DTAA for students decides who taxes your foreign earnings once you start making money abroad, and for most students on a stipend the answer is that India taxes very little or nothing at all. Your Indian tax exposure hinges on residential status: cross 182 days outside India in a financial year and you usually become a non-resident, which means only India-source income stays taxable here. The Double Taxation Avoidance Agreement plus the foreign tax credit mechanism stops the same rupee being taxed twice. This is the map, not tax advice.

I get this question from second-year Master’s students more than almost anything else. They land a part-time campus job or start OPT, see tax withheld from a small paycheck, and panic that India is also going to come after the same money. Then a cousin or a YouTube clip tells them they “have to file in both countries” and the anxiety doubles.

The honest version is calmer than the panic. Most students earning a stipend or a modest part-time wage owe India little or nothing, because once you cross the day thresholds you are a non-resident for Indian tax, and a non-resident is only taxed on income that arises in India. The reason to understand DTAA anyway is that the filing hygiene you build now matters later, when you apply for PR, renew a visa, or move money home. This post is the map of how it works.

Residential status is the hinge for DTAA for students

Before any treaty article matters, one question settles most of the outcome: are you a resident or a non-resident of India for the financial year? Indian tax residency runs on physical presence, counted in days, under Section 6 of the Income Tax Act. The treaty only comes into play when both countries claim you, and your residency status is what decides whether that even happens.

The basic rule: you are a resident of India for a financial year (1 April to 31 March) if you were physically in India for 182 days or more in that year. There is a second limb (60 days in the year plus 365 days across the four preceding years), but a special carve-out exists for Indian citizens leaving India for employment abroad, which raises their threshold to 182 days. For a student going abroad to study and then work, the practical line you watch is the 182-day mark.

| Days in India during the FY | Likely Indian tax status | What India taxes |

|---|---|---|

| 182 days or more | Resident | Worldwide income (with treaty relief) |

| Less than 182 days (left for work/study abroad) | Non-resident | India-source income only |

| Returning after years abroad (conditions met) | RNOR for a transition window | India-source plus foreign income controlled from India |

The year you fly out matters most. If you leave India in August to start a September intake, you may already have spent close to 150 days in India before departure, which can keep you a resident for that first financial year. From the next full year abroad, you are typically a non-resident, and your foreign stipend stops being India’s concern. The official residency rules and the treaty texts both live on the Income Tax Department portal at incometax.gov.in.

Faz's ruleResidential status, not your passport, decides what India taxes. An Indian citizen who is a non-resident for the year is taxed by India only on India-source income.

The single most common mistake I see is students assuming their Indian passport means India taxes their foreign salary forever. It does not. Tax residency is about days in the country, not citizenship. Once you cross the 182-day line out of India, your US, UK, or Australian stipend is outside India’s net for that year. Count your days carefully in your fly-out year, because that is the one year the status can go either way.

What the DTAA actually does

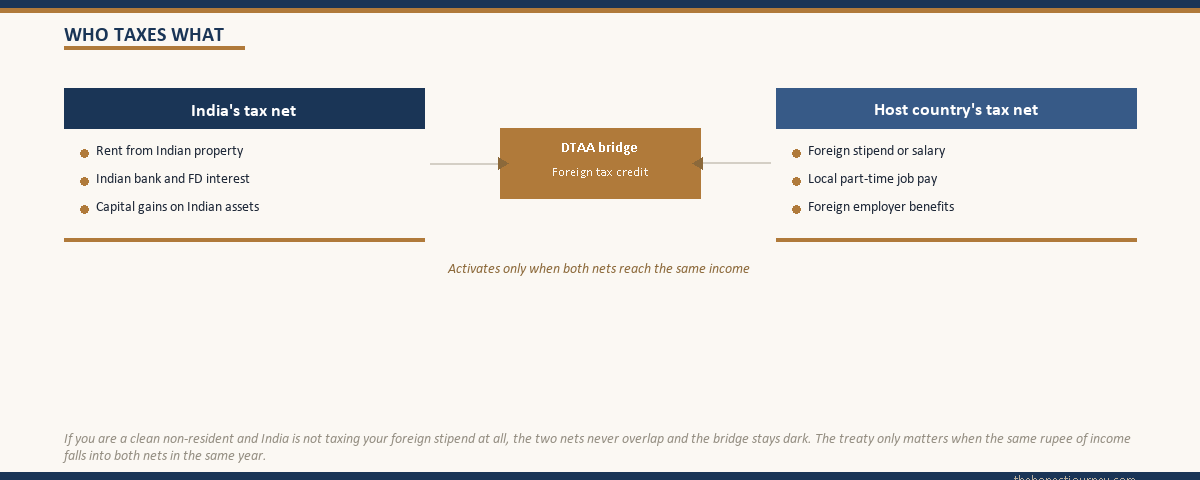

A Double Taxation Avoidance Agreement is a bilateral treaty between India and another country that allocates taxing rights so the same income is not fully taxed twice. India has signed comprehensive DTAAs with most major study destinations including the US, UK, Canada, Australia, and Germany. The Income Tax Department keeps a plain explanation and the full treaty list on its DTAA help page.

A DTAA does two things that matter to a student. First, it decides which country gets the first or sole right to tax a given type of income (employment, business, interest, the student or trainee categories). Second, where both countries can tax, it provides a relief mechanism so the tax paid in one country is credited in the other, rather than stacking. That relief is the foreign tax credit, and it is the part you will actually use.

Crucially, you only need DTAA relief if both countries are taxing the same income. If you are a clean non-resident of India for the year and your only income is your foreign stipend, India is not taxing it at all, so there is no double tax to relieve and no treaty article to invoke. The treaty becomes relevant when you remain a resident of India (the fly-out year, or a year you return), or when you have India-source income alongside your foreign earnings.

The student and trainee articles in most DTAAs

Many DTAAs contain a dedicated article (often Article 20 or Article 21, the numbering varies by treaty) covering payments received by students and business trainees. These articles typically say that money a student or trainee receives from sources outside the host country, solely for their maintenance, education, or training, is exempt from tax in the host country. The India to USA treaty, for example, carries such a students-and-trainees provision.

Read what that article does and does not cover, because students routinely over-claim it. It generally protects remittances you receive from India (your parents wiring living costs, or scholarship money sent from home) from being taxed by the host country. It does not usually shield wages you earn from a job inside the host country. A campus job, an internship paycheck, or OPT employment income is earned locally and is taxed locally under the host country’s normal rules, subject to that country’s own thresholds and standard deductions.

So the practical pattern for a typical student is: money from home for living costs is protected by the student article and not taxed abroad, while a local part-time wage or OPT salary is taxed by the host country at its own rate, often low or zero after that country’s personal allowance. India, meanwhile, taxes none of it in a year you are a non-resident. The student article matters most for funded scholars and for the fly-out and return years when residency is mixed.

Faz's ruleThe student-article exemption usually covers money sent from India for your upkeep, not wages you earn from a job in the host country. Do not assume your campus paycheck is treaty-exempt.

I have seen students confidently tell their university’s payroll office that their wages are “DTAA exempt” because of the student article. That is almost never right for locally earned wages. The article protects your maintenance money from home. Your on-campus or OPT salary is host-country income and follows host-country rules. The good news is host-country tax on a small student wage is usually tiny after the local personal allowance, so this is rarely a real cost, just a thing to get factually right.

The foreign tax credit and Form 67

The foreign tax credit (FTC) is the engine of double-tax relief, and it only matters in a year when India is also taxing the income. If you are a resident of India for a financial year (your fly-out year, or a year you return mid-year) and you also paid tax abroad on the same income, India lets you reduce your Indian tax bill by the foreign tax already paid, under the relevant DTAA article read with Rule 128 of the Income Tax Rules.

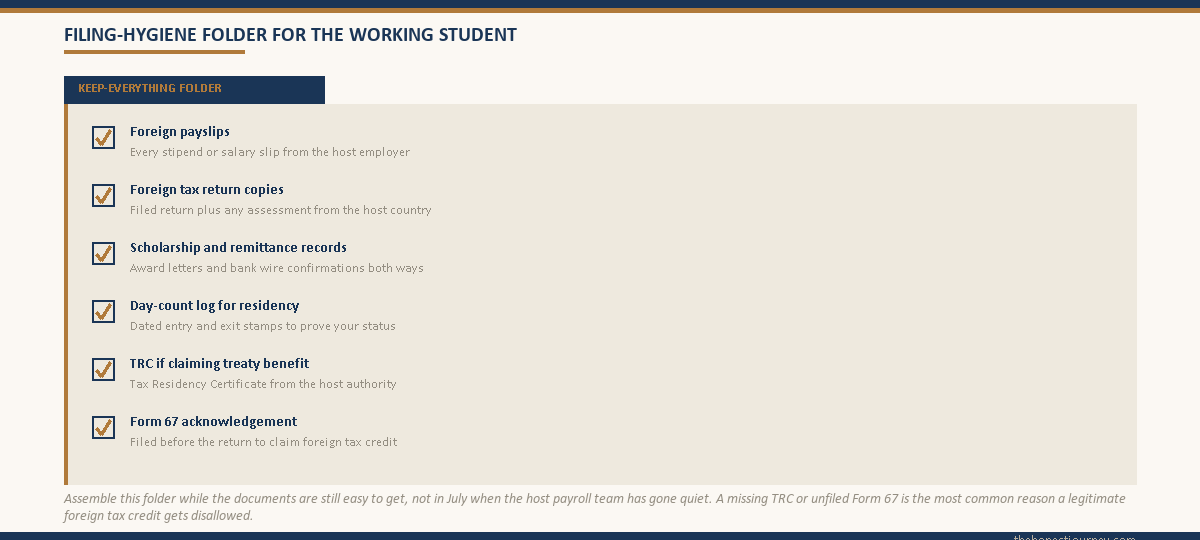

To claim the FTC in your Indian return, you file Form 67 on the e-filing portal before or along with your Indian ITR for that year. Form 67 is a statement declaring the foreign income and the foreign tax paid on it. You attach proof of the foreign tax (a payslip showing withholding, a foreign tax return, or a certificate from the foreign tax authority). Without Form 67, the Indian system can deny the credit even when the treaty clearly allows it, so the form is not optional paperwork, it is the trigger.

| Your situation that year | Is FTC / Form 67 needed? |

|---|---|

| Non-resident of India, only foreign stipend | No. India is not taxing it, so nothing to relieve. |

| Resident of India for the fly-out year, foreign wage taxed abroad | Yes. File Form 67 to credit the foreign tax against Indian tax. |

| Resident or RNOR with both Indian and foreign income | Yes, for the foreign-taxed portion India also taxes. |

The order of operations matters. First settle your residential status for the year. If you are a non-resident, you usually have no FTC question at all. Only if you are a resident (or RNOR with foreign income in India’s net) do you reach for Form 67 and the FTC. This is also why keeping your foreign payslips and any foreign tax filings is worth the drawer space, because they are the evidence the credit relies on.

The Tax Residency Certificate (TRC)

To claim treaty benefits, India can ask you to prove you are a tax resident of the other country. That proof is the Tax Residency Certificate (TRC), issued by the tax authority of your host country. If you want to rely on the India to host-country DTAA to reduce or eliminate Indian tax on a slice of income, you obtain the TRC from the host country’s tax office and keep it ready. Where the TRC lacks certain particulars, India may also ask for Form 10F, which supplies the missing details.

For most students who are clean non-residents with only a small foreign wage, you will not need to produce a TRC, because you are not claiming a treaty position in an Indian return at all. The TRC becomes relevant when you actively invoke the treaty in India: a resident-year FTC claim, or income that India would otherwise tax where you want the treaty rate. Knowing the TRC exists, and where it comes from, saves a scramble later if your situation gets more complex (say you start earning Indian rental income or interest while working abroad).

When you still file in India

Being a non-resident does not always mean you skip an Indian return. You may still need to, or want to, file an Indian ITR in these cases. If you have any India-source income (rent from a flat back home, interest from Indian savings or fixed deposits, capital gains on Indian shares or mutual funds), that income is taxable in India regardless of your residency, and you file to report it. If TDS or TCS was deducted in India and you want it refunded (for example, the TCS on your education loan remittance), filing the ITR is how you claim it back, which I covered in my TCS refund on education loan post.

You also keep an eye on India because your education loan story does not end when you fly out. The interest you pay continues to qualify for the Section 80E deduction in years you have Indian taxable income, and the lender issues an interest certificate each year, which I explain in the education loan interest certificate post. Building the habit of a clean annual filing, even a NIL or refund-only return, keeps your Indian tax record continuous, which is exactly the kind of paper trail a future PR or long-term visa process likes to see.

The RNOR transition when you come home

The day you decide to move back to India, residency flips again, and there is a soft-landing status that protects you for a while. When you return after years abroad, you usually do not become an ordinary resident immediately. You pass through Resident but Not Ordinarily Resident (RNOR) status for a transition window, during which India still does not tax your foreign income unless that income is derived from a business controlled or a profession set up in India.

This RNOR window is genuinely valuable. It gives returning students and professionals time to bring overseas savings home, close foreign accounts, and let foreign investments mature, without India immediately taxing the worldwide income. Get the timing of your return and your day counts right and you can extend the benefit across more than one financial year. I wrote the full mechanics, including how long RNOR lasts and how to plan the return, in the NRI tax for returning students and RNOR post, and it is the companion to read alongside this one.

The reason I link them is that DTAA and RNOR are two ends of the same journey. DTAA governs the years you are out and earning. RNOR governs the re-entry. Students who understand both avoid the two classic mistakes: over-paying Indian tax on foreign income while abroad, and accidentally triggering full worldwide taxation by mistiming the return.

The honest framing on cost and the cost of studying abroad

Here is the part nobody monetising fear will tell you. For the large majority of students on a stipend or a small part-time wage, the actual double-tax exposure is close to zero. You are a non-resident of India for the working years, so India taxes none of your foreign earnings. The host country taxes your local wage at its own rate, which after the personal allowance is often tiny on a student-sized income. There is frequently no double tax to relieve, because only one country is taxing the income in the first place.

So why bother with any of this? Because the filing hygiene compounds. A returning student who can show a clean, continuous tax record (residency tracked, foreign income declared where required, refunds claimed properly) has an easier time with PR applications, visa renewals, large remittances, and any future scrutiny. The cost of the income tax is small. The value of the clean paper trail is large, and it shows up years later. If you are still at the planning stage and weighing the overall numbers, my cost of studying in the USA for Indian students post sets the broader financial picture this tax question sits inside.

One more honest line, and I will keep saying it. This post is the map, not the route for your specific case. DTAA outcomes turn on the exact treaty, your precise day counts, the nature of each income stream, and the year in question. When real money is at stake, especially in a fly-out or return year with mixed residency, sit with a qualified chartered accountant who handles cross-border returns. Use the official sources to check the rules yourself: the treaty texts and residency rules on incometax.gov.in, the forex and remittance framework on rbi.org.in, the FEMA provisions on fema.rbi.org.in, and the policy backdrop from the Department of Economic Affairs at dea.gov.in.

FAQ

What is DTAA for students?

DTAA stands for Double Taxation Avoidance Agreement, a treaty between India and another country that decides which country taxes a given income so the same money is not fully taxed twice. For students who start earning abroad through part-time work, OPT, or post-study jobs, the DTAA allocates taxing rights between India and the host country and provides a foreign tax credit where both could tax the same income. In practice, students who are non-residents of India rarely need to invoke it.

Do I pay tax in India on my foreign stipend?

Usually not, if you are a non-resident of India for that financial year. India taxes a non-resident only on India-source income, so a foreign stipend or wage earned abroad falls outside India’s tax net in a year you have spent fewer than 182 days in India and left for study or work. The exception is your fly-out year, when you may still be a resident and the income could be taxable in India, with a foreign tax credit available to prevent double taxation.

How does the foreign tax credit work?

The foreign tax credit lets you reduce your Indian tax on income that India is also taxing, by the amount of tax you already paid on it abroad. It applies only in a year you are a resident of India (or RNOR with foreign income in India’s net). You claim it by filing Form 67 on the e-filing portal before or with your ITR, attaching proof of the foreign tax paid, under Rule 128 read with the relevant DTAA article. Non-residents generally have no FTC question.

When do I become a non-resident for Indian tax?

You generally become a non-resident for a financial year (1 April to 31 March) if you are physically present in India for fewer than 182 days during that year, having left for employment or study abroad. Indian tax residency is based on day count under Section 6, not on citizenship. The year you fly out is the one to watch, because pre-departure days in India can keep you a resident for that first year. From the next full year abroad, non-resident status usually applies.

What is a Tax Residency Certificate (TRC)?

A TRC is a document issued by the tax authority of your host country certifying that you are a tax resident there. India can ask for it when you claim DTAA benefits, to confirm the treaty applies to you. Where the TRC lacks certain particulars, India may also require Form 10F to supply the missing details. Most students who are clean non-residents with only a small foreign wage never need a TRC, because they are not invoking the treaty in an Indian return.

What is Form 67 and when do I file it?

Form 67 is the online statement you file on the Income Tax e-filing portal to claim a foreign tax credit, declaring your foreign income and the foreign tax paid on it. You file it before or along with your Indian ITR for the relevant year, with proof of the foreign tax attached. It is required only when you are a resident of India and claiming credit for foreign tax. Without Form 67, the system can deny the credit even when the DTAA clearly permits it, so it is essential, not optional.

Does the student article in a DTAA make my campus wages tax-free?

Usually not. The student or trainee article in most DTAAs exempts money you receive from sources outside the host country for your maintenance and education, meaning remittances from home and scholarships sent from India. It generally does not cover wages you earn from a job inside the host country. A campus job, internship, or OPT salary is locally earned income taxed under the host country’s normal rules, though often at a low or zero rate after the local personal allowance.

What is the RNOR status when I return to India?

RNOR stands for Resident but Not Ordinarily Resident, a transition status you usually pass through when you return to India after years abroad. During the RNOR window, India does not tax your foreign income unless it is derived from a business controlled or profession set up in India, giving you time to bring overseas savings home before full worldwide taxation begins. Timing your return and day counts can extend this benefit across more than one financial year, which is worth planning carefully.

Faz · The Honest Journey · 2026