A secured education loan needs collateral (property, FD, or LIC policy) and typically charges 8.5 to 10.5 percent, while an unsecured loan needs only a co-applicant and charges 11 to 14 percent. For loans above ₹20 lakh I pick secured every time. Below ₹7.5 lakh, unsecured wins on speed and paperwork.

You sat across from two relationship managers in the same week. The public sector bank manager wanted your father’s flat papers, the LIC policy, and a property valuation report. The NBFC executive smiled and said no collateral needed, just a co-applicant, sanction in seven days. One of them quoted you 9.5%. The other quoted 13%. Both of them called their version “the better option,” and neither explained what you were actually trading away.

This post is the comparison nobody sells you, because the honest answer does not earn a commission. Whether an education loan is secured or unsecured changes your interest rate, your loan ceiling, your timeline, and the worst-case picture if repayment goes wrong.

An education loan is secured when you pledge collateral, and unsecured when you do not. Secured loans run roughly 8.5% to 13%, allow much higher limits, and take weeks because the property has to be valued and legally cleared. Unsecured loans run roughly 10.5% to 15%, cap around ₹40 lakh to 80 lakh, and sanction in 7 to 10 days because the co-applicant’s income carries the file instead of an asset.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

To weigh this lender against the others: the canara bank education loan post, the bank of baroda education loan post, and the axis bank education loan post.

What “secured” and “unsecured” actually mean in an education loan

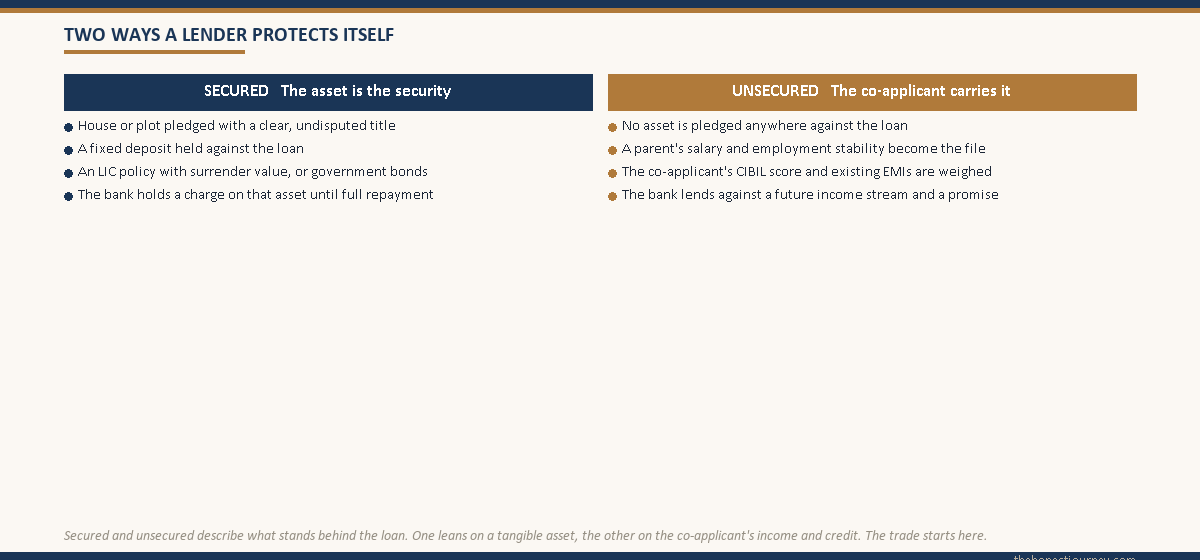

A secured education loan is one where you give the bank a lien on a tangible asset. The common forms of collateral are immovable property (a house or a plot in the family’s name with a clear title), a fixed deposit, a policy from an insurer such as LIC that carries a surrender value, or government bonds. The bank holds a charge on that asset until the loan is fully repaid. If repayment defaults completely and recovery efforts fail, the bank can move to recover its money from that asset.

An unsecured education loan, often marketed as a “collateral-free” or “non-collateral” loan, has no asset pledged against it. The bank’s security is the creditworthiness of the borrower and, far more importantly, the co-applicant. A parent’s salary, their CIBIL score, their existing EMIs, and their employment stability become the file. The bank is lending against a future income stream and a promise, not against a flat it can attach.

One thing worth saying plainly because lender blogs blur it: this is not the same as the RBI threshold for guarantees. Under the Indian Banks’ Association Model Education Loan Scheme, published on the IBA site, loans up to ₹4 lakh need no collateral and no third-party guarantee, and loans from ₹4 lakh to 7.5 lakh need a third-party guarantee but still no tangible collateral. Above ₹7.5 lakh, a public sector bank typically asks for collateral. These collateral-free thresholds sit within the broader RBI education lending framework. That is the framework. The “collateral-free up to ₹50 lakh” loans you see advertised are NBFC and private bank products built on co-applicant income, sitting outside that scheme.

The numbers side by side

Here is the comparison grid that the two relationship managers will never lay out for you honestly, because each only sells one column. These ranges reflect what students with a reasonable co-applicant profile and a recognised university were being quoted across public sector banks and the major abroad-focused NBFCs in 2025-26.

| Factor | Secured loan | Unsecured loan |

|---|---|---|

| Collateral | Property, FD, LIC, or bonds pledged | None. Co-applicant income carries the file |

| Typical interest rate | 8.5% to 13% | 10.5% to 15% |

| Loan ceiling | Up to roughly ₹1.5 crore | Roughly ₹40 lakh to 80 lakh |

| Processing time | 3 to 6 weeks | 7 to 10 days |

| Documentation | Heavy. Title deed, valuation, legal report | Lighter. Income proof, KYC, admission letter |

| Common lender type | Public sector banks | NBFCs and private banks |

| Worst-case exposure | The pledged asset is at risk | Co-applicant’s credit and income are at risk |

The two rows that matter most are the interest rate and the worst-case exposure, and they pull in opposite directions. The secured loan is cheaper, often by 2 to 3 percentage points. But the cheaper money is borrowed against your family’s home or savings. The unsecured loan is faster and asks for no asset, but you pay for that with a higher rate every month for ten years, and the co-applicant’s financial health is the thing standing behind it.

What the 2 to 3 percent rate gap is actually worth

People hear “9.5% versus 12.5%” and treat it as a small difference. It is not. On a real loan over a real tenure, three percentage points is lakhs of rupees. Take a ₹30 lakh loan repaid over 10 years, calculated on the simplified case of repayment starting on the original principal.

| Loan | Rate | Monthly EMI | Total interest paid | Total repaid |

|---|---|---|---|---|

| ₹30 lakh secured | 9.5% | ₹38,820 | ₹16,58,400 | ₹46,58,400 |

| ₹30 lakh unsecured | 12.5% | ₹43,920 | ₹22,70,400 | ₹52,70,400 |

The unsecured route costs about ₹6.1 lakh more in interest over the loan life, and the EMI is ₹5,100 higher every single month. That ₹6 lakh is the price of speed and of not pledging an asset. For some families that price is worth paying. For others it is a year of a starting salary handed to a lender for no structural reason. The point is to see the number clearly, not to feel it as an abstract “slightly higher rate.”

The gap also compounds during the moratorium period, because interest accrues while you study and usually gets added to your principal before repayment starts. A higher rate means a larger capitalized balance. If you have not read how that mechanism works, it is worth understanding before you choose, and it is covered in detail in the education loan moratorium period and interest post. For a fuller rate-by-rate picture across lenders, the education loan interest rate comparison lays out where each category sits.

Faz's ruleA 3 percent rate gap is not small. On a ₹30 lakh loan it is roughly ₹6 lakh and ₹5,000 a month for ten years.

People dismiss the rate difference because two numbers look close. They are not close in rupees. Run your own loan amount through an EMI calculation at both rates before you decide. The gap is the real cost of choosing unsecured, and it deserves a number, not a shrug.

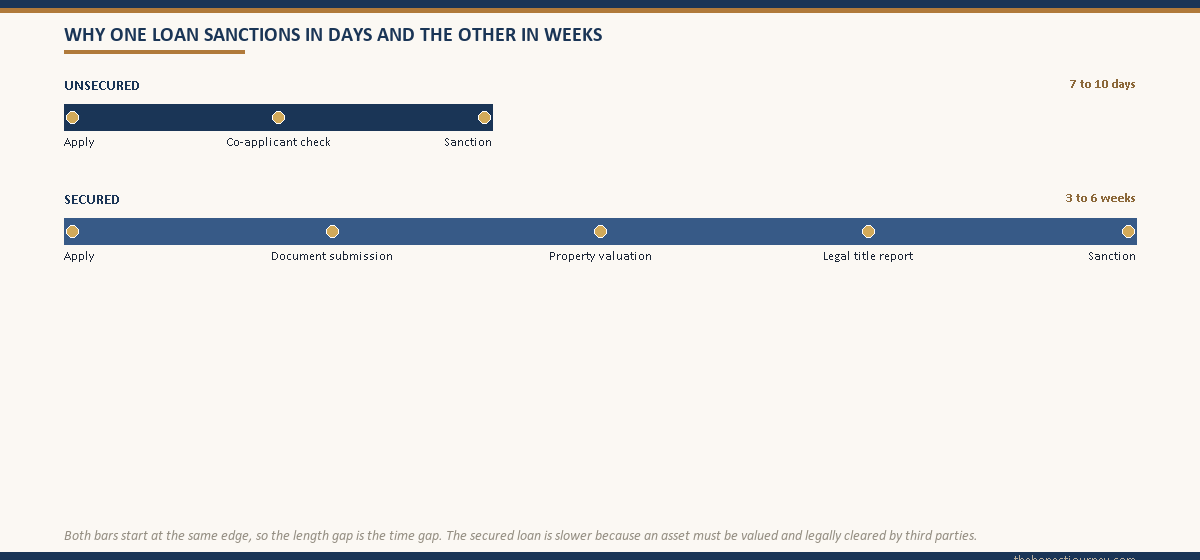

Why secured loans take weeks, and why that matters for your intake

The slowness of a secured loan is not bank inefficiency. It is the process of turning an asset into accepted collateral. Once you pledge property, the bank orders an independent valuation to confirm what the asset is worth. It then commissions a legal opinion to confirm the title is clean, that there is no existing charge, no disputed ownership, no encumbrance. Both reports take time, and they depend on third parties the bank does not control.

For a property in a metro with clear, recent title documents, the whole process might close in three weeks. For ancestral property, agricultural land converted to residential use, a flat with an incomplete chain of ownership, or papers in another state, it can stretch to six weeks or longer. None of that is in your control once you have handed over the documents.

This is the part that genuinely catches students out. If your university intake is in September and you start the secured loan process in July, you may not have a disbursement in hand when the tuition deadline lands. An unsecured loan, sanctioned in 7 to 10 days because there is no asset to verify, can be the difference between making the intake and deferring a year. Sometimes the faster loan is not the smarter loan in pure rupee terms, but it is the one that gets you on the flight. That is a real tradeoff, and timing is a legitimate reason to pay the higher rate.

The worst-case question most pages skip

Lender blogs talk about rates and limits. They rarely sit with the uncomfortable question, so let us. What actually happens if repayment goes badly wrong, the student does not land the expected job, the EMIs stop, and recovery efforts fail entirely?

On a secured loan, the pledged asset is exposed. If the loan defaults completely and the bank exhausts other recovery routes, it can move to recover its dues from the collateral. If that collateral is the family home the parents live in, the downside is not abstract. It is the roof. Banks do not jump to this. They restructure, they extend tenure, they negotiate, because recovery through asset attachment is slow and expensive for them too. But the asset is on the line, and you should choose with that fully in view.

On an unsecured loan, there is no pledged asset to attach. But “unsecured” does not mean consequence-free. The co-applicant, almost always a parent, has signed as equally liable. A default damages their CIBIL score, which affects their ability to borrow for anything else for years. The lender can pursue legal recovery against the co-applicant’s income and other unpledged assets. The harm is to the co-applicant’s financial standing and creditworthiness rather than to one specific pledged house, but it is real harm to a real person who trusted the projection.

Neither outcome is pleasant. The honest framing is this: a secured loan concentrates the worst case on one asset you can see. An unsecured loan spreads it across a co-applicant’s credit profile and income. Choose the loan whose worst case your family can actually absorb, not just the one whose monthly EMI looks comfortable on a spreadsheet.

Faz's ruleThere is no risk-free education loan. Secured risks the pledged asset, unsecured risks the co-applicant's credit and income.

Anyone who tells you a collateral-free loan is “safer” is selling, not advising. The risk did not vanish. It moved from a house you can point to onto a parent’s CIBIL score and salary. Pick the worst case your family can survive, then choose.

Can you switch from unsecured to secured later

This question comes up a lot, usually from a student who took the fast unsecured loan to make an intake and now wants the cheaper secured rate. The honest answer is that there is no automatic switch. You cannot simply call the NBFC and ask them to convert the loan and drop the rate.

What does exist is a balance transfer, also called a takeover. You apply to a second lender, usually a public sector bank, for a fresh secured loan against collateral. If they sanction it, the new lender pays off your existing unsecured loan and you continue with them at the lower rate. It is effectively refinancing. It works, and students do it, but it is not free. You go through the full secured process again: valuation, legal report, fresh documentation, possible processing fees. It only makes financial sense if the rate saving over your remaining tenure clearly exceeds the cost and effort of the transfer, which usually means doing it early in the loan life when most of the interest is still ahead of you.

The cleaner path, where possible, is to get the structure right at sanction rather than planning to fix it later. If you genuinely have collateral available and your intake timeline allows three to six weeks, starting the secured process early beats taking the unsecured loan and hoping to transfer it.

The honest closing take

There is no universally correct answer here, and any page that gives you one is selling a product. Secured and unsecured are not “good” and “bad.” They are two different trades.

The secured loan is the right call when your family has collateral with a clean title, your loan requirement is large, your intake timeline has room, and the family can genuinely live with the pledged asset being the security. You buy a lower rate and a higher ceiling, and you pay for it with weeks of process and an asset on the line.

The unsecured loan is the right call when there is no usable collateral, the loan amount sits within the ₹40 lakh to 80 lakh band, the intake is close and speed actually matters, and the co-applicant’s income and credit are strong enough to carry the file comfortably. You buy speed and the freedom of not pledging a home, and you pay for it with a higher rate every month.

What you should not do is pick on instinct, or let one relationship manager’s pitch decide for you. Run your real loan amount through both rates. Look at the EMI gap and the total-interest gap in actual rupees. Then sit with the worst case for each and ask, honestly, which one your family could absorb. The framework below walks you through it gate by gate.

The 6-gate decision framework

Answer each gate yes or no for your own situation. Use it as a structured way to land on the loan type that fits, not as a verdict handed down.

Gate 1: Do you have collateral with a clean, undisputed title? A house, plot, FD, or LIC policy in the family’s name with clear ownership and no existing charge. If no, you are heading toward an unsecured loan by default, and the remaining gates help you confirm it fits. If yes, continue.

Gate 2: Is your loan requirement above the unsecured ceiling? If you need more than roughly ₹40 lakh to 80 lakh (tuition plus living costs for an expensive destination), the unsecured route may simply not stretch far enough, and a secured loan becomes necessary rather than optional. If your requirement sits inside that band, both routes are open.

Gate 3: Does your intake timeline allow three to six weeks for processing? If your tuition deadline is more than two months out, a secured loan is feasible. If it is close and a deferral would cost you a year, the speed of an unsecured loan is a real and legitimate reason to choose it even at a higher rate.

Gate 4: Can your family genuinely live with the pledged asset being at risk? Not “will it probably be fine,” but “if the worst case happened, could we absorb losing this asset.” If the only collateral is the home the parents live in and that worst case is unthinkable, weigh that honestly before pledging it.

Gate 5: Is the rate gap, in rupees, worth more to you than the speed and the no-collateral comfort? Run your actual loan amount at both rates. If the secured loan saves ₹5 lakh to 8 lakh over the tenure and your timeline allows it, that saving is hard to ignore. If the gap is smaller or the timeline is tight, the unsecured loan earns its higher rate.

Gate 6: Is the co-applicant’s income and credit strong enough to comfortably carry an unsecured file? An unsecured loan rests entirely on the co-applicant. If their salary, CIBIL score, and existing EMI load comfortably pass a lender’s checks, the unsecured route is solid. If the co-applicant profile is borderline, a secured loan against an asset is often the more reliable sanction.

If you answered yes to Gates 1, 4, and 5 and have timeline room from Gate 3, a secured loan is likely your fit. If Gate 1 is no, or Gate 3 forces speed, or Gate 2 keeps you inside the band with a strong co-applicant from Gate 6, an unsecured loan is the sensible choice. If you are still genuinely split, that itself is useful information: it means the two options are close for you, and either is defensible. The decision is yours, and you now have the actual numbers to make it instead of a sales pitch.

If your situation points toward unsecured, the education loan for abroad studies without collateral guide goes deeper on how those products work. Whichever route you take, the documents required for an education loan and the role of the co-applicant are worth reading before you walk into a branch.

FAQ

Is an education loan secured or unsecured?

It can be either. An education loan is secured when you pledge collateral such as property, a fixed deposit, or an LIC policy against it. It is unsecured when no asset is pledged and the loan rests on the co-applicant’s income and credit instead. Under the Indian Banks’ Association Model Education Loan Scheme, loans up to ₹4 lakh need no collateral, and loans above roughly ₹7.5 lakh from public sector banks usually require it. The type depends on the amount and the lender.

Which is better, a secured or unsecured education loan?

Neither is universally better. A secured loan offers a lower interest rate (roughly 8.5% to 13%) and a higher ceiling but takes three to six weeks and puts a pledged asset at risk. An unsecured loan is faster (7 to 10 days) and needs no collateral but charges more (roughly 10.5% to 15%) and is capped lower. The right choice depends on whether you have collateral, how large your loan is, how tight your intake timeline is, and how strong your co-applicant profile is.

Is a secured education loan cheaper than an unsecured one?

Yes, usually by about 2 to 3 percentage points. Public sector bank secured loans, such as the products listed on the State Bank of India education loans page, tend to run 8.5% to 13%, while collateral-free NBFC and private bank loans run roughly 10.5% to 15%. On a ₹30 lakh loan over 10 years, that gap is about ₹6 lakh in extra interest and roughly ₹5,000 more per month on the EMI. The lower rate is the main advantage of the secured route, balanced against slower processing and the pledged asset.

How much education loan can I get without collateral?

Collateral-free education loans from NBFCs and private banks typically range up to roughly ₹40 lakh to 80 lakh, depending on the lender, the university, the course, and the co-applicant’s income. Separately, under the Indian Banks’ Association Model Education Loan Scheme, loans up to ₹4 lakh need no collateral or guarantee, and ₹4 lakh to 7.5 lakh need a third-party guarantee but no tangible collateral. Above that, public sector banks generally ask for collateral.

Is a secured education loan slower to process?

Yes. A secured loan takes three to six weeks because the pledged asset must be independently valued and a legal opinion obtained to confirm a clean title with no existing charge. Both reports depend on third parties. Older or ancestral property, agricultural land, or papers from another state can stretch the timeline further. An unsecured loan sanctions in 7 to 10 days because there is no asset to verify, only the co-applicant’s income and credit.

Can I switch from an unsecured to a secured education loan later?

There is no automatic conversion. What exists is a balance transfer or takeover, where you apply to another lender, usually a public sector bank, for a fresh secured loan that pays off your existing unsecured one. It works but is effectively refinancing: you repeat valuation, legal checks, and documentation, and may pay processing fees. It only makes sense if the rate saving over your remaining tenure clearly exceeds the cost, which usually means doing it early in the loan life.

What happens to my collateral if I cannot repay a secured education loan?

If a secured loan defaults completely and the bank exhausts other recovery routes, it can move to recover its dues from the pledged asset. Banks generally try restructuring, tenure extension, and negotiation first, because asset attachment is slow and costly for them too. Still, the collateral is genuinely exposed. If that collateral is the family home, the downside is concrete, and you should choose a secured loan only if the family can absorb that worst case.

Does an unsecured education loan have no risk because there is no collateral?

No. An unsecured loan still carries real risk, it just sits in a different place. The co-applicant, usually a parent, signs as equally liable. A default damages their CIBIL score for years and the lender can pursue legal recovery against their income and unpledged assets. The risk moved from a specific pledged asset onto the co-applicant’s overall credit standing and financial health. A collateral-free loan is not a consequence-free loan.

Faz · The Honest Journey · 2026