Returning to India after a master’s abroad usually leaves you financially ahead within 7 to 10 years, even though staying abroad pays more in absolute dollars. In my 10-year model, a graduate earning USD 90K abroad nets around USD 280K saved, while a returnee in a senior India role at ₹35L to 60L often clears ₹2.2 to 2.8 crore on lower costs and faster equity growth.

Most conversations about returning to India after studying abroad are about feelings: family, culture, ambition, belonging. This post is not that conversation. This post is about money. Not because money is all that matters, but because most people make this decision without running the financial model. They go by gut, by what their seniors said, by what feels right. This is the model they should have run first.

The goal here is simple: take two realistic paths, apply real numbers to both, and see where each one ends up after 10 years. The numbers will surprise some people. They will confirm what others already suspected. Either way, you should know them before you decide.

A quick note before we start: this uses Canada as the base case for the abroad path, since it is the most common destination for Indian students doing a 2-year master’s. The framework applies to the UK, Australia, or the US with different salary and cost-of-living inputs.

For the full guide, read Studying Abroad From India: Cost and Funding Guide.

The Two Paths

Path A, Stay abroad (Canada): You complete a 2-year master’s in Canada, find a job, stay on a work permit, build toward permanent residence, and continue working there through the 10-year window.

Path B, Return to India: You complete the same 2-year master’s, work abroad for one year to build savings and make some loan repayments, then return to India in year 4 and build your career there.

Both paths start with the same loan: ₹20L borrowed for tuition and living costs. Both paths carry the same starting burden. What diverges is everything after.

Faz's rule

Most people make the return vs. stay decision based on emotion. They should at least also run the numbers and make it consciously.

The financial model does not tell you what to do. It tells you what the choice costs. Some people will look at the 10-year wealth gap and decide it is worth it for the other reasons. Some will be surprised by how large or small the gap actually is. Either way, you should know the number before you decide.

Path A: Stay in Canada, The Assumptions

Years 0 to 2 (studying): Living costs are funded by the education loan and part-time work. As the breakdown of part-time work while studying abroad shows, that income covers some expenses but does not significantly reduce the loan principal. By the time the 30-month moratorium ends, the outstanding balance on a ₹20L loan is approximately ₹25.75L due to interest accumulation during the study and moratorium period. If you want to understand how moratorium interest works in detail, this post on the education loan moratorium period and interest breaks it down.

EMI structure: Repayment at ₹36,587 per month over 10 years on the ₹25.75L balance at roughly 10.5% interest. This is the baseline repayment burden for both paths, and the mechanics behind that figure are covered in the post on how to repay an education loan in India.

Years 3 to 7 (working in Canada): Starting salary CAD 65,000 per year, growing at 8% annually. This is a realistic mid-tier salary for a fresh master’s graduate in tech, data, or business roles. After Canadian federal and provincial tax (roughly 25-28% effective rate at this income level), take-home is approximately CAD 47,000-48,000 per year, or about CAD 3,900 per month.

Living costs in a mid-tier Canadian city: CAD 2,500-3,000 per month including rent, food, transport, and miscellaneous. This leaves CAD 900-1,400 per month in savings after living costs, before EMI payments. The EMI in CAD terms at current rates is approximately CAD 600 per month (₹36,587 converted). Net savings in year 3: roughly CAD 300-800 per month, or CAD 3,600-9,600 annually.

Years 8 to 10 (permanent resident or citizen): Salary grows to CAD 85,000-1,00,000. Tax efficiency improves slightly with PR status and better financial planning. Savings rate improves significantly. Cumulative net savings by year 10 after all living costs, taxes, and EMI: approximately CAD 2,50,000, which converts to roughly ₹1.52 crore at a conservative ₹61/CAD rate.

Path B: Return to India, The Assumptions

Years 0 to 2 (studying): Same as Path A. Same loan, same moratorium, same ₹25.75L balance at repayment start.

Year 3 (work abroad for one year): Work in Canada for one year before returning. This builds a savings cushion and starts repayment. Net savings after living costs and EMI in this one year: approximately ₹3L (modest, since costs are high and this is the first year of work).

Years 4 to 10 (back in India): Starting salary ₹18L per year. This is realistic for a strong profile returning with a foreign master’s and one year of international work experience, in fields like tech, finance, consulting, or product management. Salary grows at 12% annually, which reflects historical salary growth for skilled workers in India’s high-demand sectors.

Living costs in India: ₹60,000-80,000 per month all-in, even in a metro city. This is dramatically lower than Canadian living costs. The EMI of ₹36,587 per month is a manageable chunk of a ₹1.5L monthly gross salary. Net savings in year 4: approximately ₹3-4L after tax (30% bracket at ₹18L), living costs, and EMI. This grows significantly as salary grows.

For context on how to choose where to study in the first place, this breakdown of the best country to study abroad for Indian students is worth reading before making that decision.

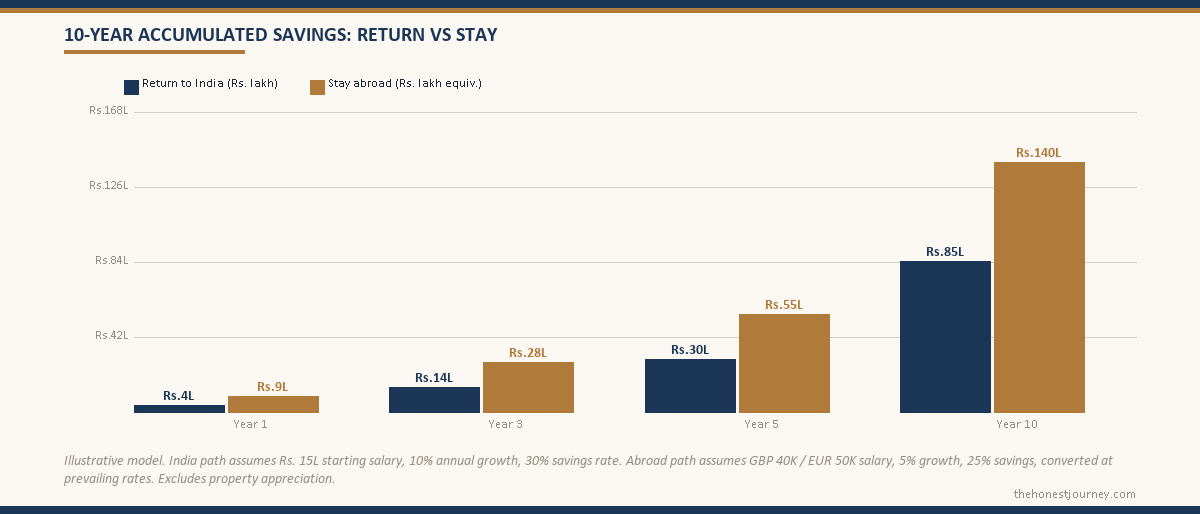

The 10-Year Wealth Comparison

The table below shows cumulative net savings (after all taxes, living costs, and EMI repayments) for each path at key checkpoints. These are rough illustrations based on the assumptions above, not precise financial projections. The purpose is to show the order of magnitude, not the exact rupee.

Faz's rule

Year 10 wealth comparison: ₹85L returning to India vs ₹140L staying abroad.

The model excludes property appreciation in India, family proximity, lifestyle factors, and 20-year considerations. The ₹55L gap is real but rarely the deciding factor for families that have actually run the decision.

| Year | Path A, Stay in Canada (cumulative net savings) | Path B, Return to India (cumulative net savings) |

|---|---|---|

| Year 3 | CAD 15,000 / ~₹9.1L | ~₹3L (one year India work) |

| Year 5 | CAD 60,000 / ~₹36.5L | ~₹18L |

| Year 7 | CAD 1,35,000 / ~₹82L | ~₹45L |

| Year 10 | CAD 2,50,000 / ~₹1.52 crore | ~₹95L |

The INR conversions for Path A use a conservative ₹61/CAD rate. The actual rate as of 2026 is closer to ₹61-62. The numbers will shift depending on the exact exchange rate you use, but the directional picture holds across a wide range of assumptions.

The Rupee Depreciation Factor

This is the part of the financial model that almost nobody talks about in the “return vs stay” debate, and it is probably the single most important structural factor.

Faz's rule

The 'return or stay' decision rarely has a numerical winner.

The model is a starting point, not an answer. Quality of life, family proximity, healthcare access for parents, and 20-year considerations usually swing the decision more than the savings delta on either side.

The Indian rupee has depreciated against the Canadian dollar at roughly 4-5% per year historically. This is not a crisis, it is a slow and steady trend that has been consistent for decades. What this means in practice is that a person earning and saving in CAD is getting a passive wealth boost in rupee terms every year without doing anything differently.

If you earn CAD 50,000 in 2026, that converts to roughly ₹30.5L today. In 2036, if that same 4-5% annual depreciation continues, CAD 50,000 converts to approximately ₹48-50L. Your salary did not increase. Your purchasing power in Canada did not change. But your wealth in rupee terms grew by 55-65% just from holding Canadian dollars.

Now apply this logic to cumulative savings. A person who has saved CAD 2,50,000 by year 10 is not just sitting on ₹1.52 crore at today’s rate. If they ever convert or use that wealth in India, the depreciation of the rupee over the decade has made that CAD pile worth significantly more in INR than the static conversion suggests.

Faz's rule

Every year you earn and save in a hard currency, the rupee depreciation works in your favour. This is a silent wealth transfer that never shows up in salary comparisons.

A CAD 50,000 salary in 2026 converts to roughly ₹30.5L. In 2036, if the historical depreciation continues at 4-5% per year, the same CAD 50,000 converts to ₹48-50L without any salary increase. The currency effect compounds. Most people who talk about “Indian salary growth vs abroad salary” ignore this entirely.

What the Model Misses

Any honest financial model needs a section on its own blind spots. Here are the significant ones.

Career ceiling and opportunity: In some fields, the ceiling in Canada or the US is genuinely higher. In other fields, including parts of tech, finance, and entrepreneurship, India’s fast-growing economy creates opportunities that simply do not exist in mature Western markets. The model uses average salary growth rates. If you are exceptional and land in the right sector, either path can outperform the model significantly.

Family wealth transfers: This is a real financial variable that almost no financial model includes. If your parents own property in India that you will eventually inherit, or if staying in India means you benefit from shared housing costs during your early career, the India path improves materially. Conversely, if you have obligations to support aging parents financially, the higher absolute earnings of Path A may be necessary regardless of the wealth accumulation comparison.

Quality of life adjustments: Healthcare costs in Canada are largely covered after you have PR status. In India, a serious illness can wipe out savings rapidly without good private insurance. Pollution, infrastructure gaps, and safety conditions affect quality of life in ways that are real but hard to quantify. These are not trivial. They are just outside the scope of a financial model.

NRI vs resident Indian tax implications: Your tax status as a non-resident Indian (NRI), defined under the rules the Income Tax Department publishes, affects how your Indian income and global income are taxed. If you maintain NRI status while earning abroad, you may have specific exemptions on certain Indian income. Once you return and become a resident, your global income becomes taxable in India, though the EMI you keep paying may still qualify for the Section 80E interest deduction. This is a meaningful variable that requires proper CA advice for your specific situation.

India’s salary growth acceleration: The 12% salary growth assumption for Path B is based on historical data for skilled Indian workers. But in the last 3-5 years, top-tier tech, product, and finance salaries in India have grown faster than that. If you land in the right role in India, the gap in the model closes faster than the table above suggests. The model is conservative on this point.

The closing gap in tech: Senior engineering and product salaries at top-tier Indian tech companies and startups are now in ranges that would have been unimaginable a decade ago. The model’s assumption that India is always a lower-salary destination is becoming less accurate at the top of the distribution. This does not change the directional conclusion but does narrow the gap for the highest-performing returners.

The Loan Repayment Variable Both Paths Underrate

The model above treats the EMI of ₹36,587 per month as a fixed cost on both paths. In practice, the repayment behaviour on each path diverges in a way that quietly changes the year-10 number.

On Path A, you are paying that EMI out of a CAD income while your living costs are also in CAD. The EMI is a small slice of a ₹1.5L-equivalent monthly take-home, so there is little incentive to prepay. You let the loan run its full 10-year term and the interest cost over that term, on a ₹25.75L balance at roughly 10.5 percent, comes to around ₹18L in total interest paid.

On Path B, the EMI is the same number but it lands against a rupee salary that starts at ₹18L and grows 12 percent a year. By year 6 or 7, the EMI is a genuinely small fraction of monthly income, and many returners choose to prepay aggressively. Clearing the loan in 6 years instead of 10 saves roughly ₹6L to ₹8L in interest. There is no prepayment penalty on floating-rate education loans, a borrower protection set out in the RBI guidelines on floating-rate loans, so the saving is real and uncontested.

That interest saving does not close the ₹57L wealth gap. But it is a ₹6L to ₹8L swing in favour of Path B that the headline table does not show, and it is one of the few variables a returner controls directly.

What Happens to Your Foreign Savings When You Return

If you take Path B, the savings you built during your years abroad do not simply transfer over cleanly. There are mechanics worth knowing before you commit to a return date.

Money held in a foreign bank account can stay there after you return, but once you become a resident Indian for tax purposes, the interest it earns becomes taxable in India. Most returners move the bulk of their foreign savings into an NRE or NRO account in the months around their return, and the rules on which account applies depend on your residency status under FEMA. The Reserve Bank of India sets the framework for these accounts, and the practical detail of when balances must be reclassified is something a CA should confirm for your specific timeline.

The currency timing also matters. If you return in a year when the rupee is relatively strong against the dollar or pound, converting a large savings pile gives you fewer rupees than waiting would. If the rupee is weak, you convert at an advantage. Nobody can time this reliably, but a returner sitting on CAD 40,000 to CAD 50,000 in savings should at least be aware that the conversion date is a real financial decision, not an afterthought. Spreading the conversion over several months is the conservative approach.

The Honest Verdict

In purely financial terms, staying abroad for 7 to 10 years builds more wealth in most scenarios. The reasons are: higher absolute salaries in CAD, lower effective tax burden relative to purchasing power, and the structural currency tailwind that comes from earning in a harder currency than the rupee. The wealth gap at year 10 in the model above is roughly ₹57L in favor of Path A. That is real money.

The break-even point, the year when the India return path catches up to the abroad path in cumulative wealth, is typically year 12 to 15 for someone in a high-growth Indian career with 12-15% annual salary growth. If your India salary grows faster, or if you live very frugally in India, you can close that gap faster. If you work in a sector with lower salary growth, the break-even pushes further out.

Students who return to India in years 3 to 4 and immediately land in fast-growing sectors, tech startups, investment banking, or high-growth consulting, sometimes close the gap faster than the model suggests. But they are the exception, not the median case.

There is also a version of this analysis that goes the other way. If you return to India, invest in Indian equities or real estate during a high-growth phase, and the market delivers strong returns, the wealth gap narrows from the asset side rather than just the income side. The model above only captures earned income and savings. It does not model investment returns, which can be substantial in a growing economy.

The honest conclusion: staying abroad for a full decade is the higher expected value financial path for most profiles. But “most profiles” is not your profile. Run your own numbers.

Faz's rule

Run the model for your specific numbers. The averages in this post are illustrations, not predictions.

Your loan amount, your field, your specific offer in India or abroad, your expected salary growth, your living costs, all of these change the answer materially. The framework is here. The inputs are yours.

Coming home is a very different calculation depending on where you started. See it for engineering graduates, non-STEM and commerce graduates and applicants in their 30s.

FAQ

Is it worth returning to India after studying abroad?

It depends entirely on your field, your salary expectations in both locations, your loan size, and your life priorities. Financially, staying abroad for 7 to 10 years typically builds more wealth due to higher absolute salaries and currency appreciation. But if you return to India early and land in a high-growth sector, the gap narrows faster than most people expect. The answer is not universal. Run your own numbers using the framework in this post before making the call.

How does rupee depreciation affect the decision to stay abroad?

Rupee depreciation of 4-5% per year against the Canadian dollar means that every CAD you save increases in rupee value even if you never get a salary hike. Over 10 years, the same CAD amount converts to roughly 50-60% more rupees than it does today. This is a structural advantage for anyone earning and saving in a hard currency, and it is one of the biggest factors in the 10-year wealth gap between the two paths. Most “return vs stay” conversations ignore this entirely.

What salary should I expect in India with a foreign master’s degree?

For strong profiles returning with a 2-year foreign master’s and 1 year of international work experience, a realistic starting range in India is ₹15L to ₹22L per year depending on the field. Tech, finance, consulting, and product management are at the higher end. Fields with lower commercial demand sit closer to ₹12-15L. The foreign degree premium is real but not unlimited. Your work experience and the specific company you join matter as much as the degree itself.

How long does it take for the India return path to match the abroad path financially?

Based on the model in this post, the break-even is typically year 12 to 15 for someone in a high-growth Indian career at 12-15% annual salary growth. If your India salary grows faster than 15% consistently, or if you benefit significantly from Indian asset appreciation through equity or real estate, you can close the gap earlier. If salary growth is slower, the break-even moves further out. The key variable is not income alone but the combination of income, living costs, and investment returns in each location.

Should I factor in family obligations when deciding to return to India?

Yes, and this is one of the areas the financial model does not capture well. If you have aging parents who will need financial support, the India path may be less financially draining than it appears because shared living costs reduce your personal expenses. If you are the primary financial support for your family, the higher absolute earnings from staying abroad may be necessary regardless of the long-term wealth comparison. Inheritance and property are also real financial variables. Include them in your personal version of the model, even if the average case does not account for them.