A gap certificate is a self-declared affidavit on ₹100 stamp paper that explains any break of six months or more in your education, and most Indian lenders ask for it the moment your dates do not line up. I draft mine in under an hour: notarised, signed by the student, with one sentence per gap year stating the reason (NEET drop, work, illness, family).

The loan officer slid a printed checklist across the desk and circled one line near the bottom. “Gap certificate,” she said. “For the year between your 12th and your bachelor’s.” It was item number eleven on a list of seventeen, but it was the only one that did not have a clear template. The mark sheet was a mark sheet. The income proof was an ITR. The gap certificate was something I had never heard of, did not have, and had to produce in three days.

This post is the one I wish someone had handed me that afternoon. It covers what a gap certificate for an education loan actually is, the difference between an affidavit and a school-issued certificate, the right stamp paper denomination by state, a real sample you can adapt, and a reason-by-reason matrix of what banks actually accept versus quietly reject.

Answer capsule: A gap certificate for an education loan is a self-declaration affidavit on non-judicial stamp paper (₹100 in most states, ₹20 in some) explaining any academic gap of one year or more between your last qualification and the course you are funding. It must be signed by the student, notarised, and state the gap reason in clear factual terms. Banks accept it for failed attempts, work experience, illness, financial breaks, and documented family reasons.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The other paperwork that sits in the loan file: the bonafide certificate education loan post, the education loan interest certificate post, and the demand letter education loan post.

What a gap certificate for an education loan actually is

A gap certificate is a written declaration that explains any period of one year or more when a student was not enrolled in formal education. Banks ask for it because an unexplained gap on a transcript looks like a risk signal. The certificate converts an unknown into a documented reason, which lets the credit team tick the file as complete.

There are two things that get called “gap certificate” in practice, and they are not interchangeable. The first is a gap affidavit, which is a self-declaration the student writes and notarises on non-judicial stamp paper. The second is an institutional gap certificate, which is a letter on the letterhead of the last school or college the student attended, usually signed by the principal or registrar, confirming the period during which the student was not enrolled there.

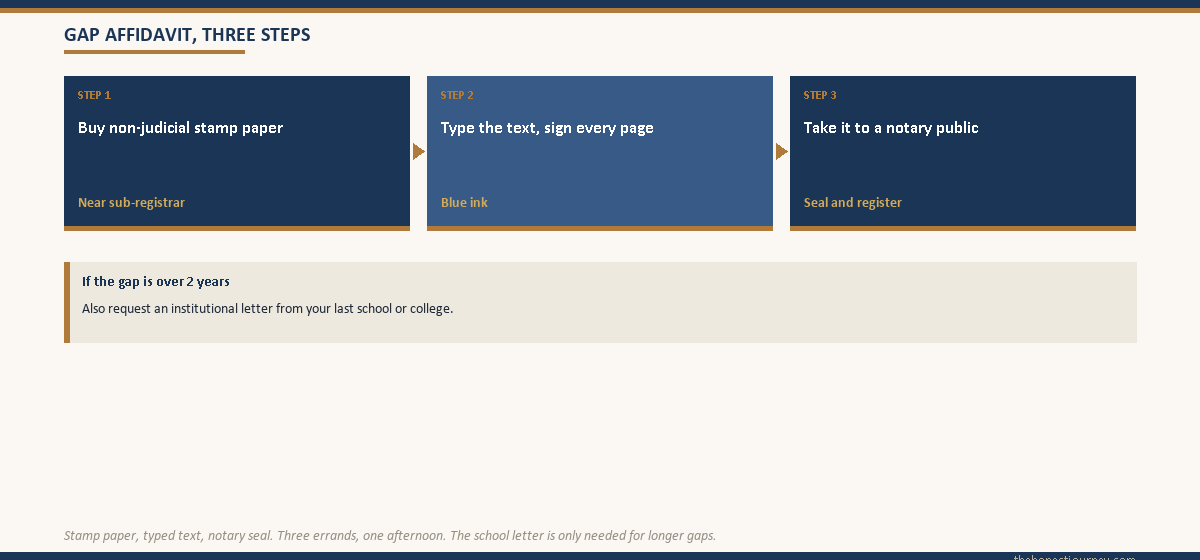

For an education loan, the bank almost always wants the affidavit version. Some banks ask for both if the gap is longer than two years. The school letter is supporting evidence. The affidavit is the primary document because it puts the explanation on the student’s own signature with legal weight.

Gap affidavit versus school-issued gap certificate

The distinction trips up most applicants. Here is the working difference.

| Aspect | Gap affidavit (self-declaration) | Institutional gap certificate |

|---|---|---|

| Who writes it | The student | The last school or college attended |

| Medium | Non-judicial stamp paper, then notarised | Institution letterhead, signed by principal or registrar |

| What it says | The reason for the gap and that nothing has been concealed | Confirms the dates the student was not enrolled there |

| Typical cost | ₹100 stamp paper plus ₹100 to 300 notary | Usually free, sometimes ₹50 to 200 admin charge |

| Turnaround | Same day if a notary is available | 3 to 10 working days at most institutions |

| What banks ask for | Required by almost every public sector and private bank | Optional supporting document, sometimes required for gaps over 2 years |

If you only have time and budget for one, do the affidavit. It is what the loan file actually needs. The school letter is a nice-to-have that strengthens longer gaps. For shorter gaps of one to two years, the affidavit alone is almost always sufficient.

Faz's ruleThe affidavit is the primary document. The school letter is supporting evidence.

Banks file the loan on the affidavit, not on the institutional letter. If you are running on a deadline, get the stamp paper and the notary done first. The school can issue a confirmation letter later if the credit officer asks for one.

Stamp paper denomination by state

This is the part most generic templates get wrong. They tell you “₹100 stamp paper” as if India ran on a single stamp duty schedule. It does not. Non-judicial stamp paper denomination for affidavits varies by state under the Indian Stamp Act and its state amendments. ₹100 is the most common, but several states use lower denominations for affidavits of this nature.

| State | Typical stamp paper for a gap affidavit |

|---|---|

| Maharashtra, Delhi, Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, Gujarat, West Bengal, Rajasthan, Madhya Pradesh, Haryana, Punjab, Uttar Pradesh, Bihar, Odisha | ₹100 |

| Kerala | ₹200 (state revised affidavit stamp upwards in recent years, confirm at the vendor) |

| Jharkhand, Chhattisgarh | ₹50 to 100 (varies by district vendor) |

| Assam, Himachal Pradesh, Uttarakhand | ₹20 to 50 |

| Goa | ₹50 |

If you are not sure, walk to the nearest stamp paper vendor near a sub-registrar’s office and ask for “non-judicial stamp paper for an affidavit.” They handle this every day and will sell you the correct denomination for your state. Going one denomination higher (₹100 in a ₹20 state) is always accepted. Going lower is the only mistake you can make, because some banks will reject the file and ask you to redo it.

What to write for each gap reason: the matrix

The single biggest reason banks ask follow-up questions on a gap certificate is vague wording. “Personal reasons” tells the credit officer nothing and creates a query that delays sanction by a week. Match your wording to the actual reason. Here is what works for each common case.

| Reason for gap | Recommended wording in the affidavit | Supporting documents to keep ready |

|---|---|---|

| Failed attempt or improvement exam | “I appeared for the [exam name] in [year] and used the period from [month, year] to [month, year] to prepare for re-attempt or improvement, after which I cleared the same in [month, year].” | Both mark sheets, coaching enrolment receipt if any |

| Competitive exam preparation (JEE, NEET, CAT, GRE, etc.) | “During the period from [month, year] to [month, year] I was preparing for [exam name] and was not enrolled in any institution. I appeared for the exam in [year].” | Admit card, score card, coaching invoice |

| Work experience | “From [month, year] to [month, year] I was employed with [company name] as [designation]. I have now resigned to pursue [course] at [institution].” | Offer letter, relieving letter, last 3 salary slips, Form 16 if available |

| Illness or medical reasons | “From [month, year] to [month, year] I could not continue formal education due to a medical condition that has since resolved. I am medically fit to resume studies.” | Doctor’s certificate, hospital discharge summary if any, fitness certificate |

| Financial break | “Due to family financial circumstances, I was unable to enrol in further education between [month, year] and [month, year]. The situation has since been resolved and the proposed loan covers my course funding.” | Co-applicant’s income documents for the gap years if available |

| Family responsibility | “From [month, year] to [month, year] I assisted with family responsibilities following [parent’s illness or family event]. Those responsibilities have concluded and I am now resuming formal education.” | Supporting medical or death certificate of the family member if relevant |

| Gap year by choice (travel, sabbatical, self-study) | “I took a planned gap year from [month, year] to [month, year] for self-study and skill development. During this period I was not enrolled in any institution and was not employed.” | Certifications from any short courses completed (MOOCs, language courses) |

Two notes from the credit team side. First, never write “personal reasons” as a standalone phrase. It triggers a query 100 percent of the time. Second, never overstate. If the gap was preparation for a competitive exam you did not eventually take, do not invent a result. Banks cross-check admit cards for any exam you claim to have appeared for.

Faz's ruleSpecific is sanction. Vague is query.

“Personal reasons” gets the file held. “From May 2023 to April 2024 I prepared for the NEET 2024 attempt, which I cleared with rank 12,400” gets the file moved. Match your wording to the actual reason and give the credit officer one less thing to ask about.

A real sample gap affidavit

Below is a sample affidavit text that has been accepted by public sector banks, private banks, and the major NBFCs for an education loan file. Adapt it to your state’s stamp paper denomination and your specific gap reason. Type it on the stamp paper, sign on every page, then take it to a notary.

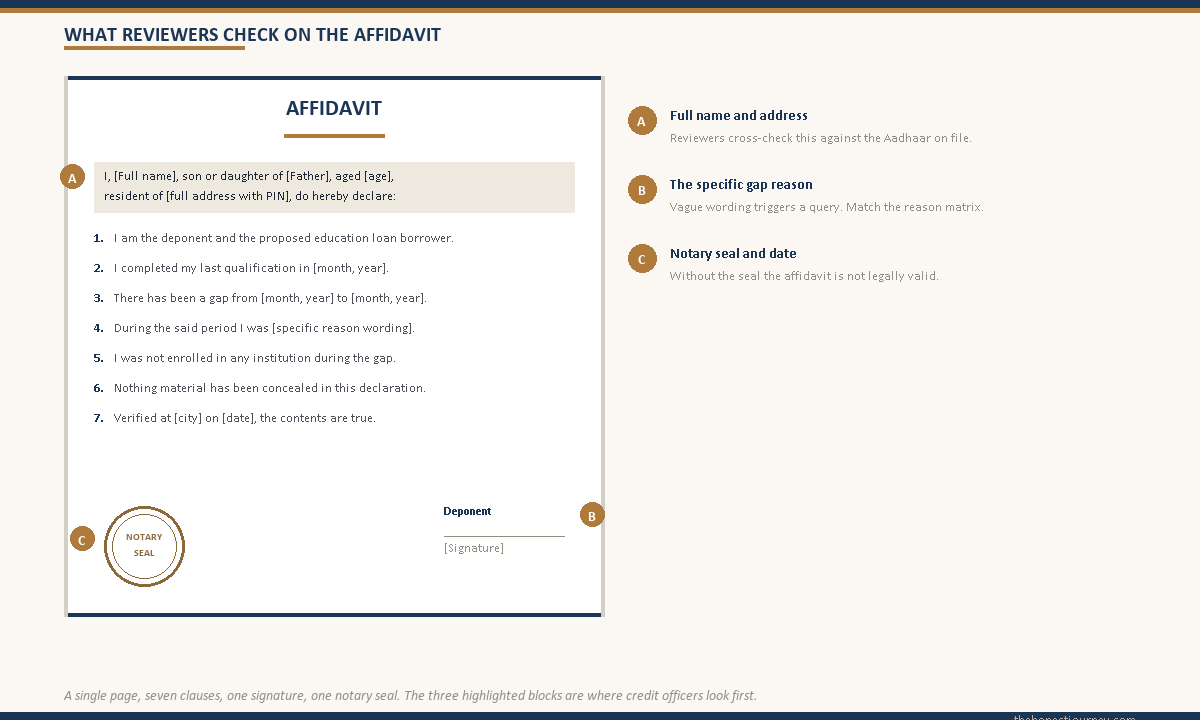

AFFIDAVIT

I, [Full name as on Aadhaar], son or daughter of [Father’s full name], aged [age] years, resident of [full address with PIN], do hereby solemnly affirm and declare as under:

1. That I am the deponent above named and the proposed borrower for an education loan from [bank or NBFC name] for pursuing [course name] at [institution name], [city], commencing in [month, year].

2. That I completed my [last qualification, for example “Higher Secondary Certificate examination”] from [board or institution name] in [month, year] with [percentage or CGPA].

3. That there has been a gap in my formal education from [month, year] to [month, year], a period of approximately [number] months.

4. That during the said period of gap, I was the specific reason that applies to you, in the wording from the matrix above.

5. That during the said gap period I was not enrolled in any college, university, or institution for any regular degree or diploma programme.

6. That nothing material has been concealed in this declaration. The statements made above are true to the best of my knowledge and belief.

Deponent

[Signature]

[Full name]

Verification: Verified at [city] on this [day] day of [month, year] that the contents of the above affidavit are true to the best of my knowledge and belief, and nothing material has been concealed therefrom.

Deponent

[Signature]

Notary attestation block (left blank for the notary to fill and seal).

Print this on the stamp paper, sign each page in blue ink, and walk it to any notary public for attestation. The notary will fix their seal, register the affidavit in their register, and hand it back. Total time at the notary is under twenty minutes for a standard case.

What banks accept versus what they reject

Not every gap affidavit clears. Here is the working pattern from credit team conversations and reader stories I have collected over the last two years.

Accepted without question: Failed-attempt gaps with both mark sheets attached. Competitive exam preparation gaps backed by an admit card. Work experience gaps backed by a relieving letter. Medical gaps backed by a hospital record or doctor’s certificate. Any gap under twelve months on a clearly documented affidavit.

Accepted with follow-up: Gaps between two to four years, especially where the reason is family responsibility or a self-funded skill break. The credit team usually asks for one supporting document (a parent’s medical record, a certification proof). Provide it once and the file moves.

Frequently rejected or sent back for redo: Affidavits that say “personal reasons” without elaboration. Affidavits where the stamp paper denomination is below the state minimum. Affidavits notarised in a different state from where the bank branch is located, when the bank is a regional cooperative or smaller private lender. Gaps over five years without any documentary supporting record. Anything where the dates in the affidavit do not match the gap visible on the transcript.

If your file gets sent back, do not panic. The fix is almost always procedural. Re-execute the affidavit on the correct stamp paper, tighten the reason wording per the matrix above, attach one piece of supporting evidence, and resubmit. The full documents required for an education loan list explains where the gap certificate sits in the broader file and what else needs to be ready alongside it.

Faz's ruleThe bank is not testing your morality. It is closing a documentation hole.

A gap certificate exists because the credit team needs a clean explanation on file. They are not judging the gap. They are filing it. Give them the cleanest possible version on the first attempt and the loan moves.

Is a gap certificate needed for a one-year gap

This is the most-asked sub-question on the topic and the answer is yes, but the standard varies. Most public sector banks treat any gap over six months as something to declare. Private banks and NBFCs almost universally ask for the affidavit if the gap is twelve months or more. If your gap is between six and twelve months, the cleanest move is to prepare the affidavit anyway. It costs ₹200 to 400 all-in (stamp paper plus notary) and removes a future query.

For gaps under six months, especially the natural break between school and college admission cycles in India, most banks do not ask for a separate affidavit. The break is treated as the standard academic gap that the admission letter already explains. The line worth watching is the actual gap visible on your transcript. If your 12th board result is from June 2024 and your bachelor’s enrolment is October 2024, there is no gap to declare. If your 12th board result is from June 2023 and your bachelor’s enrolment is October 2024, that is a 15-month gap and the affidavit is needed.

One more thing on the timing: get the affidavit notarised within sixty days of your loan application date. Banks sometimes flag affidavits older than three to six months as stale and ask for a fresh one. The affidavit itself does not expire legally, but bank credit policy treats anything older as needing a refresh. Bundle the affidavit prep with the rest of your education loan disbursement process documentation rather than executing it months in advance.

Common mistakes I keep seeing

Five patterns show up over and over in reader queries and they account for almost every gap certificate rejection.

First, getting the stamp paper denomination wrong. Below-state-minimum stamp paper is the single most common procedural reason for a redo. Always go to the vendor near a sub-registrar’s office and ask by name, not by guess.

Second, using a generic template that says “personal reasons.” This wording survives in template after template online and it does not pass credit checks. Use the matrix above and write the actual reason in factual terms.

Third, mismatching dates between the affidavit and the transcript. If your 12th mark sheet shows a pass date of June 2022 and your affidavit says the gap began in March 2022, the credit officer flags the inconsistency. Cross-check the dates against your mark sheets before you sign.

Fourth, skipping notary attestation. The affidavit must be notarised. An unattested affidavit, no matter how well written, is not legally a valid affidavit. Notary cost is ₹100 to 300 and takes fifteen minutes.

Fifth, treating the affidavit as a confessional. Some applicants write long emotional explanations about why life happened the way it did. Keep the affidavit factual and short. Five to seven numbered clauses is the standard length. The bank is not the audience for a personal essay.

If your application is otherwise borderline (income, collateral, course value), a sloppy gap certificate can be the thing that tips the file from sanctioned to declined. The full breakdown of why files get rejected is covered in the education loan rejection reasons in India post. Beyond the gap certificate, the collateral question often becomes the next pivot point, and the education loan without collateral post lays out where lenders draw that line for abroad courses.

The honest closing take

A gap certificate looks bureaucratic from outside the loan file. From inside the credit team, it is a tiny piece of paper that converts a question mark on your transcript into a documented answer. The bank is not assessing whether your reason was good enough morally. It is checking whether the file has a clean, signed, notarised explanation that closes the loop. Once that loop is closed, the credit officer moves on to the next checklist item.

If you spend an extra hour matching your wording to the actual reason, buying the correct stamp paper for your state, and getting the notary done properly the first time, you save yourself a week of back-and-forth later. The cost is ₹300 to 500 and one afternoon. The benefit is one less query in a file where queries delay disbursement and disbursement delay is what costs students their semester start.

The other thing worth saying out loud: a gap on a transcript is not a defect. Millions of Indian students take a year for competitive exam prep, for work experience, for family reasons, or for a planned break. The banking system has a standard documentary mechanism for it. Use the mechanism properly and the gap stops being a story you have to tell. It becomes a clause in an affidavit, filed, sealed, and done.

FAQ

What is a gap certificate for an education loan?

A gap certificate for an education loan is a self-declaration affidavit, executed on non-judicial stamp paper and notarised, in which the student explains any academic gap of one year or more between their last qualification and the course they are funding. Banks treat it as a mandatory file document because it converts an unexplained gap on the transcript into a documented reason on the borrower’s signature. It is sometimes also supplied as a letter on the previous institution’s letterhead, but the affidavit is the primary form.

What stamp paper is used for a gap certificate?

Non-judicial stamp paper, typically ₹100 in most Indian states including Maharashtra, Delhi, Karnataka, Tamil Nadu, Telangana, Gujarat, and Uttar Pradesh. Kerala has revised it to ₹200 in recent years. Some northeastern and hill states accept ₹20 to 50 denominations for routine affidavits. Always ask the vendor near a sub-registrar’s office for the correct current denomination in your state. Going one step higher in denomination is always accepted. Going below state minimum will trigger a redo.

Does a gap certificate need to be notarised?

Yes, almost always. An unattested affidavit is not legally a valid affidavit in the eyes of most banks, even if it is printed on the correct stamp paper. After printing the affidavit text and signing it, take it to any notary public. The notary will verify the deponent’s signature, affix their seal, and enter the affidavit into their register. Notary fee is typically ₹100 to 300 and the entire process takes fifteen to twenty minutes. Without the notary seal, the file is not complete.

Is a gap certificate needed for a one-year gap?

Yes, for almost all major public sector banks, private banks, and NBFCs. Any gap of twelve months or more between qualifications is treated as a declarable academic gap and the affidavit is required. For shorter gaps of six to twelve months, the affidavit is still recommended because it costs ₹300 to 500 all-in and removes a future query. Under six months, the standard admission-cycle break is generally accepted without a separate affidavit, since the institution’s admission letter explains the gap.

What reasons do banks accept on a gap certificate?

Banks accept any reason that is clearly stated and factually supportable. The most commonly accepted reasons are failed-attempt or improvement exams, competitive exam preparation with admit card evidence, work experience with a relieving letter, illness with medical records, family financial constraints, family responsibility caregiving, and planned gap years for self-study or certifications. The reason that consistently triggers a query is the vague phrase “personal reasons.” Always replace it with the specific factual reason, using clear dates and one supporting document where applicable.

What is the difference between a gap affidavit and an institutional gap certificate?

A gap affidavit is a self-declaration the student writes on non-judicial stamp paper and gets notarised. An institutional gap certificate is a letter on the previous school or college’s letterhead, signed by the principal or registrar, confirming the dates the student was not enrolled there. For an education loan, the affidavit is the primary document banks require. The institutional letter is a supporting document, sometimes requested for gaps longer than two years. If you can only provide one, prioritise the affidavit.

Can I write the gap certificate myself or do I need a lawyer?

You can write it yourself. The template in this post has been accepted by major banks and NBFCs and does not need legal drafting. Type the affidavit on the correct stamp paper, sign every page in blue ink, and take it to a notary for attestation. The notary is the only external professional in the loop. Lawyers are not required for a standard gap affidavit. If your case is unusually complex (multiple gaps, legal disputes during the gap, criminal record disclosure), a one-time consultation with a lawyer is worth the small fee.

How long is a gap certificate valid?

The affidavit itself does not legally expire, but bank credit policy generally treats affidavits older than three to six months as stale and asks for a fresh one. The practical rule is to execute the affidavit within sixty days of your loan application date. If your loan is sanctioned in principle but disbursement is delayed by several months, the bank may ask you to re-execute the affidavit closer to disbursement. The cost of redoing it is small and the file moves cleaner with a recent date on the document.

For factual references on stamp duty under the Indian Stamp Act, see the Reserve Bank of India for banking master directions on loan documentation, the Indian Banks’ Association for the model education loan scheme, the Ministry of Education for academic gap norms, and the State Bank of India education loan product page for the public sector documentation checklist.

Faz · The Honest Journey · 2026