A demand letter for an education loan is the document the university issues to the bank specifying exactly how much money to release, where to send it, and by which date, and the bank cannot disburse a single rupee of tuition without one. It must carry the student’s full name and ID, the semester or year being paid for, the itemised fee breakup, the due date, and the university’s bank details including SWIFT BIC and IBAN for European institutions. Vague invoices that miss any of these get rejected at the forex desk, which is the most common reason first tranches slip past the registration deadline.

The first time I helped a friend chase a tranche for her Trinity College Dublin master’s, the bank kicked the file back three times in a single week. The university had sent her a “fee statement” that listed the amount and the due date and nothing else. No SWIFT, no IBAN, no purpose code. The forex desk at her Bank of Baroda branch flagged it as an invoice rather than a demand letter, and the file did not move until the bursar’s office reissued the document on Trinity letterhead with the full banking block.

That distinction, between an invoice and a proper demand letter for education loan disbursement, is the difference between a tranche that lands on time and one that costs you a late fee or a deregistration. This post walks through what banks actually want to see, how to request the right document from your university, and what to do when the university is reluctant to issue one.

The other paperwork that sits in the loan file: the education loan interest certificate post, the gap certificate for education loan post, and the sponsorship affidavit for student visa post.

What a demand letter is, and why it is not the same as an invoice

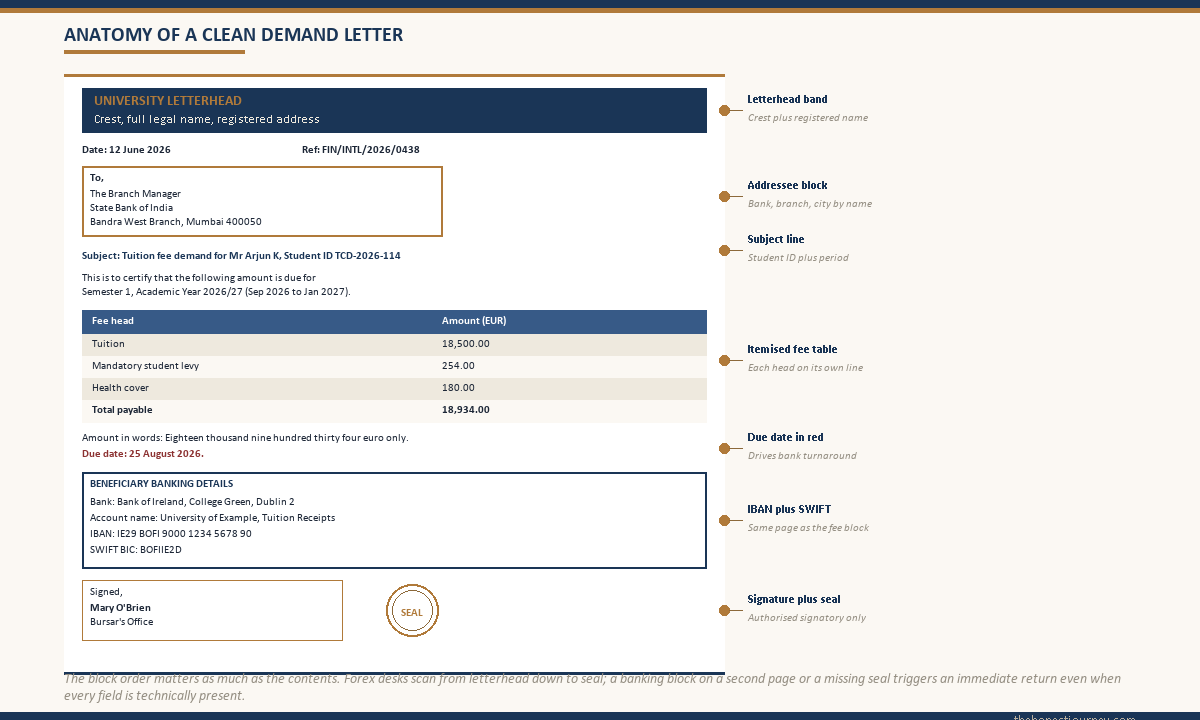

A demand letter is a formal communication from the educational institution to the lender, addressed to the bank by name and branch, stating that a specific amount is due from a specific student for a specific period, and instructing the bank to remit that amount to the university’s designated account by the stated deadline. It is on university letterhead, signed by the registrar, the bursar, or the international student office, and stamped with the institutional seal.

An invoice or fee receipt, by contrast, is a billing document. It tells the student what they owe. It is not addressed to the bank, it rarely carries the university’s bank details, and the signature is usually a finance clerk rather than a designated signing authority. Banks will not act on an invoice alone for the tuition portion of an education loan, because the IBA Model Education Loan Scheme requires direct payment to the institution against a request the institution itself has authorised.

The Indian Banks Association sets this expectation in the model scheme that PSU banks follow, and the RBI reinforces it through the documentation standards expected for foreign currency outflow under the Liberalised Remittance Scheme framework. The bank’s forex desk needs a document that proves the foreign currency is being remitted for a legitimate, university-authorised purpose. An invoice does not clear that bar. A demand letter does.

What the demand letter must contain

Across every PSU bank product I have looked at, including SBI Global Ed-Vantage and Bank of Baroda Vidya, the demand letter has to carry a consistent set of fields. Missing any one of them is enough to send the file back.

| Field | What it must show | Why the bank insists |

|---|---|---|

| Addressee | The lending bank by full name, branch, and city | Confirms the letter is issued specifically for this remittance, not a generic receipt |

| Student identification | Full name as on passport, student ID number, course name, intake year | Lets the forex desk and the university’s finance office match the payment to the right student record |

| Period covered | Semester or academic year and the exact dates it covers | Confirms the tranche is for an active enrolment period, not a back-dated or forward-dated claim |

| Fee breakup | Tuition, mandatory institutional fees, health cover where bundled, each on a separate line | Matches against the sanctioned fee structure so the bank can confirm there is no scope creep |

| Total amount due | Numerical figure and amount in words, currency clearly stated | Forex conversion is booked against this exact figure; any ambiguity stalls the deal |

| Due date | The deadline by which the university expects the payment | Drives the bank’s internal turnaround target and any deferred-undertaking letter the student may need |

| Beneficiary bank details | University’s bank name, account number, SWIFT BIC, IBAN where applicable, intermediary bank if any | The SWIFT MT103 instruction cannot be raised without these fields populated correctly |

| Signature and seal | Designated signing authority’s signature, name in print, designation, official institutional seal | Proves authenticity; unsigned or photocopied documents are rejected |

The fee breakup line is where many universities cut corners. They lump everything under a single “tuition and fees” head and quote a round number. Banks prefer to see the breakup because the sanction letter modelled specific heads, and the credit officer needs to confirm the demanded amount sits within the sanctioned envelope. If your demand letter only shows a single line, ask the bursar to reissue it with the breakup.

Faz's ruleGet the demand letter on university letterhead, addressed to your bank by name, with the SWIFT and IBAN block on the same page as the fee breakup. Anything less will come back.

The fastest fixes are the ones you push for upfront. When I email the bursar I attach a one-line template of what the bank needs and ask them to mirror it on letterhead. International student offices in Europe and the UK do this routinely for Indian and Nigerian students. They are not surprised by the request. The Indian students who struggle are the ones who accept the first PDF the university sends and then spend two weeks arguing with their branch manager about whether a fee statement counts.

Who issues the demand letter, and the title varies by country

Inside Indian universities, the demand letter typically comes from the accounts section or the registrar’s office. For IITs, NITs, and central universities, the finance officer signs it. For private deemed universities, the registrar or the dean of student affairs usually does. The seal is the institutional seal, not a departmental one.

Overseas, the office that issues the document depends on the country and the university size.

UK and Irish universities issue it through the international student office or the fees and finance office. At Trinity College Dublin and University College Dublin, the bursar’s office sends it on request. UK Russell Group universities, including Manchester, Edinburgh, and King’s College London, have dedicated international finance teams that turn this around within 3 to 7 working days.

US universities use the term “I-20 fee invoice with payment instructions” interchangeably with demand letter for Indian banks. The Office of International Students and Scholars (OISS) or the Bursar’s Office issues it. Some private universities push international students to a third-party platform like Flywire or Convera for collection; in those cases, the demand letter still comes from the university but names the third-party portal as the beneficiary for the SWIFT.

German universities use the term “Zahlungsaufforderung” or simply “fee notice.” The Studierendensekretariat (student registration office) or the international office issues it. Most German universities now have a standard PDF template available through the student portal, which they will customise on request to add the SWIFT and IBAN block in English.

Canadian universities issue it through the Student Accounts office. Australian universities use the “Statement of Account” terminology, which their Student Finance office issues with the COE (Confirmation of Enrolment) cross-referenced. New Zealand universities go through the International Student Office and reference the offer of place plus the fees schedule.

The SWIFT BIC and IBAN block is non-negotiable for European universities

For any university in the eurozone, the demand letter must carry the IBAN (International Bank Account Number) for the university’s account, not just the local domestic account number. The IBAN is a country-specific format starting with the two-letter country code followed by a check pair and the basic bank account number. For example, an Irish IBAN starts with IE and runs 22 characters, a German IBAN starts with DE and runs 22 characters, a French IBAN starts with FR and runs 27 characters.

The SWIFT BIC (Business Identifier Code) is the 8 or 11-character code identifying the beneficiary bank within the SWIFT network. Both fields are needed. Indian banks will not raise the MT103 with only one of the two. SBI and Bank of Baroda forex desks specifically flag any European university demand letter that has the SWIFT but not the IBAN, or vice versa.

For non-eurozone European countries (UK, Switzerland, Norway, Sweden, Denmark), the SWIFT plus IBAN combination still applies because these countries also use IBAN within the wider European banking standard. UK IBANs run 22 characters starting with GB, Swiss IBANs start with CH.

For US universities, the SWIFT plus the routing number (ABA) plus the account number is the standard, because the US does not use IBAN. The demand letter must clearly label which number is the routing number and which is the account number to avoid the SWIFT being raised with the fields swapped.

If the university’s standard demand letter does not carry the SWIFT or IBAN block, do not try to attach a separate banking instructions sheet downloaded from the university website. Banks reject mismatched documents. Email the bursar and ask for the demand letter to be reissued with the banking block embedded on the same page as the fee details and signed off in the same signature.

Semester-wise versus full-course demand letters

Most universities issue the demand letter per semester or per academic year. This matches how Indian banks disburse, in tranches, and it matches the documentation flow that the IBA model scheme expects.

A few universities, particularly some private Indian institutions and a handful of UK private colleges, offer to issue a single demand letter for the full course duration with a payment schedule attached. This sounds convenient and it almost always backfires. Banks treat the full-course demand letter as evidence of the total fee structure, not as a release instruction for the full amount. They will still require a fresh tranche request and a confirmation that the current period is in progress before each disbursement.

Worse, if your fees rise during the course (as they usually do for overseas master’s programs that have semester-wise tuition revisions), the full-course demand letter becomes outdated, and the bank will ask for a fresh per-semester letter anyway. The cleanest practice is one demand letter per tranche, generated within 30 to 45 days of the due date.

When the university issues only an invoice and refuses a demand letter

This happens more often than students expect, particularly with smaller private overseas universities and with some Indian state universities. The finance office insists they only issue invoices, and the registrar’s office says invoicing is the finance office’s job.

The fix is usually a polite but specific email that explains what the bank needs and why. I keep a short template that has worked across multiple universities:

“Dear (Bursar / International Office), I am an admitted student for (program, intake). My education loan is being financed by (bank name) in India, and the bank requires a formal demand letter on university letterhead before they can release the tuition payment via SWIFT. The letter must be addressed to the bank, list my student ID and the fee breakup for (semester or year), state the due date, carry the university’s SWIFT BIC and IBAN, and be signed by an authorised signatory with the institutional seal. The standard invoice you have sent does not include these elements. Could you please reissue the document with these additions, or confirm which office can do so. The bank’s processing window is 7 to 10 working days, and my registration deadline is (date), so any guidance you can provide on the typical turnaround would help.”

In my experience, that email gets the right document within 5 to 7 working days from most overseas universities. Indian state universities can take longer because the registrar’s office is the bottleneck and the request often needs to physically move between sections.

If the university still refuses to issue anything beyond an invoice, the next step is to speak to the branch manager about an exceptional approval. Some banks will accept an invoice plus a separately downloaded official banking instructions sheet from the university’s website, as long as the two documents can be tied to each other through the student ID. This is a discretionary path and you should not bank on it.

Faz's ruleRequest the demand letter 30 to 45 days before the university fee deadline, not 7 days before. The buffer is what keeps the registration confirmed.

Universities run on their own administrative calendar, especially in summer when intake offices are processing thousands of admits at once. A request that sits in a bursar’s inbox for two weeks is normal. Building a 30-day buffer means the document is in your hands by the time your bank’s forex desk is ready to act, and the SWIFT clears with room to spare. The students who get caught are the ones who request the demand letter the week of the fee deadline.

Timing the demand letter within the disbursement window

The full sequence from sanction to tuition landing in the university’s account, with the demand letter as the pivot, looks like this.

You receive your final unconditional admission letter, typically 6 to 12 weeks before semester start. You complete the sanction letter signing and loan documentation with the bank, which takes 2 to 4 weeks after the admission letter is on file. The bank opens your loan account and you are now in the window where you can request the first tranche.

30 to 45 days before the university’s fee deadline, you email the bursar with the demand letter request. The university issues the demand letter within 5 to 14 working days. You submit the demand letter, the final admission letter, and your written request to the branch. The branch verifies the document, raises the debit voucher, and the forex desk converts INR to the destination currency at the day’s card rate. The SWIFT MT103 is sent, the correspondent bank credits the university within 1 to 2 working days of the SWIFT, and the university’s finance office matches the payment to your student record using the reference field.

The compressed version of this flow is in the education loan disbursement process post. The parallel documents that travel alongside the demand letter at the first tranche, particularly the bonafide certificate and the admission letter set, are covered in the bonafide certificate for education loan guide, and the wider documents list is in the documents required for education loan reference.

When the demand letter is also used for visa proof of funds

For some countries, the demand letter doubles as the proof that you have arranged finances for the tuition portion of the visa application. UK, Ireland, and Canadian visa officers do accept a sanctioned education loan plus the corresponding demand letter (and the bank’s disbursement confirmation once the SWIFT clears) as part of the proof of funds package.

The visa officer is looking for evidence that the tuition has been paid or is contractually committed to be paid. A demand letter from the university plus a bank confirmation of disbursement does that cleanly. The mechanics of the wider proof of funds picture, including the living expenses and blocked account or GIC components, are in the proof of funds for student visa post.

The honest closing take

The demand letter is one of those small documents that determines whether the rest of the system works. Sanctioned loan, signed agreement, ready bank, eager student, none of it moves until a piece of paper from the university says “release this much, to this account, by this date.” When the paper is clean, the tranche clears in days. When the paper is sloppy or vague, the file bounces between your branch manager, the forex desk, the bursar’s office, and your inbox for weeks.

The students who get this right do two things. They request the demand letter early, well before the fee deadline. And they specify, when they request it, exactly what the bank needs to see on the document. Universities have issued these for thousands of Indian students. They will issue one for you cleanly if you ask cleanly.

The ones who struggle are the ones who treat the first PDF the university sends as the final word, or who request the document a week before the deadline and find out only then that the SWIFT block is missing. The university will not rush, the bank cannot raise a SWIFT without the right fields, and the registration office will not hold the seat indefinitely. Build the buffer, request the right document, and the rest of the disbursement flow becomes routine.

FAQ

What is a demand letter for an education loan?

A demand letter is a formal document the educational institution issues to the lending bank, on university letterhead, specifying the exact tuition amount due for a stated semester or academic year, the due date, the university’s bank account details including SWIFT BIC and IBAN for European universities, and signed by the registrar, bursar, or international student office with the institutional seal. The bank uses it to authorise direct disbursement of the tuition tranche to the university. Without a properly formatted demand letter, no PSU bank in India can disburse the tuition portion of the education loan.

What is the difference between a demand letter and a fee invoice?

A fee invoice is a billing document addressed to the student, listing what they owe, usually issued by the finance clerk’s office. A demand letter is addressed to the lending bank by name, instructs the bank to remit a specified amount to the university’s account, carries the full beneficiary banking block, and is signed by an authorised signatory with the seal. Banks following the IBA model scheme cannot disburse tuition against an invoice alone because invoices do not authorise a third-party remittance instruction. The demand letter is what unlocks the SWIFT transfer.

Who issues the demand letter at overseas universities?

It varies by country. UK and Irish universities go through the international student office or the bursar’s office. US universities issue it through the Bursar’s Office or the Office of International Students and Scholars (OISS), sometimes routed via Flywire or Convera as the collection portal. German universities use the Studierendensekretariat or the international office, where it is called the Zahlungsaufforderung. Canadian universities use the Student Accounts office. Australian universities issue it via Student Finance, often labelled as a Statement of Account. The signatory is always a designated officer with the institutional seal.

When should I request the demand letter from my university?

Request it 30 to 45 days before the university’s fee deadline. The university typically takes 5 to 14 working days to issue the document, and your bank then needs another 7 to 14 working days for the first tranche (3 to 7 for subsequent tranches), with overseas SWIFT transfers adding 1 to 2 working days for the correspondent bank to credit the university. Building a 30-day buffer means the tranche clears with room to spare, the registration is confirmed without late fees, and you are not chasing your branch manager and the bursar simultaneously in the final week.

Why is the SWIFT BIC and IBAN block mandatory for European universities?

Indian banks raise overseas tuition remittances through a SWIFT MT103 payment instruction, which routes through a correspondent bank in the destination country before crediting the university’s account. The SWIFT BIC identifies the beneficiary bank within the SWIFT network, and the IBAN identifies the specific account at that bank, in the European banking standard format. Both fields are mandatory inputs into the MT103, so a European demand letter missing either of them cannot be processed. SBI and Bank of Baroda forex desks specifically flag these as incomplete and return them for correction.

What if the university only issues an invoice and refuses to issue a demand letter?

Write a polite but specific email to the bursar or international office, explaining what the bank needs (addressed to the bank, fee breakup, due date, SWIFT and IBAN, signature and seal) and offering a template. Most overseas universities then reissue the document within 5 to 7 working days because they handle these requests routinely. If the university still refuses, speak to the branch manager about an exceptional approval where the invoice plus a separately downloaded banking instructions sheet from the university website are accepted together, tied by the student ID. This is discretionary.

Can the bank pay the university without a demand letter?

For the tuition portion, no. The IBA model education loan scheme followed by all PSU banks requires direct disbursement to the educational institution against a formal release instruction from the institution itself, which is the demand letter. The bank’s forex desk needs this to process the foreign currency outflow cleanly under the RBI framework. The only components that can sometimes be disbursed without a university-issued demand letter are smaller heads (books, laptop, living expenses for overseas students), and even those typically require quotations or receipts for reimbursement.

Can I use the same demand letter for visa proof of funds?

Yes, partially. UK, Irish, and Canadian visa officers accept a sanctioned education loan plus the corresponding demand letter, along with the bank’s disbursement confirmation once the SWIFT clears, as evidence that the tuition has been arranged or paid. This covers the tuition portion of the proof of funds package. The living expenses portion still needs separate evidence (savings, blocked account, GIC, sponsor declaration) depending on the country. The demand letter on its own does not satisfy the full proof of funds requirement; it covers the tuition slice.

Faz · The Honest Journey · 2026