An education loan top-up lets you borrow an additional ₹1 lakh to ₹25 lakh on top of your existing sanction, usually after one academic year of clean repayment behaviour and at the same or slightly higher interest rate. Banks like SBI, HDFC Credila, and Avanse process top-ups in 2 to 4 weeks if your CIBIL stayed above 700. Currency depreciation and revised fee schedules are the two most-approved reasons.

You sized the loan carefully. Tuition, hostel, a margin for living costs, even a small buffer. Then the university sent a revised fee schedule for the second year, the rupee slid four points against the dollar, and the buffer you were proud of is gone by November of your first year. Now you are sitting in a hostel room doing arithmetic that does not balance, and the bank that funded you in the first place feels very far away.

This is the situation an education loan top-up exists to solve. This post explains when a top-up is the right move, when it is a warning sign, and the one mistake that quietly costs students lakhs.

An education loan top-up is an additional amount sanctioned on top of your existing education loan, used when a genuine mid-course funding gap appears. It is usually faster to approve than a fresh loan because the lender already holds your file, but it is not automatic: the bank rechecks your co-applicant income and, on secured loans, the collateral value. The expensive trap is plugging the gap with a personal loan instead, which carries a far higher rate and no Section 80E tax benefit.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on managing repayment: the how to repay education loan india post, the education loan balance transfer india post, and the RBI education loan repayment rules post.

What an education loan top-up actually is

A top-up is exactly what the name suggests: more money added to a loan account you already have. It is not a new loan with a new account number in most cases. The lender enhances your existing sanction limit, disburses the additional amount, and folds it into the same repayment structure, the same moratorium clock, and the same interest rate basis you already agreed to.

The reason a top-up exists at all is that education costs abroad are not fixed at sanction time. Three things move after you sign:

Tuition revisions. Many universities publish fees year by year, not for the full program. A 4 to 7 percent annual increase is normal. On a course where year-one tuition was 18 lakh, year two can land at 19.3 lakh without anyone doing anything wrong.

Forex movement. Your loan is sanctioned in rupees. Your fees are paid in dollars, pounds, or euros. If the rupee weakens between sanction and your second disbursement, the same dollar fee costs you more rupees. A move from 83 to 87 on the dollar is a 4.8 percent jump in the rupee cost of everything.

Living-cost underestimation. The single most common gap. Students and banks both tend to budget living expenses on the optimistic end. Rent in the actual city, not the brochure city, plus the first-month deposits, plus a laptop the course turned out to require, adds up fast.

A top-up is the formal, low-rate way to bridge that gap inside the education loan system, rather than scrambling for expensive credit outside it.

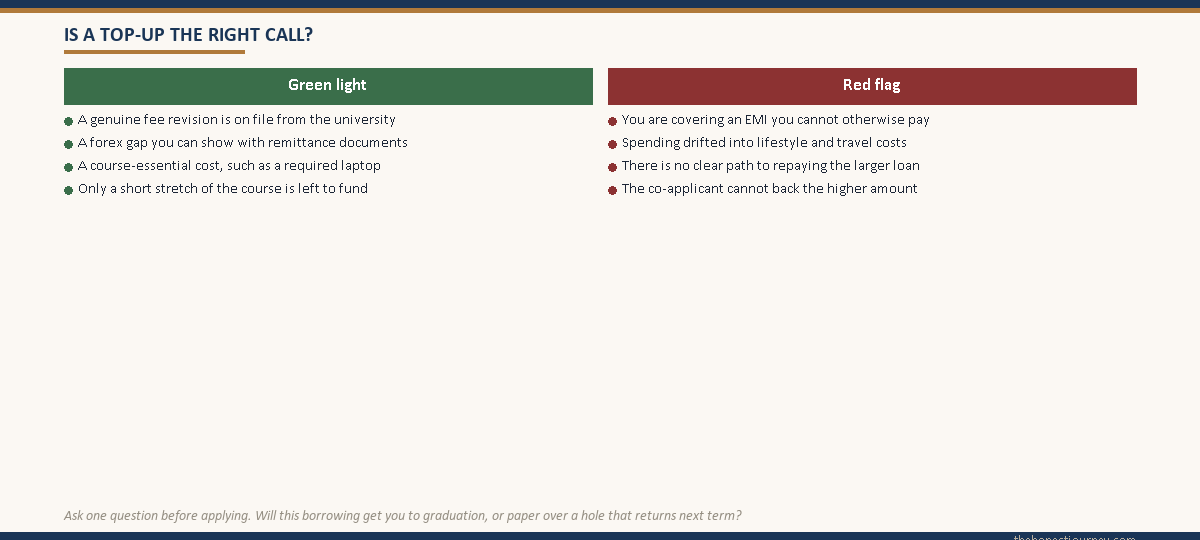

When a top-up makes sense, and when it does not

A top-up is a tool, not a rescue. It works well when the gap is genuine, documented, and tied to the cost of completing the course. It works badly when it is covering a planning failure that the extra borrowing will only deepen.

| Situation | Top-up a good idea? | Why |

|---|---|---|

| University raised year-two tuition | Yes | Documented, course-essential, finite. The lender can see the revised fee letter. |

| Rupee weakened, fee in forex costs more | Yes | Genuine and verifiable against your remittance receipts. |

| Course requires a laptop or equipment not budgeted | Usually | Course-essential costs are within the spirit of an education loan. |

| You underestimated rent and living costs | Case by case | Acceptable if the original budget was wrong, not if spending drifted. |

| You want a top-up to pay an existing EMI | No | Borrowing to service debt is the start of a debt spiral, not a fix. |

| Discretionary spending, travel, lifestyle | No | Adds principal and interest with no return on the course outcome. |

The honest filter is this question: will the extra borrowing get me to graduation, or is it covering a hole that will still be there next term? If it is the first, a top-up is sensible and cheap relative to the alternatives. If it is the second, a top-up just makes the EMI after the moratorium larger without solving anything.

Remember that everything you add through a top-up sits inside the same moratorium structure. Interest accrues on it from the day it is disbursed, and on most education loans for abroad studies that interest is capitalized into your principal at the end of the moratorium. A top-up taken in the second year still compounds for the rest of your course. The mechanics are the same as the original loan, covered in detail in our post on the education loan moratorium period and interest.

Faz's ruleA top-up should get you to graduation, not paper over a hole that returns next term.

Before you apply, write down exactly what the money is for and whether it is finite. A fee revision is finite. A spending pattern is not. If you cannot point to a documented, course-essential reason, you are not solving a funding gap, you are enlarging a problem.

Which lenders allow a top-up and how the process differs

Most public sector banks and the major NBFCs that fund abroad education allow a top-up or an enhancement of the sanctioned limit, but the path is not identical everywhere.

Public sector banks generally treat a top-up as an enhancement of the original sanction. You apply at the same branch, the request goes through the same credit process, and on a secured loan the collateral is revalued to confirm it still covers the higher exposure. State Bank of India and similar lenders document the process under their education loan schemes, and you can review the current product terms on the SBI education loans page.

NBFCs that specialise in abroad education are often quicker on a top-up because their credit models are built to revisit a file. They already hold your co-applicant income proof, your academic record, and your repayment behaviour, so an enhancement can move faster than a first-time application.

The reason a top-up is generally faster than a fresh loan from a new lender is simple: your creditworthiness is already on the lender’s books. They are not assessing you from zero. They are confirming that the additional exposure is still justified. That said, “faster” does not mean “guaranteed.” A top-up still goes through underwriting.

Two rechecks decide the outcome:

Co-applicant income recheck. The lender reapplies its income-to-obligation ratio test, often called FOIR, to the higher total loan amount. If your co-applicant’s income has not changed but the loan has grown, the ratio is tighter. If the co-applicant has taken on other debt since the original sanction, the recheck can fail even when the original loan sailed through.

Collateral revaluation on secured loans. If your original loan was backed by property or a fixed deposit, the lender revalues that security to confirm it still covers the enhanced amount with the margin the scheme requires. A top-up can be declined or capped purely because the collateral no longer stretches far enough, even though nothing is wrong with you as a borrower.

You will also need fresh paperwork: the revised fee letter or invoice from the institution, updated co-applicant income proof, and on secured loans the documents for the revaluation. The standard list is in our post on the documents required for an education loan.

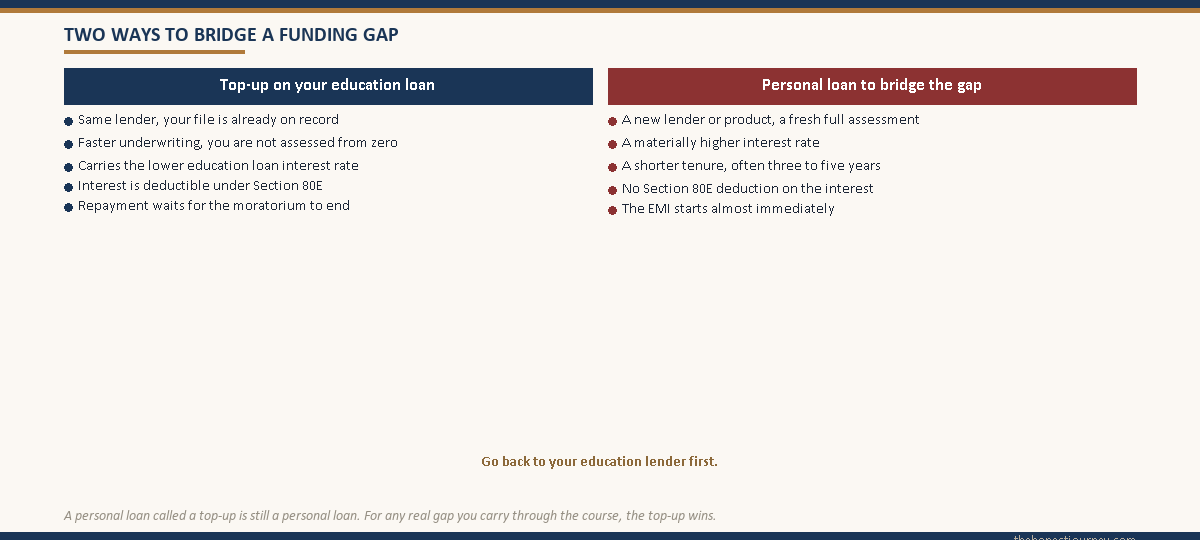

The personal loan trap

This is the part most lender blogs skip, and it is the most expensive mistake a student in a funding crunch makes.

When a gap appears and the student panics, the fastest-looking option is often a personal loan. The marketing is everywhere, approval is quick, and no one revalues a collateral. So the family takes a personal loan, calls it a “top-up” in conversation, and feels the problem is solved.

It is not solved. It is made worse in three specific ways.

The rate is far higher. Education loans for abroad studies typically run in the region of 8.5 to 14 percent depending on whether they are secured or unsecured. Unsecured personal loans commonly sit well above that, frequently in the mid-teens and higher. On a 5 lakh gap, that rate difference is tens of thousands of rupees a year in extra interest.

The tenure is shorter. Personal loans are usually structured over 3 to 5 years with no moratorium. The EMI starts almost immediately. So a family already stretched by a funding gap now has a second EMI running while the student is still studying and earning nothing.

You lose the Section 80E tax benefit. Interest paid on an education loan from an approved lender is deductible under Section 80E of the Income Tax Act, with no upper cap on the deduction, for up to 8 years from the start of repayment. Interest on a personal loan gets none of this. You can confirm the scope of the deduction directly on the Income Tax Department site, and we cover it in full in our post on the education loan tax benefit under Section 80E.

| Feature | Education loan top-up | Personal loan used as a top-up |

|---|---|---|

| Typical interest rate | Education loan rate, lower | Personal loan rate, materially higher |

| Repayment starts | After the moratorium, with the main loan | Almost immediately, no moratorium |

| Tenure | Long, aligned to the education loan | Short, usually 3 to 5 years |

| Section 80E deduction | Yes, on the interest | No |

| Collateral | Same security, revalued if secured | Usually unsecured, no collateral check |

The only honest situation where a personal loan is reasonable is a genuinely tiny, very short gap that you can clear in months, where the convenience outweighs the rate. For any real funding shortfall that you will carry through the rest of the course, the education loan top-up is the correct route, and it is worth waiting the extra few days for the underwriting to clear.

Faz's ruleA personal loan called a top-up is still a personal loan: higher rate, immediate EMI, no 80E.

I have seen families pay back a 4 lakh personal loan with the same effort a 7 lakh education loan top-up would have cost. The word people use does not change the product. Go back to your education lender first, every time.

Top-up versus a second education loan

A top-up and a second education loan are not the same thing, and people confuse them.

A top-up is more money for the same course you are already studying. It enhances the existing loan because the original purpose has not changed, only the cost has.

A second education loan is a separate loan for a different course. A student finishes a master’s, works for a few years, then decides to do another degree, an MBA, a specialised diploma, a doctorate. That is a new education loan with its own sanction, its own moratorium, and its own repayment schedule.

A second education loan is allowed. There is no rule against having had a prior education loan. But it is assessed fresh and strictly, and the assessment is stricter precisely because of the first loan. If the first loan is still being repaid, that EMI counts as an existing obligation against your co-applicant’s income, and it eats directly into the FOIR headroom for the new loan. The cleaner the repayment record on the first loan, the easier the second one is to obtain. A default or even a patchy record on the first loan makes the second very hard.

The framework lenders use is set out in the Indian Banks’ Association Model Education Loan Scheme, which the Indian Banks’ Association publishes, and which most banks adapt for their own products. The Reserve Bank of India’s guidance on fair lending and borrower transparency, available on the RBI site, applies to top-ups and second loans the same way it applies to the original sanction.

Plan the loan amount right the first time

A top-up is a useful safety valve. It is not a substitute for getting the original loan amount right, because every top-up adds principal that then compounds through whatever is left of your moratorium.

When you size the original loan, three honest habits prevent most mid-course gaps:

Budget living costs for the real city. Look up actual rent for student accommodation in the specific city, not the national average the brochure quotes. Add first-month deposits and setup costs. Then add a genuine buffer, not a token one.

Build in a forex cushion. Do not size the loan assuming today’s exchange rate holds for two years. It will not. A sensible cushion on the forex-denominated portion of your costs absorbs an ordinary currency move without a top-up.

Account for fee revisions across the full course. If the university only publishes year-one fees, assume a reasonable annual increase for the later years and include it in the sanction request. It is much cheaper to have the amount sanctioned upfront than to come back for it.

There is a real cost to over-borrowing too, so this is not an argument for taking the maximum. It is an argument for an honest estimate. A loan sized to a realistic full-course budget, including a forex cushion, rarely needs a top-up. A loan sized to an optimistic brochure budget almost always does. The role of margin money in how much you actually need to fund yourself is covered in our post on margin money in an education loan explained.

The honest closing take

A top-up is one of the more borrower-friendly features in the education loan system. It exists because the people who designed these products know that costs move after sanction, and it gives you a low-rate, tax-efficient way to close a genuine gap without leaving the education loan framework. Used for what it is meant for, it is a sensible tool and you should not feel any shame in asking for one.

The mistakes are at the edges. Treating a top-up as a way to cover an EMI you cannot pay turns a funding gap into a debt spiral. Reaching for a personal loan because it looks faster swaps a cheap, deductible loan for an expensive, non-deductible one. And leaning on the existence of top-ups as a reason to under-budget the original loan just means you compound the same money at a worse point in the moratorium.

The cleanest version of this story is the one where you never need a top-up at all, because you sized the original loan to a realistic full-course budget with a forex cushion built in. The second cleanest is the one where a genuine, documented gap appears and you go straight back to your education lender and close it properly. Both of those are fine outcomes. Which path you end up on depends on choices you make before you sign, and on whom you call first when the gap appears. That decision is yours to make.

FAQ

What is a top-up education loan?

A top-up education loan is an additional amount sanctioned on an education loan you already hold, used to cover a genuine funding gap that appears mid-course. Common triggers are a university fee revision, a weaker rupee making forex fees costlier, or living costs that turned out higher than budgeted. The extra amount is usually folded into your existing loan account, the same moratorium, and the same interest basis, rather than created as a brand-new loan.

Can I increase my education loan amount after it is sanctioned?

Yes, most public sector banks and major NBFCs allow an enhancement of the sanctioned limit. You apply to the same lender with documentary proof of the gap, such as a revised fee letter, and the request goes through underwriting again. The lender rechecks your co-applicant income and, on a secured loan, revalues the collateral. Approval is likely if the gap is genuine and your co-applicant income still supports the higher total comfortably.

Is a top-up loan faster to get than a fresh loan?

Usually, yes. Your lender already holds your file: co-applicant income proof, academic record, and repayment behaviour. They are confirming that a larger exposure is still justified rather than assessing you from zero, so underwriting tends to move faster than a first-time application with a new lender. It is still a credit decision, though, not an automatic disbursement, so allow time for the income recheck and any collateral revaluation.

Can I use a personal loan to top up my education loan?

You can, but it is usually a costly mistake. A personal loan carries a materially higher interest rate, has no moratorium so the EMI starts almost immediately, runs over a shorter tenure, and earns no Section 80E tax deduction on the interest. For any real gap you will carry through the rest of your course, going back to your education lender for a proper top-up is far cheaper. A personal loan only makes sense for a tiny gap you can clear within months.

Does a top-up education loan need fresh collateral?

Not necessarily fresh collateral, but on a secured loan the existing collateral is revalued. The lender confirms the property or fixed deposit still covers the enhanced loan amount with the margin the scheme requires. If the security no longer stretches far enough, the top-up can be capped or declined. On an unsecured loan, there is no collateral check, but the co-applicant income recheck against the larger amount becomes the deciding factor instead.

Can I get a second education loan for another degree?

Yes. There is no rule against taking a second education loan for a different course, such as an MBA or a doctorate after a master’s. It is assessed fresh and strictly. If the first loan is still being repaid, that EMI counts as an existing obligation against your co-applicant’s income and reduces the headroom for the new loan. A clean repayment record on the first loan makes the second much easier to obtain.

Does the interest rate change on a top-up education loan?

The top-up amount is generally charged at the lender’s prevailing education loan rate at the time of the enhancement, which may differ from the rate on your original disbursement if benchmark rates have moved. It is still an education loan rate, well below a personal loan rate. Ask your lender in writing how the top-up portion is priced and whether it carries the same or a separate rate before you accept the enhancement.

Will interest accrue on the top-up amount during the moratorium?

Yes. A top-up sits inside the same moratorium structure as your main loan, so interest accrues on the additional amount from the day it is disbursed. On most education loans for abroad studies, that interest is capitalized into your principal at the end of the moratorium. A top-up taken in the second year still compounds for the remaining course duration, so it adds to the outstanding balance you start repaying after the moratorium ends.

Faz · The Honest Journey · 2026