There is no single best forex card for students: the right pick depends on your destination and how you spend. A student in Germany paying rent by transfer wants the lowest reload markup, often a fintech card. A student in the US living on card swipes wants the lowest ATM and POS fees, where bank cards like HDFC ISIC or Axis Multi-Currency often beat fintech by month three on total cost.

Heading out soon? See the pre-departure checklist and how to open a bank account abroad.

Every bank that issues a forex card calls theirs the best forex card for students. The branch staff will hand you a glossy leaflet, the fintech app will flash a zero-fee banner, and a YouTube reviewer will rank five of them with stars and a verdict. None of that tells you what you actually need to know, which is what each card quietly charges you in the four or five places where the money leaks out.

This post does not crown a winner. It walks the six axes that decide whether a card costs you ₹5,000 or ₹25,000 over a year abroad, then puts the cash vs forex card vs international account choice in plain terms so you can pick the one that fits your country and spending pattern.

The honest answer up front: there is no single best forex card. The best card for a student in Germany who pays rent by transfer is not the best card for a student in the US who lives on card swipes, and a fintech card that looks cheapest on issuance can lose to a bank card on ATM fees by month three.

For the full guide, read Studying Abroad From India: Cost and Funding Guide.

What actually matters in a student forex card

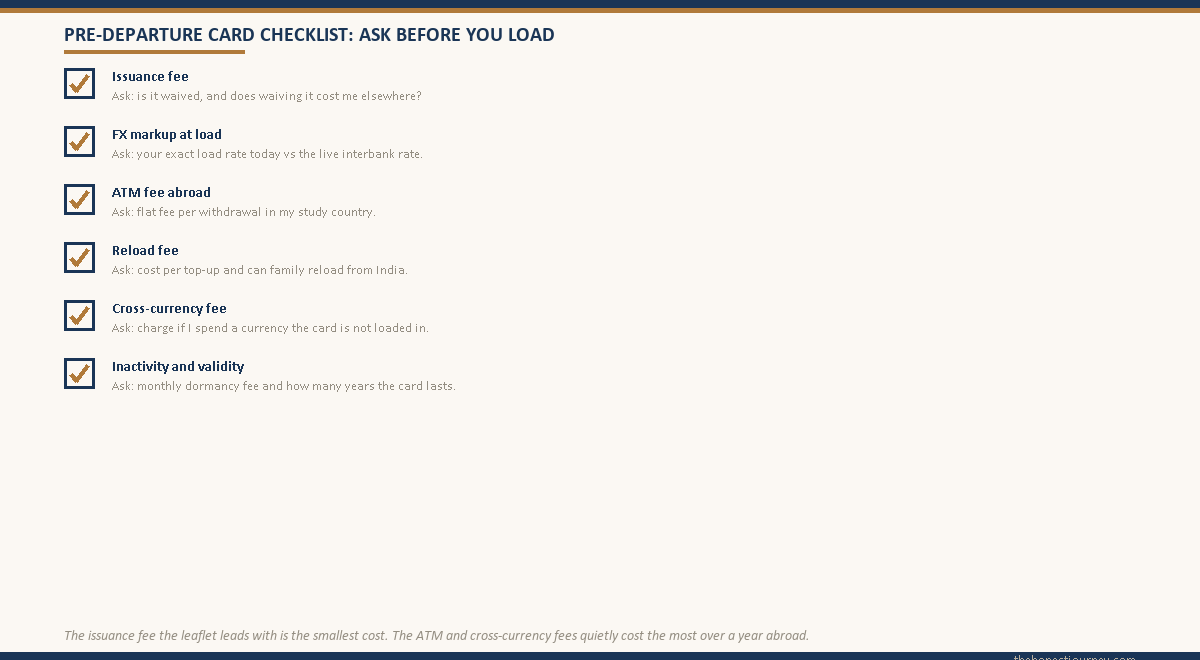

A forex card is a prepaid card loaded with foreign currency at the rate on the day you load it. You spend it abroad like a debit card. The marketing compares the wrong things. Here are the six axes that actually move your cost, and the rough range each one sits in across major Indian bank and fintech cards in 2026.

| Cost axis | What it is | Typical range | How often it bites |

|---|---|---|---|

| Issuance fee | One-time charge to get the card | ₹0 to 500 | Once |

| FX markup | Spread over interbank rate when you load or spend cross-currency | 0% to 3.5% | Every load and cross-currency spend |

| ATM withdrawal charge | Flat fee per cash withdrawal abroad | ₹100 to 250 (or USD 2 to 3) | Every withdrawal |

| Reload fee | Charge to top up after first load | ₹0 to 100 per reload | Each reload |

| Cross-currency / out-of-wallet fee | Extra spread if you spend a currency the card is not loaded in | 2% to 3.5% | Every off-currency spend |

| Inactivity / validity | Monthly dormancy fee and card expiry window | ₹0 to 150/month, 3 to 5 year validity | If unused |

The two that quietly cost the most are the ATM withdrawal charge and the cross-currency fee, not the issuance fee that the leaflet leads with. A student who withdraws cash twice a month at ₹200 a pull spends ₹4,800 a year on ATM fees alone. A student whose card is loaded in USD but who studies in Germany and pays in euros eats a 3% cross-currency spread on every single swipe. Neither shows up in the headline comparison.

The lock-in rate matters in a different way. When you load a forex card, the rate is locked at that moment. If the rupee weakens after you load, you are protected, because your money is already in dollars or euros. If the rupee strengthens, you lose the upside. For a student, the protection usually outweighs the lost upside, because you are funding a fixed cost (tuition and living) and certainty is worth more than a gamble on currency movement. This is the one genuine advantage a forex card has over an international debit card that converts at the spot rate every time you spend.

Faz's ruleCompare cards on ATM and cross-currency fees, not on the issuance fee they advertise.

The ₹0 issuance banner is the cheapest part of any card. The money leaks out at the ATM and on off-currency swipes. Add up your real withdrawal pattern for one month abroad and you will see which card is actually cheapest for you.

Comparing the major cards on facts, not stars

Rather than rank cards, here is how the main categories of card differ on the axes that matter. Exact numbers shift with each card’s terms and you must check the live schedule on the issuer’s own page before you load, because banks revise fees often. Treat this as the shape of the market, not a price list.

| Card type | FX markup | ATM fee abroad | Multi-currency | Best fit |

|---|---|---|---|---|

| Public sector bank forex card | Built into load rate, modest | Flat per withdrawal | Single or multi-wallet | Students who want branch backup at home |

| Private bank forex card | Built into load rate | Flat per withdrawal | Usually multi-currency | Students spending across several countries |

| Fintech / neobank forex card | Often near-zero on load, watch reload | Low or capped free withdrawals | Multi-currency app-managed | App-comfortable students who reload often |

| International debit card (Indian savings account) | Spot rate plus 3.5% cross-currency | High flat fee per withdrawal | No, converts each time | Backup only, not primary spend |

The pattern is consistent. Bank forex cards bury the markup in the rate at which they load your currency, so the card looks fee-free but you paid the spread at load. Fintech cards advertise near-zero markup on the first load but can recover it on reload fees or a slightly worse load rate, so you have to read past the banner. The international debit card on your existing Indian savings account is the most expensive way to spend abroad day to day, because it converts at the spot rate plus a cross-currency fee on every transaction and charges a steep flat ATM fee. Keep it for emergencies, not for groceries.

One thing no card category solves is multi-currency travel within Europe or a connecting trip. If your card is loaded in euros and you spend a weekend in the UK, you pay the cross-currency fee on pounds. A multi-currency card lets you hold euros and pounds in separate wallets and spend each from the matching wallet, avoiding that fee. If your study plan involves more than one currency, multi-currency is the single feature worth paying for.

Faz's ruleA fee-free load rate is not free. The spread is baked into the rate the bank gives you that day.

Ask the bank for the exact rate they will load at and compare it to the live interbank rate on that morning. The gap is your real markup. A card with a ₹0 markup label can still load you 2% above interbank, which is the same thing wearing a different name.

Cash vs forex card vs international account

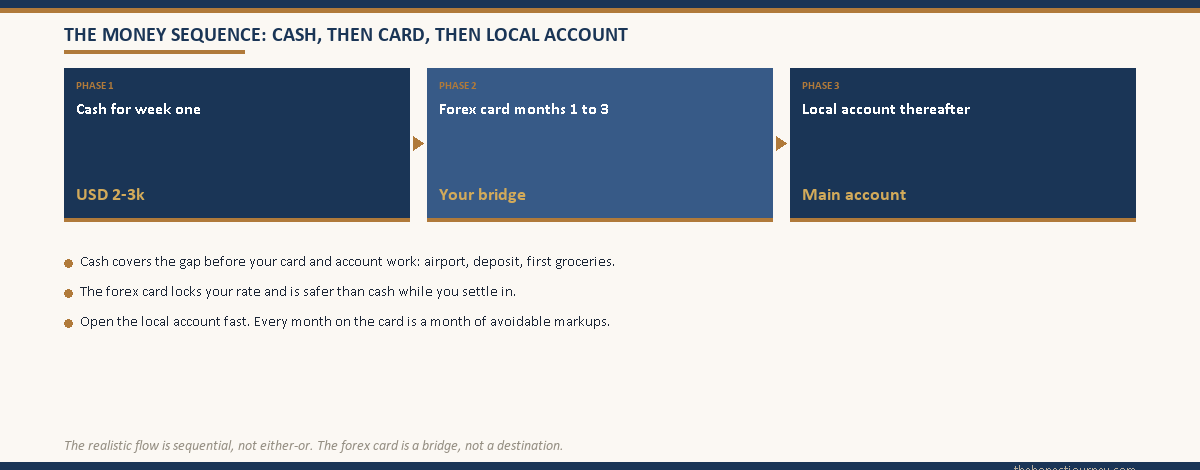

Most families overthink this and end up carrying too much cash. The honest split for a student is small cash, a forex card for the first few months, and a local bank account opened once you land. Here is how the three compare on what actually matters when you arrive.

Cash. You need some, but less than you think. Roughly USD 2,000 to 3,000 covers the first week or two: airport transfer, a deposit, groceries before your local account opens. Carry it split between two people if you travel with family. Remember the customs rule. India lets you carry foreign currency abroad within your declared limit, and most destination countries require a written declaration above the equivalent of USD 10,000. Check the destination customs page and the Indian rules on the CBIC site before you fly. Cash is for the gap before your card and account are working, not your main spending tool.

Forex card. This is your bridge. It works from day one, locks your rate, and is safer than cash because it can be blocked and reissued if lost. Load enough for the first two to three months. It is the right tool while you are still setting up a local account, which can take a few weeks. The catch is that it earns nothing, leftover balance is hard to use after you leave, and reload from abroad depends on your bank’s process.

International account. Some banks (and the GIC route for Canada) effectively give you a local account from before you land. A genuine local account opened after arrival is the cheapest long-term option: local transfers are free, rent and utilities are easy, and there is no FX markup on local spending because the money is already in local currency. The Canada GIC is a specific version of this, where you park a fixed sum that becomes your living-expense account and doubles as proof of funds. See the GIC for Canada post for how that works alongside an education loan.

The realistic flow is sequential, not either-or. Small cash for week one. Forex card for months one to three while you settle. Local account as your main account once it is open, with the forex card kept topped up modestly as a backup. For more on the carry-amount math and the customs limits, see how much money to carry abroad as a student.

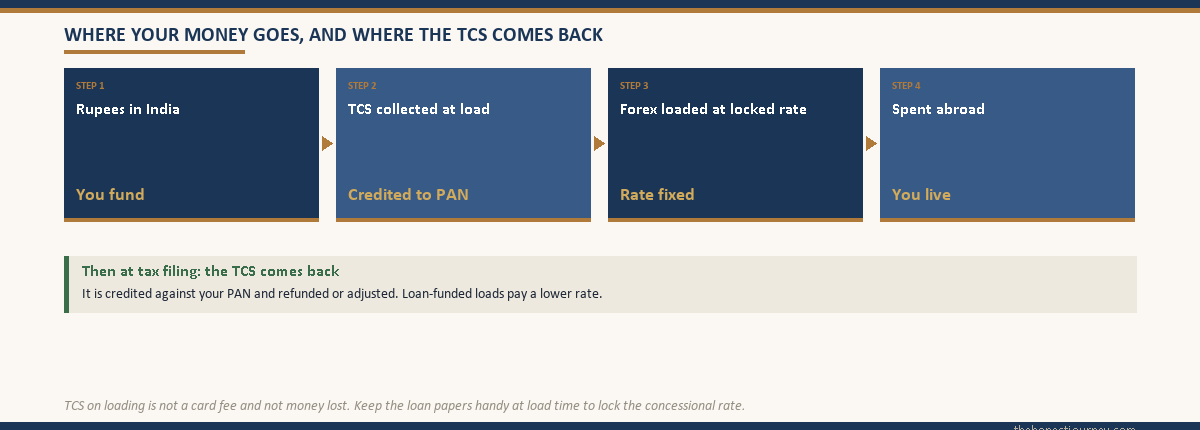

The TCS that applies when you load a forex card

This is the part that surprises families, because it is not a card fee at all. It is a tax collected at source on the money you load. Under the Liberalised Remittance Scheme administered by the RBI, loading a forex card and remitting money abroad both count toward your annual LRS limit and both attract Tax Collected at Source (TCS) above a threshold.

The mechanics, in plain terms, as they stand for education-related remittance. There is an annual threshold per individual, and remittances up to that threshold attract no TCS. Above it, a rate applies. The key relief for students is that money remitted for education funded by an education loan attracts a much lower TCS rate than self-funded remittance, which is the government’s way of not penalising borrowers. Self-funded education remittance sits at a higher rate above the threshold.

What this means in practice for loading a forex card:

| Source of money loaded | Up to the annual threshold | Above the threshold |

|---|---|---|

| Education funded by an education loan | No TCS | Lower concessional rate |

| Self-funded education remittance | No TCS | Higher rate |

Two things make this less painful than it first sounds. First, TCS is not a tax you lose. It is collected and credited against your (or your co-applicant’s) PAN, and you can claim it back as a refund or adjust it against tax payable when you file your return. Verify the current rate and threshold on the Income Tax Department site and the LRS rules on the RBI site before you load a large amount, because both the rate and the threshold have been revised more than once and the live figure is what binds. Second, if your loading is loan-funded, keep the loan disbursement paperwork ready, because that is what gets you the lower rate at the time of loading.

The practical takeaway is to load thoughtfully rather than in many small top-ups, keep your education-loan link visible to the bank so you get the concessional treatment, and remember that the TCS shows up on your card-loading receipt, not on the card’s fee schedule. It is a tax line, not a product charge. If your remittance is loan-funded, the lower rate and the eventual refund mean the real cost is far smaller than the headline number on the loading slip. The relationship between TCS and a loan-funded study budget is covered further in the TCS on education loan post.

Faz's ruleTCS on loading is not a card fee and it is not money lost. It is credited to your PAN and refundable at filing.

Families panic when they see the TCS line on the loading receipt and assume the card is expensive. It is not a card charge at all. If your remittance is loan-funded you pay a lower rate, and either way you reclaim it when you file. Keep the loan papers handy at load time to lock the concessional rate.

How to actually choose your card

Skip the rankings. Do this instead. Estimate your real spending pattern for one month abroad: how many ATM withdrawals, how much card spend, in which currency. Then ask each card you are considering three questions in writing. What is your exact load rate today against the interbank rate, which is your true markup. What is the flat ATM fee per withdrawal in my study country. Is the card multi-currency, and is there a cross-currency fee if I spend a currency it is not loaded in.

Run your one-month spending estimate against those three numbers for two or three cards. The cheapest card for you falls out of that arithmetic, and it will often differ from whatever a review ranked first, because the review did not know you withdraw cash twice a month or that you are headed to a euro country on a dollar-loaded card. Match the currency you load to the currency you will spend, get a multi-currency card if your plan crosses borders, and keep your existing Indian debit card only as an emergency backup.

One more practical point. Open your local bank account as soon as you can after landing, because every month you run primary spending on the forex card is a month of small markups and ATM fees you could avoid. The forex card is a bridge, not a destination. The student who treats it as a permanent solution pays the most over a full year. Funding the whole journey sensibly, of which the card is one small piece, is covered in the broader proof of funds for a student visa picture.

The honest closing take

There is no best forex card, only the card whose fee structure best fits your country, your spending pattern, and how long you will lean on it before a local account takes over. The marketing competes on the issuance fee because it is the one cost that is genuinely small. The real money moves at the ATM, on cross-currency spends, and in the load-rate spread that hides behind a zero-markup banner.

Do the boring thing. Write down your monthly withdrawal and spending pattern, get the exact load rate and ATM fee in writing from two or three issuers, and pick on arithmetic. Load loan-funded money to get the lower TCS rate, keep the loan papers ready at load time, and remember the TCS comes back to you at filing so it is not the cost it appears to be. Carry a little cash, lean on the card for the first couple of months, and move to a local account the moment it opens. That sequence costs less than any single card a reviewer could rank for you.

FAQ

Which is the best forex card for students?

There is no single best forex card, because the cheapest card depends on your country and spending pattern. A card that is cheapest on issuance can lose to another on ATM and cross-currency fees by the third month. The right way to choose is to estimate your monthly withdrawals and card spend, get the exact load rate and ATM fee in writing from two or three issuers, and pick the lowest total cost for your specific use. Match the currency you load to the currency you will actually spend.

Is a forex card or an international debit card better?

For day-to-day spending abroad, a forex card is almost always cheaper than an international debit card on your Indian savings account. The debit card converts at the spot rate plus a cross-currency fee (often around 3.5%) on every transaction and charges a high flat ATM fee. A forex card locks your rate at load and usually has lower ATM fees. Keep the international debit card as an emergency backup only, not as your primary way to spend.

Is there TCS on a forex card?

Yes. Loading a forex card counts toward your annual Liberalised Remittance Scheme limit and attracts Tax Collected at Source above a threshold. Education remittance funded by an education loan attracts a lower concessional rate than self-funded remittance. TCS is not lost money: it is credited against your PAN and is refundable or adjustable when you file your tax return. Verify the current rate and threshold on the Income Tax Department and RBI sites before loading a large amount.

What charges should I check on a forex card?

Check six things, not just the issuance fee. The issuance fee, the FX markup or load-rate spread, the flat ATM withdrawal charge abroad, the reload fee, the cross-currency fee for spending a currency the card is not loaded in, and the inactivity fee plus validity period. The ATM charge and the cross-currency fee usually cost the most over a year, while the issuance fee that marketing leads with is the smallest. Ask for the exact load rate against the live interbank rate to find the true markup.

Can I reload a forex card from abroad?

Most forex cards can be reloaded from abroad, but the process depends on your bank. Some allow online reload through net banking by a family member in India, others require a branch request, and a reload fee may apply each time. Confirm the reload method and fee before you leave India, and set up the net-banking access your family will need. Frequent small reloads can add up in fees, so plan your loads in fewer, larger amounts where the TCS treatment allows.

What happens to leftover forex card balance?

Leftover balance stays on the card until its validity expires, typically three to five years. You can encash the remaining foreign currency back to rupees through your issuing bank, usually at the prevailing buy rate, which means you pay a spread on the way out too. You can also keep the balance for a future trip if the card is still valid. To avoid the encashment spread, load conservatively and lean on a local account for spending once it is open, keeping the card balance modest.

How much cash should I carry alongside a forex card?

Roughly USD 2,000 to 3,000 in cash is enough for most students, covering the first week or two before your forex card and local account are fully working: airport transfer, an initial deposit, and groceries. Carrying much more is risky and unnecessary. Remember that most destination countries require a written declaration for cash above the equivalent of USD 10,000, and Indian rules apply too. Check the destination customs page and the CBIC site before you fly, and split cash between travellers where possible.

Does loading a forex card count toward the LRS limit?

Yes. Loading a forex card is a remittance under the Liberalised Remittance Scheme, so it counts toward your annual LRS limit per individual, the same as a wire transfer abroad. Both the card load and any separate transfers add up against that limit and against the TCS threshold. Keep a running total of everything you remit in a financial year, including card loads, so you do not unexpectedly cross the threshold and trigger a higher TCS rate. The live LRS limit is on the RBI site.

Faz · The Honest Journey · 2026