Choose a PSU bank education loan when you have collateral and time, because the floating rate near 9.5 to 11 percent plus the central interest subsidy and a slow but cheap moratorium make it the lowest lifetime cost. Choose an NBFC when you have no collateral, a strong parent co-applicant, and a tight deadline, accepting a rate of roughly 11.5 to 14 percent and no subsidy in exchange for speed and an unsecured sanction. On a ₹40 lakh loan that rate gap is often ₹8 to 15 lakh of extra interest over the life, which is the price you pay for not pledging property.

Two families I know took the same ₹40 lakh loan in the same season. One pledged their flat to SBI and paid a floating rate just under 10 percent. The other had no property to pledge, went to an NBFC against the father’s salary, and signed at 12.75 percent. Same amount, same destination, same two-year program. By the time both loans are repaid, the second family will have paid well over ₹10 lakh more in interest. Neither was wrong. The first had collateral and time; the second had neither and needed the money fast. That is the whole decision in one sentence.

This post is the honest framework for that choice. Not which lender is better, because there is no universal answer, but how to read your own situation against the six things that actually separate a PSU bank loan from an NBFC one: rate, collateral, speed, subsidy and tax, moratorium, and forex.

To compare this NBFC against the alternatives: the avanse education loan post, the MPOWER financing education loan post, and the prodigy finance education loan post.

The six axes that actually decide it

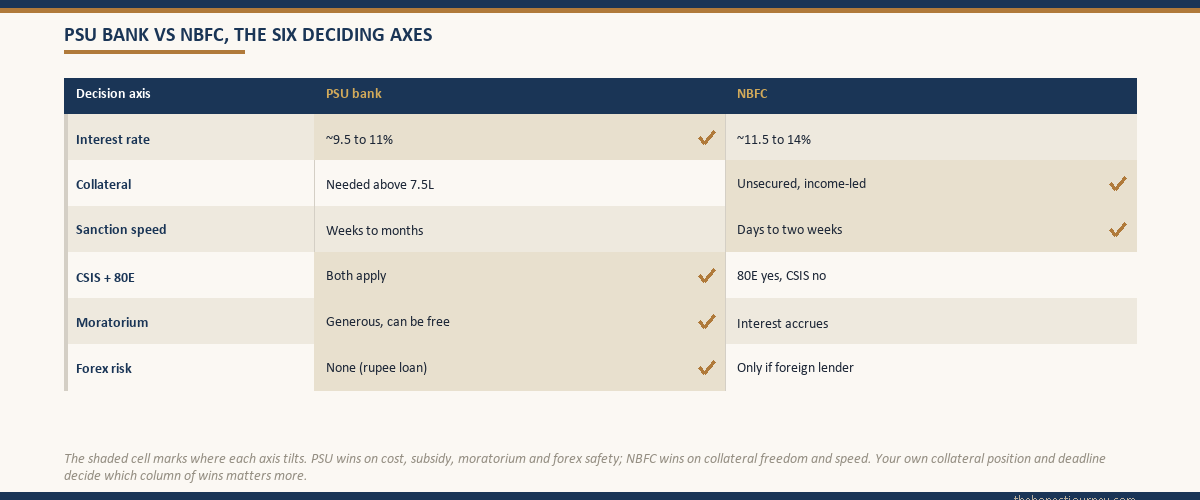

Strip away the marketing and a PSU-versus-NBFC decision comes down to six variables. Get clear on where you stand on each and the answer usually falls out on its own.

Rate is the headline. PSU banks lend at a floating rate roughly in the 9.5 to 11 percent band; NBFCs sit higher, roughly 11.5 to 14 percent, because they price in the lack of collateral and their own cost of funds. Over a long repayment that gap is the single biggest cost difference, and it is laid out in detail in the education loan interest rate comparison post.

Collateral is the gatekeeper. PSU banks require tangible collateral, property, fixed deposit or LIC, for any amount above the ₹7.5 lakh unsecured ceiling, which means almost every abroad loan. NBFCs lend unsecured well into tens of lakhs against a strong co-applicant income, which is exactly why families without property go to them. The secured-versus-unsecured trade-off itself is the subject of the secured vs unsecured education loan post, and the no-collateral route is covered in the education loan for abroad studies without collateral post.

Speed is where NBFCs win cleanly. An NBFC can sanction in days to a couple of weeks because the file is lighter and the underwriting is income-led. A PSU bank with a collateral file, valuation, and legal check routinely takes several weeks to a couple of months. When the CAS or I-20 deadline is close, that difference decides things.

Subsidy, tax, moratorium, and forex

The remaining three axes are where most families miss money, so I will take each plainly.

CSIS, the Central Sector Interest Subsidy, pays the interest on your loan during the moratorium for eligible students below an income threshold studying in India, and it applies to loans from scheduled banks under the IBA model scheme, generally not to NBFC loans. 80E, the income tax deduction on education loan interest, is broader: it applies to loans taken from banks and from notified financial institutions, so most mainstream NBFC loans do qualify for 80E even though they do not qualify for CSIS. That distinction matters: an NBFC borrower usually keeps the 80E tax benefit but loses the CSIS subsidy. How to actually claim the subsidy is in the CSIS interest subsidy post.

Moratorium is the grace period before repayment starts, usually the course length plus six to twelve months. PSU banks under the IBA scheme offer a standard, generous moratorium, and during it a CSIS-eligible borrower pays no interest at all because the subsidy covers it. NBFCs offer a moratorium too, but interest typically accrues throughout, and many NBFC borrowers are nudged toward paying simple interest during the course to keep the ballooning down. So the PSU moratorium is not just longer on paper, it can be genuinely free for eligible students, while the NBFC one quietly compounds.

Forex is a fourth-axis catch that only applies to foreign NBFCs. An Indian PSU bank or Indian NBFC lends in rupees, so the exchange rate moves your cost of living abroad but not your loan repayment. A foreign lender that disburses and is repaid in dollars or pounds puts the currency risk on you: if the rupee weakens against the repayment currency, your effective cost rises. Indian NBFCs do not carry this; foreign ones do. Confirm the repayment currency before you sign, because a rupee loan and a dollar loan at the same headline rate are not the same loan.

Faz's ruleAn NBFC borrower usually keeps the 80E tax deduction but loses the CSIS subsidy. Those are two different benefits, and conflating them is how families miscount the real cost gap.

CSIS pays your interest during the moratorium and is generally a scheduled-bank benefit; 80E is a tax deduction on interest paid and extends to notified NBFCs. So an NBFC loan is not stripped of every benefit, it keeps 80E, but it does forgo CSIS. When you compare PSU and NBFC, count both correctly or the rate gap will look smaller than it really is.

The worked INR example: the lifetime interest gap

Numbers make this concrete. Take an identical loan: ₹40 lakh for a two-year Master’s abroad, repaid over a 10-year tenure after the moratorium. One family pledges collateral and takes a PSU loan at 10 percent. The other has no collateral and takes an NBFC loan at 12.75 percent. Everything else is held equal so the rate is the only variable.

| Item | PSU secured | NBFC unsecured |

|---|---|---|

| Loan amount | ₹40,00,000 | ₹40,00,000 |

| Interest rate | ~10.0 percent | ~12.75 percent |

| Repayment tenure | 10 years | 10 years |

| Approx monthly EMI | ~₹52,900 | ~₹59,300 |

| Approx total interest | ~₹23.4 lakh | ~₹31.2 lakh |

| Lifetime interest gap | ~₹7.8 lakh more on the NBFC loan | |

That roughly ₹8 lakh is the price of not pledging collateral, on this size and tenure. On a larger loan, or with the NBFC at the top of its band near 14 percent, the gap stretches past ₹12 to 15 lakh. These EMI and interest figures are indicative, calculated to show the shape of the gap, not a quote; your actual numbers depend on the exact rate, compounding, and whether interest accrued during the moratorium, so confirm against the sanction letter.

Here is the honest other side of that table. The NBFC family got their money in two weeks and did not have to mortgage the only flat the parents own. If that flat is the family’s sole security and retirement cushion, ₹8 lakh of extra interest spread over a decade may be a price worth paying to keep it unpledged. The number alone does not decide it. The number plus your collateral position and your deadline does.

Choose PSU if, choose NBFC if

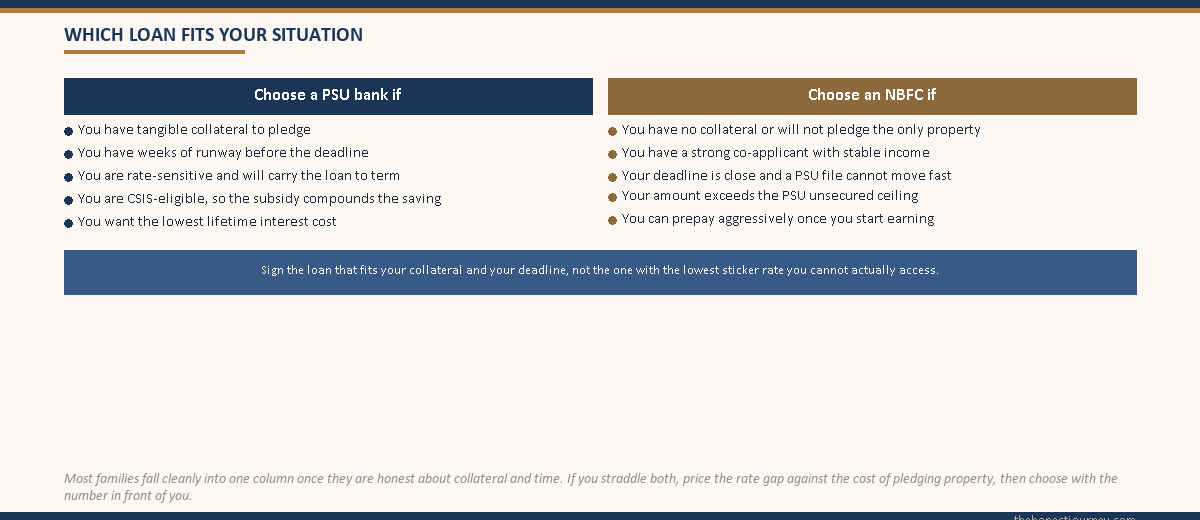

The framework collapses to two short lists. Read them against your own situation honestly.

Choose a PSU bank if you have tangible collateral to pledge, you have several weeks of runway before the deadline, you are rate-sensitive and plan to carry the loan for its full tenure, and especially if you are CSIS-eligible, because the subsidy plus the lower rate makes the PSU loan dramatically cheaper over its life. The cost of the PSU route is patience and paperwork, and if you can afford both, it is almost always the cheaper loan. The reference PSU example to compare against is the SBI education loan for abroad studies post.

Choose an NBFC if you have no collateral or do not want to pledge the family’s only property, you have a strong co-applicant with stable income and a clean credit record, your deadline is close and a PSU file cannot move fast enough, or your amount exceeds what a PSU will lend unsecured and you cannot meet the collateral demand. You will pay more in interest, and you should plan to prepay aggressively once you are earning to shrink that gap. A representative NBFC profile is in the HDFC Credila education loan post. Two other dedicated education-loan NBFCs worth comparing are the Auxilo education loan, which focuses purely on study financing, and the InCred education loan, which lends collateral-free up to ₹1.5 crore against a strong co-applicant.

The regulatory framework both lender types operate under is set by the RBI, and the IBA model scheme is the template PSU banks follow on caps, margin and moratorium. The current rules are on the RBI site and the model education loan scheme is published by the Indian Banks’ Association. Neither caps your choice; both lender types are legitimate, and the right one is the one that fits your collateral, your deadline, and your appetite for interest.

Faz's ruleThe NBFC premium is the price of speed and not pledging property. If you take it, commit to prepaying aggressively once you earn, so you pay for the speed without carrying the full rate gap for ten years.

An NBFC loan is the right call when collateral or time is the binding constraint. But the higher rate only bites if you carry the loan to term. Earn, then attack the principal in years one and two of repayment. Most NBFC loans allow prepayment with low or no penalty, so used that way the lifetime gap shrinks well below the table figure.

The honest take on PSU versus NBFC

There is no winner in the abstract. A PSU bank loan is the cheaper, slower, collateral-hungry option that rewards families with property and patience and pays off most for CSIS-eligible students. An NBFC loan is the faster, dearer, collateral-free option that exists precisely for families who have neither property to pledge nor weeks to wait, and who can lean on a strong co-applicant instead.

The mistake is treating the rate as the only number. The rate is the biggest number, but the collateral you would have to pledge, the deadline you are racing, and the subsidy you may or may not qualify for all sit on the same scale. Weigh all four, run your own loan through the EMI math at both rates, and the choice stops being a coin toss.

If you have collateral and time, the PSU loan will almost always cost you less, so take it. If you do not, the NBFC is not a trap, it is a legitimate tool, as long as you go in knowing the premium and you plan to prepay it down. Sign the loan that fits your situation, not the one with the lowest sticker rate, because the lowest rate you cannot actually access is not a real option.

FAQ

Is a PSU bank or NBFC education loan cheaper?

A PSU bank loan is almost always cheaper on interest. PSU banks lend at a floating rate roughly in the 9.5 to 11 percent band, while NBFCs sit higher at around 11.5 to 14 percent because they price in the lack of collateral. On a ₹40 lakh loan over 10 years, that gap works out to roughly ₹8 lakh more in lifetime interest on the NBFC loan, and more on larger amounts. The PSU loan also keeps the CSIS subsidy for eligible students, widening the gap further.

Why would anyone choose an NBFC over a PSU bank?

Two reasons: collateral and speed. PSU banks demand tangible collateral such as property, fixed deposit or LIC for any amount above the ₹7.5 lakh unsecured ceiling, which covers almost every abroad loan. NBFCs lend unsecured into tens of lakhs against a strong co-applicant’s income, so families with no property to pledge go to them. NBFCs also sanction in days to a couple of weeks, against several weeks to months for a PSU collateral file, which matters when a CAS or I-20 deadline is close.

Do NBFC education loans qualify for CSIS and 80E?

They differ. CSIS, the Central Sector Interest Subsidy, applies to loans from scheduled banks under the IBA model scheme and generally not to NBFC loans, so an NBFC borrower usually loses the subsidy. 80E, the income tax deduction on education loan interest, is broader and applies to loans from banks and notified financial institutions, so most mainstream NBFC loans do qualify for 80E. So an NBFC borrower typically keeps the 80E tax benefit but forgoes the CSIS subsidy, which families often miscount.

How much more does an NBFC loan cost over its life?

On a ₹40 lakh loan repaid over 10 years, a PSU rate near 10 percent against an NBFC rate near 12.75 percent produces roughly ₹8 lakh more in total interest on the NBFC loan. With the NBFC at the top of its band near 14 percent, or on a larger loan, the gap can stretch past ₹12 to 15 lakh. These are indicative figures to show the shape of the gap; your actual cost depends on the exact rate, compounding, and moratorium interest, so confirm on the sanction letter.

How does the moratorium differ between PSU and NBFC?

The moratorium is the grace period before repayment starts, usually the course length plus six to twelve months. PSU banks under the IBA scheme offer a standard generous moratorium, and during it a CSIS-eligible borrower pays no interest because the subsidy covers it. NBFCs offer a moratorium too, but interest typically accrues throughout, and borrowers are often nudged to pay simple interest during the course to limit the ballooning. So the PSU moratorium can be genuinely free for eligible students, while the NBFC one compounds.

What is forex risk on an NBFC education loan?

Forex risk applies only to foreign lenders, not Indian ones. An Indian PSU bank or Indian NBFC lends and is repaid in rupees, so the exchange rate affects your living costs abroad but not your loan repayment. A foreign lender that disburses and is repaid in dollars or pounds puts the currency risk on you: if the rupee weakens against the repayment currency, your effective cost rises. Indian NBFCs do not carry this; foreign ones do, so confirm the repayment currency before you sign.

Should I pledge my only property for a cheaper PSU loan?

That is a judgment call, not a pure math question. The PSU loan will save you several lakh in interest, but pledging the family’s only flat, often the parents’ retirement cushion, carries its own risk if repayment ever falters. If the saved interest matters more than keeping the property unencumbered, pledge and take the PSU rate. If the property is the family’s sole security, paying the NBFC premium to leave it unpledged can be the wiser call. Weigh both, not just the rate.

Can I switch from an NBFC to a PSU bank later?

Yes, through a balance transfer, but it is not automatic. Once you are earning and can either pledge collateral or show strong repayment history, you can refinance an NBFC loan to a cheaper PSU or bank loan, moving the outstanding balance to the lower rate. Check for foreclosure charges on the NBFC side and processing fees on the new loan, since they can eat into the saving. For many NBFC borrowers, aggressive prepayment in the early earning years is simpler and achieves much the same reduction in lifetime interest.

Faz · The Honest Journey · 2026