The RBI education loan repayment rules sit across two documents: the RBI Fair Practices Code for Lenders and the Indian Banks Association Model Education Loan Scheme, which together set moratorium length, prepayment penalty rules, interest reset windows and recovery procedure. Public sector banks are bound by the IBA model scheme; NBFCs are not. Prepayment penalty on floating-rate education loans has been prohibited since the RBI circular of May 2014, reaffirmed in 2019. Disputes can be escalated to the RBI Banking Ombudsman through the cms.rbi.org.in complaints portal.

A reader wrote in last month asking why her bank had quietly raised the floating spread on her education loan by 75 basis points without any written notice. She had three years of repayment left, the EMI had climbed about ₹2,800 a month, and the branch manager was telling her it was a routine reset and she had no choice. She did have a choice. Most borrowers do, they just don’t know which rule book to point at.

This post walks through the actual RBI education loan repayment rules: where they live, what they oblige the bank to do, what your rights are at each stage, and how to escalate when the branch refuses to listen.

More on managing repayment: the education loan balance transfer india post, the education loan top UP post, and the should you prepay education loan india post.

Where the rules actually live, and which lenders they bind

There is no single “RBI education loan act”. The rules are scattered across three sources, and the first thing to understand is which one applies to your lender.

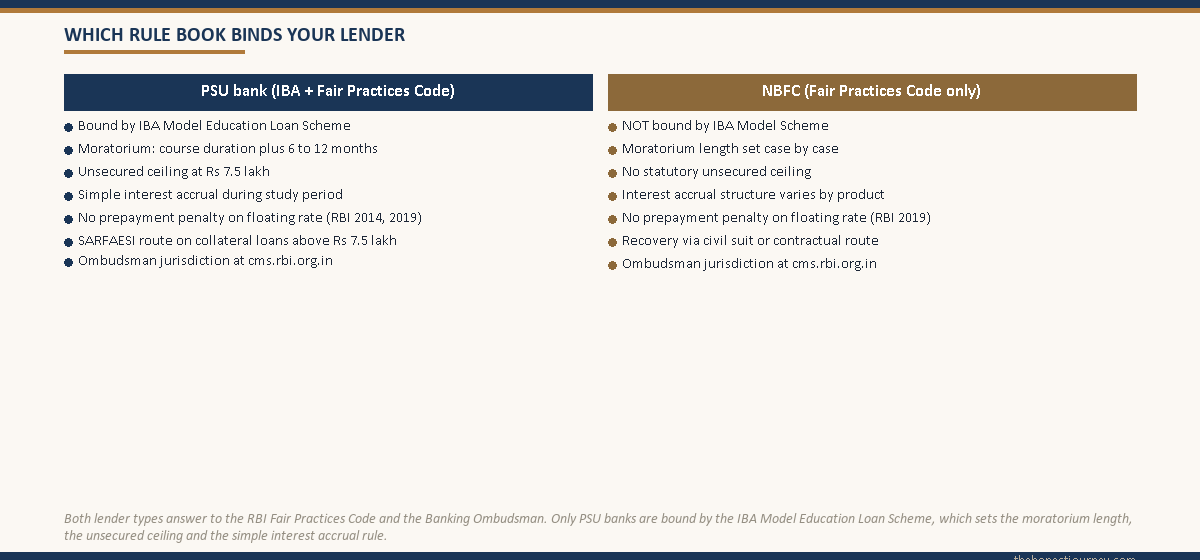

The first is the RBI Fair Practices Code for Lenders, originally issued in 2003 and updated through subsequent Master Directions. It applies to all scheduled commercial banks, all cooperative banks and all NBFCs. It covers loan application acknowledgement, sanction terms communication, changes to terms and conditions, recovery practices and grievance redressal. This is the baseline floor for every education lender in India.

The second is the IBA Model Education Loan Scheme, originally framed in 2001 and revised most recently for the Vidya Lakshmi portal era. This is binding on all member public sector banks and most old-generation private sector banks that have adopted it. The IBA scheme is where you find the moratorium structure, the unsecured ceiling at ₹7.5 lakh, the simple-interest accrual rule during the study period, and the prohibition on margin money for loans under ₹4 lakh.

The third is the body of circulars on specific repayment issues. The two that matter most for repayment are the RBI circular DBOD.Dir.BC.107/13.03.00/2013-14 dated May 7, 2014 prohibiting foreclosure charges on home loans and floating-rate term loans extended to individual borrowers, and the follow-up RBI circular DBR.Dir.BC.No.107/13.03.00/2019-20 dated August 2, 2019 extending the same protection across floating-rate loans for non-business purposes.

NBFCs sit in a different chair. They are bound by the Fair Practices Code and by RBI’s Scale Based Regulation framework, but they are not bound by the IBA Model Education Loan Scheme. So an NBFC can charge prepayment penalty on a fixed-rate education loan, can structure recovery differently, and is not obliged to offer the IBA moratorium length. This is the single most important distinction for borrowers comparing PSU loans against the newer NBFC-led players.

Moratorium rules: course period plus 6 to 12 months

The IBA model scheme sets the moratorium as course duration plus six months after course completion or three months after securing employment, whichever is earlier. In practice, every PSU bank I have seen extends this to course duration plus twelve months, because the six-month version proved unworkable for international students still searching for a first job.

During the moratorium, simple interest accrues on the disbursed portion of the loan. It does not compound. At the end of the moratorium, this accrued simple interest is capitalised (added to the principal) and the EMI is calculated on the new combined principal. So if your sanction was ₹25 lakh, you disbursed ₹20 lakh across the program, and the simple interest accrued during 4 years of study plus 1 year of grace came to ₹6 lakh, your repayment starts on a principal of ₹26 lakh.

Some banks offer an interest-servicing option during the moratorium at a lower spread, typically 0.5 to 1 percent below the standard rate. Under this option, you pay the accruing monthly interest from your own (or family’s) funds during the study period, and repayment at the end starts on the original disbursed principal only. Over a 10-year tenor on a ₹20 lakh loan, this can save ₹3 to 4 lakh in total interest. The mechanics of which banks offer this and the trade-offs are covered in the education loan restructuring and moratorium extension post.

The moratorium can be extended in genuine cases: a delayed graduation, a continuation into a higher degree, a documented health issue, or unemployment beyond the 12-month window. The IBA scheme explicitly contemplates a second 12-month extension on written request with proof. PSU banks routinely grant the first extension and contest the second. NBFCs handle extensions case by case.

Faz's ruleAsk for the interest-servicing option in writing at sanction, even if you do not plan to use it, so the option is on the loan agreement and not a verbal promise.

The interest servicing variant exists at SBI, Bank of Baroda and Canara Bank under different product names, but it is not the default. Branches will offer the standard moratorium unless you ask. If you intend to switch from accumulation to servicing partway through the course (because a family member has agreed to fund the monthly interest), get that switch in writing from the branch credit officer before you start paying. Verbal switches do not show up in the loan account ledger and the interest gets capitalised anyway.

Prepayment penalty: prohibited on floating-rate education loans

This is the rule most education loan borrowers do not know they have. The RBI circular dated May 7, 2014 prohibited foreclosure charges and prepayment penalties on home loans and on all floating-rate term loans extended to individual borrowers for non-business purposes. The August 2, 2019 circular widened this protection across floating-rate loans on non-business end-use, including education.

What this means in practice:

| Loan type | Lender | Prepayment penalty allowed? |

|---|---|---|

| Floating-rate education loan | PSU bank / private bank | No (RBI 2014 + 2019 circulars) |

| Fixed-rate education loan | PSU bank / private bank | Yes, if specified in sanction (typically 2 to 4 percent) |

| Floating-rate education loan | NBFC | No (RBI 2019 circular) |

| Fixed-rate education loan | NBFC | Yes (no RBI restriction) |

Almost every PSU bank education loan in India is floating-rate, benchmarked to the bank’s MCLR or EBLR (External Benchmark Lending Rate). The SBI Education Loan product, for example, is benchmarked to EBLR + spread, which makes it floating-rate by definition. So any branch quoting a 2 percent foreclosure fee on an SBI education loan in 2026 is in violation of the 2014 and 2019 RBI circulars.

If the branch insists, ask them in writing to cite the RBI circular that permits the charge, given the 2014 and 2019 prohibitions. Most branch managers back down at the written request stage because the charge is automated in the loan management system and they cannot defend it on the record. If they do not back down, this is a Banking Ombudsman complaint and a very winnable one.

Fixed-rate loans are different. If your sanction letter explicitly states the loan is fixed-rate and the rate does not move with MCLR or EBLR, the bank is permitted to charge a prepayment penalty, usually 2 to 4 percent of the outstanding principal, provided it was disclosed at sanction. Fixed-rate education loans are rare in India and almost always a deliberate choice by the borrower.

Interest reset windows and unilateral hikes

Floating-rate education loans reset at a frequency stated in the sanction letter: monthly, quarterly, half-yearly or yearly. The most common is quarterly reset for EBLR-linked loans and yearly reset for older MCLR-linked loans. The reset means the spread above the benchmark stays fixed for the tenor, but the benchmark itself moves with the bank’s published rate.

What the bank cannot do, under the Fair Practices Code, is unilaterally widen the spread above the benchmark without your written consent or without the contractual trigger being met. The sanction letter and loan agreement specify the spread (for example, EBLR + 2.00 percent). The benchmark moves freely; the spread does not, unless the agreement explicitly allows a re-pricing event.

If your EMI jumps and the bank attributes it to the benchmark, ask for the bank’s published EBLR or MCLR on the reset date and on the prior reset date. The increase in EMI should reconcile to the benchmark movement times your outstanding principal, divided over the remaining tenor. If it does not reconcile, the bank has widened the spread, which is a re-pricing event and requires either written consent or a contractual trigger.

The Fair Practices Code obliges the lender to give written notice of any change in terms and conditions, including the interest rate, with the effective date. A quiet system-driven hike with no email and no SMS is a Code violation. Pull your sanction letter, pull the bank’s published benchmark history (every PSU bank publishes this monthly on its website), and reconcile. If they don’t reconcile, you have grounds to push back.

Recovery process: SARFAESI for collateral, civil suit for unsecured

If a loan goes into default, the recovery path depends on whether it is secured or unsecured.

For loans above ₹7.5 lakh that are collateralised (typically with immovable property, fixed deposits, or LIC policies), the bank can invoke the SARFAESI Act 2002. Under SARFAESI, after the account is classified as a Non-Performing Asset (90 days of non-payment), the bank issues a 60-day notice under Section 13(2) calling on the borrower and guarantors to pay. If the demand is not met, the bank can take symbolic possession of the secured asset under Section 13(4), and physical possession with magistrate assistance under Section 14. The borrower has the right to file an appeal to the Debt Recovery Tribunal under Section 17.

For loans up to ₹7.5 lakh, which are unsecured under the IBA scheme, SARFAESI does not apply. The bank’s only recovery route is a civil suit for recovery in the appropriate court, or, for smaller amounts, a Lok Adalat settlement. Civil suits take 3 to 7 years in most Indian jurisdictions, which is why unsecured education loan default cases often sit in collection limbo for years before any formal action.

What both routes require, before any formal action, is proper notice. The Fair Practices Code obliges the lender to give a written demand notice with a reasonable opportunity to cure (typically 30 days for unsecured, 60 days statutory under SARFAESI for secured) before initiating recovery proceedings. The notice must specify the outstanding amount, the default period, and the consequences. A bank that starts recovery without this notice has a procedural defence handed to the borrower.

The recovery agent rules are also worth knowing. The Fair Practices Code on recovery (the most-cited section in ombudsman complaints) prohibits intimidation, calls outside 8 AM to 7 PM, contact with employer or neighbours without consent, and verbal abuse. Documented violations are an immediate ombudsman ground and can result in the lender being directed to pay compensation. The mechanics of how a default first triggers and what the bank does in the first 90 days are covered in the education loan EMI bounce consequences post.

Banking Ombudsman escalation: how it actually works

The RBI Banking Ombudsman is the dispute resolution authority for grievances against any RBI-regulated entity, which covers every scheduled commercial bank, cooperative bank and NBFC in India. The complaint portal is cms.rbi.org.in and it is free to use.

The process has a prerequisite: you must have first complained to the bank in writing and either received an unsatisfactory response or no response within 30 days. The bank’s first response must come from the designated Nodal Officer (every bank publishes this on its website under “grievance redressal”). Skipping the bank’s internal process and going directly to the ombudsman results in the complaint being routed back to the bank, which adds another 30 days.

The actual sequence:

- Write to the branch manager with your grievance. Reference the specific Fair Practices Code clause or IBA scheme rule the bank has breached. Keep the tone factual. Give the bank 15 working days to respond.

- If no resolution, escalate to the bank’s Nodal Officer for Customer Service in writing. This contact is on every bank’s “grievance redressal” page. Give them another 15 working days.

- If still no resolution after 30 days total, or if you receive a reply you find unsatisfactory, file with the RBI Banking Ombudsman at cms.rbi.org.in. The complaint form needs your bank correspondence as proof of the prior escalation. You will get a complaint reference number immediately.

- The ombudsman office assigns the complaint to an officer who hears both sides. Most complaints are resolved within 60 to 90 days. The award can include refund of incorrectly charged fees, restoration of correct interest rates, and compensation up to ₹20 lakh for documented losses or harassment.

The complaints that succeed are the ones with documentation: copies of the sanction letter, the loan agreement, the bank statements showing the disputed charge, and copies of every email exchanged. The complaints that fail are vague (“my EMI is too high”) with no specific Code or scheme violation cited. Be specific. Cite the rule. Attach the proof.

Faz's ruleIf you are going to file an ombudsman complaint, screenshot the bank's published MCLR or EBLR history for your loan period before you complain. Banks update those pages and old benchmarks vanish.

I have seen two ombudsman cases where the borrower had a clean reconciliation argument but lost time because the bank’s website no longer showed the historical benchmark on the relevant reset date. Save the page as a PDF or use the Wayback Machine to pull the archived version, the same week you realise something is off. Documentation built after the fact carries less weight than documentation built in real time.

Borrower rights at a glance

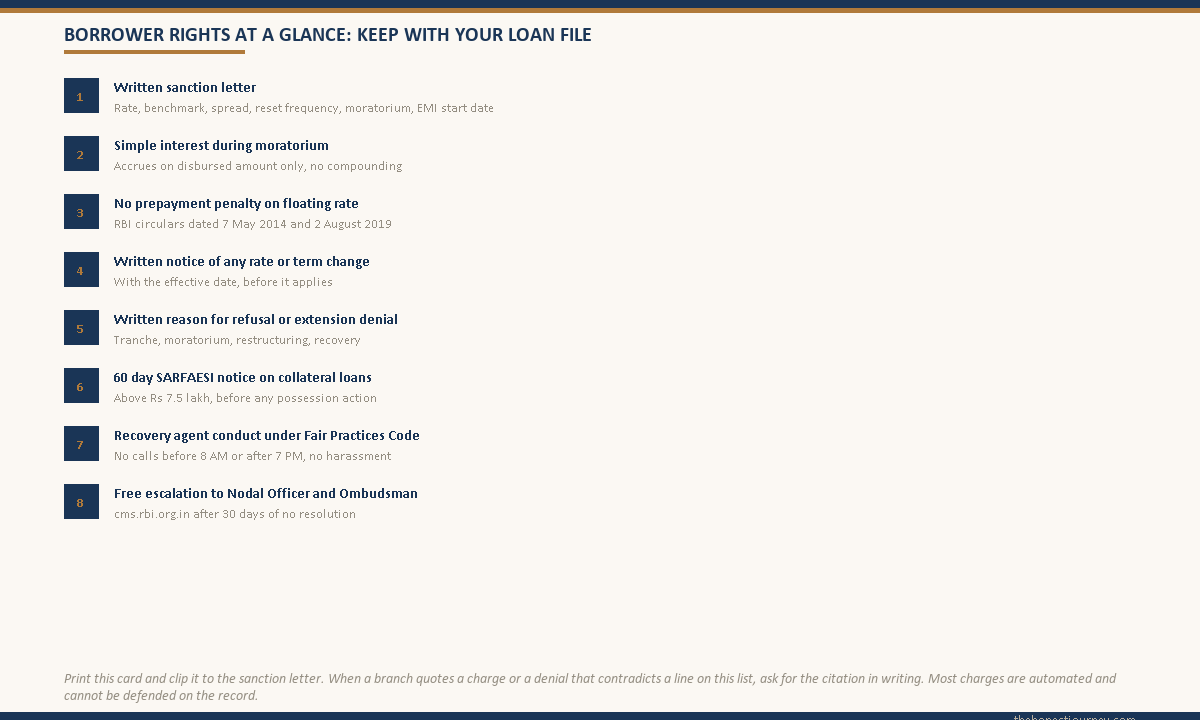

Pulled together from the Fair Practices Code, the IBA Model Scheme and the relevant RBI circulars, the borrower rights under an education loan in India are:

- Right to a written sanction letter stating all terms, including rate, benchmark, spread, reset frequency, moratorium length and EMI start date.

- Right to interest accrual on the disbursed amount only during the moratorium, on simple-interest basis if no servicing option is taken.

- Right to prepayment without penalty on any floating-rate education loan (RBI 2014 and 2019 circulars).

- Right to written notice of any change in terms and conditions, including interest rate movements, with the effective date.

- Right to a written reason for any tranche refusal, moratorium extension denial or recovery action.

- Right to the 60-day SARFAESI notice (for collateral loans above ₹7.5 lakh) before any possession action.

- Right to recovery agent conduct that complies with the Fair Practices Code on collection.

- Right to escalate to the Nodal Officer within the bank and to the RBI Banking Ombudsman thereafter, free of cost.

For Section 80E tax deductions on interest paid during repayment, the certificate the bank issues becomes the supporting document; that mechanic is in the education loan interest certificate post. And if you were rejected at sanction stage for reasons that look procedurally weak, the equivalent regulatory ground is covered in the education loan rejection reasons post.

The honest closing take

The frustrating part of education loan repayment in India is not that the rules are weak. The rules are actually reasonable, particularly the IBA scheme on PSU bank loans. The frustrating part is that the rules are spread across a Fair Practices Code, a Model Scheme document, and a stack of circulars, and most branch officers have never read the circulars. So borrowers end up arguing against a system that quietly applies whatever its software defaults to, and the burden of citing the rule lands on the borrower.

What works is being specific. “My EMI looks wrong” never moves anything. “Per the RBI circular dated August 2, 2019, prepayment penalty on a floating-rate non-business loan is prohibited, and my sanction letter dated X confirms this is a floating-rate loan benchmarked to EBLR” moves things, because the branch manager now has to defend the charge in writing.

The other thing that works is the ombudsman portal. It is free, the timelines are real, and the awards are enforceable. Most borrowers never use it because they assume it is a bureaucratic dead end. It is not. The complaints with documented breaches of specific Code clauses get resolved, and the bank pays. The complaints that fail are the ones that never name a specific rule.

For NBFC loans, you have fewer rules to point at because the IBA scheme does not bind them. But the Fair Practices Code still applies, the floating-rate prepayment ban still applies, and the ombudsman still hears the case. The differences are real, but the floor is not as low as some borrowers fear.

FAQ

What are the RBI rules on education loan repayment?

The rules sit across the RBI Fair Practices Code for Lenders, the IBA Model Education Loan Scheme that binds public sector banks, and specific RBI circulars on prepayment and benchmark-linked rates. Together they set the moratorium structure (course duration plus 6 to 12 months grace), require simple interest accrual on disbursed amounts during the moratorium, prohibit prepayment penalty on floating-rate education loans, oblige written notice of any change in terms, and require a 60-day SARFAESI notice before possession action on collateral loans above ₹7.5 lakh.

Is prepayment penalty allowed on education loans?

No, not on floating-rate loans. The RBI circular dated May 7, 2014 prohibited foreclosure charges on floating-rate term loans extended to individual borrowers for non-business purposes, and the August 2, 2019 circular widened the protection across all floating-rate non-business loans. Since almost every PSU bank education loan is benchmarked to EBLR or MCLR (and is therefore floating-rate), prepayment penalty is prohibited. Fixed-rate education loans are an exception and can carry prepayment charges if disclosed at sanction.

What is the moratorium period rule under RBI guidelines?

The IBA Model Education Loan Scheme sets the moratorium at course duration plus six months after course completion or three months after employment, whichever is earlier. In practice, every public sector bank extends this to course duration plus twelve months because the six-month version proved unworkable for international students searching for a first job. Simple interest accrues on the disbursed portion during the moratorium and is capitalised at the end. A second 12-month extension is available on written request with documented proof of unemployment, health issue or course extension.

How do I complain to the RBI Banking Ombudsman?

First complain to your branch in writing, then escalate to the bank’s Nodal Officer for Customer Service if the branch does not resolve it within 15 working days. If 30 days pass without resolution or the bank’s reply is unsatisfactory, file at cms.rbi.org.in with copies of all prior correspondence. The complaint must cite the specific Fair Practices Code clause, IBA scheme rule or RBI circular the bank has breached. The ombudsman office assigns an officer, hears both sides, and most cases are resolved within 60 to 90 days at no cost to the complainant.

Can banks change my education loan interest rate unilaterally?

The bank can pass through movements in the benchmark (EBLR or MCLR) at the contracted reset frequency, but it cannot widen the spread above the benchmark without your written consent or a specified contractual trigger. The Fair Practices Code also obliges the bank to give written notice of any change in terms with the effective date. If your EMI jumps and the increase does not reconcile to the published benchmark movement times your outstanding principal, the bank has widened the spread and you have grounds to escalate first to the Nodal Officer and then to the ombudsman.

Do RBI rules apply to NBFC education loans?

The Fair Practices Code and the RBI Scale Based Regulation framework apply to NBFCs, but the IBA Model Education Loan Scheme does not. So NBFCs are bound by the floating-rate prepayment ban and by the Code on recovery practices, written notice and grievance redressal, but they are not bound by the IBA moratorium length, the unsecured ceiling at ₹7.5 lakh, or the simple-interest accrual rule. NBFC borrowers can still escalate to the RBI Banking Ombudsman, which has jurisdiction over all RBI-regulated lenders.

What is the recovery process if I default on an education loan?

For collateral loans above ₹7.5 lakh, the bank can invoke the SARFAESI Act 2002 after the account is classified as an NPA at 90 days of non-payment, issuing a 60-day notice under Section 13(2) before any possession action. For unsecured loans up to ₹7.5 lakh, SARFAESI does not apply and the bank’s only route is a civil suit for recovery or a Lok Adalat settlement. In both routes, the Fair Practices Code requires written demand notice with a reasonable cure period before recovery proceedings, and recovery agent conduct must comply with the Code on collection.

What documents should I keep to enforce my borrower rights?

Keep the original sanction letter, the signed loan agreement, every disbursement confirmation, every interest certificate (one per financial year), every email exchanged with the branch, and a saved copy of the bank’s published EBLR or MCLR history for each reset date during your loan tenor. If you ever need to argue a wrongful charge, an unauthorised spread widening, or a procedural breach, the case rests on these documents. Banks update their websites and old benchmarks vanish, so save the benchmark page as a PDF on each reset date rather than relying on the bank’s archive.

Faz · The Honest Journey · 2026