If you return to India after studying and working abroad, you usually qualify as RNOR (Resident but Not Ordinarily Resident) for 2 to 3 financial years, and during that window your foreign salary, foreign interest, and foreign capital gains are not taxed in India. NRE interest stays tax free as long as you hold RNOR or NRI status, but NRE and FCNR accounts must be converted to resident accounts within a reasonable time of return under FEMA. Get the account conversion and the RNOR claim right in your first return filing or you lose a window worth several lakh.

The flight back is easy. The tax-status part is what nobody briefs you on. One day you are an NRI with a dollar salary and an NRE account earning tax free interest. The next day you are a returning resident, and the Income Tax Act has very specific rules about the gap.

This is the structural map I wish someone had given me before I returned. Not tax advice. Just the rules, so you walk into a CA knowing what to ask.

What changes the moment you land

Indian tax residency is decided by Section 6 of the Income Tax Act. It does not care about your passport or how you feel about home. It cares about days spent in India in a financial year (1 April to 31 March) and in the preceding 4 and 7 financial years.

The basic Section 6(1) tests: 182 days or more in the current year, OR 60 days or more this year AND 365 days or more across the preceding 4 years. If you arrive back in August, you cross 182 days that year and become Resident.

That is where RNOR enters. Section 6(6) carves out Resident but Not Ordinarily Resident. You qualify if either: you were Non-Resident in 9 of the 10 preceding financial years, OR you were in India for 729 days or less in the preceding 7 financial years. For most students who went abroad for a 2-year master’s and stayed on for 2 to 4 years of work, both tests are usually met for 2, sometimes 3, financial years after return. That is your RNOR window. The most valuable tax status you will ever hold.

Why RNOR is worth several lakh in tax

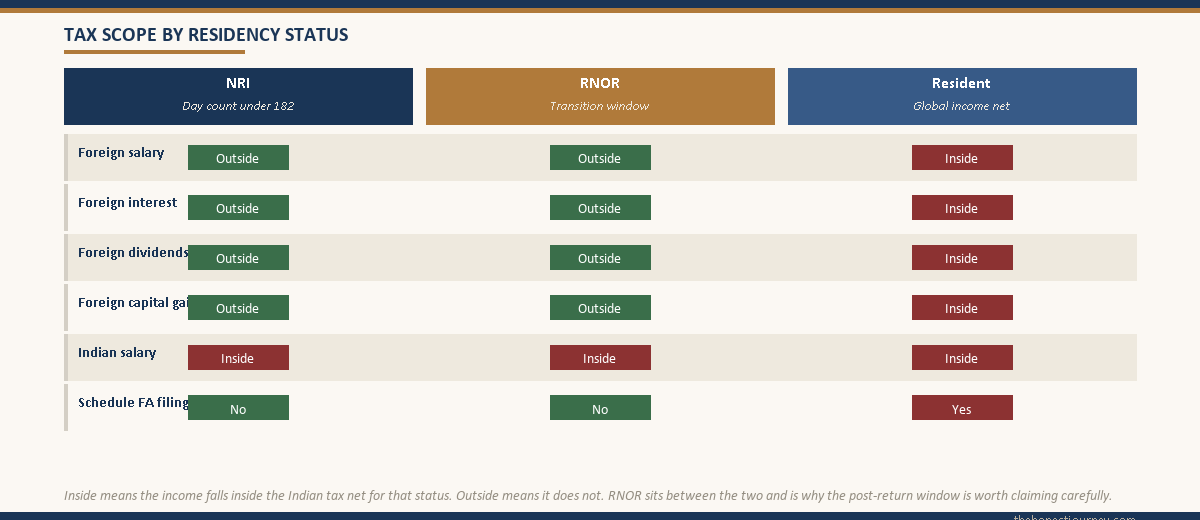

An ordinary Resident is taxed on global income: Berlin salary, US dividends, Singapore deposits. All taxable in India with a DTAA credit for tax paid abroad.

An RNOR is taxed only on income received in India, accrued in India, or from a business controlled from India. Foreign salary, foreign interest, foreign dividends, foreign capital gains, all outside the Indian tax net during RNOR years.

Here is the picture in numbers. A returning student holds $80,000 (about ₹66 lakh) in a US brokerage paying $2,000 dividends annually, ₹40 lakh in an NRE FD at 7% (₹2.8 lakh interest), and earns ₹35 lakh from an Indian employer joined in October.

| Income source | Under RNOR | Under ordinary Resident |

|---|---|---|

| Indian salary (Oct to Mar) | Fully taxable in India | Fully taxable in India |

| NRE FD interest (₹2.8L) | Tax free (account-status rule) | Tax free until status changes |

| US dividends ($2,000 / ~₹1.65L) | Not taxable in India | Fully taxable, DTAA credit for US withholding |

| US brokerage capital gains | Not taxable in India | Taxable as foreign LTCG/STCG |

| Foreign 401(k) or pension growth | Not taxable in India | Taxable on withdrawal (rules vary) |

For a meaningful US or Europe portfolio at return, RNOR saves ₹1 to ₹4 lakh per year in tax, more if liquidating a brokerage. You have to claim it in your ITR and keep evidence (passport stamps, day count, employer letters) ready.

Faz's rule

RNOR is not automatic in the sense that you can ignore it. You have to claim it in your ITR and back it with day counts.

Most returning students file their first ITR as ordinary Resident because their CA was not briefed on the prior 10 years of residency history. Walk in with your passport pages copied and a clean Excel sheet of India days for each of the last 7 years. That one sheet is the difference between paying tax on your global income and not.

NRE, NRO, and FCNR accounts: what changes on return

FEMA (Foreign Exchange Management Act) sits on top of the Income Tax layer. The account rules are FEMA’s domain. The tax on interest is the IT Act’s domain. They overlap but they are not the same.

Three account types you most likely hold:

- NRE (Non-Resident External): rupee account, fully repatriable, interest is tax free in India as long as the holder is a non-resident under FEMA.

- NRO (Non-Resident Ordinary): rupee account for Indian-source income (rent, dividends, inheritance), interest is taxable in India, TDS at 30% applies for non-residents.

- FCNR (Foreign Currency Non-Resident): term deposit in foreign currency (USD, GBP, EUR, etc.), interest is tax free in India while the holder is a non-resident under FEMA.

The day you return to India with intent to stay, your FEMA residency changes to Resident in India. This is independent of your Income Tax residency (decided by day count). The account rules update on the FEMA timeline.

What you are supposed to do:

- Inform your bank of the change in residential status.

- Convert NRE savings accounts to Resident Rupee accounts.

- NRE term deposits can usually run to maturity, but interest becomes taxable once you are a FEMA resident. Confirm treatment with your branch.

- NRO savings and term deposits get redesignated as Resident accounts.

- FCNR deposits can be held till maturity at the contracted rate. After maturity, convert to RFC (Resident Foreign Currency), the residence-equivalent allowed for returning Indians.

RFC is the underused tool. If you return with foreign currency balances and want to keep them in foreign currency (for travel, future foreign education for kids, foreign investments), RFC lets you do that legally as a resident. Interest is taxable once you are an ordinary Resident, but during RNOR can be exempt under Section 10(15)(iv)(fa) subject to its conditions.

Faz's rule

The bank does not chase you to convert accounts. The penalty when they catch up to it is yours, not theirs.

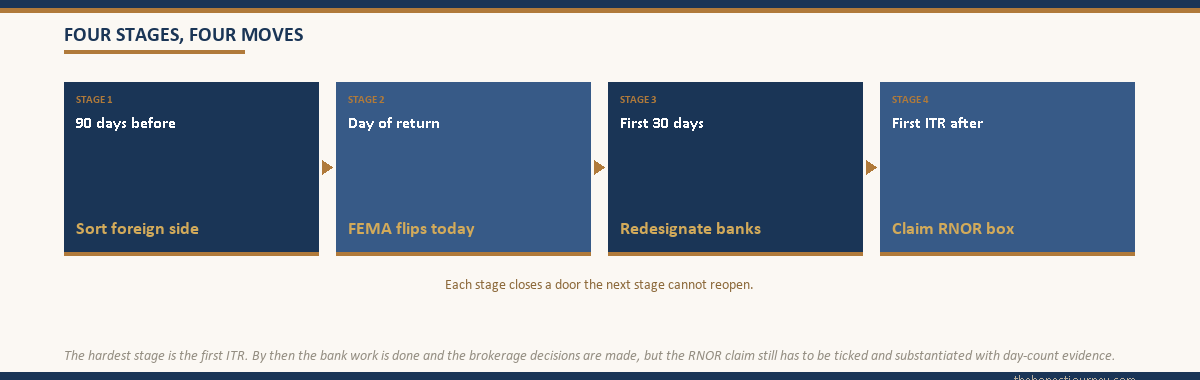

Walk into the branch with your passport, return ticket, and a letter declaring you are now a resident under FEMA. Get the redesignation done within 90 days of arrival. The interest accrual treatment, the TDS reset, and the future repatriation flexibility all hinge on this single piece of paperwork that no one will remind you to do.

What to do BEFORE you return

The single biggest tax-planning move happens before you board the plane. Once you become a FEMA resident, certain foreign-investor-only accounts become off limits or administratively heavy. Sort the foreign side while you still have non-resident status.

A practical pre-return checklist, ideally 60 to 90 days out:

- Decide on your foreign brokerage. Many US brokerages will not let you trade actively once your address is non-US. Some allow sell-only. Some close the account. Decide whether to liquidate (realising gains while you are NRI), transfer to an India-friendly broker like IBKR, or hold and not trade.

- Plan large capital gains. If you have appreciated stock or vested RSUs you planned to sell, selling before return realises the gain while you are NRI and India does not tax it. Selling after return during RNOR is also generally outside the Indian tax net. Selling as an ordinary Resident pulls it fully into Indian tax.

- Handle 401(k) or equivalent intelligently. US treats early withdrawal with a 10% penalty plus income tax. Indian treatment of foreign retirement accounts was recently clarified under Section 89A. Get specific advice, do not improvise.

- Open NRE, NRO, and FCNR accounts BEFORE return if you do not have them. Once a FEMA resident, you cannot open new NRE accounts. The door closes.

- Move money you want to repatriate while NRE is still active. NRE funds are freely repatriable. NRO is repatriable up to USD 1 million per financial year with documentation. Getting foreign earnings into NRE before status change keeps repatriation simple.

- Document your day count. Spreadsheet every entry and exit from India for the last 8 financial years against passport stamps. This is the evidence pack for your RNOR claim, much harder to assemble later from memory.

The tax filing year you return: practical mechanics

In the financial year you return, your status is almost always Resident (you will cross 182 days if you returned in the first half). You file ITR-2 or ITR-3 depending on income sources. You tick the RNOR box in the residential-status section. Ordinary Residents must disclose foreign assets in Schedule FA, but RNOR holders are not required to. Another reason the RNOR claim matters.

Schedule FA for ordinary Residents lists every foreign bank account, brokerage holding, signing authority. Non-disclosure attracts punitive Black Money Act penalties. Once RNOR ends, Schedule FA becomes mandatory.

The DTAA between India and most destinations (US, UK, Germany, Canada, Singapore) ensures no double tax once you are an ordinary Resident. The credit method applies: India taxes the income and credits tax paid abroad up to the Indian liability. The mechanics live in Form 67, filed via the income tax e-filing portal before the ITR due date. Miss Form 67 and you can lose the credit.

For broader return planning, see return to India after studying abroad. Funding context is in how to fund study abroad and TCS on education loan India. The should-I-go framing: is studying abroad worth it.

Faz's rule

Spend the RNOR window doing the asset rearrangement that becomes expensive later.

Sell appreciated foreign holdings, move foreign cash you do not need into India, restructure foreign retirement accounts, gift to family members in lower tax brackets. The two years where global income is outside the Indian net is when you make the moves that an ordinary Resident pays full tax to make. Wasted RNOR years are years of avoidable tax in years three, four, five onward.

The common mistakes that cost the most

I have watched friends make the same handful of errors. None about being clever. All about not knowing the rules existed.

Not claiming RNOR in the first ITR. The CA defaults to Resident because that is the easy box. Tax gets paid on global income, the RNOR window quietly expires unused. Revised returns under Section 139(5) can fix it within the allowed window, but most people realise the mistake too late.

Not converting bank accounts. An NRE account held by a FEMA resident is a violation. The interest continues paying tax free in error until a KYC refresh reclassifies the account, claws back the wrong treatment, and creates an audit hassle. Redesignate within 90 days.

Triggering Indian tax on foreign retirement accounts. A 401(k) cashout in the year of return is one of the costliest accidental moves. Get specific advice on Section 89A relief and the withdrawal mechanics.

Forgetting Form 67. Income taxed abroad in a year you file as Resident requires Form 67 before the ITR due date or the foreign tax credit can be disallowed.

Ignoring Black Money Act disclosure once RNOR ends. Schedule FA must list every foreign asset, account, signing authority. Penalty for non-disclosure is ₹10 lakh per asset per year plus prosecution exposure. Track when your RNOR window ends.

Faz's rule

The Black Money Act penalty for missed Schedule FA disclosure is ₹10 lakh per asset per year. Plus prosecution exposure.

The day your RNOR window ends, the disclosure switch flips. The foreign brokerage you forgot to close, the small dollar savings account you stopped logging into, the old employer ESPP, all of them must show up in Schedule FA. Calendar the date your RNOR ends and brief your CA two months ahead.

The honest closing take

RNOR exists because the drafters of Section 6 understood returning Indians need a transition window. Not a loophole, not aggressive planning. The statute working as intended. The tragedy is that most students who could benefit never claim it, because the consultancy that helped them go abroad does not advise on coming home, and the CA filing the first Indian ITR does not ask about the previous decade.

If you take one thing from this post: build the day-count spreadsheet now. Save boarding passes, photograph passport stamps, log every entry and exit. That hour is worth lakhs.

Second: do the asset rearrangement while RNOR holds. The window closes faster than you expect. Refer to the official ITR guidance on residential status when you sit with your CA. Use the window.

FAQ

What is RNOR status and how do I qualify?

RNOR (Resident but Not Ordinarily Resident) is a sub-category of Indian tax resident defined under Section 6(6) of the Income Tax Act. You qualify if you are a resident in the current year (usually because you stayed 182 days or more in India) AND you were either a non-resident in 9 out of the 10 preceding financial years, or you were in India for 729 days or less in the preceding 7 financial years. Most returning students who spent 4 or more years abroad satisfy this test for at least 2 financial years after their return.

How long can I claim RNOR after returning to India?

Typically 2 to 3 financial years. The exact length depends on your day count history. If your departure was clean (you left in your early twenties and stayed abroad for 4 plus years), you will usually get the full 2 to 3 years. If you visited India often during your time abroad, the 729-day test in the preceding 7 years may fail earlier and reduce the window. Build a precise day-count spreadsheet to know exactly which years qualify.

Do I pay tax in India on foreign salary as RNOR?

No, foreign salary earned and received abroad is not taxable in India during your RNOR years, provided the services were rendered abroad and the income was not received in India. Foreign interest, foreign dividends, and foreign capital gains are also outside the Indian tax net during RNOR. Only income received in India, accrued in India, or from a business controlled from India is taxable. Indian salary from an Indian employer after you return is fully taxable.

What happens to my NRE account when I return to India?

Under FEMA, you become a resident from the day you return with intent to stay. Your NRE savings account must be redesignated as a Resident Rupee account. NRE term deposits can usually be held to maturity at the contracted rate, but their tax treatment changes once you are a FEMA resident. The interest that was previously tax free becomes taxable. Inform your bank within a reasonable time of return (commonly 90 days) and get the redesignation done in writing.

Do I need to close my NRO account?

No, you do not close it, you redesignate it. The NRO account holds Indian-source income (rent, dividends, inheritance) and once you become a resident, the bank converts it to a Resident Rupee account. The balance and the account number often remain, only the status flag changes. TDS treatment shifts from the 30% non-resident rate to the regular slab-based treatment with TDS only above the prescribed thresholds.

Can I keep my FCNR deposit after returning?

Yes, you can hold an FCNR term deposit to maturity at the contracted rate even after becoming a resident. After maturity, you can convert it to an RFC (Resident Foreign Currency) account, which is the resident-equivalent and is designed for returning Indians. RFC allows you to hold foreign currency in India, repatriate it for foreign travel or investment, and keep the balance outside the rupee. Interest is tax free during your RNOR window under Section 10(15)(iv)(fa) subject to its conditions.

Does DTAA help returning NRIs?

DTAA matters most once you become an ordinary Resident, because that is when India taxes your global income and the credit for tax paid abroad becomes essential. During RNOR, foreign income is generally not taxable in India, so DTAA credit is not relevant. Once RNOR ends, Form 67 must be filed before your ITR due date to claim the foreign tax credit. Missing Form 67 can disallow an otherwise legitimate credit, so build it into your ITR workflow.

What if I do not claim RNOR in my first ITR after return?

You file as ordinary Resident, pay tax on global income, and lose the benefit of the year. You can file a revised return under Section 139(5) within the time allowed (currently up to 31 December of the assessment year, subject to amendments), and reclaim RNOR if you can substantiate it with day-count evidence. Outside that revision window, the benefit for that year is lost. This is the single most common and costly mistake returning students make, and it is preventable by briefing your CA upfront with your residency history.

Faz · The Honest Journey · 2026