An education loan covers your tuition and usually your hostel fees, but it does not cover your full living cost abroad. The living and incidental allowance is typically capped at 10 to 20 percent of the loan, the laptop allowance often around ₹50,000 to ₹1 lakh. The money that reaches your own hands is smaller and slower than the headline number suggests.

The brochure said “up to 100% of the cost of attendance.” The relationship manager nodded along when your mother asked whether the loan would cover everything. Then the first disbursement landed, the tuition went straight to the university, and you were standing in a new country working out how to pay a deposit on a flat, buy a winter coat, and eat for six weeks before any part of the loan reached your own account. The loan covered the college. It did not, in any practical sense, cover your life.

This post is the gap between the marketing line and the disbursement reality. If you are reading a sanction letter and trying to work out what money actually reaches you and when, this is the post to read before your first disbursement.

Does an education loan cover living expenses? Partly. It covers hostel or accommodation fees almost always, usually paid straight to the institution, and it covers a capped allowance for personal and incidental expenses. It does not cover your full month-to-month living cost abroad, and the portion that reaches your own hands is smaller and slower than the headline number suggests.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

The loan basics nearby: the education loan EMI calculator math post, the RBI guidelines education loan post, and the education loan vs personal loan post.

The “100% cost of attendance” line and what it really means

Banks and NBFCs advertise education loans as funding the full cost of attendance. The phrase is not a lie. It is just doing a lot of quiet work. The “cost of attendance” is the figure printed on your university’s official offer letter or I-20 equivalent, and a lender will sanction a loan amount up to that number minus your margin money contribution. So the sanction letter genuinely can show a number that matches the university’s total estimate.

The problem is the difference between the sanctioned amount and what the lender actually releases into spendable form. Tuition is released directly to the institution. Hostel fees, where the institution bills them, are also released directly to the institution. What is left for you to live on is whatever the lender agreed to release as a living or maintenance allowance, and that figure is almost always capped well below your real cost of living.

A loan can be sanctioned at “100% of cost of attendance” and still leave you short of cash in week three, because the cost of attendance the bank used was the conservative university estimate, the living-expense slice of it is released in tranches, and your real spending in an expensive city runs ahead of that estimate. The headline is the sanction. The reality is the disbursement schedule.

What an education loan covers: the full breakdown

It helps to split every cost into four buckets: covered by default, partly covered, covered only if you ask explicitly, and not covered. Almost every confusion about education loans comes from treating the second and third buckets as if they were the first.

| Expense | Coverage status | How it works in practice |

|---|---|---|

| Tuition fees | Covered | Released directly to the university or institution each semester or term. You never handle this money. |

| Hostel or accommodation | Covered | Covered when the institution bills it. Paid directly to the institution. Private off-campus rent is treated differently (see below). |

| Exam, library, lab fees | Covered | Part of the institutional fee structure. Released against the official fee schedule. |

| Books and study material | Covered | Funded within a capped allowance, usually a fixed amount per year of the course. |

| Laptop or computer | Covered | Covered when the course makes it essential. Capped, typically one purchase per course. Most lenders fund it without much friction for technical degrees. |

| Caution deposit, building fund | Partly covered | Capped. Many schemes limit the refundable deposit slice to a small percentage of the total loan. |

| Living and personal expenses | Partly covered | A capped maintenance allowance, not your actual cost of living. Released in tranches, often termwise. |

| Travel and airfare | Request explicitly | Usually not in the default disbursement. You have to ask for it in writing and have it added to the schedule. |

| Loan or life insurance premium | Request explicitly | Funded by some lenders, declined by others. Folded into the principal if funded, so you pay interest on it. |

| Off-campus private rent | Not covered well | The maintenance allowance is meant to absorb this, but it rarely stretches to a real-city deposit plus rent. |

| Personal and discretionary spending | Not covered | Phone, clothing, travel within the country, social life. None of this is the lender’s concern. |

The Indian Banks Association Model Education Loan Scheme, which most public sector banks follow, lists the broad categories that can be financed: tuition, hostel and mess charges, examination and library and laboratory fees, books and equipment and instruments, caution deposit, travel expenses for studies abroad, the cost of a computer where essential, and other expenses needed to complete the course such as study tours or project work. The official framework is on the IBA site at iba.org.in. Notice that the scheme says these costs can be financed. Whether a particular cost is released, and how much, is decided by the lender’s own scheme and your sanction terms.

The living-expense cap: what actually reaches your hands

This is the part the brochure does not headline. The living and incidental expense allowance inside an education loan is capped, and the cap is set by the lender’s scheme, not by your real cost of living in London or Toronto or Sydney.

State Bank of India, the largest education loan lender in the country, gives a useful reference point. Under its scheme, the slice of the loan that can go toward incidental expenses such as travel, study tours, project work and similar costs is limited. For studies in India, that incidental and miscellaneous slice is commonly capped at around ₹1 lakh or 20 percent of total tuition, whichever is lower. For studies abroad the absolute living component is larger because the total cost is larger, but it is still a defined slice of the sanctioned amount, not an open allowance. You can read SBI’s education loan scheme details on the official page at sbi.co.in.

Here is what that means on the ground. Take a two-year master’s in a high-cost city where realistic living costs run ₹12 lakh to 16 lakh over the course. The maintenance slice of your loan might be sanctioned at a fraction of that, released to you in two or four tranches, and timed to the academic calendar rather than to when your landlord wants the deposit. The lender is not being unfair. It is funding a conservative estimate. But a conservative estimate plus tranche timing is exactly how a student with a “fully funded” loan ends up borrowing from a roommate in month one.

Faz's ruleA loan that covers 100 percent of the cost of attendance still does not cover 100 percent of how you actually live.

The lender funds the university’s conservative estimate, releases the living slice in tranches, and times it to the academic calendar. Your real cost of living runs ahead of all three. Plan for a three to six month cash buffer of your own before the first living tranche arrives.

The costs you have to ask for: airfare, travel, insurance

There is a category of cost that an education loan will fund, but only if you put it on the lender’s desk in writing. Travel is the clearest example. The IBA scheme explicitly allows travel expenses for studies abroad to be financed. Yet in a large number of sanctions, airfare is simply not in the default disbursement schedule. The lender released tuition, released the hostel fee, sanctioned a maintenance slice, and never added the flight, because nobody asked.

If you want airfare funded, you make a written request, usually before the relevant disbursement, and you back it with a ticket quote or booking. The lender then adds it to the schedule. The same applies to a one-time visa-related cost where the scheme allows it. Do not assume the flight is in there. Check the sanction letter line by line and ask the lender to confirm which costs are scheduled and which are not.

Insurance is the other ask-explicitly item. Many lenders, especially NBFCs funding collateral-free abroad loans, offer or push a loan-protection or life insurance policy and will fund the premium by adding it to the loan principal. That is convenient and it is also expensive, because you then pay interest on the premium for the life of the loan. It can still be the right call on a large unsecured loan where a single parent is the co-applicant. The point here is narrower: if a premium is being funded, it is part of what your loan “covers,” and you should know it is in there and what it adds to your balance. Whether that cover is worth funding at all is a separate decision, weighed in full in the education loan insurance post.

The gap between sanctioned and disbursed

One number on your sanction letter quietly causes more trouble than any other: the difference between the amount sanctioned and the amount disbursed.

Sanctioned is the ceiling the lender approved. Disbursed is what is actually released, and it is released against proof. Tuition is released when the university invoice arrives. The living tranche is released on a schedule. If your course costs less than projected, or a semester is cheaper, or you do not draw the full maintenance slice, the loan is disbursed below the sanctioned amount, which is fine and even good because you pay interest only on what is drawn.

The problem runs the other way. If your real costs run above the sanctioned amount, the loan does not stretch. A mid-course fee hike, a forex swing that makes a foreign-currency tuition bill jump in rupee terms, a city that turned out more expensive than the university’s estimate: none of these are automatically covered. The loan covers what it was sanctioned for, in the currency split it was sanctioned in, and the gap is yours to fund or to take a top-up loan against.

| Term | What it means | Why it matters to you |

|---|---|---|

| Sanctioned amount | The maximum the lender approved, set against the university’s cost of attendance minus your margin money. | This is a ceiling, not a guarantee of cash in hand. |

| Disbursed amount | What is actually released, against invoices and on a schedule. | Interest accrues only on what is disbursed, so undershooting the sanction saves you money. |

| Margin money | The share of the cost the lender expects you or your family to fund, common on larger loans. | This is your own money, due alongside the loan, not covered by it. |

| The shortfall | Real costs above the sanctioned amount: fee hikes, forex swings, an expensive city. | Not auto-covered. You fund it yourself or apply for a top-up. |

This is why two of the most useful things you can do are read the documents required for an education loan before you apply, so the sanction is sized on accurate cost figures, and understand how margin money on an education loan works, because the margin is your own contribution and it is not part of what the loan covers.

Faz's ruleSanctioned is the ceiling. Disbursed is the reality. Plan your cash flow on the second number, not the first.

A loan sanctioned at the full cost of attendance still releases money against invoices and on a schedule. If your real costs run above the sanction, nothing stretches automatically. Size the loan on honest cost figures at application time, because correcting it later means a top-up loan at a fresh approval.

The interest cost of borrowing for living expenses

There is one more honest point that the coverage question hides. Every rupee of living expense you fund through the loan is a rupee you pay interest on, often for ten years, and often with interest compounding through the moratorium period before repayment even begins. Education lending in India is governed by RBI norms, which set the broad framework within which lenders price interest and structure the moratorium.

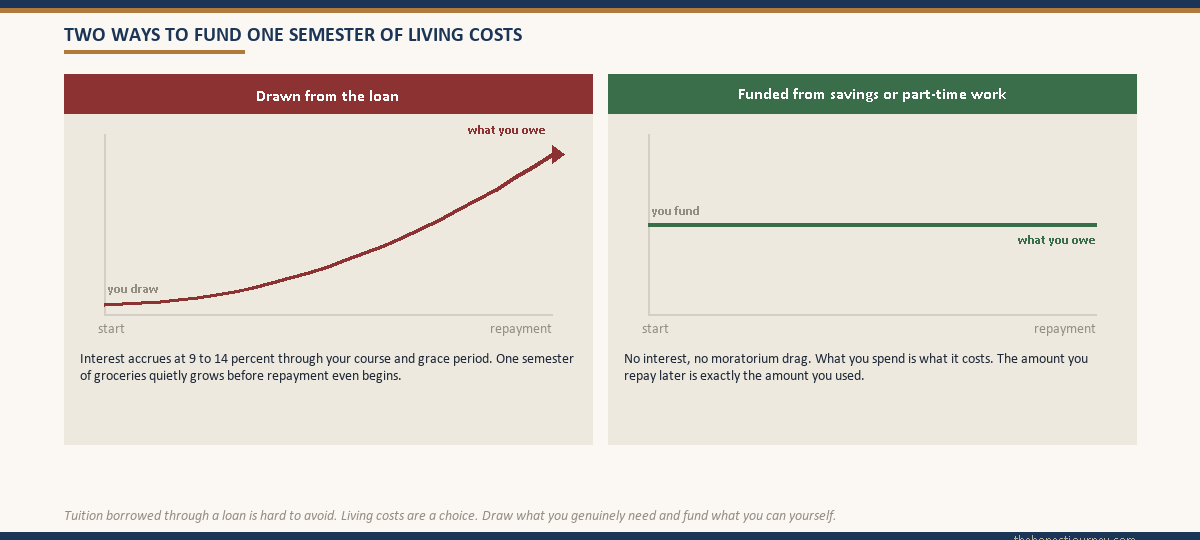

Tuition borrowed through a loan is hard to avoid. Living expenses are different. A maintenance tranche drawn in your first semester sits on your loan accruing interest at 9 percent to 14 percent right through your course and your grace period. By the time you start repaying, that semester of groceries has quietly grown. This is the mechanism explained in detail in the education loan moratorium period and interest post, and it is worth reading before you decide how much of your living cost to put on the loan versus fund from family savings or a part-time job.

None of this means you should not borrow for living costs. For many students it is the only realistic way to fund a degree abroad. It means you should borrow for living costs on purpose, with the interest cost in view, rather than drawing the full maintenance slice by default because it is available.

The honest take before you sign

An education loan is genuinely good at covering the institutional half of studying abroad: tuition, hostel, exam fees, the laptop your course needs. That half is large, it is the part most families cannot fund from a current account, and the loan does it cleanly with money you never even handle.

What the loan does not do well is fund your life. The living slice is capped below your real cost, released in tranches, and timed to the university calendar. Airfare and insurance sit in a “ask for it” category that students routinely miss. And the gap between a sanction sized on a conservative estimate and the real cost of an expensive city is yours to carry.

So before you sign, do three plain things. Read the sanction letter line by line and list exactly which costs are scheduled for disbursement and which are not. Ask the lender, in writing, to confirm the living-expense cap and the tranche timing. And build your own cash buffer, three to six months of real living costs, that does not depend on the loan, because the loan will not be there in week one and your landlord will be. If you are weighing a collateral-free abroad loan, the education loan for abroad studies without collateral post covers how the living-expense slice tends to be tighter on unsecured products.

The loan covers what it covers. Knowing the boundary before you cross it is the whole job. What you do with that boundary, how much you borrow and how much you fund yourself, is your decision to make.

Faz's ruleBorrow for living costs on purpose, not by default, because every maintenance tranche is a rupee you pay interest on for a decade.

Tuition borrowed through a loan is hard to avoid. Living costs are a choice. A maintenance tranche drawn in semester one accrues interest right through your course and grace period. Draw what you genuinely need, fund what you can from savings or part-time work, and keep the interest cost in view.

FAQ

Does an education loan cover living expenses?

Partly. An education loan funds a capped living and maintenance allowance, but that cap is set by the lender’s scheme, not by your real cost of living abroad. The allowance is usually released in tranches timed to the academic calendar, and it rarely stretches to cover a high-cost city in full. Treat the loan as funding part of your living costs and plan a personal cash buffer for the rest.

Does an education loan cover a laptop?

Yes, in most cases. Lenders fund a laptop or computer when the course makes it essential, which covers almost all technical, design and management programmes. The amount is capped, usually to one purchase per course, and released within the overall sanctioned amount. Technical degrees rarely face friction on this. If your course is non-technical, keep the offer letter or course requirement handy in case the lender asks why the device is essential.

Does an education loan cover airfare?

It can, but usually only if you ask. The IBA Model Education Loan Scheme allows travel expenses for abroad studies to be financed, yet airfare is often left out of the default disbursement schedule. To get it funded you make a written request to the lender, normally before the relevant disbursement, backed by a ticket quote or booking. Check your sanction letter and confirm with the lender whether travel is scheduled or not.

Does an education loan cover hostel fees?

Yes, when the institution bills the hostel or accommodation as part of its fee structure. In that case the lender releases the hostel fee directly to the institution, the same way it handles tuition, and you never handle the money. Private off-campus rent is different. It is meant to come out of your capped maintenance allowance, which often does not stretch to a real-city deposit plus monthly rent.

What does an education loan not cover?

An education loan does not cover personal and discretionary spending: phone bills, clothing, travel within the country, social life. It does not cover off-campus private rent well, since the maintenance cap rarely matches real-city rent. It does not automatically cover shortfalls from fee hikes or forex swings above the sanctioned amount. And margin money, your own contribution on larger loans, is by definition not funded by the loan.

Does an education loan cover the full cost of studying abroad?

Not in practice, even when the sanction letter says it does. A loan can be sanctioned at the full cost of attendance, but it releases tuition and hostel directly to the institution, caps the living slice below real costs, and disburses against invoices on a schedule. Forex swings, fee hikes and an expensive city create gaps the sanction does not stretch to. Plan to fund part of the cost yourself.

Does an education loan cover exam and insurance fees?

Exam, library and laboratory fees are covered as part of the institutional fee structure and released against the official fee schedule. Insurance is different. A loan-protection or life insurance premium is funded only by some lenders and usually only if requested, and when funded it is added to the loan principal, so you pay interest on it. Check whether a premium has been built into your loan and what it adds to your balance.

How much living expense does an education loan give for studies abroad?

There is no single figure, because the living slice is a defined portion of the sanctioned amount rather than a fixed allowance. It is larger for abroad study than for domestic study because the total cost is larger, but it remains a capped portion released in tranches. SBI, for example, caps the incidental and miscellaneous slice for India studies at around ₹1 lakh or a small percentage of tuition. Ask your lender for the exact cap and tranche schedule in writing.

Faz · The Honest Journey · 2026