An education loan interest certificate is the annual statement your bank issues that shows how much interest you paid on your education loan in a given financial year, and it is the single document the Income Tax department wants when you claim a section 80E deduction. You can download it from SBI YONO, Bank of Baroda bob World, Canara ai1, HDFC NetBanking and ICICI iMobile in under five minutes if the loan account is mapped to your login. The certificate is free, must show your loan account number, the financial year, principal repaid, interest paid and a reference to section 80E, and you can claim every rupee of interest paid for up to 8 assessment years from the year repayment begins.

Every July my inbox fills up with the same panic. People who finished their B.Tech two years ago, started repaying their education loan, and are filing their first ITR as a salaried earner. They have heard about section 80E. They cannot find the interest certificate. The bank tells them it is on the app. The app shows them a generic loan statement that does not say “80E” anywhere, and they assume that is wrong.

It usually is not wrong. The certificate is there, the wording is just unfamiliar, and the path inside each bank’s app is slightly different. This post walks through what the certificate is, exactly how to pull it from the five banks most of my readers actually use, how to plug it into the new ITR portal under 80E, and what to do when the certificate the bank gives you is wrong.

The other paperwork that sits in the loan file: the documents required for education loan post, the bonafide certificate education loan post, and the gap certificate for education loan post.

What an education loan interest certificate actually is

It is a financial-year summary. For the year 1 April to 31 March, the bank tells you three numbers for your loan account: the opening balance, the principal you repaid, and the interest you paid. It also states your loan account number, the borrower’s name and PAN, and a reference line that says something like “issued for the purpose of claiming deduction under section 80E of the Income Tax Act, 1961”. That last line is the one the Income Tax department wants to see.

It is not the same as a regular loan statement. A statement shows every transaction with date stamps. The interest certificate is a one-page (sometimes two-page) summary that totals the interest column for the FY and adds the 80E reference. Most banks generate a fresh certificate around the second week of April, once the March EMI has cleared and the financial year has closed.

It is also not the same as the provisional certificate some banks issue mid-year. A provisional one is an estimate of interest you will pay by 31 March, useful for employers who want a Form 12BB declaration. The final certificate, the one you upload at ITR time, is post-March and shows actuals.

The deduction itself is governed by section 80E of the Income Tax Act. The full statutory text and the IT department’s clarification on what qualifies sits on the Income Tax India e-filing portal. The short version: 100 percent of the interest you pay on a higher-education loan, taken from a scheduled bank or notified financial institution, for yourself, your spouse, your children, or a student for whom you are the legal guardian, is deductible from your taxable income for up to 8 assessment years starting the year you begin repaying. There is no upper limit on the deduction amount.

Faz's ruleDownload the certificate in the second week of April, after the March EMI clears. Earlier downloads can miss the last instalment and short your 80E claim.

Every year I see people pull the certificate on 1 April, file ITR in June, and then realise the March EMI interest was not on it. The bank ledger had not closed yet. Wait one week into April. The certificate is free to regenerate, so you can pull it again if needed, but it is easier to do it once and do it right.

Why this matters more than people think

For a salaried 25 year old in the 30 percent slab who paid 1.2 lakh of interest in a FY, an 80E claim is a 36,000 rupee tax saving. That is one EMI. Over the typical 6 to 8 year repayment window, the cumulative saving on a 25 to 40 lakh loan often crosses 2 to 3 lakh. People skip the claim because the paperwork feels like too much for the first year, then they discover what they left on the table and back-file.

The other reason it matters: 80E is one of the cleaner deductions in the new tax regime conversation. As of AY 2025 to 2026, 80E is available only under the old tax regime. If your interest outflow is meaningful (above 80,000 to 1 lakh a year), running the old-regime calculation with 80E often beats the new regime even after losing the standard deduction differential. The certificate is what makes that calculation defensible to the assessing officer if a notice ever comes.

I cover the full 80E math, the 8 assessment year clock, and the eligibility edge cases (loans from family members, NBFCs not on the notified list, foreign lenders) in the education loan 80E deduction pillar. This post is the operational companion: how to actually get the document in hand.

SBI YONO: how to download from the State Bank of India app

SBI services more education loans than any other lender in the country, including the Global Ed-Vantage portfolio for overseas study. If your loan is with SBI, you have two clean paths.

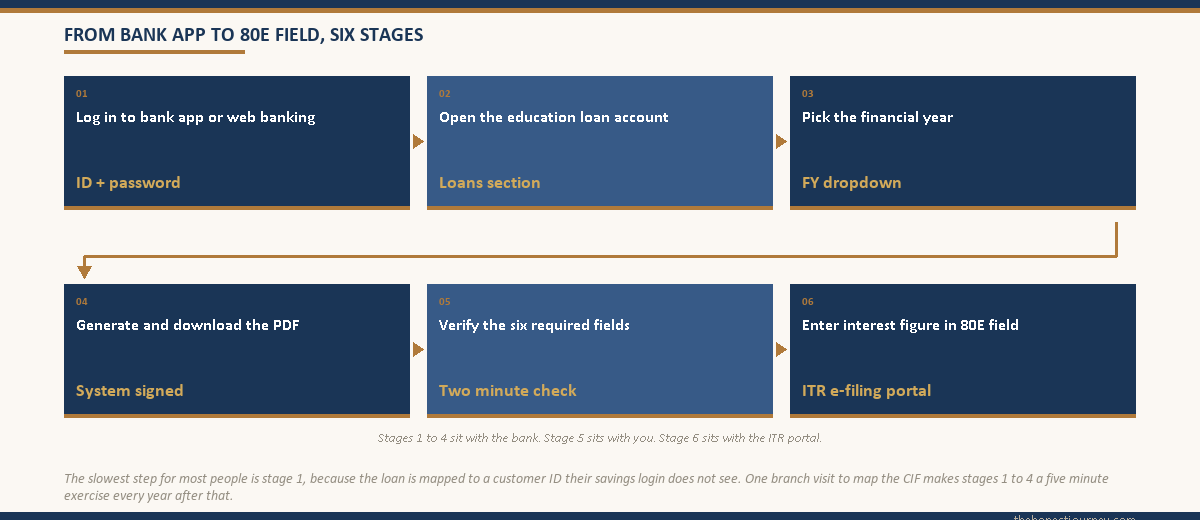

The first is YONO. Log in to YONO, go to the Loans section, and find the education loan account. Inside the account page there is a tab that groups statements and certificates together. Under that tab the relevant entry is the interest certificate for the requested financial year. You pick the FY (the app will offer the current and previous years), and YONO generates a PDF you can save or share. The PDF is system-generated, carries SBI’s digital signature, and is accepted by the ITR portal as is.

The second path is SBI’s retail internet banking on a laptop. Log in to onlinesbi.sbi, go to e-Services, and find the section for issuing certificates. The interest certificate option lists your eligible loan accounts and the FY dropdown. Same PDF, same digital signature.

If neither shows your loan account, the most common reason is that the loan is mapped to a customer ID that is not linked to your YONO login (this happens when the loan was sanctioned at a branch different from your savings account branch). The fix is a branch visit with your loan sanction letter and account number, asking them to map the loan customer ID to your CIF. Once mapped, the certificate shows up the next working day.

Bank of Baroda bob World: how to download

BOB has consolidated its retail apps into bob World. Log in, open the menu, and find the Loan Account section. Inside the education loan account, the documents area lists the interest certificate option grouped with statements. Select the financial year, and the app generates the certificate as a PDF.

If the certificate option is not visible on the app, the BOB internet banking site on a laptop usually shows more. Log in at bankofbaroda.in retail banking, go to Services or Loans, and look for the certificate request flow. BOB also accepts requests by email to the branch where the loan is held. The branch turnaround for an emailed request is usually 2 to 5 working days, and they send the PDF back to your registered email.

A small thing worth knowing: BOB’s certificate for the Vidya scheme overseas loans sometimes splits interest into pre-moratorium and post-moratorium sections, with a note about the capitalised interest from the moratorium period. Both pre and post numbers are eligible for 80E as long as they are actual interest payments you made (capitalised interest that was added to principal during the moratorium and is being repaid through EMI counts as interest under 80E in the year you actually pay it through EMI, not the year it was capitalised).

Canara ai1: how to download

Canara Bank’s ai1 app is the consolidated retail app after the eSyndicate merger. Log in, go to the Loan section, and open the education loan account. The interest certificate option sits in the account services area, sometimes labelled “IT certificate” rather than “interest certificate”. Pick the FY, generate the PDF.

Canara’s older internet banking portal at canarabank.com also offers the same. The login flow is netbanking, then the services or loans tab. For old syndicate-origin accounts that did not migrate cleanly, the app sometimes shows the loan but not the certificate option. In that case, a written request at the branch where the loan sits, with your loan account number and the FY, gets a certificate issued in 3 to 7 working days. Canara branches issue it on letterhead with a stamp, which is also accepted by the ITR portal as long as it has the standard fields.

HDFC NetBanking: how to download

HDFC’s education loan portfolio is smaller than the PSU banks but the digital path is the cleanest. Log in to HDFC NetBanking on a laptop, go to the Enquire section, and find the Loan section. Under the education loan account, there is a Loan Interest Certificate option. Select FY, generate, download.

On HDFC’s mobile banking app, the same option lives under the loan account page in the statements and certificates grouping. The PDF is digitally signed. HDFC also lets you forward the certificate to your registered email directly from the same screen, which is useful if you are filing ITR from a phone.

If your education loan is with HDFC Credila (the education loan subsidiary spun off from HDFC), the certificate is on the Credila customer portal, not on HDFC Bank’s app. The two systems do not share login. For Credila loans, the customer portal login uses your loan account number, and the same certificate flow exists there.

ICICI iMobile: how to download

ICICI’s iMobile Pay app handles both retail accounts and loans for most customers. Log in, open the loan account, and find the certificate section grouped with account statements. The interest certificate option lists the eligible FYs. Generate, save.

ICICI internet banking at icicibank.com retail login also offers the same under a tax-related certificates section. ICICI’s certificates carry both the digital signature and a QR code that the IT department can use to verify authenticity if a notice is raised on the deduction.

For ICICI loans that were sanctioned through the corporate or salaried lending arm rather than the standard retail branch, the certificate sometimes does not show up on iMobile. The branch or relationship manager can email it within 2 to 5 working days on request. Make sure the request specifies “education loan interest certificate for FY 2025 to 2026 for the purpose of section 80E claim”. The wording matters because the bank’s internal teams have different formats for personal loan certificates and education loan certificates, and you want the one that carries the 80E reference line.

Faz's ruleIf the bank's app cannot find your loan account, the loan is mapped to a different customer ID. Fix it once at the branch, and every future certificate is one tap away.

This is the single most common reason readers say the app does not work. The loan was sanctioned at branch A, your savings is at branch B, and the customer IDs were never linked. Walk in once with your sanction letter and ask for CIF mapping. Two months later you will forget you ever had this problem.

What the certificate must show before you upload it to the ITR portal

Before you upload, eyeball the certificate for six things. Loan account number printed in full and matching your sanction letter. Borrower’s name spelled the way it sits on your PAN (initials versus full middle name causes problems). The financial year stated clearly (1 April to 31 March of the relevant year). Principal repaid in the FY (this is not deductible under 80E but is useful for your own records). Interest paid in the FY (this is the number that goes into the deduction field). A reference line that mentions section 80E of the Income Tax Act 1961, or the phrase “issued for income tax purposes” with the interest component clearly labelled.

If any of the six is missing or wrong, the certificate is technically incomplete. The ITR portal will accept it without complaint, but a future scrutiny notice can ask for the corrected document. Banks fix these on request without charging anything.

How to use the certificate on the ITR portal under section 80E

The interest paid figure goes into the section 80E field of your ITR form. On the new income tax e-filing portal at incometax.gov.in, the path inside the ITR-1 or ITR-2 form is the deductions tab, where 80E sits in the list of chapter VI-A deductions. You enter the interest paid as a single rupee figure. You do not need to upload the certificate at the time of filing.

You do need to keep the certificate. If the IT department raises a section 143(1) intimation or a 143(2) scrutiny notice, the certificate is the primary evidence. Keep both the digital PDF and a printed copy in your loan folder. The retention rule is 8 years from the end of the relevant assessment year, which lines up neatly with the 8 assessment year claim window.

One subtlety: 80E covers interest on a loan taken for “higher education” of the borrower, spouse, children or a student under legal guardianship. The borrower of the loan and the claimant of the deduction must be the same person, with one exception. If your parent took the loan as the primary borrower and you are the co-applicant, the deduction is claimable by whichever of you is actually paying the EMI. The bank’s interest certificate is issued in the primary borrower’s name by default. If you (the student) are repaying and want to claim, request the bank to issue the certificate in your name as co-borrower, citing your contribution to the repayment. PSU banks accept this; some private lenders push back. The cleanest setup is to make sure the EMI is debited from the account of whoever will claim 80E.

What to do when the bank’s certificate is wrong

The three errors I see most often: an interest figure that does not match what the loan account ledger shows (usually because a March EMI was clubbed or excluded), a missing 80E reference line, and a borrower name that does not match the PAN. All three are fixable.

For the interest figure, request the bank to issue a fresh certificate after reconciling against the loan account ledger. Ask for a transaction-level statement alongside, so you can see exactly which EMIs were counted and which were not. The bank reconciles and reissues within 3 to 7 working days for most PSU banks, sometimes faster for HDFC and ICICI.

For the missing 80E reference, this is almost always a template issue. Ask specifically for “the format that carries the section 80E reference line”. The bank has multiple certificate templates and the wrong one was sent.

For a name mismatch, the bank updates your records using your PAN card and a request letter. The corrected certificate gets issued the same week. This is also a good time to check that your registered name with the bank matches your registered name with the IT department, because mismatches there cause separate problems at refund stage.

The deeper context on when interest accrues, when it capitalises, and how the disbursement structure affects what shows up on the certificate sits in the education loan disbursement process post. If you are also dealing with TCS on a remittance for an overseas course, the certificate for 80E and the TCS credit are separate threads, covered in the TCS refund on education loan post. And if your loan was rejected partway through and you switched lenders mid-course, you can still claim 80E on the interest paid to each lender; both will issue separate certificates. The full lender-switch context is in the education loan rejection reasons post. And once you finish an overseas course and start earning there, the tax side is governed by the DTAA rules for Indian students abroad, which keep the same income from being taxed in both countries.

Faz's ruleMatch the certificate's interest figure to your own loan account ledger before you file. A two minute check now saves a notice response later.

I keep a small spreadsheet where each month’s EMI is split into principal and interest using the bank’s amortisation schedule. At year end I sum the interest column and compare to the certificate. If they differ by more than 50 rupees, I ask the bank to reconcile before I file. Once in five years it has caught a real error. The other four years it took two minutes and gave me peace of mind.

The honest closing take

The certificate itself is a five-minute download for most people most of the time. The reason it feels harder than that is that the apps phrase it differently, the option sometimes hides behind a “statements” grouping rather than a “certificates” one, and the loan is sometimes mapped to a customer ID that the app does not see.

None of those are real problems. They are one branch visit or one email away from being solved permanently. What is a real problem is people who do not download the certificate at all, file ITR without claiming 80E, and lose 20 to 40 thousand rupees a year in tax for no reason other than the paperwork felt unfamiliar.

If you took an education loan and you are now repaying it, the second week of April is the moment to pull the certificate, verify the six fields, and tuck it into your tax folder. Six years from now when the loan is closed and the 80E clock has run, you will have a clean record and a clean conscience. The tax department respects both.

FAQ

What is an education loan interest certificate?

It is an annual statement issued by the bank or lender that summarises the interest you paid on your education loan in a given financial year. It states the loan account number, the borrower’s name and PAN, the financial year, the principal repaid, the interest paid, and a reference to section 80E of the Income Tax Act. The interest figure on this certificate is what you claim as a deduction in your income tax return. It is free, and most banks generate it automatically after the financial year closes in early April.

How do I download an interest certificate from SBI YONO?

Log in to YONO, go to the Loans section, open your education loan account, and look for the statements and certificates grouping inside the account page. The interest certificate option lets you pick the financial year and generates a digitally signed PDF you can save or share. If the loan account is not visible on YONO, it means the loan is mapped to a different customer ID; a branch visit with your sanction letter to request CIF mapping fixes this permanently. After that, every future certificate is one tap away.

Is the interest certificate needed for the section 80E claim?

Yes, it is the primary supporting document. You do not need to upload it at the time of filing your ITR, but you must retain it for at least 8 years from the end of the relevant assessment year. If the Income Tax department raises a section 143(1) intimation or a 143(2) scrutiny notice on your 80E deduction, the certificate is what proves the interest figure you claimed. Without it, a notice can lead to the deduction being disallowed and the tax becoming payable with interest and penalty.

Is the education loan interest certificate free?

Yes, in every PSU and major private bank in India the certificate is issued free of charge, whether you download it from the app or request it at the branch. Some private banks charge a nominal fee for additional physical copies on letterhead, but the digital PDF version is always free. If a bank or NBFC tries to charge for the first issuance of the certificate, that is non-standard and worth escalating to the branch manager or, for systemic refusals, to the RBI banking ombudsman.

What if the bank does not give me an interest certificate?

Submit a written request at the branch where the loan is held, addressed to the branch manager, asking for an interest certificate for the relevant financial year stating it is required for a section 80E claim. PSU banks are obliged to issue this under the RBI’s fair practices code; the turnaround is usually 3 to 7 working days. If the branch refuses or delays beyond 30 days, escalate to the bank’s nodal officer and then to the RBI banking ombudsman. Refusal to issue the certificate is rare and almost always resolves at the branch level.

How many years of interest certificate can I claim under 80E?

Section 80E allows deduction of education loan interest for up to 8 consecutive assessment years, starting from the year you begin repaying the loan, or until the loan is fully repaid, whichever is earlier. Each year is a separate claim and needs its own interest certificate. There is no upper monetary limit on the deduction amount. If your loan repayment runs longer than 8 years, the interest you pay from year 9 onwards is not deductible under 80E, so the calculation is worth running before you opt for the longest repayment tenure.

Can both parent and child claim 80E on the same education loan?

No. The deduction can only be claimed by the person who is actually paying the EMI, and only that person should receive the interest certificate in their name. If the parent took the loan and the parent is repaying, the parent claims 80E. If the student (as co-applicant) starts repaying after course completion, the student claims, and the bank can reissue the certificate naming the student as co-borrower-claimant. Splitting the deduction between two people or claiming it twice from the same certificate is not allowed and will trigger a notice.

What if my interest certificate shows the wrong interest figure?

Request the bank to reconcile against the loan account ledger and issue a corrected certificate. Ask for a transaction-level statement alongside, so you can match each EMI’s interest component against the certificate total. PSU banks reconcile and reissue within 3 to 7 working days; private banks are often faster. If you have already filed your ITR with the wrong figure, you can file a revised return under section 139(5) before the assessment is completed, attaching the corrected certificate. Do not let a wrong figure sit through scrutiny.

Faz · The Honest Journey · 2026