Education loan restructuring and moratorium extension is a formal RBI-permitted process where the bank revises your repayment terms (longer tenure, lower EMI, or extended moratorium) after a genuine financial setback like a job loss, salary cut, or course extension. Most banks allow a 12 to 24 month moratorium extension or a tenure stretch up to the regulatory cap of 15 years. The trade-off is real. Restructured accounts get reported to CIBIL with a “Restructured” tag that sits on your report for years and can hurt future credit applications.

The email I get most often goes the same way. The reader took a job, lost it nine months in, the EMI is still hitting the account, savings are gone, and they just figured out the bank has something called “restructuring.” The question is always the same. Can I do this, what does it cost, and will it wreck my CIBIL.

This post walks through when banks allow it, the formal request process, the CIBIL trade-off in plain language, the new EMI math, and what the RBI framework permits versus what your bank actually offers.

More on managing repayment: the education loan balance transfer india post, the RBI education loan repayment rules post, and the education loan top UP post.

What restructuring and moratorium extension actually mean

Restructuring is the umbrella term. Banks can extend the moratorium (push EMI start out by 6, 12, or 24 months), extend tenure (turn a 10-year loan into 12 or 15), apply a step-up EMI that starts low and ramps up later, or convert overdue interest into a separate funded interest term loan. The menu varies bank to bank.

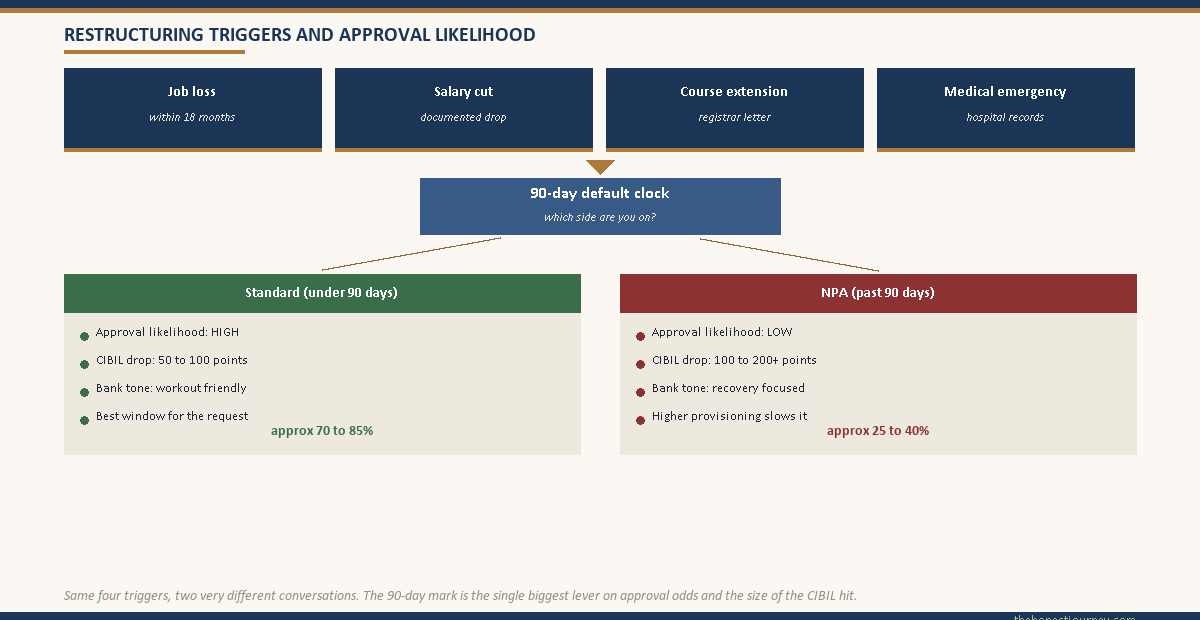

The legal backbone is the RBI’s Prudential Framework for Resolution of Stressed Assets (June 2019, with updates). Under this framework, a bank can restructure a standard account before it slips into NPA. The 90-day default clock is the trigger. Act before day 90 and you are restructuring a standard account. Act after day 90 and you are restructuring an NPA, where the conversation is harder and the CIBIL damage is already done.

Education loan restructuring moratorium extension typically gets approved for three groups. Students whose course got extended (a 2-year master’s stretched to 3 because of a thesis delay or backlog). Fresh graduates who lost their first job or took a salary cut within 12 to 18 months of EMI start. Borrowers facing a documented medical emergency or a parental income loss where the co-applicant cannot service the EMI.

Faz's ruleRestructuring is not a favour the bank does for you. It is a regulated process they are allowed to offer, and the rules are public.

Walk in knowing the RBI framework exists. Most branch managers will not volunteer restructuring as an option. They will push for top-ups, NACH retries, and one-time settlements long before the word restructuring comes up. You have to ask for it by name, in writing, with documentation.

When banks actually allow it (and when they will refuse)

Bank policy decides this, and policy sits behind your written request, your credit file, and the loan officer’s recommendation. The IBA Model Education Loan Scheme that public sector banks broadly follow includes provisions for moratorium extension on grounds of unemployment or course extension, and allows the repayment period to stretch up to 15 years.

Approval likelihood is highest when three conditions are met. The account is still standard (not yet 90 days past due). You have documented proof of the hardship (termination letter, medical records, university letter). You have a credible plan for resuming full EMIs at the end of the restructured period. The bank is not interested in a permanent reduction. They want a believable bridge.

Refusal is common when the loan is already NPA, the hardship is undocumented, the co-applicant has the income to service the EMI (banks will ask), or the borrower has not paid a single EMI yet. Some private banks and NBFCs prefer top-ups, settlements, or sale to an asset reconstruction company over a formal restructuring on their books.

The formal request process step by step

There is no central application form. Each bank handles restructuring through its loan recovery or restructuring cell, and the path is broadly the same.

Step 1. Email the branch manager and loan officer. Use the email IDs on your sanction letter. The subject line should literally say “Request for restructuring of my education loan account under the RBI prudential framework.” Vague subject lines get filed under general queries and lose two weeks.

Step 2. Attach hardship documentation. Termination or relieving letter with the date of separation. Three months of bank statements showing the income drop. For course extension, a letter from the university registrar. For medical, hospital discharge summary and bills. The bank needs a paper trail it can defend in its internal credit committee.

Step 3. Attach a written proposal. One page is enough. State the specific relief (e.g., “12-month moratorium extension followed by EMI restart at a revised tenure of 12 years”). State why it is sufficient. State what you can pay in the interim.

Step 4. Visit the branch in person within a week. Requests that sit only in the inbox get deprioritised. A physical visit moves the file to the credit committee faster than another follow-up email.

Step 5. Get the bank’s response in writing. If approved, the addendum will state the new tenure, the new EMI, the new moratorium end date, and the fact that the account will be reported to CIBIL as restructured. Read this section carefully before signing.

Step 6. Sign the addendum and update your NACH mandate. A fresh NACH registration with the new EMI amount and start date is mandatory. Old mandates do not auto-update. Many “approved” restructurings fall apart because the borrower forgot to register the new auto-debit and bounced the very first revised EMI.

The whole cycle takes 30 to 60 days at a PSU bank and 15 to 30 at a private bank or NBFC. Keep paying whatever you can during the review period to avoid drifting into NPA while the file moves.

The CIBIL trade-off in plain language

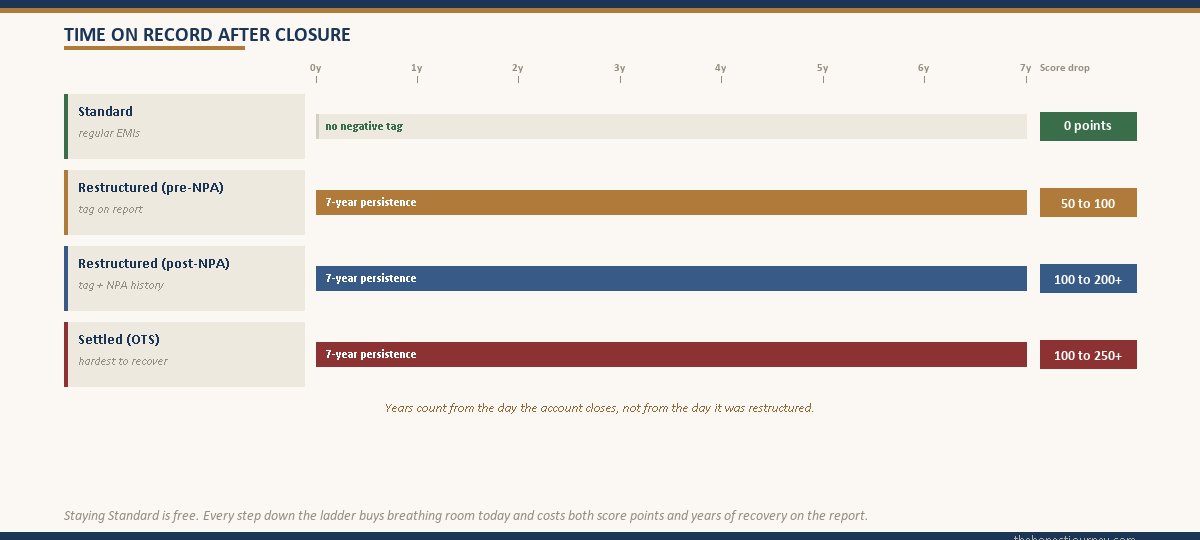

Restructuring is reported to CIBIL. The account status field on your credit report will read “Restructured” instead of “Standard.” The CIBIL TransUnion scoring models treat restructured accounts as a negative signal because they correlate with higher future default rates.

In practice, your CIBIL score drops by 50 to 100 points immediately after restructuring is reported, even if you never missed a single EMI. The “Restructured” tag stays on the account for the remaining tenure and the history persists for up to seven years after closure. For the next two to three years, you will be treated as higher risk on any new credit application (home loan, car loan, credit card limit).

It is not a permanent disqualification. Lenders look at pre-NPA restructuring very differently from post-default restructuring. A pre-NPA restructuring with consistent post-restructuring repayment can be defended in a future loan application with a written explanation. Post-NPA restructuring is closer to default and harder to recover from.

| Account status | Typical CIBIL impact | How long it lingers |

|---|---|---|

| Standard (regular EMI) | Positive, builds score | Ongoing positive history |

| Restructured (pre-NPA) | Drop of 50 to 100 points | Tag on report for loan tenure, history for 7 years after closure |

| Restructured (post-NPA) | Drop of 100 to 200+ points | Tag plus NPA history, 7 years post-closure |

| Settled (OTS) | Drop of 100 to 250+ points | “Settled” tag, 7 years, hardest to recover from |

The honest framing. Restructuring is worse for your credit file than paying on time. It is much better than missing EMIs, drifting into NPA, or doing a one-time settlement. If you genuinely cannot service the current EMI, restructuring is the route that does the least long-term damage to your credit, provided you initiate it before the account slips into default. The full picture of what happens when an education loan is not paid is covered in my what happens if education loan is not paid post.

Faz's rulePre-NPA restructuring is a controlled cost. Post-NPA restructuring is damage control. Settlement is a last resort.

The order of preference for your CIBIL file is: keep paying on time, restructure before day 90, restructure after default, settle for less than the full amount. Each step down the ladder costs you more points and more years of recovery time. The earlier you raise your hand, the cheaper the outcome.

The revised EMI math after tenure extension

The mechanical relief comes from two levers, usually applied together. A moratorium extension pushes the EMI start out by 6 to 24 months. A tenure extension stretches the repayment period and drops the monthly EMI.

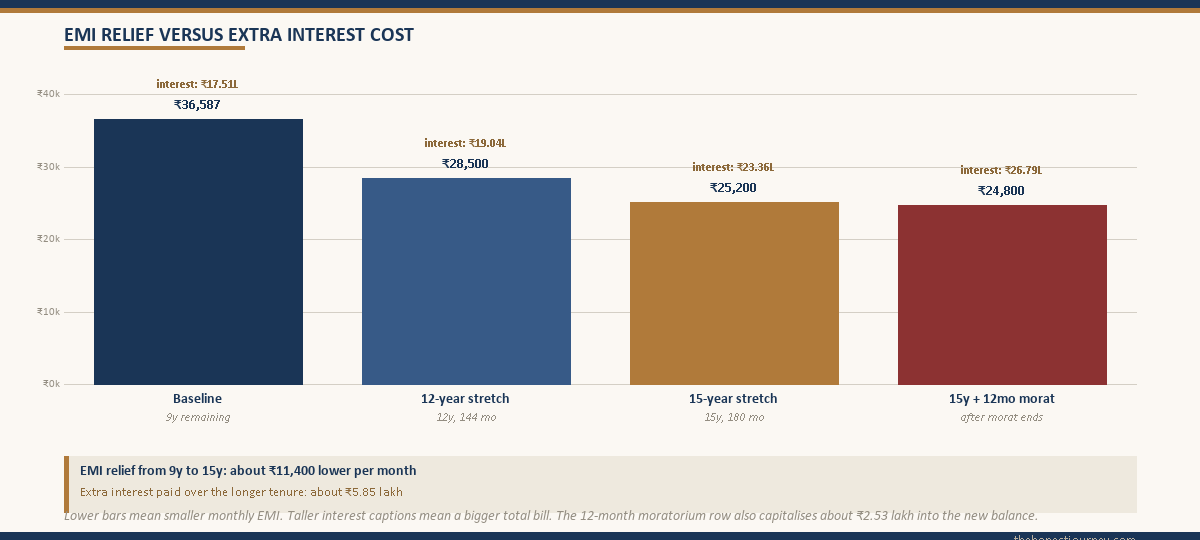

Take a real example. Outstanding balance of 22 lakh after a year of EMIs (started at 25.75 lakh post the original moratorium). Tenure remaining: 9 years. Rate: 11.5 percent. Current EMI: 36,587. The borrower lost their job and needs the EMI cut.

| Restructuring option | Revised tenure | New EMI | Total interest from here |

|---|---|---|---|

| No change (baseline) | 9 years remaining | 36,587 | 17.51 lakh |

| Tenure extension to 12 years | 12 years (144 months) | 28,500 | 19.04 lakh |

| Tenure extension to 15 years | 15 years (180 months) | 25,200 | 23.36 lakh |

| 12-month moratorium + 15-year tenure | 15 years post moratorium | 24,800 (after the new moratorium ends) | 26.79 lakh (includes 2.53 lakh capitalised during the extension) |

Stretching from 9 to 15 years drops the EMI by roughly 11,400 per month. The cost is an extra 5.85 lakh in interest over the longer tenure. A 12-month moratorium extension capitalises another 2.53 lakh into the new balance. If you can pay simple interest during the restructured moratorium (about 21,000 per month on a 22 lakh balance at 11.5 percent), the capitalisation collapses and the total cost drops back toward the tenure-only scenario. Same logic as the moratorium period interest post.

What the RBI framework permits versus what your bank will offer

The RBI framework gives banks significant latitude. The IBA Model Scheme allows tenure extension up to 15 years and contemplates moratorium extension for unemployment and course extension. The Prudential Framework allows restructuring of any stressed account before NPA classification.

What your bank actually offers is narrower. PSU banks tend to follow the IBA Model closely and are more likely to grant 12 to 24 month moratorium extensions and 15-year tenure stretches for documented unemployment. SBI’s education loan scheme handles restructuring through the local branch under the stressed assets framework. Private banks and NBFCs vary. Some restructure willingly to keep the account standard. Others prefer the asset to slip into NPA so they can sell it to an asset reconstruction company. You usually find out which kind you have only when you raise the request.

One option that gets confused with restructuring is EMI bounce remediation. If you have missed one or two EMIs but the account is still under 90 days past due, the bank may restart the NACH mandate, waive the bounce charges, and continue the original terms. That is account regularisation, not restructuring. The CIBIL impact is much smaller (the DPD on missed months reports, but the account stays standard). Covered in detail in my EMI bounce consequences post.

Faz's ruleIf you can solve it with NACH regularisation, do not ask for restructuring. The CIBIL cost is much lower.

Restructuring is the right answer for a 12+ month income gap or a course extension. For a one or two month rough patch, a top-up to the bank account, a NACH retry, and a written explanation of the bounce is the correct route. Match the tool to the size of the problem.

The honest closing take

Restructuring is not a clever workaround. It is an admission to the bank and to the credit bureau that the original plan did not work. The cost is real (50 to 100 CIBIL points, a tag on your report for years, a higher total interest bill). What you buy with it is time, a lower EMI, and a clean record that you did not default.

The decision frame. If the income gap is genuinely 12 months or more and you cannot service the current EMI even with family support, restructure before the 90-day mark. If the gap is 1 to 3 months and you can bridge with family help or partial payments, regularise the account and keep it standard. If you can pay the interest portion but not principal, ask for an interest-only servicing arrangement before going to full restructuring. More repayment levers in my how to repay an education loan in India post.

The biggest mistake I see is waiting too long. By day 90 the account is NPA, the CIBIL damage is done, and the bank’s tone changes from helpful to recovery-focused. The window to control the outcome is the first 60 days of the income shock. Use it.

FAQ

Can I extend my education loan moratorium after the course ends?

Yes, in specific circumstances. Most banks allow a 6 to 24 month extension if you can document a genuine reason like job hunt difficulty in the grace period, a course extension, or a medical emergency. The request goes through the branch in writing with supporting proof. The extended moratorium accrues interest the same way as the original (capitalised into the principal at the end), and the account is reported to CIBIL as restructured. Approval depends on the bank’s internal policy and the strength of your documentation.

How do I formally request restructuring of my education loan?

Email the branch manager and your loan officer with a subject line referencing restructuring under the RBI prudential framework. Attach hardship documentation and a one-page written proposal stating the specific relief you want. Visit the branch in person within a week. The bank’s credit committee usually responds within 30 to 60 days at a PSU bank or 15 to 30 days at a private bank. If approved, you sign an addendum and register a fresh NACH mandate with the new EMI amount.

Does education loan restructuring affect my CIBIL score?

Yes. Restructured accounts are reported with a “Restructured” tag, which typically drops the score by 50 to 100 points if done before the 90-day default mark, and by 100 to 200+ points if done after NPA. The tag stays on the account for the loan tenure and the history persists for up to seven years after closure. It is not a permanent disqualification, but you will be treated as higher risk for new credit applications for two to three years.

Will the bank reduce my EMI after restructuring?

Usually yes, via tenure extension (up to 15 years) or a combined moratorium plus tenure extension. On a 22 lakh outstanding balance, a stretch from 9 years to 15 years drops the EMI from about 36,500 to about 25,200, a relief of roughly 11,300 per month. The trade-off is an additional 5 to 6 lakh in total interest paid over the longer tenure.

How much moratorium extension can I get on an education loan?

The typical range is 6 to 24 months beyond the original moratorium end date. The IBA Model Education Loan Scheme that most PSU banks follow allows extension for documented unemployment or course extension, subject to a maximum total repayment period of 15 years from the original EMI start. Private banks and NBFCs may offer shorter extensions or none at all. The longer the extension, the more interest capitalises during the extended period.

What proof do I need to submit for restructuring approval?

For job loss, a termination or relieving letter and three months of bank statements showing the income drop. For a salary cut, a fresh salary slip and an employer letter confirming the revised CTC. For course extension, a letter from the university registrar with the revised completion date. For medical emergencies, hospital discharge summary, bills, and a doctor’s certificate. The bank wants a paper trail it can defend in its internal credit committee.

Can I restructure if my education loan is already 90 days overdue?

Yes, but the conversation is harder. After 90 days the account is NPA and most of the CIBIL damage is done. Banks can still restructure NPA accounts under the RBI framework, but they must make higher provisions, which makes them more reluctant. The CIBIL hit from post-NPA restructuring is typically 100 to 200+ points versus 50 to 100 for pre-NPA. If you are approaching day 90, raising the request before you cross it is the single highest-value action.

Is education loan restructuring the same as a one-time settlement?

No. Restructuring revises the terms (longer tenure, lower EMI, extended moratorium) and you continue to repay the full amount plus interest under the new schedule. The account stays open and active. A one-time settlement (OTS) is when the bank accepts a lump sum less than the full outstanding balance and closes the account as “Settled.” Settlement is much more damaging to CIBIL (drops of 100 to 250+ points) and the “Settled” tag is one of the hardest negatives to recover from. Restructure first, settle only as a last resort.

Faz · The Honest Journey · 2026