If you stop paying, the account is reported to credit bureaus after 30 days, classified as a Non-Performing Asset at 90 days, and a legal demand notice follows. Your CIBIL can drop 80 to 120 points, and the tag attaches to your co-applicant too. There is no jail for non-payment. Most borrowers settle through OTS or restructuring.

The first thing that happens when you miss an education loan EMI is nothing dramatic. No knock on the door, no court summons, no manager at your parents’ house. You get a polite SMS, an automated call, then a formal email. The system is patient at the start because it knows the timeline. It has 30 days before your account becomes a credit bureau report, and 90 days before that turns into something that follows your co-applicant for years.

This post walks the actual timeline of what happens if education loan is not paid in India. No legal jargon. Just what the bank is doing on their side, what shows up on your CIBIL, and your real options at each stage, including the one banks do not advertise. If you are reading this in panic after one missed EMI, you have more time than the recovery call made you feel.

If you do not pay your education loan in India, the account is reported to credit bureaus after 30 days past due, classified as a Non-Performing Asset at 90 days, and a legal demand notice follows. Secured loans can be enforced under the SARFAESI Act, unsecured loans go to recovery agents and civil court. There is no jail for non-payment, though a bounced cheque can trigger Section 138 proceedings. Most borrowers settle via OTS or restructure.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

More on managing repayment: the education loan balance transfer india post, the RBI education loan repayment rules post, and the education loan top UP post.

The timeline: what happens if education loan is not paid, month by month

Here is what happens on a ₹25 lakh loan with a ₹36,000 EMI (10-year tenure, 11.5%) if the first EMI is missed.

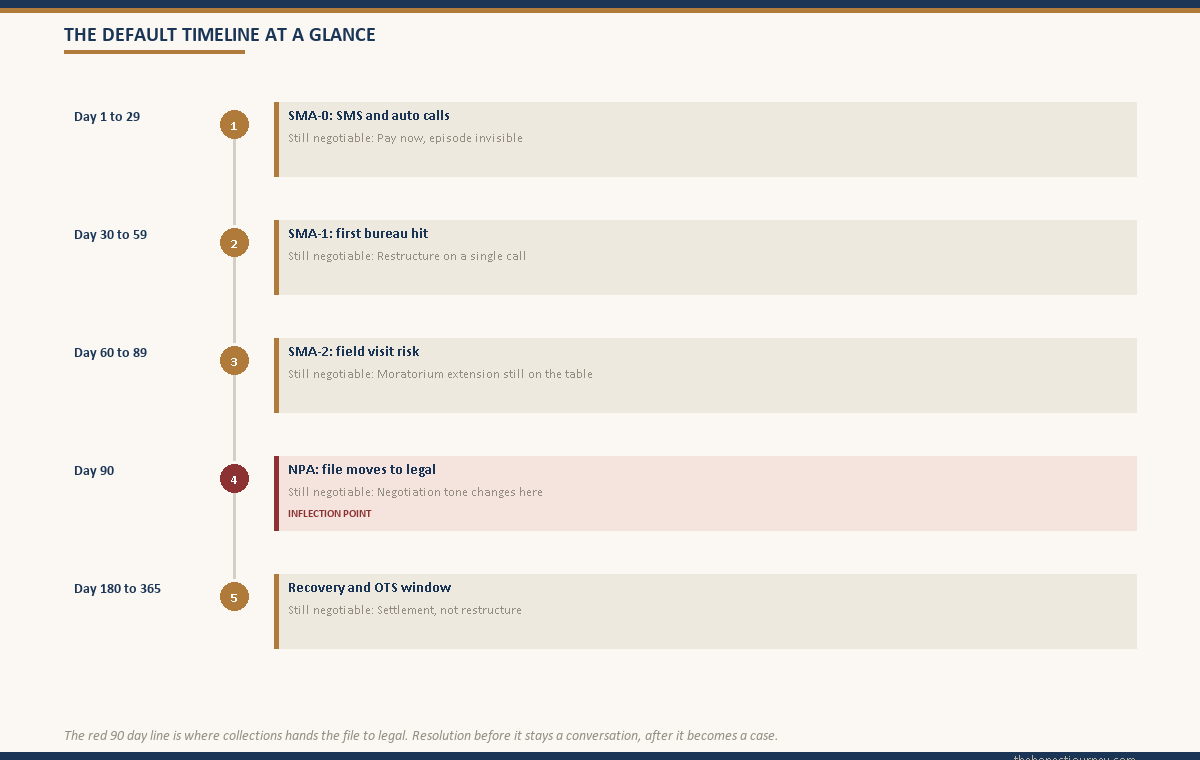

Day 1 to Day 29 (SMA-0 stage). Your account is flagged internally as Special Mention Account 0. The collection desk sends an SMS and an automated call. Late payment charges accrue at roughly 2 percent per month on the overdue EMI. Nothing is reported externally yet. Pay within 30 days and the episode is invisible to anyone outside the bank.

Day 30 to Day 60 (SMA-1 stage). Your loan crosses the 30-day Days Past Due (DPD) threshold. The bank reports the account to CIBIL, Experian, Equifax, and CRIF. Your credit report shows a “30+ DPD” tag, and the same tag attaches to your co-applicant. A human caller from collections reaches out, still in a helpful tone.

Day 60 to Day 89 (SMA-2 stage). DPD ages to 60+ days. CIBIL score drops further, typically 80 to 120 points cumulative. Collections calls intensify and a field visit is possible. A second formal letter is issued, warning of NPA classification if payment is not made in 30 days.

Day 90 onwards (NPA classification). Per RBI’s master directions on Income Recognition and Asset Classification, the loan is classified as a Non-Performing Asset. This is the line that matters. The file moves from collections to the recovery or legal department, and legal notices start.

What “NPA” actually means for you

Three things change once your loan is NPA.

First, your CIBIL report carries a “sub-standard” tag with a DPD of 90+. Any future application, yours or your co-applicant’s, sees this. New credit becomes very difficult for at least 12 months after resolution, and the tag sits on your report for 7 years from closure.

Second, the bank’s legal department takes over. You receive a formal demand notice signed by an authorised officer. For secured loans, this references the SARFAESI Act, 2002, and gives you 60 days. For unsecured loans, the route is a civil suit under Order 37 of the CPC or filing with the Debt Recovery Tribunal if the outstanding is above ₹20 lakh.

Third, penal interest, late fees, and legal costs the bank can claim from you stack on top of the principal.

Faz's rule

The 90-day NPA mark is the most expensive line you can cross. Negotiate before it, not after.

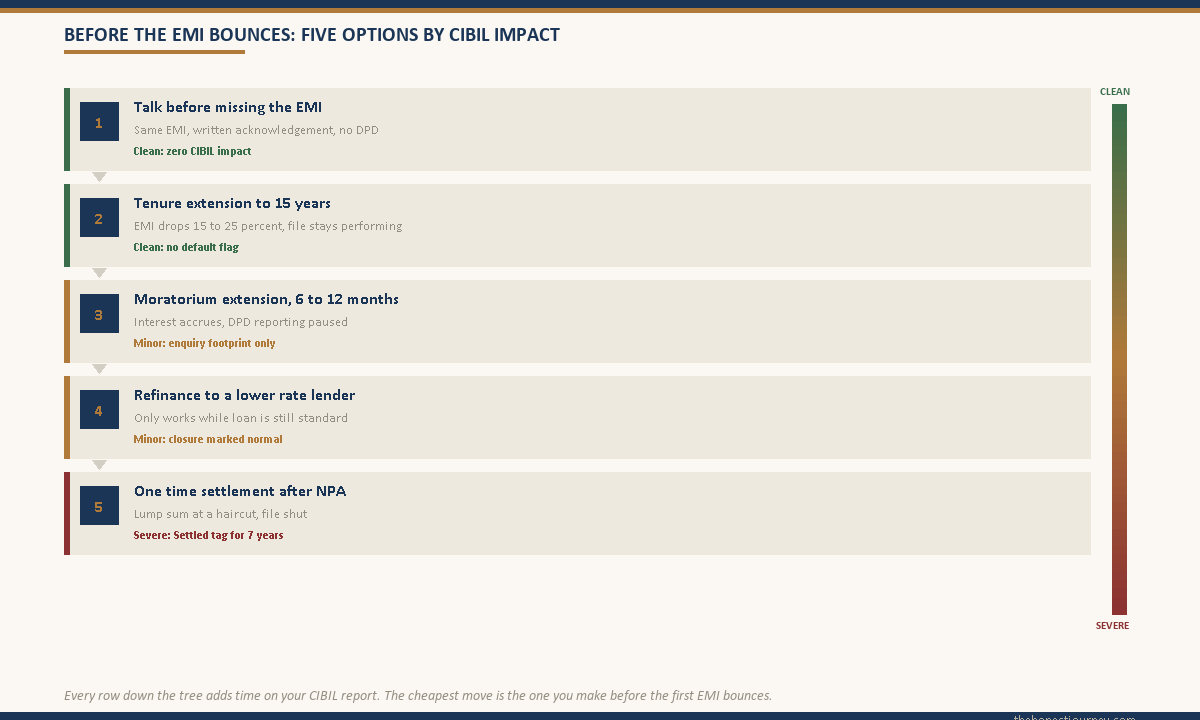

Before NPA, the bank’s collections team has discretion to offer revised EMIs, a temporary holiday, or a tenure extension. After NPA, your file sits with the legal department whose KPI is recovery, not retention. The same restructuring becomes a settlement conversation with a haircut to your CIBIL.

SARFAESI for secured loans: what the bank can actually do

If your loan was secured against collateral (house, plot, FD pledge, LIC policy), SARFAESI is the recovery route. The steps are predictable.

Step 1: Section 13(2) notice. A formal demand giving 60 days to pay the full outstanding.

Step 2: Section 13(4) action. If you do not pay in 60 days, the bank takes symbolic possession of the asset and publishes a possession notice in two newspapers. The asset is not sold yet, you can still pay and reclaim it.

Step 3: Sale notice. The bank values the asset, fixes a reserve price, and publishes a 30-day auction notice. The reserve is usually 70 to 80 percent of fair market value, which is why borrowers regret reaching this stage.

Step 4: Auction. Proceeds clear the loan, surplus comes back to you. Shortfall remains your liability.

You can appeal to the Debts Recovery Tribunal (DRT) under Section 17, but it requires a 25 to 50 percent deposit. Most borrowers pay, restructure, or settle before Step 3.

Unsecured education loans: recovery agents and civil court

If your loan was unsecured (no collateral, usually below ₹7.5 lakh for public sector banks or up to ₹50 lakh for NBFCs against a strong co-applicant), SARFAESI does not apply. The recovery path is different and more drawn out.

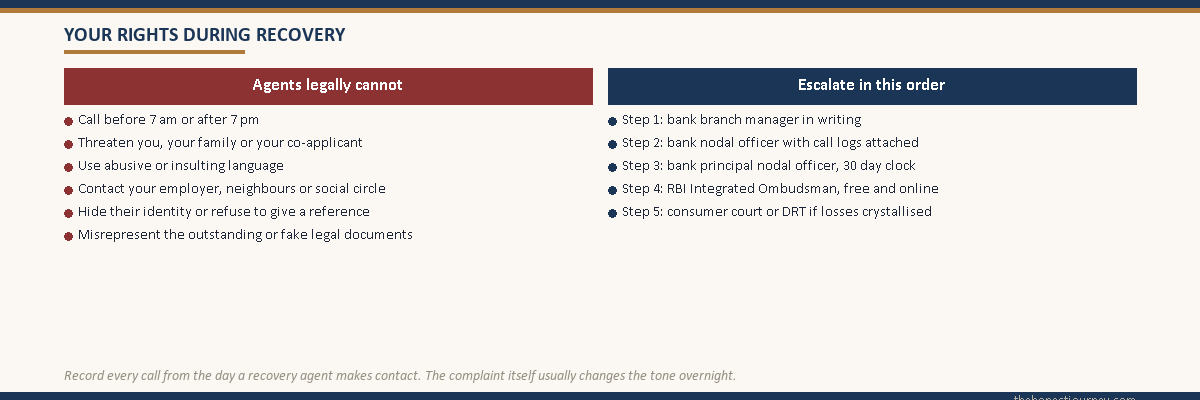

The first phase is recovery agents. RBI’s Master Directions on recovery agents require agents to identify themselves, contact you only between 7 am and 7 pm, and never threaten you or your family. If an agent crosses the line, complain to the bank’s nodal officer and escalate to the RBI Integrated Ombudsman. Keep call recordings.

The second phase is civil court. The bank files a summary suit or recovery suit. The process can take 2 to 5 years and is expensive for the bank, which is why most unsecured defaults end in settlement before judgment.

Faz's rule

Recovery agents have rules. Use them.

Any call outside 7 am to 7 pm, any contact with your employer or neighbours, any abusive language, all of it is a violation under the IBA’s Code on Recovery Agents. Document it, escalate to the bank’s nodal officer, then to the RBI Ombudsman. The complaint itself often changes the tone of the calls overnight.

One-time settlement (OTS): the option lenders rarely advertise

Once your loan is classified as NPA, the bank has a strong incentive to settle rather than litigate. A one-time settlement (OTS), where you pay a lump-sum lower than the total outstanding and the bank closes the file, is a routine commercial transaction on every public and private bank’s books.

Typical OTS haircuts on education loans:

| Stage | Typical settlement range | Likelihood of bank acceptance |

|---|---|---|

| NPA but pre-legal notice (90 to 180 days) | 85 to 95 percent of outstanding | Moderate, bank still hopes for full recovery |

| Post legal notice, pre-suit (6 to 18 months) | 70 to 85 percent of outstanding | High, bank wants to clean books |

| Account “written off” by bank (typically 2+ years) | 50 to 70 percent of outstanding | Very high, anything recovered is upside for the bank |

The bank’s internal write-off policy is the key. Once an NPA is fully provisioned and written off the active books (usually 12 to 24 months after classification), the recovery officer has authority to accept lower offers. This is not a favour, it is a normal commercial process governed by each bank’s recovery policy and the IBA model framework.

How to negotiate one: write to the bank’s recovery department, not the branch. Acknowledge the dues, explain the cause of default in one paragraph, and make a specific lump-sum offer with proof of funds. Be realistic. Do not start at 30 percent expecting a 50 percent landing. Most successful settlements happen in the second or third round of correspondence.

How OTS marks your CIBIL versus a clean closure

An OTS clears the loan but does not give you a clean CIBIL report. A loan closed via full repayment is marked “Closed Obligations Met.” A loan closed via settlement is marked “Settled” or “Written-off and Settled.” Both stay on your report for 7 years from closure, but the two tags read very differently to lenders.

A “Closed” tag is a non-event for future applications. A “Settled” tag is a near-automatic red flag for the next 3 to 5 years, especially for home and business loans. You can still get credit cards and personal loans, but at higher rates and lower limits. If you have any path to full closure, even a stretched restructured EMI, the CIBIL outcome will be materially better. The CIBIL score and education loan post covers the long-tail impact.

Faz's rule

Settlement closes the loan. Full repayment closes the chapter.

An OTS at 70 percent of outstanding looks like a financial win on the day you sign. The “Settled” tag on your CIBIL for the next 7 years is the part you feel three years later when you apply for a home loan and the bank pulls your report. If full closure is possible at any stretched tenure, take it.

Will I go to jail? The honest answer on Section 138

Non-payment of an education loan is a civil matter. You do not go to jail for failing to repay, no matter what a recovery agent threatens. The Supreme Court has been clear on this for decades.

The one exception is Section 138 of the Negotiable Instruments Act. If you gave the bank post-dated cheques as part of your documentation and one bounces because of insufficient funds or a stop-payment instruction, the bank can file a criminal complaint. The penalty can include a fine of up to twice the cheque amount and up to two years imprisonment. Most Section 138 cases end in settlement before judgment, but the case is criminal, the summons comes from a magistrate’s court, and ignoring it has real consequences including a non-bailable warrant.

If you anticipate a cheque bounce, engage with the bank before presentation. Ask in writing to hold the cheque, and offer a revised payment plan. Banks usually cooperate because filing a 138 case is paperwork they would rather avoid.

What to do BEFORE you default: the conversations that actually help

Almost everything above becomes avoidable if you talk to the bank before the EMI is missed. At the pre-default stage, the bank’s incentive is aligned with yours: keep the account performing.

Restructuring. Banks can extend the tenure (10 years to 15 years), lowering the EMI by 15 to 25 percent. They can also offer a step-up structure with lower EMIs for the first 2 to 3 years. RBI’s framework allows this without treating it as a default, provided you initiate before NPA.

Temporary moratorium extension. With a documented reason (job search, illness, family emergency), most banks extend the moratorium by 6 to 12 months. Interest continues to accrue, but you avoid DPD reporting.

Partial EMI. A formal arrangement where you pay 40 to 60 percent of the EMI for 3 to 6 months and make up the shortfall later. Document it in writing, otherwise the system reports 30+ DPD because the full EMI did not come in.

Loan transfer or refinance. If your risk is driven by a high NBFC rate (12 to 14 percent), refinancing to a public sector bank at 9 to 10 percent drops the EMI by 15 to 20 percent. Only possible while the loan is performing. Once NPA, no bank will take over the file. The education loan repayment strategies post walks through the refinance arithmetic.

What if my co-applicant cannot pay either

The co-applicant is jointly and severally liable. The bank can pursue them for the full amount independently, their CIBIL is hit at the same DPD threshold, and SARFAESI runs against both.

If neither can pay, the same three paths apply: restructure (before NPA), settle (after NPA), or contest in court if the dues are inflated. The realistic outcome in a true joint-default is a negotiated settlement at 50 to 65 percent, paid through liquidation of an asset (FDs, gold, or a property sale on your terms rather than through auction). Painful, but recoverable. Most families rebuild their CIBIL within 4 to 5 years.

The honest closing take

The system is designed to scare you at every stage. The calls, the notices, the “your CIBIL will be ruined forever” warnings, all of it is meant to extract payment. What it leaves out is that the bank’s incentive at every stage is to recover money, not to punish you. A bank that recovers 80 percent via settlement is happier than one that wins a court case in year four for 100 percent.

The borrower’s job is to be the calmer party at the table. Read the notices. Reply in writing. Do not ignore court summons. Make realistic offers backed by proof of funds. The borrowers who get the worst outcomes are the ones who stop replying.

If the loan turned out to be the wrong size or against the wrong outcome, the only useful question from here is how to limit damage to your CIBIL, your co-applicant, and future borrowing. The education loan versus self-funding post covers the upstream decision. The loan rejection reasons post is worth reading if you are at the application stage.

FAQ

What happens if I default on my education loan in India?

After a missed EMI you receive SMS and calls. At 30 days past due, the default is reported to credit bureaus. At 90 days the account is classified as a Non-Performing Asset (NPA), the bank issues a formal demand notice, and the file moves to legal recovery. For secured loans, SARFAESI enforcement begins. For unsecured loans, recovery agents and civil court follow. Most defaults end in restructuring or one-time settlement rather than asset auction.

Will I go to jail for not paying my education loan?

No. Non-payment of a loan is a civil matter in India and does not by itself lead to jail. The Supreme Court has held this consistently. The one exception is Section 138 of the Negotiable Instruments Act, which makes the dishonour of a post-dated cheque a criminal offence punishable by a fine and up to two years imprisonment. If you gave the bank post-dated cheques and they bounce, you can be summoned to a magistrate’s court.

Can the bank take my house if I default on an education loan?

Only if your house was pledged as collateral. For loans secured against immovable property, the bank can enforce under SARFAESI after a 60-day Section 13(2) notice, take symbolic possession, and auction the asset. For unsecured loans (typical up to ₹7.5 lakh from public banks or against a strong co-applicant), the bank cannot seize property directly. They must obtain a civil court decree first, which is a much longer process.

What is a one-time settlement (OTS) on an education loan?

An OTS is a lump-sum payment, lower than the full outstanding, that the bank accepts to close the account. Once a loan is classified as NPA, banks routinely offer OTS to clear non-performing accounts off their books. Typical haircuts range from 5 to 15 percent immediately post-NPA, 15 to 30 percent after legal notice, and 30 to 50 percent on written-off accounts. It is a normal commercial process governed by each bank’s recovery policy.

Does a settlement damage my CIBIL like a default?

Yes, though less severely than an active default. A loan closed via OTS is marked “Settled” or “Written-off and Settled” and stays on your report for 7 years from closure. The “Settled” tag is read by future lenders as a sign of repayment stress and typically makes you a B-grade applicant for 3 to 5 years. A clean “Closed” tag from full repayment is materially better. If you can manage full closure through a restructured EMI, that path is almost always worth the longer timeline.

How long does an education loan default stay on my CIBIL report?

A default record stays on your CIBIL report for 7 years from the date the account is closed, settled, or written off. The impact on your score is heaviest in the first 18 to 24 months and fades as you build fresh credit history with timely payments on other obligations. Disputes can be raised with CIBIL if any entry is factually incorrect.

What happens to my co-applicant if I default?

The co-applicant (usually a parent) is jointly and severally liable for the full outstanding. Their CIBIL is reported at the same DPD thresholds as yours. Recovery actions, including SARFAESI on pledged collateral, run against both. The bank can pursue the co-applicant independently even if you are unreachable or abroad. Keep them in the loop the moment a default risk appears, since options like restructuring need their cooperation.

Can I restructure my education loan if I cannot pay the EMI?

Yes, if you act before the account turns NPA. Banks can extend the tenure (lowering the EMI by 15 to 25 percent), grant a temporary moratorium extension of 6 to 12 months, or convert to a step-up EMI. RBI’s restructuring framework permits this without classifying the account as a default, provided you initiate while the loan is still performing. Once NPA classification kicks in, restructuring is replaced by settlement, and the CIBIL impact is much harder to undo.

Faz · The Honest Journey · 2026