanction letter to every remittance. It is the single document that drops your TCS rate from 5 percent to 0.5 percent on education wires.

I have watched a parent pay 5 percent TCS on a loan-funded wire purely because they did not hand over the sanction letter at the counter, and the bank defaulted to the self-funded rate. The TCS was reclaimable later, but it parked an extra chunk of money with the government for a year for no reason. The sanction letter is not optional paperwork. It is money. Keep a copy in the same folder as the fee demand.

SWIFT wire vs forex card vs demand draft

There are three normal ways to get money to a university abroad, and they serve different jobs. Confusing them is how people overpay.

SWIFT wire transfer. This is a direct bank-to-bank transfer in foreign currency, routed through the SWIFT network. It is the default and usually the only acceptable method for tuition, because the university wants a clean bank credit it can match to your fee demand and student reference. You give the bank the university’s SWIFT code, IBAN or account number, and the exact amount from the fee demand. The money lands in the university’s account, typically in one to four working days.

Forex card. A prepaid card loaded in foreign currency, locked at the exchange rate on the day you load it. This is built for living expenses abroad: rent, groceries, transport, the day-to-day. It is excellent for that, because it freezes the rate and protects you from daily currency swings while you are overseas. It is the wrong tool for tuition. Universities want a bank wire against an invoice, not a card swipe, and card load limits are far smaller than a tuition bill.

Demand draft. A bank-issued instrument in foreign currency that you physically carry or courier to the university. This was common a decade ago and is now mostly obsolete for tuition. A few institutions still accept it, and it has a niche use for one-off payments where a wire is impractical. The downsides are real: it can be lost, it takes time to clear once the university deposits it, and there is no instant confirmation.

| Method | Best for | Speed | University accepts for tuition? |

|---|---|---|---|

| SWIFT wire | Tuition and large fees | 1 to 4 working days | Yes, the standard |

| Forex card | Living expenses abroad | Instant on swipe | Rarely, not designed for it |

| Demand draft | One-off legacy payments | Days to clear after deposit | Sometimes, mostly phased out |

The clean practical split most students settle on: SWIFT wire for tuition straight to the university, a forex card loaded with two or three months of living costs to carry over for the first stretch, and almost never a demand draft. The disbursement timing of all this should line up with your loan release, which my education loan disbursement process post maps out.

Bank charges and the forex spread

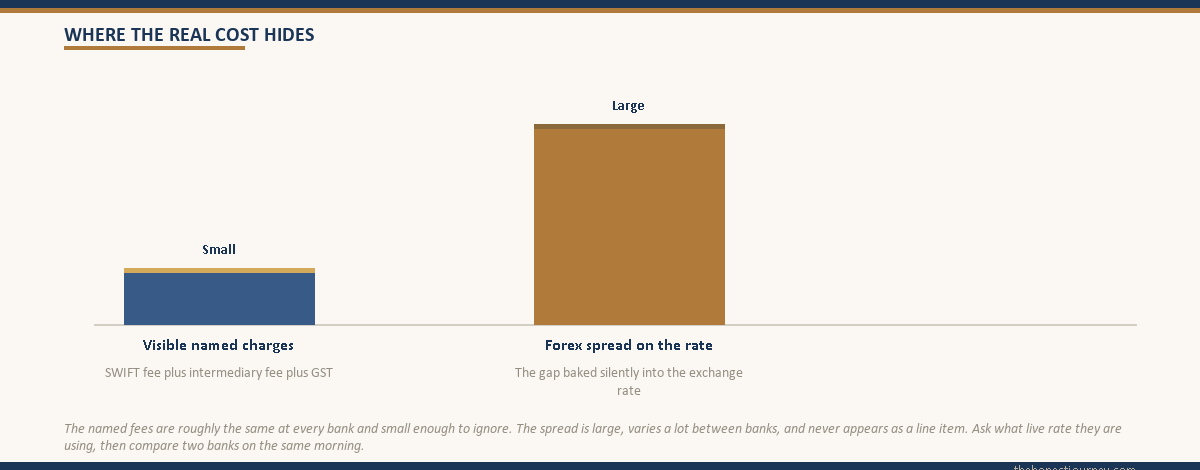

Now the part that actually costs you money. A forex remittance has two layers of cost, and most people only ever see the smaller one.

The visible charges. These are itemised on your remittance receipt and they are modest. A SWIFT remittance fee usually runs around ₹500 to ₹1,500 per wire. There may be a correspondent or intermediary bank charge of USD 10 to USD 40 deducted en route, which can mean the university receives slightly less than you sent unless you choose to bear those charges upfront. GST applies on the rupee-equivalent service portion. None of this is large.

The hidden cost: the forex spread. This is the gap between the live interbank exchange rate and the rate the bank actually gives you. The bank does not charge this as a line item. It bakes it into the rate. If the live USD to INR rate is 86.00 and the bank gives you 86.80, that 0.80 rupee per dollar is the spread, and it is pure margin for the bank. On a USD 40,000 tuition wire, a 0.80 rupee spread is ₹32,000 that never appears on any receipt as a charge. It is simply the difference between what the money was worth and what you paid for it.

This is the single most important thing to understand about sending money abroad. The named charges are small and roughly the same everywhere. The spread is large, varies a lot between banks, and is almost never quoted unless you ask for it directly.

Faz's ruleAlways ask: what live rate are you using, and what rate am I getting? The gap is your real cost. The SWIFT fee is a rounding error next to it.

The move that saved me the most money was simple. Before authorising a wire, I pulled up the live USD to INR rate on my phone, then asked the bank what rate they were giving me. The difference is the spread, and once you say it out loud, some banks will narrow it, especially for a larger tuition wire. I also learned to compare two banks on the same morning. The spread on the same USD 40,000 differed by enough to matter. The fee was identical. The rate was not.

How to keep the cost down

A few honest habits that genuinely reduce what you pay, without any gimmicks:

Compare the rate, not the fee. Banks advertise low or zero SWIFT fees while quietly running a wider spread. The fee is theatre. The rate is the cost. Always evaluate on the rate you actually receive.

Send larger, fewer wires. Every wire carries its own fixed SWIFT and intermediary charges. Two semester payments cost less in fixed fees than four quarterly ones, and a larger wire sometimes earns a slightly better negotiated rate. Balance this against the LRS year reset on 1 April if your payments straddle it.

Match the fee demand to the rupee. Because TCS is held back from the wire amount, ask the bank to ensure the university receives the exact figure on the fee demand. If you wire the gross and TCS comes off the top, the university gets less than the invoice, and you end up topping up. Build the cushion in.

Use the right tool for the job. SWIFT for tuition, forex card for living costs. Loading living money onto a card freezes the rate on a good day and shields you from swings, and it keeps tuition wires clean against the invoice.

SBI and the other public sector banks publish their forex remittance schedules and TCS handling, and it is worth reading the actual schedule on sbi.co.in rather than relying on counter conversation. The numbers on the page are the ones that bind. The biggest US cost picture, where these wires ultimately land, sits in my cost of studying in USA for Indian students post.

The honest verdict

Sending money abroad for education is not complicated once you separate the regulation from the cost. The regulation is generous: USD 250,000 per person per financial year under LRS, an A2 declaration you sign and the bank processes, and a concessional 0.5 percent TCS on loan-funded education above ₹7 lakh that you reclaim through your ITR anyway. None of that should keep you up at night.

The cost is where the attention belongs, and it is not the SWIFT fee. It is the forex spread, the silent margin baked into the exchange rate that no receipt itemises. On a single year of tuition, the spread can quietly cost more than a year of named bank charges combined. The fix is not clever. You ask what live rate is being used, you compare two banks on the same morning, and you treat the rate as the real price.

Get the documents right so the bank applies the cheap TCS rate, use the right instrument for each kind of payment, and watch the rate like it is the cost it actually is. Do that, and a tuition remittance becomes one of the simplest parts of the whole journey abroad.

FAQ

What is the LRS limit for students?

There is no special student limit. Students fall under the standard Liberalised Remittance Scheme cap of USD 250,000 per individual per financial year, the same as any resident Indian. The limit is per person, so a student, mother, and father each have their own USD 250,000 ceiling. In practice no student gets near it, since a full year of tuition and living costs abroad rarely crosses USD 80,000. The cap resets every 1 April. The funding, not the limit, is the real constraint.

What is the A2 form and who files it?

The A2 form is the application-cum-declaration you submit for any outward forex remittance under FEMA. It states the amount, currency, beneficiary, and purpose code of the wire. You complete and sign the A2, declaring the remittance is genuine and within your LRS limit, but the bank, as an Authorised Dealer, actually processes the remittance and reports it to the RBI. Many banks now allow online A2 submission through net banking, with documents uploaded digitally and no branch visit needed.

How much TCS applies on an education remittance?

For education remittances funded by an education loan from a notified financial institution, TCS is 0.5 percent on the amount exceeding ₹7 lakh in a financial year, with nothing below that threshold. Self-funded education remittances attract 5 percent above ₹7 lakh. Most other LRS spending attracts 20 percent. TCS is not a tax but a prepayment, reclaimable as a credit or refund through your ITR. Carry the loan sanction letter so the bank applies the 0.5 percent rate.

Can I use a forex card to pay tuition?

Generally no. A forex card is a prepaid card built for living expenses abroad, like rent, groceries, and transport, and it freezes the exchange rate on the day you load it. Universities want tuition paid by SWIFT bank wire against a fee invoice, not a card swipe, and card load limits are far smaller than a tuition bill. Use a forex card for day-to-day living costs and a SWIFT wire for tuition. That split keeps tuition clean against the invoice and protects living money from rate swings.

What is the difference between a SWIFT wire and a demand draft?

A SWIFT wire is a direct bank-to-bank electronic transfer in foreign currency that lands in the university’s account in one to four working days, with the student reference attached so the university can match it. A demand draft is a physical bank-issued instrument in foreign currency that you carry or courier, which must then be deposited and cleared. Wires are faster, traceable, and the modern standard. Demand drafts are largely obsolete for tuition, slower to clear, and carry loss risk.

What documents does the bank need for a tuition wire?

The bank wants the signed A2 form, the university admission or offer letter, the university fee demand or invoice stating the exact amount and the beneficiary bank details, and your PAN for TCS reporting. For loan-funded remittances, add the education loan sanction letter, which is what lets the bank apply the 0.5 percent TCS rate rather than 5 percent. The fee demand ties it together, since it carries the precise sum, the university’s SWIFT and account details, and a student reference number.

What are the typical bank charges on a forex remittance?

Visible charges are modest: a SWIFT remittance fee of roughly ₹500 to ₹1,500 per wire, a possible correspondent bank charge of USD 10 to USD 40 deducted en route, and GST on the service portion. The far larger cost is the forex spread, the gap between the live interbank rate and the rate the bank gives you, which is baked into the exchange rate and never itemised. On a large tuition wire the spread can dwarf every named fee combined. Always compare the rate, not the fee.

How does the university demand letter tie the remittance together?

The fee demand is the anchor document. It states the exact amount the university expects, the SWIFT code and IBAN or account number of the university’s bank, and usually a student reference number that must travel with the wire. The bank remits against it, so the figures match the invoice, and the university can credit the payment to your account. Without the demand letter the bank has no concrete beneficiary or amount to wire against, and the university cannot match an unlabelled payment to you.

Faz · The Honest Journey · 2026