Yes, interest accrues every month during the moratorium, your course plus a 6 to 12 month grace period, and most banks capitalise it onto your principal. On a 20 lakh loan at 11.5 percent with a 30 month moratorium, roughly 5.75 lakh gets added, so you start repaying on 25.75 lakh. Pay just the interest while studying and you avoid that entirely.

The relationship manager who called after your loan was sanctioned used the word “benefit.” The moratorium period, he said, gives you time to focus on your studies without worrying about EMIs. He is right. The moratorium is a benefit. It is just not a free one, and the cost he did not mention is the part that catches people off guard two years later when the repayment statement arrives and the outstanding balance is not ₹20 lakh anymore.

This post runs the actual numbers. If you just got a sanction letter and you are trying to figure out what you actually signed, this is the post you need to read before your first disbursement.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

What the moratorium period actually is

A moratorium period in an education loan is the window during which you are not required to pay EMIs. For abroad studies, it typically covers your course duration plus a grace period of 6 to 12 months after you finish. So on a 2-year master’s program, the moratorium might run 30 months (24 + 6) or 36 months (24 + 12) depending on your lender and your loan agreement. On a private MBBS education loan for an abroad course, it can stretch to 60 months (48 + 12).

Faz's rule

The moratorium is a period without EMI, not a period without interest.

Most families conflate these and discover the difference when EMI starts at the inflated number. Interest accrues every month during the moratorium on the principal disbursed; if you don’t service it, it capitalises into the principal.

What the moratorium does not mean: the interest stops. The bank’s cost of capital does not take a holiday because you are in class. Interest accrues every single month on your outstanding principal from the day of first disbursement. The only question is what happens to that accrued interest.

In most Indian education loans, especially from public sector banks and the major NBFCs that fund abroad studies, the accrued interest during the moratorium is capitalized. That means it gets added to your principal at the end of the moratorium period. You are now repaying interest on interest. This is the trap the relationship manager’s product brochure does not headline.

The math nobody shows you at sanction time

Let us use a real scenario: ₹20 lakh loan at 11.5% per annum. These numbers are not hypothetical. They are typical of what students with a solid co-applicant profile and a well-ranked university were getting sanctioned in 2025-26 from NBFCs and some private banks.

Monthly interest accrual = ₹19,167

(₹20,00,000 × 11.5% ÷ 12 = ₹19,167 per month)

Now run this across the different moratorium windows:

| Scenario | Moratorium length | Interest capitalized | Balance at EMI start |

|---|---|---|---|

| 2-year course, 6-month grace | 30 months | ₹5,75,000 | ₹25,75,000 |

| 2-year course, 12-month grace | 36 months | ₹6,90,000 | ₹26,90,000 |

| 4-year MBBS, 12-month grace | 60 months | ₹11,50,000 | ₹31,50,000 |

You borrowed ₹20 lakh. Before you make a single repayment, you owe ₹25.75 lakh. That ₹5.75 lakh did not appear because of any fee or hidden charge. It appeared because compound interest worked exactly as designed, and you did not know it was running.

Faz's rule

The moratorium is a repayment holiday, not an interest holiday. The meter runs from day one.

The bank’s cost of funds does not stop because you are in class. Every month of the moratorium is another ₹15,000-25,000 being added to what you owe. The only question is whether you manage it actively or discover the total at EMI start.

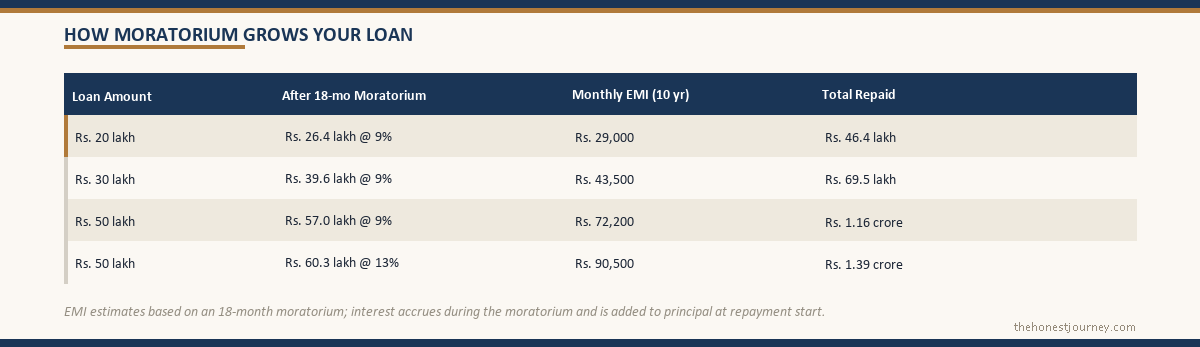

What this does to your EMI and total repayment

The capitalized balance becomes your new principal. Your 10-year repayment clock starts from there. Here is what that looks like in hard numbers, all calculated at 11.5% over 10 years (120 months):

Faz's rule

Servicing interest during moratorium costs ₹11L upfront. Capitalising it costs ₹18.2L extra over the loan life.

On a ₹40L abroad-studies loan at 11% with a 30-month moratorium and 10-year repayment. Net saving from servicing interest during studies: ₹7L. The decision is rarely framed this way at sanction stage.

| Starting balance | Scenario | Monthly EMI | Total repaid | Total interest paid |

|---|---|---|---|---|

| ₹20,00,000 | No moratorium (immediate repayment) | ₹28,420 | ₹34,10,400 | ₹14,10,400 |

| ₹25,75,000 | 30-month moratorium (2yr + 6mo grace) | ₹36,587 | ₹43,90,440 | ₹18,15,440 |

| ₹26,90,000 | 36-month moratorium (2yr + 12mo grace) | ₹38,220 | ₹45,86,400 | ₹18,96,400 |

| ₹31,50,000 | 60-month moratorium (4yr MBBS + 12mo grace) | ₹44,760 | ₹53,71,200 | ₹22,21,200 |

Read that bottom row carefully. On a 4-year MBBS program with a standard 12-month grace period, a ₹20 lakh loan at 11.5% results in ₹53.7 lakh repaid over the loan tenure. You borrowed ₹20 lakh. You repay ₹53.7 lakh. The moratorium alone added ₹11.5 lakh to your principal before repayment even began.

For the 2-year master’s scenario that most readers here are looking at: you borrowed ₹20 lakh, you repay ₹43.9 lakh, and your EMI the month you finish your grace period is ₹36,587. If your first job out of grad school pays ₹50,000 take-home, that EMI is 73% of your monthly income before rent. That math does not work and it was visible in the sanction letter the day you signed it.

Faz's rule

Ask the bank one question before signing: what is my outstanding balance at the end of the moratorium period?

Not the EMI. The outstanding balance. Most banks will calculate this if you ask. The gap between what you borrowed and what you owe at EMI start is the single most important number in your loan, and almost no one checks it at sanction time.

The government subsidy exception (and why most abroad students do not qualify)

There is a real exception to this trap and it is worth understanding clearly. The Central Sector Interest Subsidy scheme, known as CSIS, covers the full interest during the moratorium period for students from families with a parental annual income below ₹4.5 lakh. If you qualify, the government pays the accruing interest to the bank during your moratorium. You start repayment on the original principal only. No capitalization. The trap does not apply to you.

But here is the honest part: most students pursuing abroad education do not come from families earning below ₹4.5 lakh annually. The CSIS scheme was designed primarily for domestic higher education. The income ceiling that made sense for an engineering seat at a state college becomes an extremely low bar when the tuition alone is ₹15-30 lakh a year. If your family can arrange a co-applicant with enough income to pass FOIR checks at a major NBFC, you almost certainly earn more than ₹4.5 lakh, which means CSIS is not your safety net.

There is also a revised version of the scheme with a higher income ceiling for education loans accessed via the PM Vidyalakshmi portal. The specifics are worth checking at the time you apply, because the numbers do shift. But the broad reality remains: the majority of students funding a master’s or an MBBS abroad are outside the subsidy bracket and are looking at full interest capitalization.

What you can actually do about it

The moratorium is a structural feature of almost every education loan product for abroad studies. You cannot usually opt out of it. But you are not without options.

Pay simple interest during the moratorium. This is the single most impactful move available to you. Most lenders allow partial payments during the moratorium. If you or your family can pay even the monthly interest (₹19,167 in the ₹20L example), you prevent capitalization entirely. You arrive at EMI start with the original ₹20L balance, not ₹25.75L. The EMI drops from ₹36,587 to ₹28,420 and total repayment drops by nearly ₹10 lakh. If you have a part-time job during your studies, directing even half the monthly interest toward the loan changes the outcome materially.

Make partial payments when you can. Even irregular lump-sum payments during the moratorium reduce the principal on which interest accrues. A ₹1 lakh payment in month 6 of your program reduces the compounding base for the remaining 24 months. The math is not as clean as consistent interest servicing, but it is better than nothing.

Ask the bank upfront whether they apply simple or compound interest during the moratorium. The RBI master directions on lending require that accrued interest during a moratorium be communicated clearly. Some lenders apply simple interest on the original principal throughout the moratorium and capitalize it once at the end. Others compound monthly. The difference over 30-36 months is not huge at these principal sizes (compounding at 11.5% monthly vs. simple interest over 30 months is a difference of roughly ₹40,000-60,000 on ₹20L), but it matters and you are entitled to know which method your lender uses before you sign.

Know the number before you sign. Ask your relationship manager to give you, in writing, the projected outstanding balance at the end of the moratorium period. Any bank that has run the disbursement schedule can produce this number. If they cannot or will not, that tells you something about how they handle transparency.

If you are still at the research stage and have not signed yet, this is also a reason to look closely at collateral-secured loans from public sector banks, which tend to carry lower interest rates (8.5 to 10 percent vs 11.5 to 14 percent from NBFCs, compared in detail in the bank vs NBFC interest rate post). The rate difference is meaningful in moratorium math: at 9.5% on ₹20L, the monthly interest accrual is ₹15,833 instead of ₹19,167. Over 30 months, that is ₹4.75L capitalized instead of ₹5.75L. A 1-2% rate gap compounds into a significant EMI difference. For more on the unsecured vs. collateral tradeoff, see the education loan without collateral post.

One more thing worth knowing: the interest you pay on an education loan, including during the moratorium if you service it, qualifies for a deduction under Section 80E of the Income Tax Act. There is no cap on the deduction amount and it applies for 8 years from the year you start repayment. If your co-applicant (typically a parent) is on the old tax regime, this is real money. The full rules are covered in the Section 80E education loan tax benefit post.

The honest closing take

The moratorium period did not create your financial problem. It revealed it. If the loan was sized correctly relative to your expected earning potential, a 30-month moratorium and a ₹36,000 EMI is manageable. If the loan was oversized (because the bank approved the maximum it could justify under FOIR and you took the full amount without running the post-moratorium EMI math) then the capitalization is simply the mechanism that makes the problem visible.

The number that matters is not the rate, and it is not even the EMI. It is the ratio of your first-year monthly take-home to your monthly EMI after the moratorium ends. If that ratio is above 40-50%, you either need a higher-paying outcome than you are projecting, a lower loan amount, a shorter moratorium structure, or all three. The bank ran its approval math on FOIR. You need to run your own math on what the EMI looks like the month your grace period ends.

Everything else, the rate negotiations, the tax deductions, the prepayment schedules, is secondary to that one number being survivable on day one of repayment.

Faz's rule

If your first salary after graduation cannot cover the capitalized EMI plus rent at 35% of take-home, the loan amount was wrong, not the moratorium.

A ₹25.75L balance on a 10-year term at 11.5% is ₹36,587/month. If your expected starting salary is ₹50,000/month, that EMI is 73% of take-home before rent. This is not a moratorium problem. It is a loan sizing problem that the moratorium makes visible.

How the moratorium interacts with tranche-wise disbursement

One detail that quietly changes the moratorium math: the bank does not hand you the full ₹20 lakh on day one. Education loans for abroad studies are disbursed in tranches, usually aligned with each semester’s tuition invoice. So in a 2-year master’s program, you might see ₹6 lakh disbursed before semester one, ₹5 lakh before semester two, and so on across four tranches.

This matters because interest accrues only on the amount actually disbursed, not on the full sanctioned figure. If the bank disburses ₹6 lakh in month one, your monthly interest in month one is roughly ₹5,750, not the ₹19,167 you would pay if the whole ₹20 lakh were already in play. The accrual climbs tranche by tranche as more money goes out the door.

The capitalised numbers in the table above are a slight simplification because they assume the full principal accrues from day one. In a real tranche schedule, the actual capitalised interest on a ₹20 lakh, 30-month moratorium loan is closer to ₹4.6 lakh to ₹5.1 lakh rather than the flat ₹5.75 lakh, because the early months carry a smaller outstanding balance. It is still a large number. It is just not quite as brutal as the worst-case flat calculation. Understanding the staggered pattern of tranche-wise disbursement helps you time any interest servicing you plan to do, because servicing makes the biggest difference once the larger later tranches are out.

Ask your lender for the projected disbursement schedule alongside the moratorium balance. The two together give you the only honest picture of what the loan actually costs.

Moratorium on a top-up loan: the trap inside the trap

Plenty of students discover mid-course that the sanctioned amount falls short. The rupee weakened, the university raised fees, or the original cost sheet underestimated living expenses. The fix is usually a top-up loan, and top-up loans carry their own moratorium clock.

Here is what catches people. A top-up taken in the second year of a 2-year program has a shorter remaining course period but the same grace period bolted on. If your original loan finishes its moratorium 30 months after first disbursement, a top-up disbursed 14 months in might run its moratorium 22 to 28 months from its own start date. You can end up with two slightly offset moratorium windows and two separate capitalisation events landing in different months.

The interest rate on a top-up is also frequently higher than the original loan, because the lender is now extending more credit against the same collateral and co-applicant profile. A ₹4 lakh top-up at 13 percent capitalising over a 20-month moratorium adds roughly ₹85,000 to that balance. If you are heading toward a possible top-up, read the education loan top-up post before you sign, and ask the lender to show you the combined post-moratorium EMI across both loans, not each one in isolation. The combined number is the one your salary has to survive.

What the moratorium does to your CIBIL score and future borrowing

A common misconception: that the moratorium pauses everything, including how the loan shows up on your credit report. It does not. From the day of first disbursement, the education loan is a live account on your CIBIL file. It reports as an active loan with an outstanding balance, even though you are not paying EMIs yet.

During the moratorium, as long as you are not required to pay and you do not miss any interest servicing you committed to, the account stays in good standing and does not hurt your score. The risk window opens the month EMIs begin. A missed EMI in month one of repayment, often because the borrower underestimated the capitalised number, is a genuine default that drops your score by 50 to 100 points and stays on the report for years.

There is also a less obvious effect. The capitalised balance is a large outstanding liability on your file. If you apply for a car loan or a personal loan in the first two years of repayment, the lender sees a ₹25 lakh-plus education loan and factors the EMI into your debt-to-income calculation. That can shrink what you are eligible to borrow elsewhere. If you plan to build credit history while studying, understand how the loan sits on your file by reading the CIBIL score and education loan post, and check your report directly through CIBIL once repayment starts. Knowing the borrower rights and grievance routes set out in the RBI notifications for borrowers is worth ten minutes before you sign anything.

If you want to run your own figures, use the education loan moratorium calculator to see exactly how much interest capitalises on your own loan amount and moratorium length.

FAQ

Is interest charged during the moratorium period in education loans?

Yes. Interest accrues from the date of first disbursement, including during the moratorium. The moratorium only means you are not required to pay EMIs during that period. The interest that accrues is typically added to (capitalized into) your principal at the end of the moratorium, which is why your outstanding balance at EMI start is higher than what you originally borrowed.

What is interest capitalization in an education loan?

Interest capitalization is when unpaid interest is added to the loan principal. In the context of an education loan moratorium, it means the monthly interest that accrued while you were studying gets folded into the principal balance. Your EMIs are then calculated on this larger balance, not on the original sanctioned amount. On a ₹20L loan at 11.5% with a 30-month moratorium, roughly ₹5.75L gets capitalized, making the effective principal ₹25.75L at EMI start.

Should I pay interest during the moratorium period?

If you can, yes. Paying simple interest during the moratorium prevents capitalization and is the most effective way to reduce your total repayment cost. It lowers your outstanding balance at EMI start, reduces your monthly EMI, and can save you ₹8-10 lakh in total interest over a 10-year tenure on a ₹20L loan. Even partial interest payments during the moratorium reduce the compounding base and make a meaningful difference.

Does the government subsidize interest during the moratorium?

Yes, under the Central Sector Interest Subsidy (CSIS) scheme, students from families with a parental annual income below ₹4.5 lakh per year are eligible to have the moratorium interest paid by the government. This eliminates capitalization entirely for eligible borrowers. However, most students pursuing abroad education come from families with incomes above this threshold and do not qualify. Always verify the current income ceiling at the time you apply, as the scheme parameters can be updated.

How much does a 3-year moratorium cost on a ₹20 lakh loan at 11.5%?

A 36-month moratorium on a ₹20 lakh loan at 11.5% per annum results in approximately ₹6.90 lakh in capitalized interest, making your outstanding balance ₹26.90 lakh at EMI start. On a 10-year repayment at the same rate, this translates to a monthly EMI of around ₹38,220 and a total repayment of approximately ₹45.86 lakh, compared to ₹34.10 lakh if you had begun repayment immediately on the original ₹20L principal.

Can I prepay during the moratorium period?

Most lenders allow partial prepayments during the moratorium. There is generally no penalty for prepayment on floating-rate education loans as per RBI guidelines, though you should confirm this with your specific lender at the time of sanction. Even small, irregular prepayments during the moratorium reduce the principal on which interest compounds, which lowers the capitalized balance and your eventual EMI. If your lender imposes any restriction on moratorium-period prepayments, get it in writing before signing.