For funding education, I would take an education loan over a personal loan every time. Rates run 8 to 14 percent against 11 to 24 percent, tenure stretches to 15 years versus 5, and only the education loan carries the Section 80E interest deduction. On a ₹5 lakh borrowing the lifetime cost difference is typically ₹2 to 3 lakh.

A friend’s cousin asked me last month whether he should take a personal loan for his MBA. The education loan paperwork was taking too long, his admission deadline was three weeks away, and a pre-approved personal loan offer was sitting in his banking app at the tap of a button. He wanted to know if the difference really mattered. He was about to sign for ₹5 lakh.

It mattered. By the time we finished walking through the actual math, the gap between the two options on that ₹5 lakh was roughly ₹2.3 lakh over the life of the loan, plus the tax deduction he would have lost. This post is the same conversation, written down, so you can run the numbers before you tap that button.

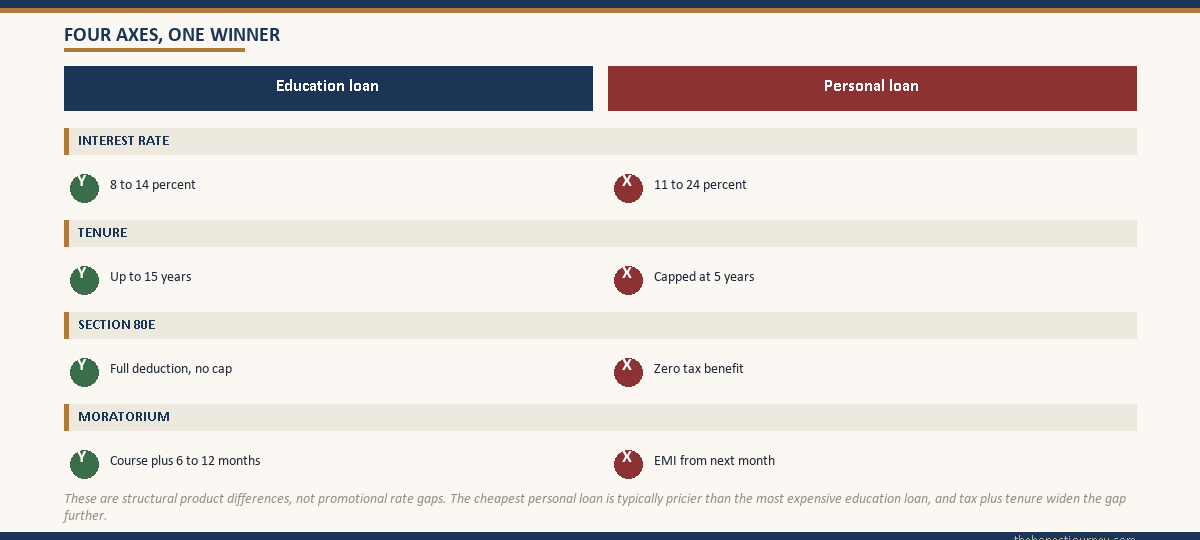

For funding education, an education loan beats a personal loan on every single axis that matters. Rates run 8 to 14 percent versus 11 to 24 percent. Tenure is up to 15 years versus 5. Section 80E tax deduction applies to one and not the other. A moratorium covers your study years on the education loan; the personal loan EMI starts next month. On a ₹5 lakh borrowing, the lifetime cost difference is typically ₹2 to 3 lakh.

The loan basics nearby: the what education loan covers post, the education loan EMI calculator math post, and the RBI guidelines education loan post.

The four reasons education loan vs personal loan is not a fair fight

People treat this as a close call because both loans put rupees in your account. Mechanically they look similar. Financially they are not in the same category, and the reasons are structural, not marketing.

Interest rate. Education loans from public sector banks sit between 8.5 and 11 percent today. Private banks and the larger NBFCs run 11 to 14 percent for unsecured exposure. Personal loans start at 11 percent for the cleanest salaried profiles and stretch comfortably past 18 to 24 percent for anyone outside that narrow band. The RBI publishes weighted average lending rate data and the gap shows up clearly in every release on the RBI site. The cheapest personal loan is typically more expensive than the most expensive education loan.

Tenure. Education loans run up to 15 years per the IBA model scheme that most public sector banks follow. The full text of the scheme is on the Indian Banks’ Association site. Personal loans cap at 5 years at most lenders, and 6 to 7 at a handful. Longer tenure means lower monthly EMI for the same amount, which matters when you are repaying out of a starting salary.

Tax deduction under Section 80E. The interest you pay on an education loan is fully deductible under Section 80E for 8 years from the year you start repayment. No cap on the deduction amount. The clause is at incometaxindia.gov.in. Personal loans get zero tax benefit. None. If you are in the 30 percent slab, every ₹1 lakh of interest you pay on an education loan saves you ₹30,000 in tax. The same interest paid on a personal loan saves you nothing.

Moratorium. Education loans give you the course duration plus 6 to 12 months of grace before EMIs begin. You can focus on the degree without an EMI hitting your account every month. Personal loans start EMI the month after disbursal. If you take a personal loan in August to pay fees, the September EMI is non-negotiable.

Faz's ruleThe education loan is not just cheaper. It is a different product designed for a different problem.

A personal loan is built for someone with a stable salary who needs cash for a wedding, a medical bill, or a renovation. An education loan is built for someone whose income starts two years from now. Treating them as substitutes is a category error, not a financial trade-off.

The ₹5 lakh worked example, line by line

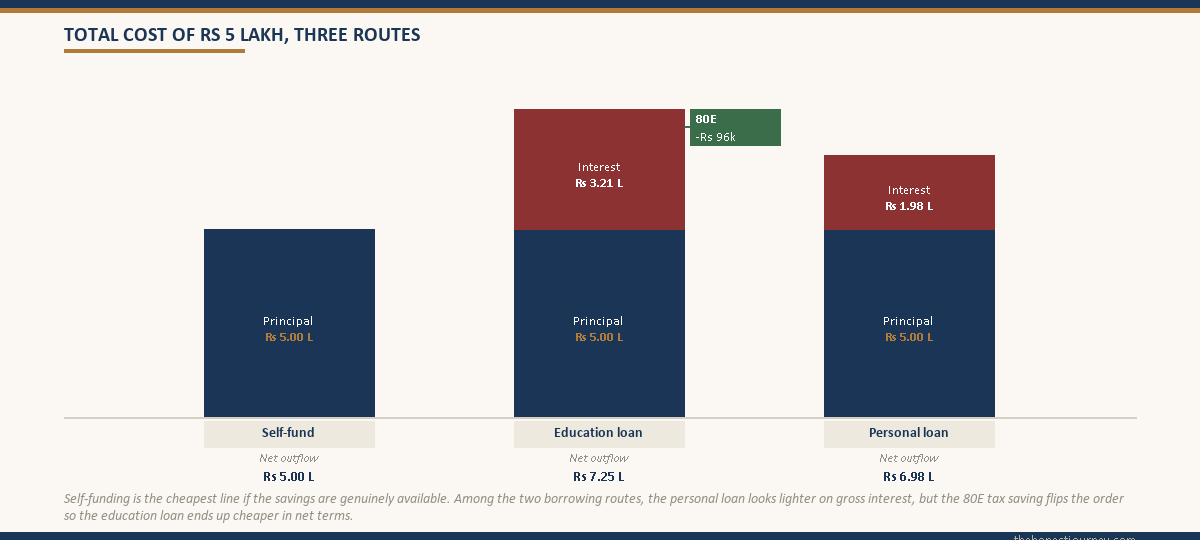

Numbers do the talking. Same borrowed amount, same rough timeline, two products. Education loan at 10.5 percent for 7 years (modest tenure for a small ticket, post 1-year grace). Personal loan at 14 percent for 5 years, EMI starting immediately. Both numbers are real market rates I have seen quoted in 2025 to 2026.

| Parameter | Education loan (₹5L) | Personal loan (₹5L) |

|---|---|---|

| Interest rate | 10.5 percent | 14 percent |

| Tenure | 7 years (84 months) | 5 years (60 months) |

| Moratorium | 2 years (interest accrues) | None |

| Monthly EMI | ₹8,470 (after grace) | ₹11,634 (from month 1) |

| Total interest paid | ₹3.21 lakh (with capitalized interest) | ₹1.98 lakh |

| 80E tax saving (30 percent slab) | ₹96,000 | ₹0 |

| Net cost after tax benefit | ₹2.25 lakh | ₹1.98 lakh |

Look at the bottom row carefully. On total interest before tax, the personal loan actually looks cheaper because the tenure is shorter and the moratorium on the education loan capitalizes interest. But once Section 80E is applied (assuming the borrower or co-applicant is in the 30 percent slab), the education loan wins by roughly ₹27,000 in net cost on a ₹5 lakh borrowing.

That is the conservative scenario. Most students take education loans for amounts closer to ₹10 to 20 lakh, where the absolute interest amounts are larger and the 80E saving becomes meaningfully bigger. Stretch the tenure to 10 years instead of 7 and the monthly EMI falls further, which is the whole point of having a 15-year tenure ceiling available. The personal loan does not give you that lever.

For a deeper breakdown of the rates each bank is actually offering in 2026, I have run the numbers in the education loan interest rate comparison post.

What Section 80E actually covers (and why personal loans cannot touch it)

Section 80E of the Income Tax Act allows a deduction for interest paid on a loan taken for higher education. The exact language matters here because it explains why a personal loan, even if used for tuition, does not qualify.

The section requires the loan to be taken from “a financial institution or an approved charitable institution” for the purpose of “higher education.” Higher education is defined as any course pursued after senior secondary, in India or abroad, from a recognised institution. The deduction is on interest only, not principal, and runs for 8 assessment years from the year repayment begins. There is no upper limit on the deduction amount. Full text at incometaxindia.gov.in.

The catch is in the loan documentation. The lender’s sanction letter has to state that the loan is for education. Banks and NBFCs that issue education loans build this into the standard sanction document. A personal loan sanction does not say “for higher education” because it is a personal loan, sanctioned against your repayment capacity for any end use. The income tax officer assessing your return uses the sanction letter to verify the deduction. A personal loan sanction letter will not pass that test, no matter what you actually spent the money on.

Faz's ruleThe 80E benefit lives in the sanction letter, not in how you spend the money.

I have seen people argue that they used a personal loan for tuition and therefore should qualify. The income tax department does not care what you spent it on. It cares what the lender’s sanction document says the purpose of the loan was. If it does not say “education,” 80E does not apply.

The rare cases where a personal loan is the right call

I want to be honest here because real life does not always fit the textbook answer. There are three scenarios where a personal loan, despite the structural disadvantages, is worth considering.

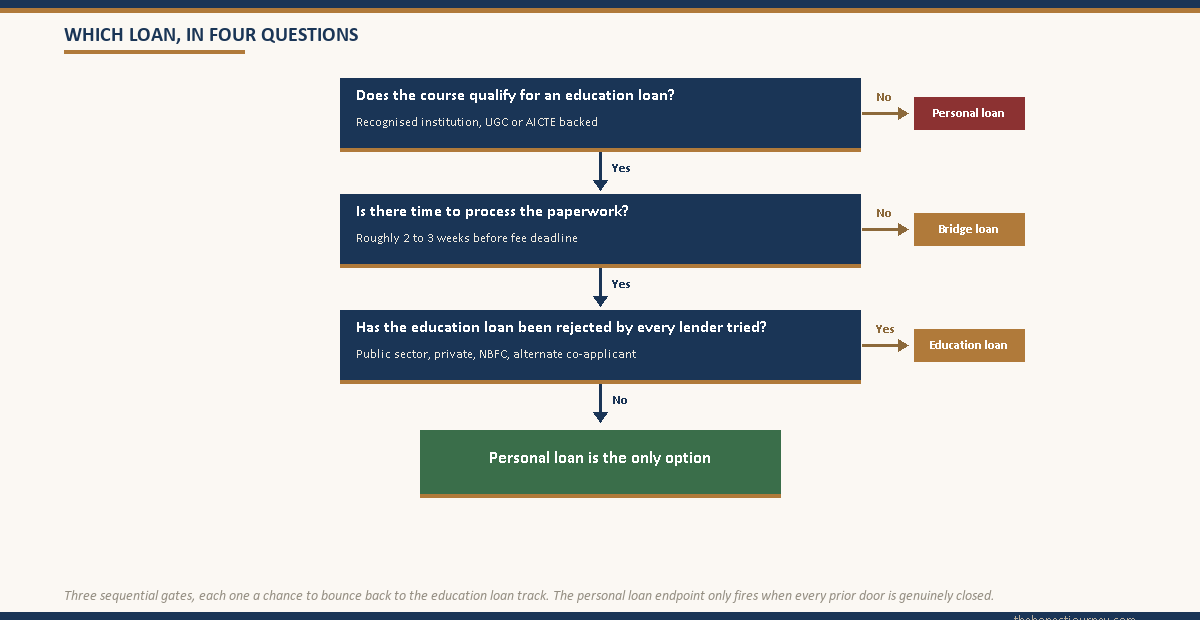

Bridge funding when your education loan is delayed. Your education loan is sanctioned, but the first disbursement is stuck in paperwork and your fee deadline is in two weeks. A short-tenure personal loan can bridge the gap. You pay it off as soon as the education loan disburses. The total cost is bounded because the tenor is short, and you protect your admission. This is the only time I would suggest tapping that pre-approved offer.

Very short courses that no bank will fund. A 3-month certification, a 6-week boot camp, or a self-paced online course that does not have UGC or AICTE backing will not get an education loan from a public sector bank. NBFCs are sometimes more flexible but not always. If the course costs ₹50,000 to ₹1 lakh and the education loan route is closed, a personal loan is the realistic alternative. The absolute interest amount is small enough that the structural disadvantages matter less.

Your education loan got rejected. Co-applicant CIBIL is low, the course is not in the bank’s approved list, or the institution is unrecognised. You can dispute and reapply, look at NBFC options, or escalate. If all those fail and you still need to enrol, a personal loan is the fallback. But before you accept that the education loan is closed, exhaust every option. The numbers above show why it is worth the effort.

For working professionals especially, there is also the education loan top-up option if you already have an existing education loan and need more funds for an additional course. That sits above either of the two products discussed here.

Why the personal loan offer feels easier (and what that easiness costs you)

The reason the personal loan feels like the obvious choice in the moment is that the friction is much lower. Pre-approved offers from your salary account bank can disburse in 24 hours with three taps. The education loan needs co-applicant documentation, admission letter, fee structure, course details, sometimes collateral paperwork, and 7 to 21 days of processing. When the deadline is close, the path of least resistance wins.

The bank knows this. The pre-approved personal loan exists because someone in the lender’s risk team calculated that you are profitable to lend to at 14 to 18 percent, and the cost of acquisition is essentially zero because you are already a customer. The product is engineered to feel frictionless because friction is what makes you stop and compare.

The frictional cost of doing the education loan paperwork is roughly 10 to 15 hours of effort spread over 2 to 3 weeks. The financial benefit of choosing the education loan, on a ₹5 lakh borrowing, is somewhere around ₹27,000 to ₹50,000 depending on your tax slab and tenure. That is ₹2,000 to ₹5,000 per hour of paperwork. Hard to beat that hourly rate anywhere else.

The self-funding question that sits above all of this

Before you even compare the two loan products, the question worth asking is whether you should be borrowing at all for this specific course. If the course cost is ₹1 to 3 lakh and your family savings can absorb it without disrupting any goal, the cheapest loan is the one you do not take. The interest you save plus the tax complexity you avoid plus the CIBIL impact you sidestep is worth real consideration.

Where this gets nuanced is when there are alternative uses for that savings (a parent’s medical buffer, a younger sibling’s education, a down payment plan). Then the question becomes opportunity cost. The full version of this trade-off is in the education loan vs self-funding post if you want to walk through it before you commit either way.

The honest closing take

If the course you are funding qualifies for an education loan, take the education loan. The rate is lower, the tenure is longer, the tax benefit is real, and the moratorium gives you breathing room. The only reason you would choose a personal loan instead is friction or timing, and the cost of trading away those structural benefits for convenience is measurable in lakhs, not thousands.

The exception is bridge funding. If your education loan is approved but the disbursement is delayed, a short personal loan that you pay off within 6 to 12 months is a defensible move. The total interest paid is small because the tenor is short, and you keep your admission. Outside of that specific case, and outside the genuine no-other-option scenarios, the personal loan is the more expensive product wearing better marketing.

Run your own ₹5 lakh numbers. Or ₹10 lakh or ₹20 lakh, whichever fits your actual borrowing. Apply your tax slab. Add the moratorium math if relevant. The answer will land where the structural math always lands, but doing it yourself is the thing that makes you trust the answer when the bank’s relationship manager is pushing the other product.

Faz's ruleThe right loan for education is the one designed for education. Everything else is a workaround.

I have never seen a worked example where, for a course that qualified for an education loan, a personal loan came out ahead once 80E and the moratorium were both factored in. If you find one, check the assumptions. Usually the tax benefit was left out or the tenure was set artificially short on the education loan.

FAQ

Should I take an education loan or a personal loan for studies?

Take the education loan if the course qualifies. The interest rate is typically 3 to 10 percentage points lower, the tenure can stretch to 15 years versus 5 for personal loans, Section 80E gives you a full tax deduction on the interest, and the moratorium means no EMIs during your study years. On a ₹5 lakh borrowing, the net cost saving after tax benefit is usually ₹25,000 to ₹50,000. The only reason to choose a personal loan is bridge funding, a course that does not qualify, or a confirmed education loan rejection.

Why is an education loan cheaper than a personal loan?

Education loans are a regulated product category with priority sector classification under RBI guidelines, which lowers the bank’s cost of capital. Banks also recognise that education loan repayment starts after the borrower is earning, which spreads default risk differently. Personal loans are pure unsecured retail lending priced on individual credit risk with no priority sector benefit. The result is education loan rates of 8 to 14 percent versus personal loan rates of 11 to 24 percent. The structural rate gap typically does not close even for borrowers with excellent credit profiles.

Can I claim Section 80E tax deduction on a personal loan used for education?

No. Section 80E requires the loan to be specifically taken for higher education from a financial institution or approved charitable institution. The sanction letter must state that the purpose of the loan is education. A personal loan sanction does not contain this purpose, regardless of how you actually spent the money. The income tax department uses the sanction letter to verify the claim. You cannot retroactively reclassify a personal loan as an education loan for tax purposes. This is the single biggest hidden cost of choosing the wrong product.

What is the EMI difference between an education loan and a personal loan on ₹5 lakh?

On ₹5 lakh, an education loan at 10.5 percent over 7 years gives an EMI of around ₹8,470 (after the moratorium ends). A personal loan at 14 percent over 5 years comes to roughly ₹11,634 per month, starting immediately. The personal loan EMI is roughly ₹3,164 higher and the repayment burden begins right away. Stretch the education loan tenure to 10 years and the EMI drops further. The longer tenure flexibility is one of the main structural advantages.

How long is the moratorium on an education loan?

For most Indian education loans, the moratorium covers your full course duration plus a grace period of 6 to 12 months after completion. So a 2-year master’s program typically gets a 30 to 36 month moratorium. A 4-year MBBS abroad can stretch to 60 months. Interest accrues during this period and is typically capitalized at the end. Personal loans have zero moratorium. The EMI starts the month after disbursal regardless of your earning situation. For a full breakdown of moratorium costs, see the education loan moratorium post.

Can I get an education loan rejected and then take a personal loan?

You can, but exhaust your options first. If your education loan was rejected by one bank, try another (rejection reasons vary by lender’s internal policies). Public sector banks, private banks, and NBFCs use different underwriting criteria. If co-applicant CIBIL is the issue, a guarantor or different co-applicant can help. If the course is not on the approved list, NBFCs like the larger education-focused ones are usually more flexible. Only after these routes are closed does the personal loan become the realistic fallback for funding the enrolment.

Is a personal loan ever better than an education loan?

Only in narrow scenarios. Bridge funding when your education loan disbursement is delayed but the admission deadline is not. Very short courses (under ₹1 lakh, 3 to 6 months) that no bank will fund as an education loan. Or as a fallback when the education loan route is genuinely closed. In each of these, the personal loan is not the better product. It is the only available product. For any course that qualifies for an education loan and where you have time to process the paperwork, the education loan is structurally better on every parameter.

Does the moratorium make education loans more expensive overall?

The moratorium adds capitalized interest to the loan balance, so the total amount repaid is higher than if you started EMIs immediately. On a ₹5 lakh loan at 10.5 percent with a 2-year moratorium, the capitalized interest is roughly ₹1.05 lakh. However, the moratorium exists because you do not have income to service EMIs during studies. Comparing it to “no moratorium” is theoretical because the alternative is a personal loan at a higher rate with immediate EMIs you cannot pay. Even with capitalized interest, the education loan remains cheaper than a personal loan once 80E tax benefit is applied for any borrower in the 20 or 30 percent tax slab.

Faz · The Honest Journey · 2026