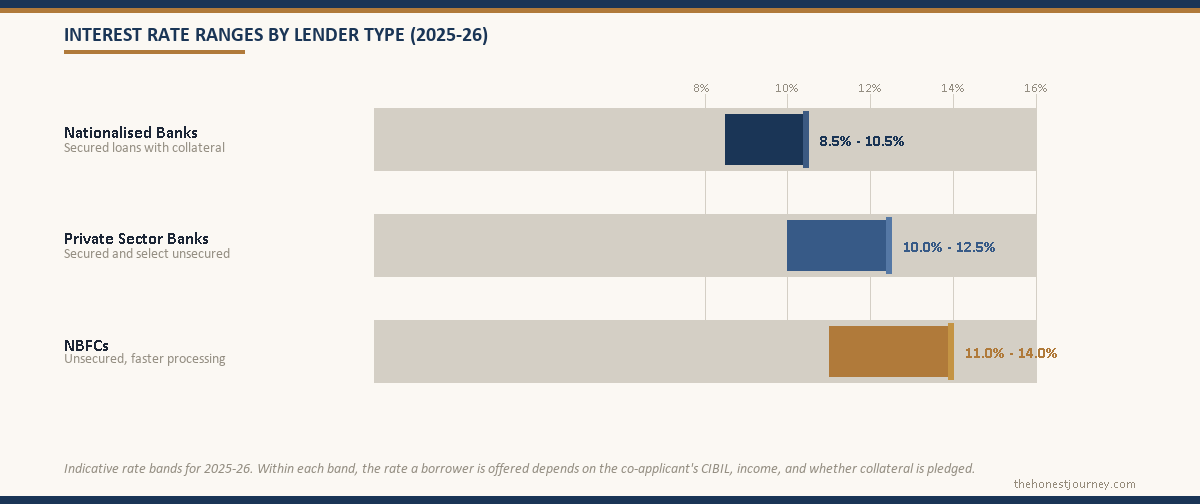

Education loan interest rates in India in 2025 range from 8.5 percent at nationalised banks with collateral, to 10 to 12.5 percent at private banks, up to 13 to 14 percent at NBFCs without collateral. On a ₹40 lakh loan over 10 years, the gap between an SBI loan at 9.15 percent and an NBFC loan at 13.5 percent works out to roughly ₹12 to 14 lakh in extra interest. Collateral is what unlocks the cheap rate.

If you are comparing education loan interest rates in India for abroad studies, here is the honest picture: rates range from 8.5% at nationalised banks (with collateral) to 14% at NBFCs (unsecured). The difference sounds small in percentage terms. Over a 10-year repayment, it is not.

This post breaks down the three lender categories, what each one actually offers, and the real rupee cost of choosing one over another. No brand pitches, no hidden nudges toward paid partners. Just the numbers.

For the full guide, read Studying Abroad From India: Cost and Funding Guide.

The Three Lender Categories and Where They Stand

Education loans for abroad studies in India come from three buckets: nationalised (public sector) banks, private sector banks, and Non-Banking Financial Companies (NBFCs). Each has a different risk appetite, which directly sets the rate you pay.

| Lender Type | Typical Interest Rate | Collateral Required | Max Loan Amount | Typical Processing Time |

|---|---|---|---|---|

| Nationalised Bank | 8.5% to 10.5% p.a. | Yes (above ₹7.5 lakh) | ₹1.5 crore (select schemes) | 4 to 8 weeks |

| Private Sector Bank | 10% to 12.5% p.a. | Depends on amount and profile | ₹75 lakh to ₹1 crore | 2 to 4 weeks |

| NBFC | 11% to 14% p.a. | Often not required (unsecured) | ₹75 lakh to ₹1.5 crore | 1 to 2 weeks |

Rates above are floating unless stated otherwise. The actual rate you receive depends on your co-applicant’s income, CIBIL score, the university’s ranking, your chosen program, and the collateral you can offer.

Faz's rule

Floating rates mean your EMI can go up mid-repayment.

Most education loans in India are linked to the lender’s benchmark rate (MCLR or repo-linked). When the RBI raises rates, your EMI rises too. Factor this into your affordability calculation, not just the rate at disbursal.

Nationalised Banks: The Cheapest Option, With Conditions

Public sector banks offer the lowest rates in the market, and a Bank of Baroda education loan sits firmly in this category. The catch is qualification. To access the 8.5% to 9.5% band, much like the rates on an SBI education loan for abroad studies, you typically need:

- Tangible collateral, usually immovable property worth at least 1.25x to 1.5x the loan amount

- A co-applicant (parent or guardian) with a stable income and a clean credit history

- Admission to a university on the bank’s approved list, or a strong-ranking institution

- Loan amount above ₹7.5 lakh (below this, unsecured loans are available but rates are higher)

Processing time at nationalised banks, including a Canara Bank education loan, is longer because documentation is more intensive. Property valuation, legal verification, and internal credit committee approvals all add time. Budget 4 to 8 weeks from first inquiry to sanction letter.

The government’s PM Vidyalakshmi portal aggregates nationalised bank schemes. It is worth starting there to compare the specific scheme documents for each bank before walking into a branch. If you are unsure what paperwork each lender wants, the documents checklist by lender saves you a second branch visit.

Private Sector Banks: Mid-Range Rates, Faster Process

Private banks price loans at 10% to 12.5%. They are more aggressive in their sales process and faster in documentation. Some offer pre-approved loans based on university admit letters before complete paperwork is submitted.

Collateral requirements vary. For loans above ₹40 to 50 lakh, most private banks still want some form of security, though some accept financial collateral (fixed deposits, mutual fund folios) rather than property. If your profile is strong, meaning a co-applicant with high income, or admission to a top-25 global university, some private banks will go unsecured up to ₹50 to 60 lakh, which is roughly how an ICICI Bank education loan tends to treat top-tier admits.

Private banks are also more consistent in servicing. Branch-level arbitrariness (a real problem at nationalised banks) is lower. If your time before the visa deadline is short, the private bank route is more predictable.

NBFCs: Highest Rates, Highest Accessibility

NBFCs specialising in education loans, such as the lender behind the Avanse education loan, have built their entire model around students who cannot or do not want to pledge collateral. Their rates run from 11% to 14%, occasionally higher for weak profiles or unfamiliar institutions. The Auxilo education loan, for instance, prices off a benchmark near 15.10% plus a spread, while the InCred education loan uses a floating, risk-graded rate that varies with your profile.

Why do students go here despite the rates? Three reasons:

- No collateral needed. For a first-generation student whose family does not own property in their name, the NBFC is often the only option. We go deeper into this in the guide to education loans without collateral.

- Faster turnaround. Approvals in 5 to 10 working days are normal. For students with tight timelines, this matters.

- Coverage of living expenses. Some NBFCs fund up to 100% of COA (Cost of Attendance), including tuition, living expenses, airfare, and laptop. Nationalised banks are stricter on what they disburse.

The trade-off is real: you pay more. How much more? See the next section.

Faz's rule

NBFCs are not a last resort. For unsecured loans, they are often the only option.

If your family has no property to pledge and your co-applicant’s income is moderate, the NBFC rate is not a penalty, it is the price of access. The question is whether the degree’s return on investment justifies even a 13% loan, not whether the NBFC rate is “too high” compared to a bank you cannot qualify for.

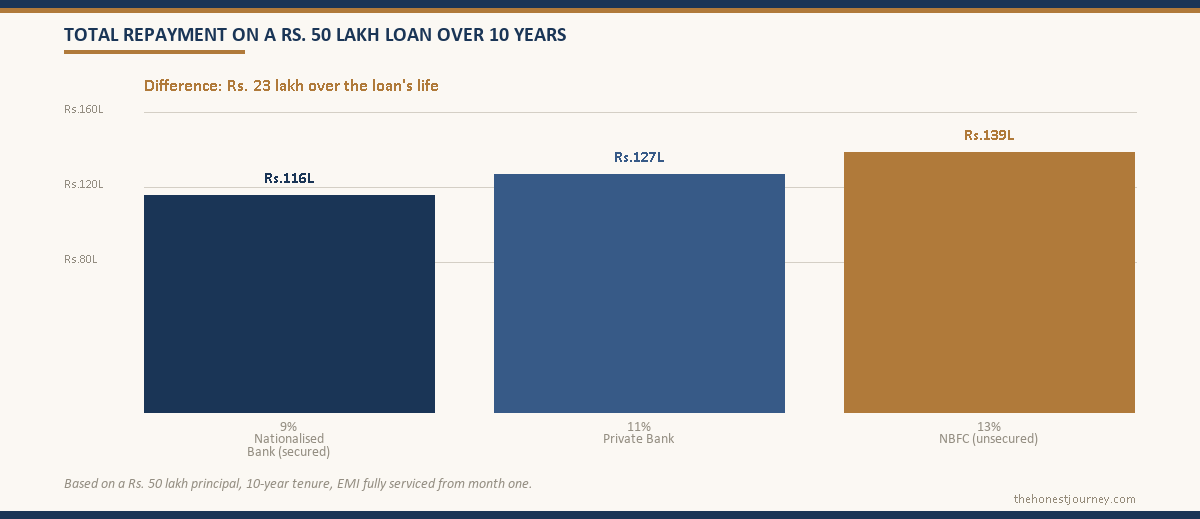

The Real Cost Difference: 9% vs 13% Over 10 Years

Let us run the numbers on a ₹50 lakh loan repaid over 10 years (120 EMIs), with a 1-year moratorium (study period plus 6 months), after which repayment begins.

Faz's rule

9% vs 13% on a ₹50L loan over 10 years is ₹23L of additional interest.

The lender choice matters more than the loan amount choice. ₹23L over a decade is roughly two years of starting salary for the typical Indian student abroad. Worth the 2-4 week extra processing time at a PSU bank if visa deadlines allow.

For simplicity, interest during the moratorium accrues and is added to principal. Assume 18 months moratorium total. The mechanics of how this capitalisation works are covered in detail in the moratorium interest guide.

Interest accrued during moratorium at 9%: approximately ₹7.0 lakh. Effective principal at repayment start: ₹57 lakh.

Interest accrued during moratorium at 13%: approximately ₹10.3 lakh. Effective principal at repayment start: ₹60.3 lakh.

Monthly EMI at 9% on ₹57 lakh over 10 years: approximately ₹72,200

Monthly EMI at 13% on ₹60.3 lakh over 10 years: approximately ₹90,500

Total outflow at 9% (tuition + interest across full tenure): approximately ₹1.16 crore

Total outflow at 13% (tuition + interest across full tenure): approximately ₹1.39 crore

The difference is roughly ₹23 lakh over the loan’s life. On a ₹50 lakh loan, that is 46% extra in interest, just from the rate gap.

Processing Fees and Hidden Charges You Should Factor In

Interest rate is not the only cost. Here is what else you pay:

| Charge | Nationalised Bank | Private Bank | NBFC |

|---|---|---|---|

| Processing fee | Nil to 0.5% of loan | 0.5% to 1% of loan | 1% to 2% of loan |

| Prepayment penalty | Generally nil | Nil to 2% on floating rate loans | 2% to 4% if prepaid within 1-3 years |

| Property valuation fee | ₹5,000 to ₹15,000 | ₹5,000 to ₹15,000 | Not applicable (unsecured) |

| Insurance premium | Optional at most banks | Often bundled (check fine print) | Sometimes mandatory (adds 0.5-1%) |

| Currency conversion / forex fee | Varies by disbursal method | Varies by disbursal method | Varies by disbursal method |

On a ₹60 lakh loan, a 2% processing fee at an NBFC is ₹1.2 lakh upfront, deducted before disbursal. You borrow ₹60 lakh but receive ₹58.8 lakh. Factor this into your actual funding gap.

Mandatory insurance bundling is a watch-out. Some lenders fold a credit life insurance premium into the EMI without clearly disclosing the annual cost. Ask for the APR (Annual Percentage Rate), not just the stated interest rate.

Collateral vs Unsecured: The Real Trade-Off

Pledging property gives you 150 to 200 basis points lower rate. Whether that trade-off makes sense depends on your family situation:

Faz's rule

PSU bank rates are 1.5-2.5% lower than NBFC rates.

But PSU processing is 2-4 weeks slower and requires collateral above ₹7.5L. The right move depends on family circumstances: collateral availability, timing pressure, co-applicant strength. There is no universal best lender.

Go secured (nationalised or private bank with collateral) if: your family owns property that can be legally mortgaged, you have enough lead time (8 to 10 weeks minimum), and the lower rate meaningfully changes your post-study cash flow.

Go unsecured (NBFC or private bank unsecured scheme) if: you have no property to offer, your timeline is under 4 weeks, or the psychological and legal risk of property mortgage is not acceptable to your family.

One underappreciated point: a property mortgage means if you default, the lender can initiate SARFAESI proceedings on your family’s home. The lower rate is real, but so is the downside. For students going to programs with uncertain job placement outcomes, this is worth a hard conversation with your family before signing.

Faz's rule

Check the CIBIL impact of your co-applicant before applying.

The loan shows on your co-applicant’s credit report from day one, even during the moratorium. If your parent is planning to take a home loan or business loan in the next 2 to 3 years, their liability-to-income ratio just changed. Plan accordingly.

Which Category Should You Approach First?

There is a logical order to this:

- Check if you qualify for a nationalised bank scheme. If you have collateral and 8 to 10 weeks, this is the cheapest source. Start the process early, even if you are also applying elsewhere.

- If collateral is available but you need a faster process, a private bank is the middle path. Rates are higher, but documentation and turnaround are more predictable.

- If you have no collateral or no time, an NBFC is not the “bad option.” It is the accessible option. Just go in knowing the total cost and factor it into your ROI calculation for the degree.

This is essentially the PSU bank versus NBFC education loan decision in practice. Many students apply to an NBFC first for speed, receive the sanction letter (needed for the visa), and then continue the nationalised bank process in parallel. If the bank comes through, they use the bank loan. This is a legitimate strategy, though confirm there is no prepayment penalty if you close the NBFC loan early.

How Your Rate Is Actually Set: The Spread Over the Benchmark

The headline rate a lender quotes is not pulled out of the air. It is built in two layers. The first layer is an external benchmark. Most banks today price education loans against the repo-linked lending rate, where the floor moves with the RBI repo rate. Older loans are still linked to MCLR (the Marginal Cost of Funds based Lending Rate). The second layer is the spread, the margin the lender adds on top of the benchmark to cover its own risk and profit.

Here is what that looks like in practice. If the repo rate is 6.5 percent and a nationalised bank works on a repo-linked rate of around 9 percent, the spread it is charging you is roughly 2.5 percent. An NBFC at 13 percent on a similar funding base is charging a spread closer to 6 percent. That spread gap is the price of accepting your profile without collateral, faster processing, and a wider net of approved institutions.

Why does this matter to you as a borrower? Because the spread is the part you can sometimes negotiate, and the benchmark is the part you cannot. When you walk into a branch, asking for a lower rate is really asking for a smaller spread. A co-applicant with a high credit score, a salaried government job, or an existing relationship with the bank gives the loan officer room to trim the spread by 25 to 50 basis points. On a ₹50 lakh loan that is real money. The benchmark, by contrast, will move with RBI policy whether you like it or not, which is exactly why a floating loan can feel cheap at sanction and expensive three years later.

One practical tip: ask the lender in writing what benchmark your loan is linked to and what the current spread is. A repo-linked loan reprices faster when rates fall, which works in your favour during a rate-cut cycle. An MCLR-linked loan can lag. If you are choosing between two similar offers, the one with the more transparent and lower spread is usually the better long-term deal even if the headline number looks identical today.

Fixed vs Floating Rate: Which One Should an Education Loan Borrower Pick

Almost every education loan in India is offered on a floating basis by default, but a handful of lenders, mostly private banks and a few NBFCs, will give you a fixed rate option. The honest answer to which is better is that it depends on where interest rates are in the cycle and how much certainty your family needs.

A fixed rate locks your interest for the full tenure or for an initial block of years. Your EMI does not move. The cost of that certainty is that fixed rates are usually quoted 75 to 150 basis points higher than the floating rate on the same day. You are paying a premium upfront for protection against future rate hikes.

A floating rate moves with the benchmark. If RBI cuts rates, your EMI falls and you benefit automatically. If RBI hikes, your EMI rises. Over a 10-year education loan tenure, rates almost always cycle up and down at least once, so a floating loan tends to average out close to the long-run rate.

My honest take for most Indian students: floating is the sensible default. The premium on a fixed rate is steep, and over a decade you are statistically likely to see at least one rate-cut cycle that a floating loan captures for free. The exception is a family with a genuinely tight monthly budget where an EMI rising by ₹8,000 to ₹10,000 mid-repayment would cause real stress. For that family, paying the fixed-rate premium buys peace of mind, and peace of mind has a value. If you do go floating, build a buffer into your affordability math: assume your EMI could rise 15 to 20 percent above the sanction-day figure and check that the number still works. If it does not, you have borrowed too much, not chosen the wrong rate type. The decision is closely tied to whether you should take a loan at all, which we unpack in the loan versus self-funding comparison.

How to Negotiate a Lower Rate Before You Sign

Most students treat the quoted interest rate as a fixed price. It is not. Within the lender’s internal band, the loan officer has discretion, and the rate you walk away with depends on how you present your case. Here is what actually moves the number.

- Bring a competing sanction letter. If you already hold an NBFC sanction at 12.5 percent and you are talking to a private bank, say so. Lenders track conversion rates and a documented competing offer gives the officer a reason to escalate your file for a better rate.

- Lead with the co-applicant’s strength. A co-applicant with a CIBIL score above 780, a stable salaried income, and a low existing EMI load is the single biggest lever. Have the credit report and the latest three salary slips ready before the meeting.

- Offer collateral even if the scheme is unsecured. Some private banks will shave 50 to 100 basis points off an otherwise unsecured loan if you voluntarily pledge a fixed deposit or property. If your family is comfortable with it, this is a clean rate cut.

- Ask for the processing fee waiver as a fallback. If the officer cannot move the rate, the processing fee is often easier to discount. On a ₹60 lakh loan, a waived 1 percent fee is ₹60,000 saved upfront.

- Time your application to the lender’s targets. Branch and regional managers chase disbursal targets near quarter-end. A file that lands in the last few weeks of a quarter sometimes gets more flexibility on pricing.

One thing to be honest about: a nationalised bank loan officer has far less discretion than a private bank or NBFC sales manager, because PSU rates are more rule-bound. Your negotiating energy is better spent on private banks and NBFCs. And whatever rate you settle on, get the spread, the benchmark, the processing fee, and any insurance bundling confirmed in the sanction letter, not just verbally. Knowing your borrower rights, set out in the RBI fair lending guidelines, gives you a stronger footing if a lender later adds a charge that was never disclosed. If a rejection is a risk, the common rejection reasons guide is worth reading before you apply, and the repayment mechanics guide explains how the EMI is structured once disbursal begins.

FAQ

What is the current education loan interest rate in India for abroad studies?

As of 2025 to 2026, nationalised banks offer rates in the 8.5% to 10.5% range for secured loans. Private banks charge approximately 10% to 12.5%. NBFCs charge 11% to 14%, sometimes higher for weaker profiles. All figures are floating rates and will change with RBI benchmark movements.

Is a nationalised bank always better than an NBFC for an education loan?

Not always. A nationalised bank is cheaper if you qualify with collateral and have time. If you have no collateral or a short visa deadline, the NBFC may be the only practical option. Comparing a 9% loan you cannot get to a 13% loan you can get is not a meaningful comparison.

What happens to interest during the moratorium period?

Interest accrues during the moratorium (your study period plus 6 months, typically). Most lenders add this to the principal, which means your repayment amount is larger than what you originally borrowed. Some lenders let you pay simple interest during study, which reduces the total burden significantly. Ask specifically about this before signing.

Can I get a tax deduction on education loan interest?

Yes. Under Section 80E of the Income Tax Act, interest paid on education loans is fully deductible for 8 years from the year repayment starts, as set out by the Income Tax Department. There is no cap on the deduction amount, which meaningfully reduces the effective cost for borrowers in the 30% tax bracket. The deduction applies to the borrower (the student), not the co-applicant.

Does the lender type affect how funds are disbursed abroad?

Yes, and it matters. Nationalised banks typically disburse directly to the foreign university in foreign currency via wire transfer, semester by semester. Some NBFCs and private banks will disburse to your account or to the university, with more flexibility. Confirm the disbursal mechanism, because delays in fund transfer can affect enrollment confirmation deadlines at foreign universities.

What credit score is required for an education loan in India?

The loan is primarily assessed on the co-applicant’s credit profile, since the student has no income. A CIBIL score above 700 for the co-applicant is generally the minimum; above 750 gets better rates. If the co-applicant has defaults or high existing EMIs, even nationalised banks may decline or price the loan at the higher end of their range. NBFCs are more flexible on co-applicant profile, which is part of why their rates are higher.