An education loan EMI calculator shows you the EMI on the original sanctioned amount, but the real EMI is calculated on a much larger figure because the moratorium interest gets added to your principal. A ₹30 lakh loan at 10.5 percent with a 4-year moratorium (course + 1 year grace) capitalises into roughly ₹42.6 lakh before EMI starts, pushing the actual EMI on a 10-year tenure from ₹40,492 (calculator number) to about ₹57,500 (real number). The honest total cost is principal plus moratorium interest plus repayment interest, which is what the sanction letter never adds up for you on one line.

Education loan EMI calculator

With the moratorium toggle the bank calculators leave out. See your real EMI after interest capitalises.

Your EMI: —

—

—

—

—

Indicative only. Most banks charge simple interest during the moratorium and capitalise it onto the principal when EMI begins, per the IBA model scheme. Exact figures vary by lender. Confirm against your sanction letter.

The first time I sat with a friend’s education loan sanction letter, the number that jumped out was the EMI. ₹39,800 a month for ten years on a ₹25 lakh loan. We concluded it was manageable. Then his banker called the next week and mentioned the EMI would actually start at closer to ₹56,000 once the moratorium ended. The sanction letter was honest. The EMI calculator was honest. We had just both been reading the wrong number for the wrong moment in the loan’s life.

This post is the math almost no online EMI calculator shows upfront. The moratorium interest. The capitalisation. The reason the EMI that hits your account in year five is meaningfully larger than what the calculator quoted in year zero.

The loan basics nearby: the what education loan covers post, the RBI guidelines education loan post, and the education loan vs personal loan post.

What an education loan EMI calculator actually computes

Every standard EMI calculator uses the reducing balance formula. You feed it three inputs (principal P, monthly rate r, number of months n) and it returns the equated monthly instalment. The formula is EMI = P × r × (1+r)^n / ((1+r)^n – 1). For a ₹30 lakh loan at 10.5 percent over 10 years (120 months), r = 0.00875 and n = 120. The EMI works out to ₹40,492. Total repayment is ₹48.59 lakh. Interest cost is ₹18.59 lakh. Clean and easy to plan around.

The problem is the calculation pretends EMI starts on day one. For most consumer loans that assumption is correct. For an education loan it almost never is. Education loans have a moratorium period. During the moratorium you are not paying EMI, but the lender is still charging interest, and that interest does not disappear. It gets added back into the principal, a process called capitalisation, and the EMI you eventually pay is calculated on that larger, post-moratorium number.

The moratorium: why the calculator number is the wrong number

Under the IBA Model Education Loan Scheme, the moratorium is the course duration plus a grace period of 6 to 12 months. For a 2-year Master’s abroad it is typically 2 + 1 = 3 years. For a 4-year engineering UG it is 4 + 1 = 5 years. For an MBA, 2 + 1 = 3 years. The grace period exists because the lender accepts you will not have a job the day you finish the course.

During the moratorium, you have three choices:

| Choice | What you pay during moratorium | What happens to the unpaid interest |

|---|---|---|

| Full servicing | Monthly interest in full | Nothing to capitalise. Principal stays at original amount |

| Simple interest servicing | Only simple interest each month | Nothing to capitalise. Same as full servicing |

| Nothing (most common) | Zero | Interest accrues monthly and gets added to principal |

The third option is what most students pick, because the whole point of taking a loan was that the family did not have the money to pay anything during the course. The lender allows it. There is no penalty. But it is also where the calculator number quietly stops being true.

Faz's ruleThe sanction letter shows the EMI on the original principal, not the EMI you will actually pay. Ask the banker for the post-capitalisation EMI before you sign.

Banks quote the smaller number because it is technically correct (that EMI does apply if you service interest during the moratorium). But most borrowers do not, so the smaller number on the sanction letter is the number you will never actually pay. Ask explicitly: “What will the EMI be if I do not service interest during the moratorium?” That is the number to plan your future salary around.

How capitalisation actually works (the worked example)

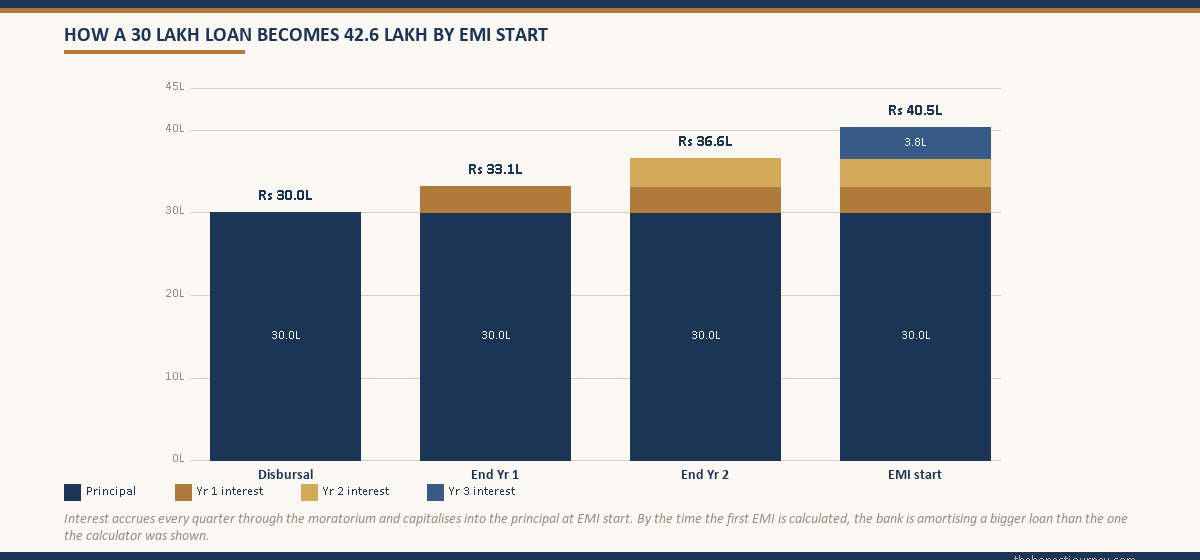

Take a ₹30 lakh loan at 10.5 percent, 2-year Master’s abroad, 3-year moratorium (2 + 1), 10-year repayment after moratorium ends. Disbursement in 4 semester tranches of ₹7.5 lakh each, every six months.

Moratorium interest is calculated tranche by tranche, on the outstanding balance, at simple or compound interest depending on the lender. Most PSU banks use simple interest during moratorium and convert to compound at EMI start. Most NBFCs use compound interest throughout. We will use the PSU model below.

Tranche-wise interest accrual during the 3-year moratorium:

| Tranche | Amount | Months outstanding in moratorium | Interest accrued at 10.5% p.a. |

|---|---|---|---|

| 1 (Sem 1) | ₹7.5 lakh | 36 | ₹2,36,250 |

| 2 (Sem 2) | ₹7.5 lakh | 30 | ₹1,96,875 |

| 3 (Sem 3) | ₹7.5 lakh | 24 | ₹1,57,500 |

| 4 (Sem 4) | ₹7.5 lakh | 18 | ₹1,18,125 |

| Total interest accrued | ₹7,08,750 |

So by moratorium end, the borrower owes ₹30 lakh + ₹7.08 lakh = ₹37.08 lakh. That accrued ₹7.08 lakh is capitalised and EMI is calculated on ₹37.08 lakh, not ₹30 lakh. Run the EMI formula with P = ₹37,08,750, r = 0.00875, n = 120, and the EMI works out to ₹50,051 per month. Total repayment over 10 years is ₹60.06 lakh. Total interest cost (moratorium + repayment) is ₹30.06 lakh, more than the original principal.

If the lender compounds during moratorium (the NBFC case), accrued interest is closer to ₹8.5 to ₹10.5 lakh, the capitalised principal is ₹40 to ₹42.6 lakh, and the 10-year EMI climbs to ₹54,000 to ₹57,500. The original calculator quote of ₹40,492 was off by 35 to 42 percent.

What the sanction letter actually shows you

Read your sanction letter carefully. It typically lists four numbers near the EMI line. Sanctioned amount, the original loan (e.g. ₹30 lakh). Rate of interest, usually a margin above the lender’s external benchmark like EBLR + 2 percent. For PSU banks the effective rate in 2026 sits in the 9.5 to 11.25 percent band; for NBFCs it is 11 to 14 percent. Moratorium period, course duration plus grace, e.g. 36 months. Indicative EMI, the number that catches your eye.

The honest sanction letters from PSU banks (SBI, BoB, Canara) print two EMIs: one assuming you service interest during moratorium (smaller) and one assuming you do not (larger, capitalised). The less honest letters print only the first. If yours shows only one EMI, it is almost certainly the smaller one. Document-level checks before you sign are covered in the moratorium interest guide.

Faz's ruleCompute the capitalised principal yourself before signing. Sanctioned amount + (sanctioned amount × rate × moratorium years × 0.6) is a quick estimate for staggered disbursement at simple interest.

The 0.6 multiplier accounts for the staggered tranche release (not the full principal accrues interest for the full moratorium). For ₹30L at 10.5% over 3 years, the estimate is 30 + (30 × 0.105 × 3 × 0.6) = 30 + 5.67 = ₹35.67 lakh, close to the ₹37 lakh actual figure. Good enough for a sanity check at the kitchen table.

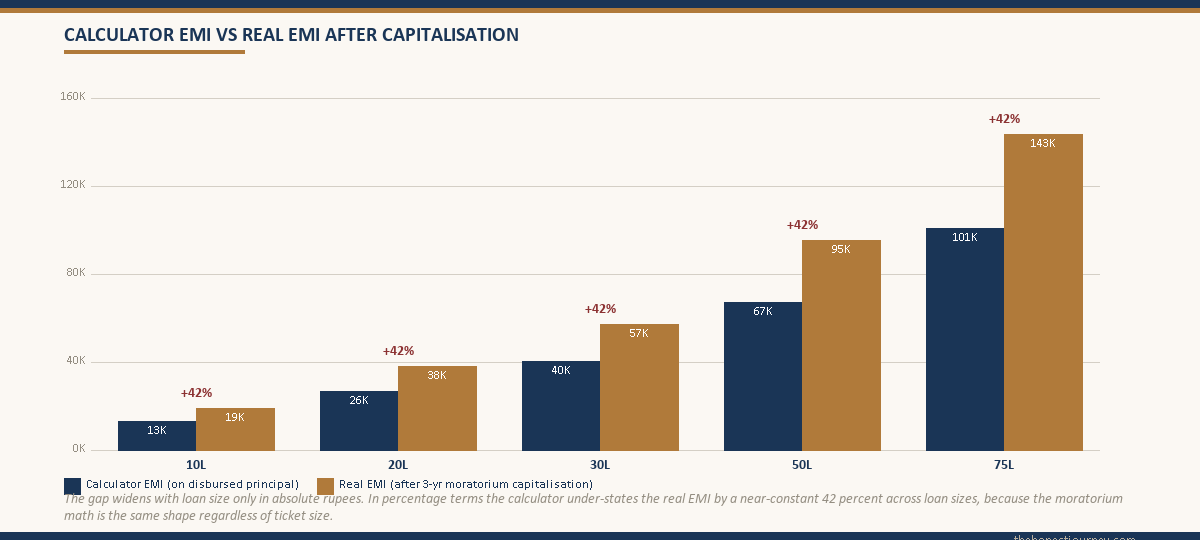

The honest total cost table for typical loan sizes

Below is what the real total cost looks like across common education loan amounts. Assumptions: 10.5 percent annual interest (mid-band PSU rate), 3-year moratorium (2-year Master’s abroad with 1-year grace), 10-year repayment, no interest servicing during moratorium, simple-interest accrual converted to compound at EMI start.

| Sanctioned amount | Calculator EMI (on original P) | Capitalised principal at EMI start | Real EMI (post-capitalisation) | Total amount paid over 10 years | Total interest cost |

|---|---|---|---|---|---|

| ₹10 lakh | ₹13,493 | ₹12,36,250 | ₹16,683 | ₹20.02 lakh | ₹10.02 lakh |

| ₹20 lakh | ₹26,987 | ₹24,72,500 | ₹33,366 | ₹40.04 lakh | ₹20.04 lakh |

| ₹30 lakh | ₹40,492 | ₹37,08,750 | ₹50,051 | ₹60.06 lakh | ₹30.06 lakh |

| ₹50 lakh | ₹67,486 | ₹61,81,250 | ₹83,418 | ₹100.10 lakh | ₹50.10 lakh |

| ₹75 lakh | ₹1,01,228 | ₹92,71,875 | ₹1,25,128 | ₹150.15 lakh | ₹75.15 lakh |

The pattern is consistent. The real EMI is roughly 23 to 25 percent higher than the calculator quote, and total interest paid over the life of the loan is close to (and sometimes exceeds) the original principal. For a ₹30 lakh loan, you end up repaying ₹60 lakh. That is the honest number.

Why the EMI is what it is (the reducing balance mechanic)

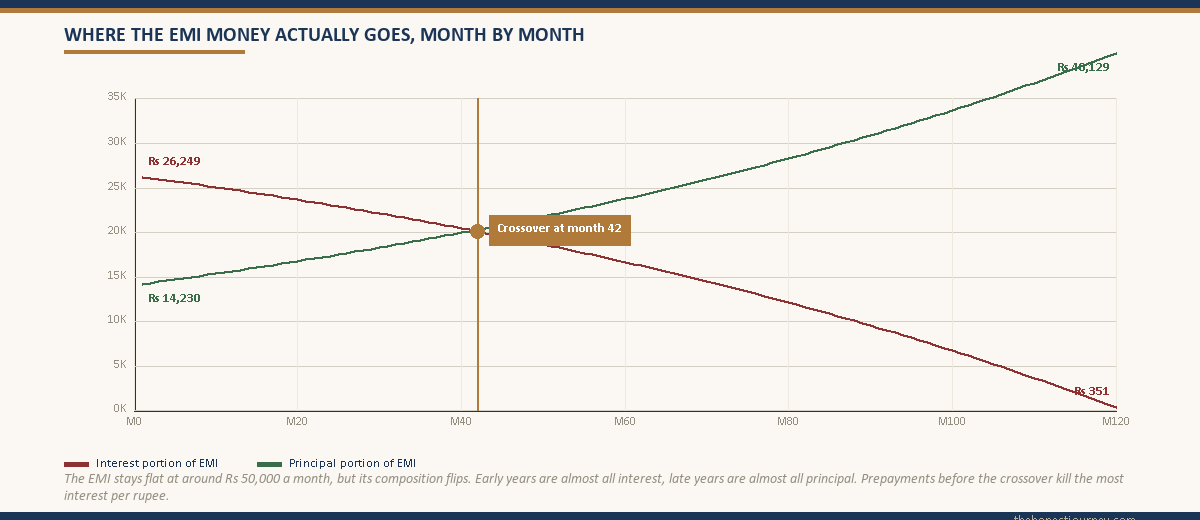

Education loan EMIs work on the reducing balance method, the same as a home loan. Each EMI is split between interest (on the current outstanding) and principal (the rest). In the early months of EMI, almost the entire payment is interest. The principal barely moves. By year 7 or 8, the split flips and most of each EMI is chipping away at the principal.

For a ₹37.08 lakh capitalised principal at 10.5 percent over 10 years, the first EMI of ₹50,051 splits as ₹32,445 interest and ₹17,606 principal. By month 60 the split is roughly ₹22,300 interest and ₹27,750 principal. By month 120 it is ₹434 interest and ₹49,617 principal. Total repayment-phase interest is ₹23 lakh on top of ₹7.08 lakh of moratorium interest, for a combined ₹30 lakh on a ₹30 lakh loan.

This is why prepayment in the early years has such an outsized effect. Every rupee of prepayment in year 1 or 2 reduces the principal that interest will accrue on for the next 8 to 9 years. The same prepayment in year 8 or 9 is almost wasted because most interest is already paid. The arithmetic of when prepayment beats 80E tax benefit is in the broader India education loan guide.

What lowers the real EMI (and what does not)

Three levers actually move the real EMI. Two are widely advertised. The third is the one that matters most and is barely mentioned.

Lower rate. Every 50 basis points off the rate cuts EMI by 2.5 to 3 percent. A PSU loan at 9.75 percent versus an NBFC at 12.5 percent on a ₹30 lakh ticket saves ₹8 to ₹10 lakh across the loan’s life. The rate is set by CIBIL, collateral, and institution. Baselines sit in RBI’s monthly lending rate data.

Longer tenure. Stretching repayment from 10 to 15 years drops EMI by 18 to 22 percent but raises total interest sharply. On a ₹37.08 lakh capitalised principal, 15-year EMI is ₹40,990 but total repayment is ₹73.78 lakh, versus ₹60.06 lakh on 10 years. Lower EMI, higher total cost. The trade is real.

Service interest during the moratorium. The lever almost no one uses, and the one with the cleanest math. If you (or your parents) pay just the monthly interest during the 3-year moratorium, nothing capitalises. EMI is calculated on the original ₹30 lakh, not ₹37.08 lakh. It drops from ₹50,051 to ₹40,492. Monthly moratorium interest starts at about ₹6,500 in year 1 and climbs to ₹26,000 by year 3 as more tranches release. Across 3 years the family pays roughly ₹6.5 to ₹7 lakh, and total loan cost drops by ₹4 to ₹5 lakh because you avoid 10 years of interest-on-interest.

Faz's ruleIf the family has any monthly slack, service the moratorium interest. It is the highest-return rupee you will spend on the loan.

Every ₹1 of moratorium interest paid out of pocket saves about ₹0.65 to ₹0.75 of compounded interest later. No mutual fund returns that. The full economics of paying versus not paying during moratorium are in the honest repayment guide.

One detail about Section 80E that changes the math

Section 80E lets you deduct the entire interest paid on an education loan from taxable income, with no upper cap, for up to 8 years from the year EMI starts. Principal is not deductible. For a borrower in the 30 percent bracket, every ₹1 lakh of interest paid saves ₹31,200 in tax (30 percent + 4 percent cess).

On a ₹30 lakh loan with ₹30 lakh of total interest, the theoretical maximum 80E benefit at 30 percent bracket is ₹9.36 lakh. Since 80E only applies for 8 years and the interest portion of EMI declines over time, the realistic benefit is ₹6 to ₹7 lakh. That drops the after-tax cost of a ₹30 lakh loan from ₹60 lakh of total repayment to ₹53 to ₹54 lakh. Eligibility and timing are in the Section 80E guide. The text sits on the Income Tax India portal.

The honest closing take

An EMI calculator is useful, but only if you feed it the right principal. The right principal for an education loan is not the sanctioned amount. It is the sanctioned amount plus moratorium interest, computed for the actual moratorium length on the actual tranche schedule. Almost no online calculator does this in one screen. The PSU lenders, particularly SBI and Bank of Baroda, will run the capitalised EMI if you ask. NBFCs usually will not volunteer it.

The cost of not asking is the difference between planning around a ₹40,000 EMI and discovering, five years in, that the real number is ₹56,000. The math is not hard. The discipline is running it once, with honest inputs, before you sign. If you have a sanction letter in front of you, do the 0.6 estimate from the callout above, compare it to the bank’s quote, and ask the banker to reconcile the two. Their answer (or their hesitation) tells you everything about how the loan will feel in year 5.

FAQ

How is education loan EMI calculated in India?

Education loan EMI uses the reducing balance formula: EMI = P × r × (1+r)^n / ((1+r)^n – 1), where P is principal, r is monthly rate, n is months. The catch is the P used at EMI start is not the sanctioned amount. It is the sanctioned amount plus all the interest accrued during the moratorium, which gets capitalised into the principal. The lender applies the formula to that larger figure, which is why the real EMI is meaningfully higher than the calculator quote on the original loan amount.

Why is my education loan EMI higher than the calculator showed?

Because the calculator computed EMI on the original sanctioned amount, but the lender computes it on the post-moratorium capitalised principal. During the moratorium (3 to 5 years for an abroad Master’s or Indian engineering degree), interest accrues on disbursed tranches and gets added to the loan. By EMI start the principal is 20 to 40 percent larger than what you originally borrowed. For a ₹30 lakh loan at 10.5 percent with a 3-year moratorium, the calculator quotes ₹40,492 but the real EMI starts at roughly ₹50,051.

What is capitalised interest in an education loan?

Capitalised interest is the interest that accrues during the moratorium but is not paid by you, so the lender adds it to the principal at the end of the moratorium. Future interest is then charged on the larger combined amount, including the capitalised interest itself (interest on interest). Most students do not service interest during the moratorium because they have no income. The bank allows it. The trade-off is a larger principal at EMI start and a lifetime loan cost 30 to 40 percent higher than if interest were serviced as accrued.

How does moratorium increase the total cost of the loan?

Two compounding ways. First, accrued moratorium interest is added to the principal, so you start paying EMI on a larger amount. Second, that capitalised interest itself attracts compound interest across the 10 to 15 year repayment tenure, meaning you pay interest on interest for a decade. On a ₹30 lakh loan at 10.5 percent with a 3-year moratorium, the moratorium adds about ₹7 lakh to principal, and the extra interest from that ₹7 lakh over the 10-year repayment phase is roughly ₹4.5 to ₹5 lakh, on top of the moratorium interest itself.

What is the real EMI on a ₹30 lakh education loan?

At 10.5 percent annual interest, 3-year moratorium (typical 2-year Master’s plus 1-year grace), 10-year repayment, no interest servicing during moratorium, and simple-interest accrual that converts to compound at EMI start, the moratorium interest accrues to roughly ₹7.08 lakh. The capitalised principal at EMI start is ₹37.08 lakh. The real EMI works out to about ₹50,051 per month. Total repayment over 10 years is ₹60.06 lakh, total interest is ₹30 lakh, almost equal to the original principal. The calculator quote of ₹40,492 is not the real number.

How can I lower my education loan EMI?

Three levers actually work. Negotiate a lower rate by improving co-applicant CIBIL, providing collateral, or choosing a PSU bank over an NBFC where rates run 11 to 14 percent. Each 50 basis points off the rate cuts EMI by 2.5 to 3 percent. Extend repayment tenure from 10 to 15 years, which drops EMI by 18 to 22 percent but raises total interest paid. The most underused lever, service monthly interest during the moratorium so nothing capitalises. On a ₹30 lakh loan this drops post-moratorium EMI from ₹50,051 to ₹40,492.

Is there a difference between simple and compound interest during moratorium?

Yes, and it matters. PSU banks typically charge simple interest during the moratorium and convert the accrued amount into principal at EMI start, after which compound interest applies. NBFCs (Avanse, Credila, Auxilo) usually charge compound interest throughout, including during moratorium. On a ₹30 lakh loan with a 3-year moratorium at 10.5 percent, simple interest accrues to about ₹7.08 lakh while compound interest accrues to roughly ₹10.5 lakh. That ₹3.4 lakh gap is the cost of choosing an NBFC over a PSU bank just on moratorium math.

Does Section 80E change the real cost of the loan?

Yes, materially. Section 80E lets you deduct the entire interest paid on an education loan from taxable income, with no upper cap, for up to 8 years from the year EMI starts. For a borrower in the 30 percent bracket, every ₹1 lakh of interest paid reduces tax by ₹31,200. On a ₹30 lakh loan with ₹30 lakh total interest cost across moratorium and repayment, the realistic 80E benefit over 8 years is ₹6 to ₹7 lakh, dropping the effective after-tax cost from ₹60 lakh to roughly ₹53 to ₹54 lakh. Principal is not deductible.

Faz · The Honest Journey · 2026