Studying abroad is worth it when three things line up: a real post-study work route, a job that clears the loan EMI inside three to four years, and funding that does not break the family. The all-in cost of a typical loan-funded master’s lands between ₹50 lakh and ₹95 lakh. When any one fails, it usually is not worth it.

The consultant showed your parents a slide. It had a number on it, the average salary of an international graduate, and it was big. What the slide did not have was the loan EMI, the two years some graduates spend looking for a job that sponsors a visa, or the family that sold a flat to fund a degree that never paid for itself. The number on the slide was real. It was just not the whole story.

Large numbers of Indians go overseas to study every year, a trend the Ministry of External Affairs tracks through its data on Indian students abroad. This post asks a blunt question: is studying abroad worth it for Indian students? Not the inspirational version. The version with the actual arithmetic, three real outcomes, and a yes/no test you can run yourself before you sign anything.

Studying abroad is worth it for Indian students when three things line up: the destination has a genuine post-study work route, the course leads to a job that clears the loan EMI inside three to four years, and the total cost is funded without breaking the family’s retirement security. When any one of those fails, it usually is not worth it, and most of the regret stories fail on the third.

For the full guide, read Should I Study Abroad? The Honest Decision Guide.

The honest ROI math, start to finish

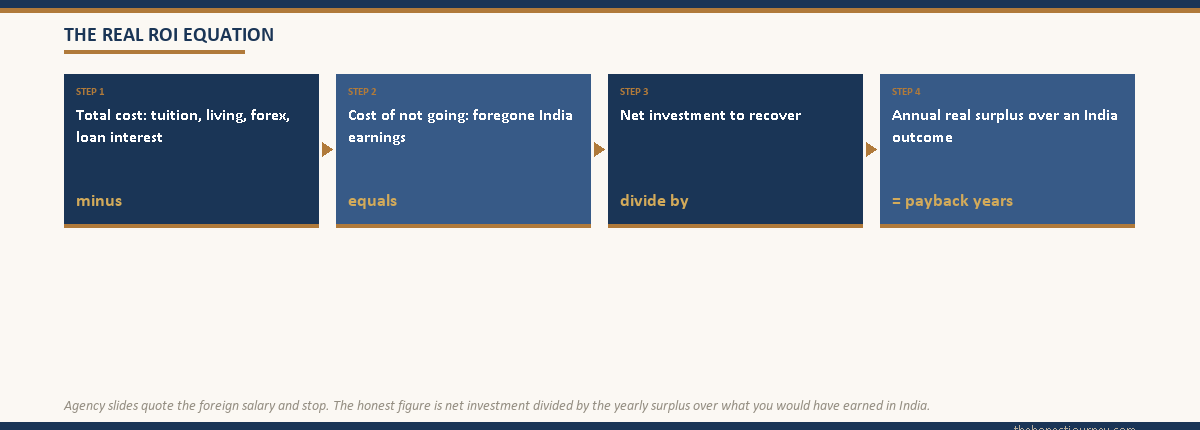

Return on investment for a degree abroad is not the salary you earn. It is the salary you earn minus what that same person would have earned staying in India, minus the full cost of going. Most agency pages quote the first number and stop. Here is the full calculation.

The cost side. A two-year master’s in a mid-tier destination runs roughly like this. Tuition ₹18 lakh to 45 lakh depending on country and university. Living costs ₹12 lakh to 24 lakh across two years. Forex markup, visa, insurance, flights and the TCS on remittances above the annual threshold, sent under the RBI Liberalised Remittance Scheme, add another ₹3 lakh to 6 lakh. If the bulk is funded by a loan at 11% to 12.5%, interest over a ten-year tenure adds ₹14 lakh to 22 lakh. Total all-in cost for a typical loan-funded master’s lands between ₹50 lakh and 95 lakh.

The “cost of not going” side. This is the number nobody calculates. A capable graduate from a tier-1 Indian college, or even a sharp one from a tier-2 college with two years of work experience, is not earning zero. They might be on ₹8 LPA to 18 LPA in India. Over the same period the abroad student spends studying and job-hunting, the stay-home version of that person is earning, saving and compounding. That foregone income is a real cost of going, and it can run ₹20 lakh to 40 lakh across three years.

The return side. The honest return is the gap between the abroad salary (after tax, after cost of living in that country) and the realistic India salary, sustained long enough to clear the cost. A graduate earning the equivalent of ₹45 LPA gross abroad is not ₹45 lakh better off. After higher taxes and far higher rent and groceries, the real surplus over an India outcome might be ₹12 lakh to 20 lakh a year. That surplus is what pays back the ₹50 lakh to 95 lakh.

Three real outcomes: success, neutral, struggle

Averages hide everything that matters. Here are three anonymised real cases, same starting question, three different endings.

The success. A 23-year-old engineer from a tier-1 college, two years of work experience, did a one-year master’s in a STEM field in a country with a three-year post-study work visa. All-in cost about ₹38 lakh, half funded by a collateral-backed loan at 9.5%. She landed a job four months after graduating at the equivalent of ₹52 LPA gross. After tax and living costs her real annual surplus over what she would have earned in India was around ₹16 lakh. She cleared the loan in just under four years and stayed on. For her, studying abroad was clearly worth it.

The neutral. A 24-year-old from a tier-2 college, no work experience, did a two-year master’s in a business field in a popular destination. All-in cost about ₹62 lakh, mostly loan-funded at 11.75%. He found a job nine months after graduating, not in his field, paying the equivalent of ₹34 LPA gross. The EMI was manageable but tight. After three years he returned to India and joined a role at ₹19 LPA, helped by the international degree and English fluency. He broke roughly even. The degree did not lose money, but a sharp domestic MBA might have reached the same ₹19 LPA without the ₹62 lakh outlay.

The struggle. A 25-year-old from a tier-3 college did a two-year master’s in a generic management program at a low-ranked private university, chosen because the consultant said admission was “guaranteed.” All-in cost about ₹55 lakh, funded by an unsecured loan at 13.5% plus the family liquidating a retirement FD for the margin money. The post-study job market in that field was saturated. He worked part-time roles, never found a sponsored full-time job, and returned to India after his visa lapsed. He is now repaying a ₹38,000 EMI on a salary that barely covers it. For this family, studying abroad was not worth it, and the deciding factor was not effort. It was the course, the college tier and the funding structure.

Faz's ruleThe destination and the course tier decide the outcome far more than how hard the student works.

All three of these people were capable and willing. The success picked a STEM field in a country with a real work visa. The struggle picked a generic program at a college nobody hires from. Effort did not separate them. The choice made before they boarded the flight did.

When it is clearly worth it

Strip away the marketing and a few patterns hold up consistently. Studying abroad tends to be worth it when most of these are true.

The destination has a genuine post-study work route, not a 90-day “look for a job then leave” stamp. A two to three year work visa is the difference between recovering your investment and not. The course is in a field with real hiring demand in that country, STEM, healthcare, certain engineering and data roles, rather than a generic management degree at a university with no recruiter relationships. The university is one employers in that country actually recruit from, which often matters more than its global ranking. The student already has a strong base, a good undergraduate record or work experience, because a weak profile does not become strong by changing countries. And the funding is structured so the EMI after the moratorium is below 40% of a realistic first-year take-home salary. The math behind that EMI is worth understanding in detail before you sign, which is covered in the education loan moratorium and interest post.

When five or six of those line up, the success case becomes the likely case, not the lucky one.

When it is clearly not worth it

The honest counterpart. Studying abroad is usually not worth it when these show up.

The destination is chosen for ease of admission rather than work prospects, and the post-study visa is short or unreliable. The course is a generic program with no specific employability, picked because it was the cheapest route to a visa. The university is unranked and unknown to employers, the kind of place a commission-driven consultancy pushes because the agency commission is high, not because graduates do well. The funding requires liquidating a parent’s retirement corpus or selling the family home, which converts an education decision into a bet on a single uncertain job outcome. Or the student is going mainly to “get out of India” without a clear field or plan, which is the most expensive way to buy a few years of clarity.

If two or more of those are true, the probability you land in the struggle case rises sharply, and no amount of effort abroad reliably fixes a decision that was wrong at the planning stage.

Faz's ruleIf funding the degree means breaking your parents' retirement, the answer is almost always no.

A loan is recoverable. A sold flat or a liquidated retirement FD, at an age when your parents cannot rebuild it, is not. The degree might still pay off. But you are no longer betting your money. You are betting theirs, and the downside lands on people who cannot start over.

Country, course and college tier: what actually moves the needle

The single biggest variable is the post-study work policy of the destination. A country that lets you stay and work for two to three years gives you time to find a sponsored role and earn back the cost. A country that expects you to leave within months of graduating turns the degree into a pure expense with a tourism component. Before you fall in love with a destination, check its current post-study work rules on official sources, and compare destinations honestly in the best country to study abroad post and the cheapest country to study abroad post. If you have already narrowed it to a shortlist, the head to head breakdowns help, such as USA vs UK for Indian students and Canada vs Australia for Indian students, where the work visa difference is the deciding factor.

The second variable is course employability. A STEM or healthcare qualification with clear demand is a different financial product from a generic management degree, even at the same price. The third is college tier, but not the way rankings suggest. What matters is whether employers in that country recruit from that specific university. A modestly ranked university with strong local recruiter ties can beat a higher-ranked one with none.

| Factor | Pushes toward “worth it” | Pushes toward “not worth it” |

|---|---|---|

| Post-study work route | Two to three year work visa | Short or uncertain post-study stay |

| Course field | STEM, healthcare, in-demand engineering | Generic management with no specialisation |

| University | Employers in that country recruit there | Unknown to recruiters, agency-pushed |

| Funding structure | Loan with EMI under 40% of expected salary | Retirement corpus or family home liquidated |

| Student profile | Strong undergrad record or work experience | Weak base, going mainly to leave India |

The post-study work and return-to-India scenarios

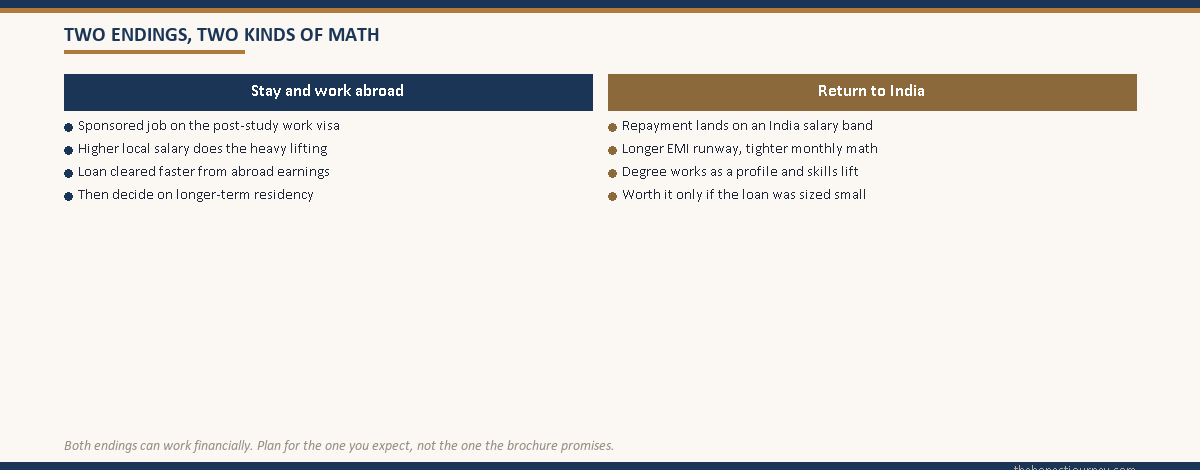

Two endings are common and both can work financially, but they work differently. In the stay-abroad ending, you find a sponsored job, work two to three years on the post-study visa, clear most of the loan from the higher local salary, and then decide whether to pursue longer-term residency. This is the path where the raw numbers look best, because the abroad salary does the heavy lifting on the EMI.

In the return-to-India ending, you study, perhaps work abroad briefly, then come back. Here the degree still has value. The international exposure, the English fluency, the specific skill set and the network can lift your India salary band. But the math is tighter, because you are repaying an abroad-sized loan from an India-sized salary. This ending is worth it when the loan was sized conservatively and the field genuinely commands a premium in the Indian market. It goes wrong when a ₹55 lakh loan meets a ₹16 LPA return salary. If returning is a real possibility for you, plan for it from the start rather than treating it as failure, and read the return to India after studying abroad post before you commit.

One practical lever in both scenarios: part-time work during the course. It does not fund a degree, but it covers a slice of living costs and, more importantly, can service the loan interest during the moratorium so it does not capitalise. The realistic limits and earnings are covered in the part-time work while studying abroad post.

The 6-gate decision framework

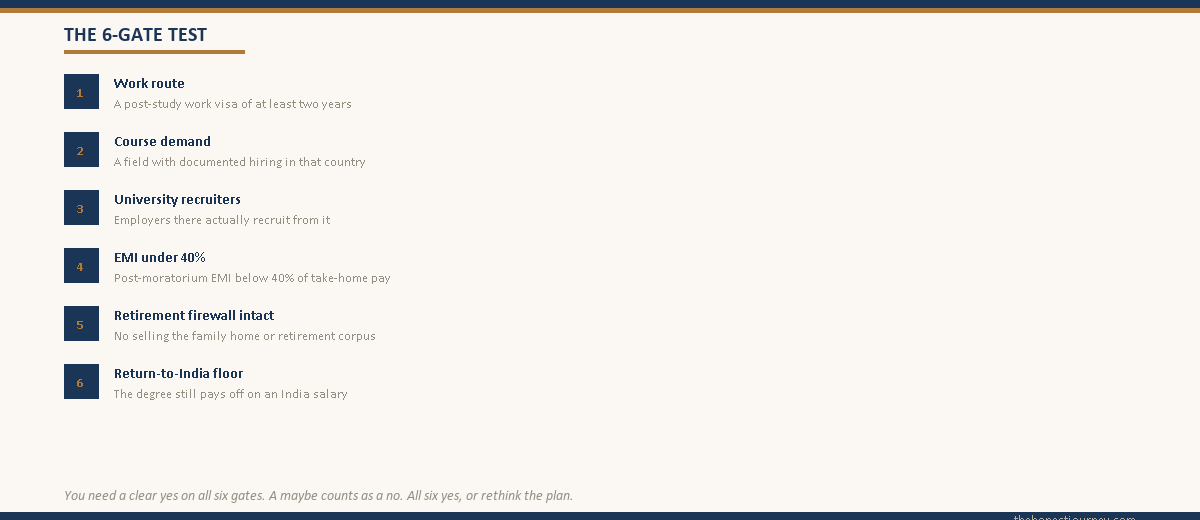

Here is the test. Run your own situation through these six gates honestly. The rule is simple: you need a clear yes on all six. A “maybe” counts as a no, because the cost of being wrong here is measured in decades, not years.

Gate 1: The work route. Does your target destination currently offer a post-study work visa of at least two years for your course type? Check the official immigration source, not a consultancy blog. For the two destinations Indian students ask about most, the route mechanics are laid out in the guides to studying in the USA and studying in the UK for Indian students. No real work route, no go.

Gate 2: The course. Is your course in a field with documented hiring demand in that country, or is it a generic degree chosen for easy admission? If you cannot name three types of employers who hire from your program, that is a no.

Gate 3: The university. Do employers in that country actually recruit from this specific university? Look at where past graduates of your exact program landed, not the brochure. If you cannot verify it, treat it as a no.

Gate 4: The EMI test. Take your honest expected first-year take-home salary in the destination. Is the post-moratorium loan EMI below 40% of it? If you are funding partly by loan and the EMI crosses 40%, the loan is oversized for the likely outcome.

Gate 5: The retirement firewall. Can you fund this without selling the family home or liquidating a parent’s retirement corpus? A loan you can repay is fine. A bet on irreplaceable family security is not. If funding requires the firewall to come down, that is a no.

Gate 6: The return floor. If the abroad job never materialises and you return to India, does the degree still lift your India salary enough to make the loan serviceable on an India income? If the entire plan collapses without the abroad job, the plan has no floor.

Six clear yeses, and studying abroad is very likely worth it for you. Even one honest no, and you should either fix that gate before going or seriously consider a strong domestic alternative.

The honest closing take

Studying abroad is not a good decision or a bad decision. It is a financial and life decision that is good for some people and genuinely costly for others, and the marketing you are surrounded by is built to hide that split because the people doing the marketing get paid on “yes.”

The version that works is specific: a real work route, an employable course, a university with recruiter ties, a loan sized to a realistic salary, family retirement left untouched, and a fallback if you return. The version that hurts is also specific, and it is not the student’s effort that fails. It is a decision made on a brochure number instead of the full math.

Run the six gates. Run the ROI calculation with your own honest figures, including the cost of not going. Compare it squarely against a strong domestic path, because for some students an Indian degree plus a few years of experience, at an institution recognised by the Ministry of Education, reaches a similar place without the ₹50 lakh-plus risk. And then decide. It is your degree, your money or your family’s, and your years. The math can tell you the odds. The choice is still yours to make.

Country by country, is the return worth the loan? See the honest ROI and payback math for the USA, the UK, Germany, Canada and Australia.

Worth it for whom, though? The math swings hard by profile. See the honest version for engineering graduates, non-STEM and commerce graduates, an MBA on a working salary and applicants in their 30s.

FAQ

Is studying abroad worth it for Indian students?

It depends on three things: whether the destination offers a genuine multi-year post-study work visa, whether the course leads to employable demand, and whether the funding leaves family retirement security intact. When all three hold, it is usually worth it. When the course is generic, the university is unknown to recruiters, or the funding requires selling family assets, it often is not. There is no single yes or no that applies to everyone.

Is it worth taking a loan to study abroad?

A loan can be the right call when the EMI after the moratorium stays below roughly 40% of a realistic first-year take-home salary. A loan is recoverable from future earnings, which makes it far safer than liquidating a parent’s retirement corpus. It becomes a problem when the loan is oversized relative to the likely salary outcome, or taken at a high unsecured rate for a course with weak job prospects. Size the loan to the outcome, not to the maximum the bank approves.

Do Indian students get jobs abroad after studying?

Many do, but the outcome depends heavily on the field, the university and the destination’s hiring market, not just on effort. Graduates in STEM, healthcare and in-demand engineering roles, from universities that local employers recruit from, have a strong record. Graduates from generic programs at low-ranked universities often struggle to find sponsored full-time roles. Before choosing, check where past graduates of your exact program actually landed.

Is studying abroad worth it financially?

Financially it is worth it when the real annual surplus over an equivalent India salary, after foreign taxes and living costs, clears the all-in cost within roughly three to four working years. For a loan-funded master’s costing ₹50 lakh to 95 lakh all-in, that requires a solid sponsored job. The honest figure to calculate is not the gross foreign salary but the surplus over what you would have earned staying in India.

Should I study abroad or in India?

For some students a strong domestic degree plus two to three years of work experience reaches a similar career position without the large cost and currency risk. Studying abroad pulls ahead when the destination offers a real work route, the field is in demand there, and you want international exposure or longer-term residency. Run both paths through honest numbers, including the income you would earn while studying if you stayed in India.

Is it worth going abroad for a master’s?

A master’s abroad is worth it when it is a specialised, employable degree at a university with recruiter relationships, in a country with a multi-year post-study work visa. A one-year STEM master’s with a strong job market often has the cleanest ROI. A two-year generic management degree at a low-ranked university, funded by a high-rate unsecured loan, is the configuration most likely to disappoint. The course and university choice matter more than the master’s label itself.

What is the cost of not going abroad?

The cost of not going is the income a capable graduate would earn by staying and working in India during the years otherwise spent studying and job-hunting abroad. For a tier-1 graduate or an experienced tier-2 graduate, that foregone income can run ₹20 lakh to 40 lakh across three years. An honest ROI calculation subtracts this from the abroad gain, because a degree abroad has to beat the realistic India outcome, not a salary of zero.

Is studying abroad worth it if I plan to return to India?

It can be, but the math is tighter, because you repay an abroad-sized loan from an India-sized salary. The degree still adds value through international exposure, skills and network, often lifting your India salary band. This ending works when the loan was sized conservatively and the field commands a genuine premium in the Indian market. It goes wrong when a large loan meets a modest return salary. If returning is likely, plan the loan size around that outcome from the start.

Faz · The Honest Journey · 2026