An education loan balance transfer is worth it when the rate gap between your existing loan and the new offer is at least 1.5 percent and you have more than 4 years of repayment left. Below that, the foreclosure fee on the old loan plus the processing fee on the new one (typically 0.5 to 1 percent of sanctioned amount) eats most of the saving. On a 20 lakh balance with 6 years left, a 2 percent rate cut saves roughly 2.4 lakh in interest after costs. On a 4 lakh balance with 2 years left, the same cut saves under 15,000.

The pitch lands as a WhatsApp message six months after your first EMI. Some NBFC sales executive who somehow has your number says they can shift your education loan to a bank charging two percentage points less and your EMI will drop by a few thousand a month. He sends a one-page comparison. The numbers look good. You start wondering why you didn’t do this earlier.

I have run this math on enough loans, mine and friends’, to know that the comparison is almost never as clean as the WhatsApp slide makes it look. Sometimes the transfer is the right call and the saving is real. Sometimes the costs swallow the gap and you have just spent two months of paperwork to move a few thousand rupees. This post is the actual math, not the brochure.

More on managing repayment: the RBI education loan repayment rules post, the what happens if education loan not paid post, and the education loan restructuring moratorium extension post.

What an education loan balance transfer actually is

A balance transfer is a takeover. A new lender pays off your existing education loan in full, closes it at the old bank, and issues you a fresh loan for the same outstanding balance (minus fees) at a different rate, tenure, and set of terms. Your relationship with the old bank ends. Your new EMI starts with the new lender, usually at a lower rate. The collateral, if any, is released by the old bank and pledged afresh to the new one.

This is the same instrument used in home loan transfers, except education loans add a few wrinkles. The moratorium status matters (mid-moratorium transfers are restricted at many banks). The co-applicant gets re-evaluated. Section 80E continuity has to be preserved. If the old loan is under the Central Sector Interest Subsidy or another government scheme tied to the IBA Model Education Loan Scheme, the transfer may invalidate the subsidy for the remaining tenure.

The good news: RBI has explicitly disallowed prepayment penalties on floating-rate retail loans to individuals, education loans included. So the foreclosure cost on the old loan, in most cases, should be either zero or a small administrative fee (500 to 2,000 rupees for documentation closure). The number to watch is the processing fee on the new loan, which is where lenders make their money.

The rate-gap-vs-cost math, in actual rupees

This is the only section that matters. Everything else in this post is process. The decision is a single number: does the interest saved over your remaining tenure exceed the cost of moving?

Let me run three realistic scenarios. All assume your existing loan is at the Indian-NBFC abroad-studies range (around 12 percent) and the new offer is from a public sector bank (for example SBI’s education loan terms) that came in cheaper after you finished your course (around 10 percent). The numbers shift if your starting rate is different, but the shape of the answer holds.

| Outstanding balance | Years left | Old rate | New rate | Interest saved | Transfer cost (1% PF) | Net saving |

|---|---|---|---|---|---|---|

| 20 lakh | 8 | 12% | 10% | 2,68,000 | 20,000 | 2,48,000 |

| 15 lakh | 6 | 12% | 10% | 1,55,000 | 15,000 | 1,40,000 |

| 8 lakh | 4 | 12% | 10% | 52,000 | 8,000 | 44,000 |

| 4 lakh | 2 | 12% | 10% | 13,500 | 4,000 | 9,500 |

Read the bottom row. On a 4 lakh balance with 2 years to go, a clean 2 percent rate cut nets you 9,500 rupees after costs. That is real money, but it is also two months of follow-ups, fresh KYC for you and your co-applicant, a new sanction file, collateral re-pledging if applicable, and a re-evaluation of your income. The hours-per-rupee ratio is brutal. Most people who run this calculation honestly decide it is not worth it below a 1 lakh net saving.

The top row is the opposite case. On a 20 lakh balance with 8 years left, the same 2 percent gap saves 2.48 lakh after costs. That is worth a month of paperwork. The same logic applies whenever the saving comfortably crosses 1.5 to 2 lakh after fees.

Faz's ruleBelow a 1.5 percent rate gap, the transfer is rarely worth the paperwork.

Run the saving in rupees, not basis points. A “100 bps cheaper” pitch on a 5 lakh balance with 3 years left is roughly 25,000 saved before costs. After a 5,000 processing fee and your time, you are doing two months of work for a four-figure number. Decline politely and move on.

The full cost stack of a balance transfer

The processing fee is the headline cost, but it is not the only one. The honest sticker on a transfer includes the following.

Processing fee on the new loan. 0.5 to 1 percent of sanctioned amount plus 18 percent GST. On a 15 lakh transfer, that is 9,000 to 18,000 plus tax. Negotiable if the lender is hungry for the file. Some public sector banks waive it during specific periods.

Foreclosure / closure fee on the old loan. For floating-rate education loans to individuals, the RBI directive prohibits foreclosure penalties. Most lenders comply by charging zero. A few try to recover an “administrative closure fee” of 500 to 2,000 rupees, which is fine. If your old lender quotes a percentage-of-balance prepayment penalty on a floating-rate loan, push back and cite RBI’s circular. If it is a fixed-rate loan, the penalty is legally allowed and you need to check your sanction letter for the exact percentage.

Collateral re-valuation fees. If the loan is secured by property, the new bank will commission its own legal opinion and valuation report. Together this runs 5,000 to 15,000 depending on city and property type. Unsecured loans skip this.

Stamp duty on the new loan agreement. Varies by state. Maharashtra, Karnataka, Tamil Nadu, and a few others charge meaningful amounts (0.1 to 0.5 percent of loan value). Other states are nominal.

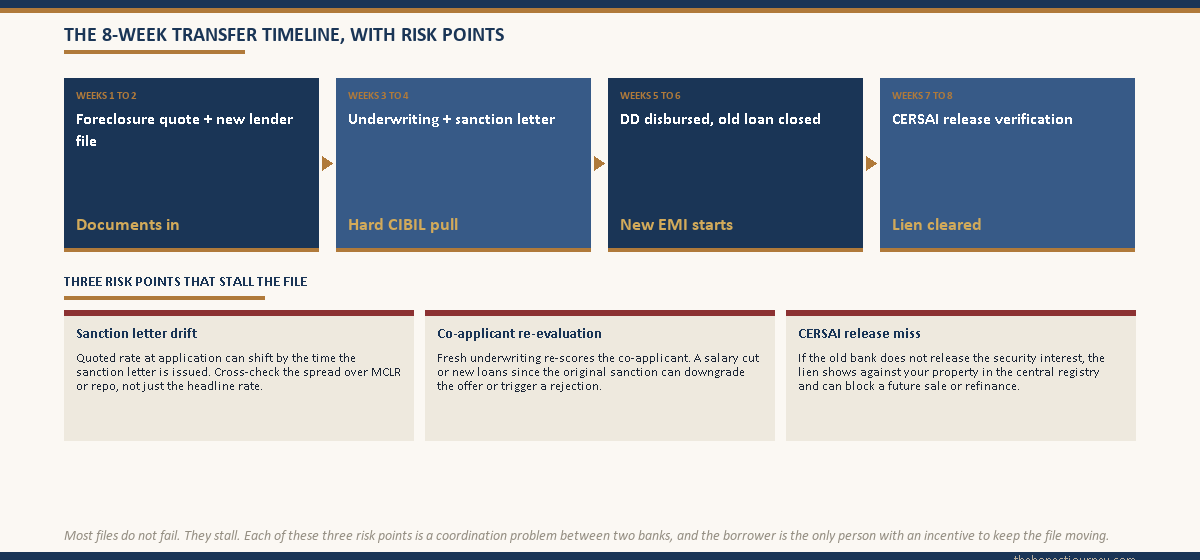

CERSAI charge re-registration. For secured loans, the security interest at CERSAI has to be released and registered afresh. Around 100 rupees, but it is a step that has to be tracked because if it is missed your old bank still shows a lien against your property in the central registry.

Total fixed cost on a typical 15 lakh secured transfer: roughly 25,000 to 40,000 all in. On an unsecured transfer: 12,000 to 20,000. Run your saving against that total, not just the headline processing fee.

When a balance transfer is actually worth it

Four conditions roughly need to be true at the same time. If you tick all four, the transfer is almost certainly going to pay off. If you miss two or more, you are probably better off staying put.

- The rate gap is 1.5 percent or higher. Below 1 percent, fees consume nearly everything. Between 1 and 1.5 percent, the saving is real only on large, long-dated balances.

- You have at least 4 years of repayment left. Interest savings compound across the remaining tenure. With under 3 years left, most of your EMI is now principal anyway and a rate cut does very little.

- Your outstanding balance is 10 lakh or more. Fixed costs (legal, valuation, stamp duty) hit smaller loans disproportionately. A 30,000 cost-stack on a 5 lakh balance is six percent of the loan itself.

- You are out of moratorium and have a clean repayment record. Mid-moratorium transfers are restricted at most public sector banks (the few that allow it want extensive documentation). A clean 12-month repayment track is what makes a new lender treat you as a low-risk takeover file and gives you negotiating room on the rate and fee.

If you check all four, run the rupee math from the table above. If your net saving crosses 1 lakh, start the process.

Faz's ruleThe four-condition check beats any sales pitch. If you fail two or more, do not start the paperwork.

Rate gap >= 1.5 percent, tenure left >= 4 years, balance >= 10 lakh, repayment record clean. Anything less and you are probably moving the same money sideways with extra steps.

When a transfer is not worth it (the cases the pitch hides)

The WhatsApp pitch never mentions these. They are the situations where transferring actively makes you worse off, or where the saving is so small it does not justify the hours.

Small balance, late in repayment. Anything under 5 lakh with under 3 years left. The amortisation schedule is already past the interest-heavy years. A rate cut on a balance that is mostly principal saves you almost nothing.

You are still in the moratorium. Most banks will not take over a loan that has not seen 6 to 12 months of regular EMI repayment. A few NBFCs will, but typically at rates that are not meaningfully better than your existing loan. Wait until you are 12 months into EMI before approaching new lenders. Read the education loan moratorium period and interest post for what is happening to your balance during this window.

You are claiming CSIS or another government interest subsidy. Transferring the loan typically ends the subsidy on the original sanction. If you are still mid-moratorium and CSIS is paying your interest, a transfer means you start paying that interest yourself at the new lender. The “saving” disappears instantly.

The old loan is a fixed-rate loan with a percentage-based foreclosure penalty. Read the sanction letter. If it says 2 to 4 percent prepayment penalty, that alone can wipe out the rate-gap benefit. Quote it back to yourself before you start anything.

Your co-applicant’s financial situation has worsened. A balance transfer is a fresh credit underwriting. The new bank re-evaluates the co-applicant’s income, CIBIL score, and existing liabilities. If your co-applicant has taken a job change, a salary cut, or other loans since your original sanction, the new lender may either reject you, offer a worse rate than the WhatsApp pitch suggested, or demand a different co-applicant.

You are about to prepay aggressively or close the loan within a year. If a bonus, an inheritance, or aggressive monthly prepayments are going to close the loan in 12 to 18 months anyway, transferring is a waste. Pay it down where it sits. The how to repay an education loan post covers prepayment math in detail.

The step-by-step process (timeline: 30 to 60 days)

If the math works and you have decided to move, here is the actual sequence. None of it is technically hard. The friction is all in coordinating between two banks at once.

Week 1: Get a foreclosure quote from your existing bank. Walk into the branch or use the customer portal. Ask for a “foreclosure statement” or “loan closure quote” dated 30 days forward. It will show the exact balance, accrued interest to closure date, and any closure fees. This is the number the new bank needs.

Week 1 to 2: Apply to the new lender with the foreclosure quote. Standard documents: PAN, Aadhaar, address proof, your old sanction letter and statement of account, latest 12 months of EMI payment record, co-applicant KYC and income proof (latest 3 ITRs and 6 months of salary slips), original property documents if secured.

Week 2 to 3: New bank does its underwriting. Credit check on you and co-applicant (a hard CIBIL pull), income verification, FOIR calculation, and for secured loans a fresh legal and valuation report. This is where most files stall. Stay on top of the relationship manager.

Week 3 to 4: Sanction letter from new bank. Read it carefully. The interest rate quoted should match what you were promised (sales pitches sometimes drift between application and sanction). Check the spread over MCLR or repo rate. Check the processing fee. Check whether the rate is floating or fixed, and what the reset clause says.

Week 4 to 5: Disbursement of the takeover demand draft. The new bank issues a DD or NEFT in the exact foreclosure amount made payable to your old bank. You hand it over (or it is sent directly bank-to-bank). The old bank closes the loan, issues you a closure letter, releases the original collateral documents, and removes the CERSAI charge.

Week 5 to 6: New loan EMI begins. The new lender sets up the NACH mandate on your bank account. First EMI is typically the following month. Keep the closure letter and the new sanction letter together in a single folder. You will need both for Section 80E claims to demonstrate loan continuity.

Week 6 to 8: CERSAI verification (secured loans only). Check the CERSAI portal yourself 30 days after closure to confirm the old bank has released the security interest and the new bank has registered the fresh one. If the old release is missing, follow up in writing. An unreleased CERSAI charge can block a future sale or refinance of the property.

Section 80E, CIBIL, and other small-print effects

Section 80E continues, but document the link. The income tax deduction on education loan interest applies to interest paid on a loan taken from a notified financial institution for higher education. A balance transfer does not break eligibility, but in the year of transfer you will have two separate interest certificates (one from the old bank for partial year, one from the new). Keep both. Some assessing officers ask for the closure letter as proof that the new loan is a continuation, not a fresh loan for a different purpose. The Section 80E tax benefit post covers the full claim rules.

CIBIL impact is small and temporary. The new lender’s hard credit pull at application costs you 5 to 10 points for a few months. Once the old loan is closed (status: “closed by the borrower, refinanced”) and the new loan begins reporting on-time payments, your score recovers in 3 to 6 months. A balance transfer is not a derogatory event. It does not look like a default or settlement.

Co-applicant gets re-evaluated. Already mentioned, but worth repeating. If your co-applicant’s financial position has weakened since the original sanction, the new lender may demand a different or additional co-applicant. Discuss this before starting.

Tenure can be reset (carefully). The new lender will often offer to extend tenure back to a full 10 or 15 years, dropping the monthly EMI further. This looks attractive and is sometimes the right call (if cash flow is genuinely tight), but extending tenure means paying interest for more years. Run the total-repayment number, not just the EMI. A lower EMI over a longer tenure can mean lakhs more in total interest paid.

Faz's ruleResetting the tenure back to 10 years to lower the EMI is the most expensive optical illusion in a transfer.

The EMI drops. The total interest paid rises sharply. If cash flow is tight, fine, this is a legitimate tool. If you just want a lower number on the WhatsApp pitch, you are buying a smaller monthly bill at the cost of a much larger lifetime bill.

How to negotiate the new lender down

Sales executives quote the rack rate first. The actual offered rate is almost always 0.25 to 0.75 percent lower if you push. A few specific levers that work.

Get two competing sanction letters. Apply to two banks in parallel. Once both have sanctioned, show each the other’s rate and ask for a match or beat. This works at every public sector bank and most private banks.

Ask for processing fee waiver in exchange for committing. “I will sign today if you waive the processing fee” is a common closer. Public sector banks have less flexibility here than private banks and NBFCs, but it costs nothing to ask.

Negotiate the spread over MCLR or repo rate, not just the headline rate. The headline rate today does not matter as much as your spread over the benchmark, because that spread is what stays fixed when MCLR or repo moves. A loan at MCLR + 1.5 percent will become more expensive than a loan at MCLR + 1 percent as MCLR rises, regardless of where they start today.

Reference the RBI directive on prepayment penalties if the old bank pushes back on closure. Quote the circular date and direct the old bank to its own policy document. They will back down.

For broader rate context across banks, the education loan interest rate comparison post tracks current ranges across PSBs, private banks, and NBFCs.

If the transfer math does not work, what else can you do

You do not always have to transfer. Two cheaper alternatives often deliver most of the saving without the paperwork.

Ask your existing bank for a rate reset. If interest rates have fallen since your sanction (or if MCLR has dropped at your bank), you can apply for a rate reset on your existing loan. Most banks charge a small conversion fee (around 0.25 percent of outstanding balance plus GST) and reset your rate to the current rack rate. This is much faster than a transfer (2 weeks vs. 6 to 8) and significantly cheaper. The catch is the rate the bank will reset you to is typically 0.25 to 0.5 percent above the rate they would offer to a new customer, so the saving is smaller than a transfer. But the cost-saving ratio is often better.

Top-up or restructure within the existing bank. If your goal is a lower EMI rather than a lower total cost, ask your existing bank for an EMI restructure. They can extend tenure within the existing loan without the full transfer overhead. Useful when cash flow is the actual problem. See the education loan top-up post for related options.

Aggressive prepayment. If you have lump sums available, partial prepayments on the existing loan reduce both balance and total interest without involving a new lender at all. RBI prohibits prepayment penalties on floating-rate education loans, so prepay as much as your cash flow allows. On a 15 lakh balance, paying 2 lakh as a lump sum cuts a year off the tenure at most rates.

Reconsider whether the old loan should be unsecured at all. If you took an unsecured loan at 13 to 14 percent because collateral was unavailable at the time, and collateral has since become available (a parent’s property in a clear title state, an FD that has matured), a transfer to a secured product at 9 to 10 percent is one of the highest-saving moves available. The rate gap there can be 3 to 4 percent. See the secured vs unsecured education loan post for that math.

The honest closing take

A balance transfer is one of the few financial moves available to you that can save lakhs of rupees if the conditions line up, and one of the most time-wasting if they do not. The four-condition check (rate gap >= 1.5 percent, tenure left >= 4 years, balance >= 10 lakh, repayment record clean) catches almost every honest case. Run the rupee math, not the basis-point math. Two percent of nothing is nothing.

The other quiet truth is that the cleanest transfers are the ones nobody tries to sell you. The WhatsApp pitch is incentivised on you signing, not on you saving. The person who walks you through your own foreclosure statement and tells you the saving does not justify the cost does not get paid. Be that person for yourself. Run the table from this post against your own numbers, and only then decide.

If you are deep into repayment with a small balance, sit tight and prepay. If you are 18 months into EMI on a large NBFC loan at 12 to 13 percent and a public sector bank is now offering you 9.5 to 10 percent, this is your move. The math, for once, is in your favour.

FAQ

Can I transfer my education loan to another bank?

Yes. Education loans can be transferred to another bank or NBFC the same way home loans can. The new lender pays off your existing loan in full, takes over the balance at a different rate, and you start fresh EMIs with them. Most public sector banks, private banks, and NBFCs accept takeover files, though each has its own minimum-balance and minimum-tenure-left criteria. You typically need at least 6 to 12 months of clean EMI repayment on the existing loan before another lender will entertain the file.

Is there a foreclosure penalty on an education loan?

For floating-rate education loans to individual borrowers, RBI has prohibited foreclosure and prepayment penalties. Most lenders comply, charging either zero or a small administrative closure fee of 500 to 2,000 rupees. For fixed-rate loans, penalties are legally allowed and your sanction letter will specify the percentage (typically 2 to 4 percent of outstanding balance). Always check your loan agreement before initiating a transfer. If a floating-rate lender tries to charge a percentage-based penalty, push back and reference the RBI directive.

How much rate gap makes an education loan balance transfer worth it?

As a rough rule, a 1.5 percent or higher rate gap, combined with at least 4 years of remaining tenure and a balance of 10 lakh or more, makes a transfer worthwhile after accounting for the typical 25,000 to 40,000 in total transfer costs. Below 1 percent gap or with smaller balances and shorter remaining tenures, the costs eat most of the saving. Always calculate the net saving in rupees, not basis points. A 100 bps cut on a 5 lakh balance with 3 years left saves less than 25,000 before costs.

Does CIBIL score drop after an education loan balance transfer?

A balance transfer triggers a hard credit inquiry from the new lender, which can cost 5 to 10 points on your CIBIL score temporarily. The old loan gets reported as “closed” or “closed by refinancing,” which is a neutral status, not a negative one. Once the new loan begins reporting on-time payments, the score typically recovers within 3 to 6 months. A balance transfer is not treated as a default, settlement, or restructuring event. It is a clean refinance and should not have any lasting negative impact on your credit profile.

Can I transfer my education loan during the moratorium period?

Most lenders, especially public sector banks, do not accept balance transfers during the moratorium. They want to see at least 6 to 12 months of regular EMI repayment as proof of your repayment behaviour before taking over the loan. A few NBFCs do allow mid-moratorium transfers, but typically at rates that are not meaningfully better than your existing loan. The better strategy is to wait until you are 12 months into the EMI phase, at which point you have a track record to negotiate with and more lenders compete for the file.

What documents are needed for an education loan balance transfer?

Standard documents include: PAN and Aadhaar of borrower and co-applicant, recent address proof, your original education loan sanction letter and full statement of account, last 12 months of EMI payment record, co-applicant’s latest 3 years of ITRs and 6 months of salary slips, and original property documents (if the loan is secured). The new lender will also request a foreclosure quote from your existing bank, valid for 30 days, showing the exact takeover amount. Have these ready before you apply to avoid stalling the file.

Does Section 80E continue after a balance transfer?

Yes. Section 80E deduction on education loan interest continues after a balance transfer, since the loan remains a higher-education loan from a notified financial institution. In the year of transfer, you will receive two interest certificates (one from the old bank for the partial year, one from the new bank), and you can claim both. Keep your loan closure letter from the old bank and the fresh sanction letter from the new bank together, in case the assessing officer asks for proof that the new loan is a continuation rather than a fresh loan.

Should I extend my tenure during a balance transfer to lower the EMI?

Only if cash flow is the actual problem. Extending tenure during a balance transfer (for example, resetting a loan with 6 years left back to a full 10-year tenure) lowers the monthly EMI but significantly increases total interest paid over the life of the loan. On a 15 lakh balance, extending from 6 years to 10 years at 10 percent can add 2.5 to 3 lakh to total interest. If you can afford the existing EMI, keep the shorter tenure. Use the lower rate to reduce total cost, not just the monthly number.

Faz · The Honest Journey · 2026