Margin money is the slice of your education cost the bank will not fund, so you arrange it yourself from savings, scholarships, or family. Loans up to 4 lakh usually carry zero margin. Above that it is typically 5 percent for studies in India and 15 percent abroad. On a 20 lakh abroad loan that means putting up 3 lakh yourself before the bank releases its 17 lakh.

A reader’s father called last September, three weeks after his daughter’s loan sanction. The sanction letter said the bank would fund 85% of the total cost; the remaining 15% needed to be brought in by the family as “margin money.” Total course cost: ₹42L. The bank was lending ₹35.7L. The family needed to find ₹6.3L of their own funds before the first disbursement could happen. They had ₹2L in savings and no other liquid assets. They had assumed the loan would cover everything. They hadn’t asked at sanction stage what “margin” meant. Now, two weeks before the visa appointment, they were calling relatives to put together the difference.

This is the most common surprise at sanction stage. The phrase “margin money” is buried in the loan agreement, often in fine print, and the implication for the family’s cashflow is significant. This post is what margin money actually means, why banks ask for it, how it varies by loan size and lender category, and how to negotiate it down or fund it intelligently.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on collateral and how much you can borrow: the education loan against property post, the loan against FD for education post, and the maximum education loan amount india post.

The 60-second answer

Margin money in an education loan is the portion of the total course cost that the family has to fund from their own resources, not from the loan. It is typically expressed as a percentage of the total cost. Standard margin requirements: 0% for loans up to ₹4 lakh (banks cover the full amount), 5% for loans between ₹4-7.5 lakh (for studies in India), and 15% for loans above ₹7.5 lakh, especially for studies abroad. For NBFCs and some private banks, margin can be 0% (zero-margin loans) if the loan covers tuition and “related costs” only. The margin is required upfront, before the first disbursement. It can typically be funded from scholarships, family savings, or smaller separate loans, but is not part of the main education loan.

What margin money actually is

The conceptual basis: lenders don’t fund 100% of any loan as a matter of risk management policy. They want the borrower to have “skin in the game”, a personal financial stake in the success of the venture. For a home loan, this is the down payment (typically 10-20% of property value). For an education loan, this is the margin contribution (typically 0-15% of total course cost).

Faz's ruleMargin money is the family's own contribution to total course cost, not a separate fee.

Standard 15% margin on a ₹40L abroad-studies loan means the family puts up ₹6L from savings before the first disbursement. Most surprised families discover this in the fine print of the sanction letter, two weeks before visa stage.

The thinking: if the student or family has contributed their own money toward the education, they have an incentive to ensure the student completes the course, finds a job, and repays the loan. If 100% is loan-funded, the family’s perceived stake is lower; default risk (in the lender’s calculation) is marginally higher.

The reality: this is a regulatory and policy convention more than a strict risk principle. Margin requirements are set by the Indian Banks’ Association (IBA) Model Education Loan Scheme and adopted by most PSU banks, within the broader education-loan framework laid down by the Reserve Bank of India. Private banks and NBFCs sometimes deviate, offering zero-margin products as a competitive feature.

How margin is calculated

Total course cost (as estimated at sanction stage), margin percentage = loan amount.

Worked example for a ₹30L total course cost:

| Margin policy | Family contributes | Loan covers |

|---|---|---|

| 0% margin (zero-margin product) | ₹0 | ₹30L |

| 5% margin (PSU studies in India bracket) | ₹1.5L | ₹28.5L |

| 15% margin (studies abroad standard) | ₹4.5L | ₹25.5L |

| 20% margin (some collateral-light products) | ₹6L | ₹24L |

The margin is computed on the total cost the bank recognises, not on the maximum the bank could have lent. If you apply for a ₹35L loan against a ₹40L total cost with 15% margin, the bank lends ₹40L minus 15% margin = ₹34L, not ₹35L. The shortfall of ₹1L needs to be either covered by additional family contribution or supplemented by another smaller loan.

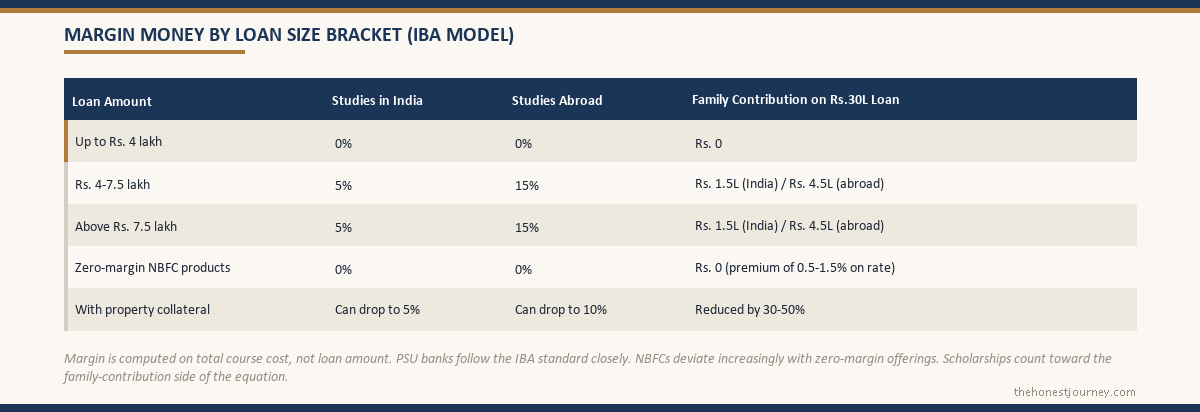

Margin by loan size bracket (IBA model)

The standard IBA model schedule that most PSU banks follow:

Loan up to ₹4 lakh:

- Margin: 0%

- Banks fund the full amount; no family contribution required

- Typically for short courses, diplomas, or domestic UG programs

Loan ₹4-7.5 lakh:

- Margin for studies in India: 5%

- Margin for studies abroad: 15%

- Common for domestic PG programs or partial-cost abroad funding

Loan above ₹7.5 lakh:

- Margin for studies in India: 5%

- Margin for studies abroad: 15%

- This bracket covers most international master’s loans

The margin percentage doesn’t increase further as loan size grows. A ₹50L loan has the same 15% margin as a ₹15L loan: ₹7.5L vs ₹2.25L family contribution respectively.

Variations by lender category

The 15% standard isn’t universal. Different lenders have moved away from it for competitive reasons.

PSU banks (SBI, BoB, Canara, Union, PNB):

- Closely follow IBA model

- 15% margin for abroad studies, 5% for domestic

- Some exceptions for SBI Global Ed-Vantage to premier institutions (lower margin possible)

- Collateral can sometimes reduce margin to 10% or less

Private banks (Axis, ICICI, Kotak):

- Generally follow 15% standard but with flexibility

- Some products offer 10% margin for select institutions

- For best rates, may match NBFC zero-margin offers selectively

NBFCs (HDFC Credila, Avanse, Auxilo, InCred, IDFC First):

- Increasingly offer zero-margin or low-margin products

- “Coverage” definition matters: tuition only, or tuition + living + visa + airfare

- Total comprehensive coverage is the competitive differentiator

- May charge slightly higher processing fees or rates to offset the no-margin risk

USD lenders (Prodigy Finance, MPOWER Financing):

- Concept of margin doesn’t quite apply in the same way

- They typically fund a defined “cost of attendance” set by the institution

- The student usually arranges any extra costs separately

What margin money covers vs the loan

Worth being clear on what “the loan covers” actually means. A typical comprehensive education loan covers:

- Tuition fees

- Hostel / accommodation expenses

- Examination fees

- Library and lab fees

- Books and study material

- Equipment (laptop, instruments)

- Travel: to-and-fro airfare (one-way at start, return at end)

- Insurance premium (sometimes)

- Caution deposit, building fund, refundable deposits (in some lender policies)

- “Other reasonable expenses” related to the course

The total of these is what the bank estimates as “course cost.” Margin is calculated on this total.

What margin money typically funds (the family’s contribution):

- Visa fees and visa-stage processing costs

- Forex commissions and bank charges

- Initial living expenses before the first living-expense disbursement arrives

- Any expenses the loan policy doesn’t explicitly cover

- Buffer for currency fluctuation

Some lenders specify that margin money cannot be funded from another bank loan (so a personal loan to fund the margin is technically not allowed). In practice, the source of margin money is rarely deeply scrutinised; the bank cares that it’s there at disbursement stage.

How to reduce margin requirement

Faz's ruleZero-margin NBFC loans cost 0.5-1.5% more on rate. Worth it only if your family genuinely can't arrange the margin cash.

On a 10-year ₹35L loan, that 1% rate premium is ₹4-5L of extra interest. Compare that to the cost of pulling together the ₹5-6L margin from family savings, scholarship, or asset sales. The cheapest path is usually the PSU margin loan if the cash can be arranged.

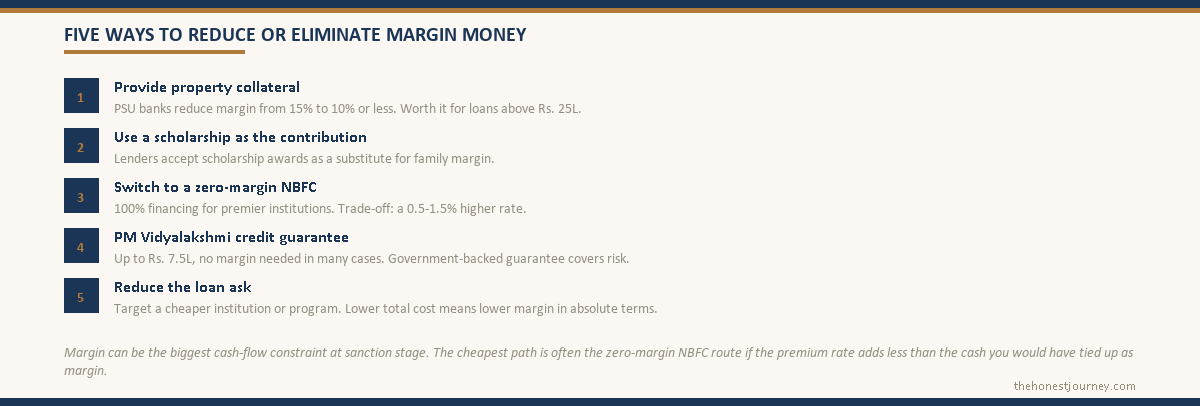

Three legitimate paths to bring margin down:

1. Provide collateral

PSU banks reduce margin when collateral is offered, sometimes from 15% to 10% or lower. The collateral effectively underwrites the bank’s risk; margin becomes redundant.

Worked example: ₹30L loan with 15% margin = ₹4.5L family contribution required. Same loan with property collateral worth ₹38L = bank may reduce margin to 10%, requiring only ₹3L from the family.

Catch: collateral comes with its own costs (property valuation, legal fees, time delay for verification). Worth it only for larger loans where the margin reduction is material.

2. Use scholarships to fund the margin

Most lenders accept that scholarships can substitute for margin money. If the student has been awarded a ₹3L scholarship by the institution or a third-party fund, the lender can treat this as part of the “non-loan” contribution to total cost.

This requires the scholarship letter to be presented at sanction stage. The lender adjusts the loan structure: total cost ₹40L, scholarship ₹3L, family margin ₹3L, loan ₹34L. We covered scholarship sources in the scholarships post.

3. Switch to a zero-margin NBFC product

The simplest route. Several NBFCs offer 100% financing for premier institutions and strong profiles. The trade-offs: slightly higher rate (typically 0.5-1.5% premium over PSU margin loans), faster sanction, less documentation.

Worth doing if:

- The institution is on the NBFC’s pre-approved premier list

- The co-applicant profile is strong, with a CIBIL score of 750 or above

- Cashflow is genuinely tight at the family level

Worth avoiding if:

- The rate differential is more than 1.5%

- The premium over 8-10 years exceeds the cashflow value of avoiding the margin

A worked calculation: ₹35L loan with 11% PSU rate + ₹6L margin contribution vs ₹41L zero-margin NBFC loan at 12.5%. Over 10 years, the PSU option saves approximately ₹4-5L in total interest, but the ₹6L margin is required upfront. For most families, the PSU option is better economics if the ₹6L can be arranged.

When margin money becomes a roadblock

The hard cases:

Family genuinely cannot put up margin. ₹4-7L is a significant amount for many middle-income Indian families. The options narrow:

- Zero-margin NBFC loan (the most common solution)

- PM Vidyalakshmi credit-guaranteed loan up to ₹7.5L (no margin in some cases), we covered this in the PM Vidyalakshmi post

- Scholarship that covers the margin gap

- Sale of a small asset to fund margin

- Loan from extended family as bridge funding (not formal margin)

- Reduce the loan ask: target a less expensive institution or program

Margin requirement appears after sanction. Sometimes the sanction letter is verbal or generic, and the specific margin requirement only appears in the detailed disbursement document later. This catches families off guard.

The fix: ask explicitly at application stage what the margin will be. Get it confirmed in writing before signing the loan agreement.

Margin needs to be deposited in escrow before disbursement. Some lenders require the margin amount to be held in a specific account (sometimes the same bank’s savings account) as proof of family contribution. The amount may be locked until first disbursement.

The fix: confirm this requirement at sanction. Plan for the cashflow lock-up period.

Margin money treatment in subsequent years

The margin is typically computed once at sanction, based on the total estimated course cost. As the course progresses and actual expenses materialise:

- If actual costs are lower than estimated, the unused loan portion doesn’t accrue interest, but the margin is already deployed

- If actual costs exceed estimates (currency depreciation, fee hikes), the family may need to put up additional contribution mid-course

The honest planning advice: estimate course cost conservatively at sanction (10-15% buffer), so the sanctioned loan amount has some headroom for cost inflation over 2-3 years. Margin computed on the buffered amount is slightly higher but provides flexibility later.

Margin money in the loan agreement

The loan agreement specifies:

- Total project cost as estimated by the bank

- Loan amount sanctioned

- Margin amount (the difference)

- Conditions on margin deployment (when it must be brought in, in what form)

- Treatment of any surplus or shortfall

Read this section carefully. The standard clause says margin “must be brought in upfront before first disbursement” but the actual practice varies. Some lenders accept margin contribution against semester-by-semester disbursement rather than all upfront, which ties directly into how the loan disbursement process is structured.

Margin money vs the down payment myth

A lot of families hear “margin” and mentally file it next to a home-loan down payment, money that is gone, sunk into an asset the bank now part-owns. That mental model is wrong, and getting it wrong changes how families plan. Margin money on an education loan is not paid to anyone. It is your share of the same course cost, spent on the same tuition and living expenses, just not borrowed. The bank does not hold it, does not charge interest on it, and does not own anything in return.

Why this matters in practice: a home-loan down payment is locked into the property the moment you pay it. Margin money is fungible until the day it is deployed. If you can show the bank the funds exist, in many cases you can keep that money earning a return right up to the disbursement date. A family with ₹6L of margin sitting in a sweep fixed deposit at 7% is earning roughly ₹3,500 a month on it while the loan is being processed. The mindset shift is simple: margin is not a cost of the loan, it is the part of the bill you were always going to pay, scheduled slightly earlier than you expected.

A real cashflow timeline for the margin contribution

The reader’s father from the opening was not caught out by the amount. He was caught out by the timing. Margin money has a date attached to it, and that date is usually earlier than families assume. Here is the honest sequence for an abroad-studies loan with a 15% margin.

At sanction stage, roughly three to four months before the course starts, the bank confirms the total cost and the margin figure. At this point nothing is paid, but the clock has started. Two to four weeks before the first disbursement, the bank asks for proof that the margin is in place, and for the first tuition tranche the margin portion has to be ready alongside it. For a ₹42L course at 15% margin, that means the family needs ₹6.3L available not on course start day, but several weeks before it, in time to clear with the first fee payment to the institution.

The honest planning rule: treat the margin as due 60 to 75 days before the course start date, not on it. Families who plan to “arrange it closer to the time” end up borrowing from relatives at the worst possible moment, two weeks before a visa appointment, which is exactly the trap in the opening story. If the margin is coming from a fixed deposit, check the maturity date against this 60-to-75-day window, because breaking an FD early to fund margin can cost a penalty of 0.5 to 1% on the interest. A small thing, but it is real money, and it is avoidable with one calendar entry made at sanction stage.

How margin interacts with TCS and forex on the first transfer

There is a cost layer that sits right next to margin money and is almost never explained at sanction: the tax collected at source on foreign remittances. Under current rules, remittances for education funded by a loan from a recognised financial institution attract a low TCS of 0.5% on amounts above ₹7L in a financial year. But remittances not funded by such a loan, which is exactly what margin money is, attract TCS at 5% above the ₹7L threshold. The margin portion of your first transfer abroad can therefore be taxed at ten times the rate of the loan-funded portion.

A worked example makes this concrete. Say the first-year transfer abroad is ₹20L, split as ₹17L loan-funded and ₹3L margin. The loan-funded ₹17L attracts 0.5% TCS on the amount above ₹7L, roughly ₹5,000. The ₹3L of margin, if it pushes past the threshold, can attract 5% TCS, another large chunk. The TCS is not lost money, it is adjustable against your income tax or refundable, but it is cash locked up for several months until you file a return, and for a family already stretched on margin, that lock-up stings.

The practical move: where possible, route the margin contribution through the education loan channel, or have the bank structure the transfer so the loan and margin portions are clearly documented as one education remittance. Banks that handle education loans well will guide this. Add to that the forex spread, typically 1 to 2% over the interbank rate at most banks, and a small SWIFT charge per transfer, and the honest conclusion is the same one this whole post keeps returning to: the margin is not just 15% of the course cost, it is 15% plus the friction of moving it. Ask your lender to lay out the TCS and forex treatment in writing at sanction, alongside the margin figure itself.

Frequently asked questions

What is margin money in an education loan?

The portion of total course cost that the family or student contributes from their own funds, not from the loan. Standard margin is 0% for loans up to ₹4L, 5% for ₹4-7.5L (in India) or 15% for ₹4-7.5L (abroad), and 15% for loans above ₹7.5L for abroad studies. NBFCs increasingly offer 0% margin (zero-margin) products.

Why do banks ask for margin money?

To ensure the borrower has financial commitment to the course (skin in the game). Also a regulatory convention from the Indian Banks’ Association model education loan scheme.

Can I get an education loan without margin money?

Yes. NBFCs (HDFC Credila, Avanse, Auxilo, InCred) increasingly offer zero-margin products for premier institutions. PM Vidyalakshmi credit-guaranteed loans up to ₹7.5L often have no margin requirement. Collateral-backed PSU loans can have reduced or eliminated margins.

When is margin money required to be paid?

Typically upfront, before the first disbursement. Some lenders accept it in tranches matching the disbursement schedule. The loan agreement specifies the exact requirement.

Can scholarship be used as margin money?

Yes, most lenders accept scholarships as a substitute for family margin contribution. Present the scholarship letter at sanction stage so the loan structure is adjusted accordingly.

What if the actual course cost is more than estimated?

The loan amount is fixed at sanction. Any cost overrun has to be funded by additional family contribution or a separate top-up loan. Build a 10-15% buffer into the estimated cost at sanction to avoid this.

Is margin money refundable?

It is the family’s own money; it is “deployed” toward course costs but not borrowed and not interest-bearing. The bank doesn’t refund it because it never received it as part of the loan. If course costs come in lower and excess remains, that excess stays with the family.

Can I take a personal loan to fund margin money?

Officially most lenders specify that margin should be from own savings. In practice, source verification is light. A personal loan to fund margin creates a second monthly EMI burden which can stress family cashflow.

Do NBFCs really offer 100% financing with zero margin?

Yes, for select profiles and institutions. The premium is typically a 0.5-1.5% higher rate. Worth doing if the family cannot arrange margin or if the institution is on the NBFC’s premier list.

What is margin money for an education loan from SBI?

For the SBI Education Loan: 0% margin for loans up to ₹4L, 5% margin for studies in India ₹4L+, and 15% margin for studies abroad ₹4L+. SBI Global Ed-Vantage for premier institutions has some flexibility on margin.

For the related decisions: the interest rate comparison post covers how rates change between zero-margin NBFCs and margin-required PSU loans; the no-collateral loan post covers when going collateral-free is the right move (and how it affects margin); and the PM Vidyalakshmi post covers the credit-guarantee route that can eliminate both margin and co-applicant requirements at smaller loan sizes.