CSIS pays your full moratorium interest on education loans up to 10 lakh, but only if family income is under 4.5 lakh a year and you study in India under the IBA scheme. You apply through the Vidyalakshmi portal or your bank with an income certificate. The government pays the bank quarterly, so you never see cash. On an 8 lakh loan it can save around 3 lakh.

The CSIS scheme is one of those government programs that everyone has heard of and almost nobody understands the actual mechanics of. The branch officer mentions it during sanction. The Vidyalakshmi portal has a tickbox for it. The form your co-applicant signed had a CSIS declaration buried in page 4. And then, somewhere between disbursement and the end of the moratorium, the question becomes: did the subsidy actually get applied, or did the interest quietly capitalize anyway.

This post is the version I wish someone had written when my own co-applicant asked me to explain what the subsidy actually pays for, who actually qualifies, and what the portal trail looks like end to end. No marketing language, just the parts that matter when you are filing the claim and trying to figure out why a status is stuck.

CSIS (Central Sector Interest Subsidy) pays the full moratorium-period interest on education loans up to ₹10 lakh for students from families with annual income below ₹4.5 lakh. You apply through the Vidyalakshmi portal (or directly via your bank for non-portal loans) by submitting an income certificate from a competent authority. The government pays the bank quarterly through Canara Bank, which is the nodal bank. You do not receive cash. The subsidy reduces your capitalized balance at EMI start.

Not sure which interest subsidy is even yours? CSIS is one of four schemes people mix up, and most abroad students qualify for none. See which subsidy scheme is actually yours.

What CSIS actually is, in plain language

The Central Sector Interest Subsidy scheme was launched by the Ministry of Education in 2009 to make IBA-model education loans usable for families that could clear the loan eligibility but not the moratorium-period interest burden. The mechanics are simple. During your moratorium (course duration plus the grace period, usually 6 to 12 months after course completion), the interest accrues on your loan the way it normally would. Under CSIS, the central government pays that accrued interest to your bank instead of capitalizing it onto your principal. When your EMI starts, you begin repaying on the original sanctioned amount, not on a bloated capitalized balance.

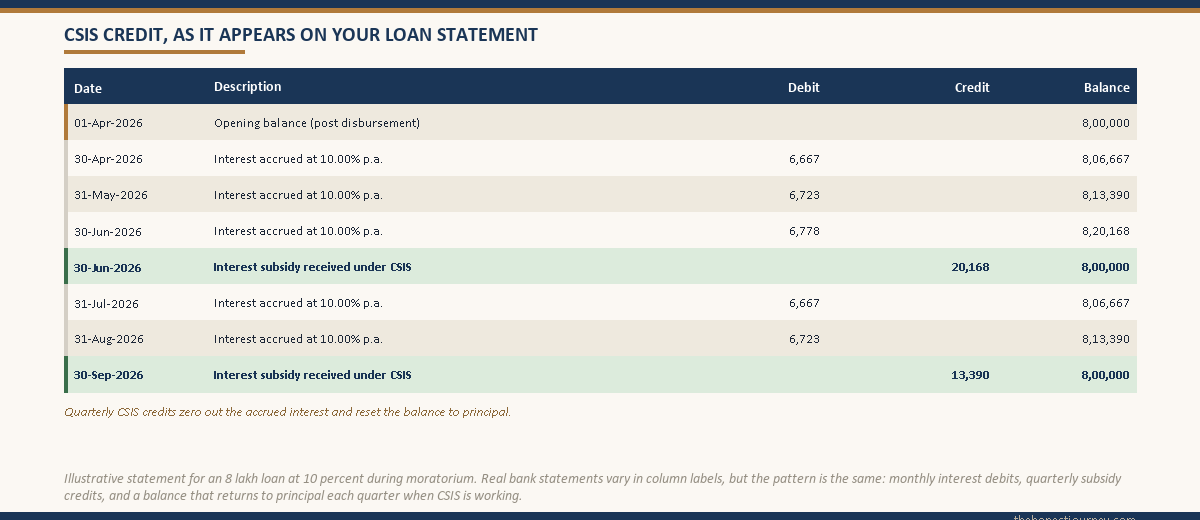

The scheme runs through Canara Bank as the nodal agency. Your lending bank uploads CSIS claims on the Canara Bank portal every quarter, the ministry releases funds, and the subsidy gets adjusted against your loan account. You will see the credit in your loan statement under a heading like “CSIS subsidy received” or “interest subvention credit.” If you never see that line item across a full year of moratorium, something has gone wrong with the claim and you need to chase it.

Who is eligible (the part most people get wrong)

Eligibility has four moving parts. All four must hold simultaneously. Miss one and the claim gets rejected.

| Criterion | Requirement |

|---|---|

| Family annual income | Up to ₹4.5 lakh (gross, from all sources, both parents combined) |

| Loan amount | Up to ₹10 lakh (subsidy capped at interest on this slab even if loan is larger) |

| Course type | Professional or technical course in India only, from a recognised institution |

| Loan scheme | Must be under the IBA Model Education Loan Scheme from a scheduled bank |

The “India only” condition is the one that surprises most applicants. CSIS does not cover abroad studies. If you are funding a master’s in Germany or the US, this scheme is not your subsidy. The equivalent for abroad studies is the Dr Ambedkar Central Sector Scheme for OBC and EBC students (covered separately on the site) or the Padho Pardesh scheme for minority communities, both with their own income ceilings and rules.

The “IBA scheme” condition is the second filter. NBFC education loans (Avanse, Credila, Auxilo and others) do not qualify, because they sit outside the IBA model framework. CSIS works for SBI, Canara, Bank of Baroda, Punjab National Bank, Union Bank, and the other public sector and major private banks that have adopted the IBA scheme. Before you sign, ask your branch officer in writing whether your sanctioned loan is “under the IBA Model Education Loan Scheme.” If the answer is yes, CSIS is in play. If they hedge, it is not.

Family income is calculated on the basis of the previous financial year. For a 2026-27 disbursement, the income certificate should cover FY 2025-26. The certificate must be issued by a competent authority designated by the state government, typically a Tahsildar, SDM, Revenue Officer, or in some states a District Magistrate’s office. A salary slip or an employer letter is not sufficient. The certificate must explicitly state gross annual family income in numbers.

Faz's rule

The eligibility cutoff is ₹4.5 lakh family income, not individual. The course must be in India. The loan must be under the IBA scheme. Miss any one and the subsidy goes to zero.

I have seen people assume their NBFC loan or their abroad master’s qualifies because their income is genuinely below the threshold. It does not. The income condition is necessary but not sufficient. Check the loan scheme classification on your sanction letter before you build a repayment plan around the subsidy.

What gets reimbursed and what does not

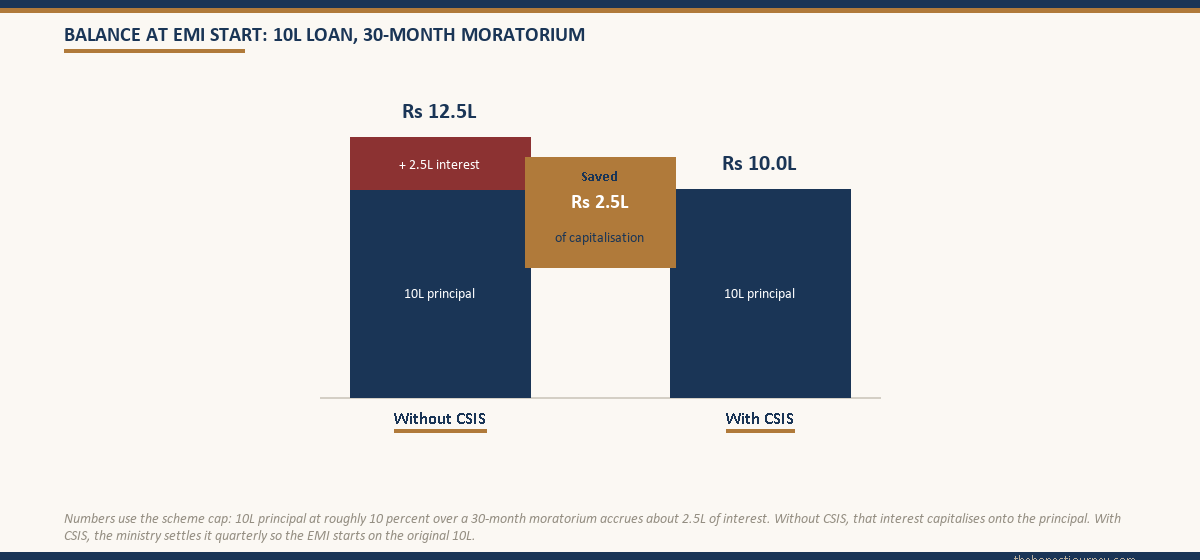

The subsidy covers the full interest accruing on the loan during the moratorium period, capped at the interest applicable to a ₹10 lakh slab. If your loan is exactly ₹10 lakh and your moratorium is 30 months at 10 percent interest, the subsidy covers roughly ₹2.5 lakh of capitalized interest. If your loan is ₹15 lakh under the same terms, the subsidy still only covers interest on ₹10 lakh. The remaining ₹5 lakh worth of principal continues to accrue interest that capitalizes onto your balance the normal way.

What CSIS does not cover, and the gaps are worth noting:

Repayment-period interest is not subsidised. Once your moratorium ends and EMIs start, you pay the full interest at the contracted rate for the full tenure. CSIS is a moratorium-only benefit. The post-moratorium math is identical whether you claimed CSIS or not, except that your starting balance is lower because capitalization was prevented.

Penal interest, processing fees, insurance premiums attached to the loan, and any charges for delayed documentation are not covered. These remain your direct responsibility regardless of CSIS status.

If you drop out, switch courses without prior bank approval, or fail to complete the course, the subsidy already credited can be reversed. Banks have the right to reclaim the subsidy amount and add it back to your outstanding balance. This is in the fine print of the CSIS agreement that your co-applicant signed during loan disbursement.

How to claim through the Vidyalakshmi portal, step by step

For loans originated through the PM Vidyalakshmi portal, the CSIS claim is integrated into the loan application flow. You do not file a separate claim. The bank initiates the subsidy request on your behalf using the income certificate you submitted with the loan application. For loans sanctioned directly at a branch (the older offline route), the process is similar but the documents are routed manually.

The end-to-end flow:

Step 1. Log in to vidyalakshmi.co.in using the credentials you created during the loan application. If you applied offline, you will not have a portal account, and your CSIS claim runs through the branch.

For portal users: under “My Applications,” select the loan application that is now sanctioned and disbursed. Open the CSIS subsidy section. You should see a section asking for family income, the income certificate upload, and a declaration. If this section is not visible, your loan was not flagged as CSIS-eligible at sanction. You will need to raise the issue with your branch.

Step 2. Upload the income certificate from the competent authority. The file should be a clear PDF or JPEG, under the file-size limit shown on the portal (usually 2 MB). The certificate must include the issuing authority’s name, designation, official seal, date of issue, and the explicit family annual income figure.

Step 3. Confirm the family income declaration. The portal will show you a self-declaration of family income that must match the certificate. The co-applicant (usually the parent) is the declared head of family for this purpose. Mismatches between the certificate and the declaration cause rejection.

Step 4. Submit and note the application reference number. The bank’s CSIS verification cell processes the claim, validates the income certificate, and either approves or rejects. Approval typically takes 30 to 60 working days. Once approved, the subsidy is part of the quarterly claim batch that the bank uploads to Canara Bank.

Step 5. Track status periodically. The Vidyalakshmi portal shows a CSIS status field under your loan application. The possible states are “submitted,” “under verification,” “approved,” “rejected,” or “claim disbursed.” For offline applications, the bank’s branch manager or CSIS desk is the only point of contact. There is no standalone CSIS portal you can log in to outside the bank’s internal systems.

Faz's rule

A CSIS application that sits in 'under verification' for more than 90 days is not normal. Escalate at the branch and ask for the verification officer's name.

The bank has internal SLAs for CSIS processing. Most branches do not chase pending claims unless the borrower flags it. If you applied at sanction and saw nothing in your loan statement after 6 months, write a formal letter (email plus physical copy at the branch) requesting a status update. Cite your loan account number and the CSIS application reference.

The reimbursement flow inside your loan account

When CSIS is approved and disbursed by the ministry, here is what you actually see in your loan statement. Canara Bank, as the nodal agency, releases the quarterly subsidy amount to your lending bank. Your lending bank credits the amount against the accrued interest on your loan account. The credit appears as a line item, typically labelled “interest subsidy received under CSIS” or similar.

You do not receive cash in hand. The subsidy adjusts the loan account directly. At the end of the moratorium, when capitalization happens, the amount that gets capitalized is the accrued interest minus the CSIS credits received. If the subsidy fully covered your moratorium interest (which it should, for an eligible loan up to ₹10 lakh), there is no capitalization. Your EMI starts on the original principal.

Worked example: ₹8 lakh loan, 10 percent interest, 30-month moratorium. Without CSIS, interest accrued is roughly ₹2 lakh, and your balance at EMI start is ₹10 lakh. With CSIS approved and credits received quarterly, the ₹2 lakh of interest is paid by the ministry, and your balance at EMI start remains ₹8 lakh. On a 10-year repayment, that drops your EMI from approximately ₹13,215 to around ₹10,572. Over the life of the loan, that is a saving of ₹3.17 lakh. That is the real value of CSIS.

Why claims get rejected and how to avoid it

From the patterns I have seen on borrower forums and from talking to a few branch officers, here are the most common rejection reasons.

Income certificate from a non-competent authority. A village panchayat letter or an employer’s salary certificate is not accepted. The certificate must come from the state-designated Revenue Officer / Tahsildar / SDM / DM office. Each state publishes a list of competent authorities. Confirm the list with your branch before paying for the certificate.

Family income above ₹4.5 lakh. This sounds obvious, but it catches families where one parent has irregular agricultural income or freelance income that they under-report on tax filings but the income certificate reflects accurately. The certificate is the authoritative document, and if it states ₹4.5 lakh and 1 rupee, the claim is rejected.

Loan amount slabbed incorrectly. If your sanctioned loan is ₹12 lakh, only ₹10 lakh worth of interest is subsidised. Branches sometimes file the claim for the full ₹12 lakh and the claim is auto-rejected. Confirm with the branch that the slab is correctly recorded.

Course or institution not on the approved list. CSIS requires that the institution be approved by a recognised regulatory body (UGC, AICTE, MCI, etc.) and that the course be a professional or technical programme. Generic arts or commerce courses at non-recognised institutions are excluded. The MyScheme portal at myscheme.gov.in lists eligibility filters that mirror the scheme guidelines.

Loan not under IBA scheme. NBFC loans, loans against property used for education, and loans from non-scheduled banks are outside CSIS. If your sanction letter does not explicitly reference the IBA Model Education Loan Scheme, the claim will not pass verification.

Delay in application. While the official guidelines do not impose a hard cutoff, in practice claims filed after the moratorium has ended become administratively difficult to process because the capitalization has already happened. File at sanction time, not at moratorium end. For a deeper look at how moratorium interest works and why the capitalization timing matters, see the moratorium-period interest post.

Faz's rule

Get the income certificate before the loan application, not after. Take it to the branch with the loan documents. CSIS is a 'paperwork at sanction' game, not a 'fix it later' game.

I have seen families try to retro-file CSIS after disbursement when they realised they qualified. Some branches will accept it. Most will tell you it should have been filed at sanction, and the verification chain becomes painful. Build the income certificate into your loan-application packet and submit them together.

How CSIS interacts with other subsidies and the PM Vidyalakshmi scheme

The PM Vidyalakshmi scheme (the 2024 cabinet-approved enhancement) introduced a separate credit guarantee and partial interest subvention for students at top-ranked institutions, with an income ceiling of ₹8 lakh per year. This is administratively distinct from CSIS. A student can potentially qualify for both schemes if they meet both sets of conditions, but the subsidies do not double up. The bank applies whichever is more beneficial, or applies them sequentially as per the scheme rules. For the broader picture of how the Vidyalakshmi portal handles subsidies, see the PM Vidyalakshmi portal post.

For OBC and EBC students studying abroad, the Dr Ambedkar Central Sector Scheme covers moratorium interest with an income ceiling of ₹8 lakh and a defined list of approved courses and countries. CSIS and the Ambedkar scheme do not overlap, because CSIS is India-only and Ambedkar is abroad-only. Several states also run their own state-level education loan and interest subsidy schemes that can stack on top of these central programmes, and the full state-by-state rundown is in the state education loan schemes in India post. Read more on the Dr Ambedkar scheme post.

For loans where the entire interest is structured to be zero for the borrower (rare, usually employer-sponsored or specific philanthropic programmes), the zero-interest education loan post covers what is real and what is not in that space.

The honest closing take

CSIS is one of the few central government schemes in this space that actually does what it says, provided you qualify and you file the paperwork correctly. The mechanics are not complicated. The eligibility is narrow but real. The savings on a ₹10 lakh loan with a 3-year moratorium can run to ₹3 lakh of avoided capitalization, which translates to a meaningfully lower EMI for the next decade.

The two failure modes are predictable. The first is assuming you qualify when you do not (NBFC loan, abroad course, family income above the threshold). The second is qualifying but never seeing the subsidy applied because the branch did not file the claim or filed it incorrectly. Both are avoidable with one habit: ask the branch in writing, at sanction time, to confirm in writing whether your loan is CSIS-eligible, who is filing the claim, and when you can expect the first quarterly credit to appear in your loan statement.

If the answer is unclear, treat it as a no. Plan your repayment math on the unsubsidised version of the loan. If the subsidy comes through, it is a windfall. If it does not, you are not surprised at EMI start.

How to check your CSIS subsidy status

There is no separate CSIS enquiry portal. To check your subsidy status, log in to the Vidyalakshmi portal and open your loan application, or ask your lending bank branch to confirm the interest subsidy claim they filed with Canara Bank, the nodal agency. The subsidy is credited straight to your loan account, never paid to you as cash, so a zero moratorium interest balance is the real confirmation it went through.

FAQ

Who is eligible for CSIS interest subsidy?

Students from families with a combined annual income of up to ₹4.5 lakh, who have taken an education loan up to ₹10 lakh under the IBA Model Education Loan Scheme from a scheduled bank, for a professional or technical course at a recognised institution in India. All four conditions (income, loan size, course type, loan scheme) must be met simultaneously. Family income is verified through an income certificate issued by a state-designated competent authority such as a Tahsildar or SDM, not by a salary slip or employer letter.

How do I apply for CSIS?

For loans originated via the Vidyalakshmi portal, the CSIS application is part of the loan flow. You upload the income certificate and confirm the family income declaration in the CSIS section of your loan application. For loans sanctioned offline at a branch, you submit the income certificate and a CSIS application form directly at the branch, which then files the claim through the bank’s internal CSIS verification cell. The bank routes approved claims to Canara Bank as the nodal agency, which disburses the subsidy quarterly to your lending bank.

What does CSIS cover?

CSIS covers the full interest accruing on your education loan during the moratorium period, capped at the interest applicable to a ₹10 lakh loan slab. The moratorium is your course duration plus the grace period of 6 to 12 months after course completion. CSIS does not cover repayment-period interest, penal interest, processing fees, insurance premiums, or any charges for delayed documentation. It also does not cover any interest accruing on loan amounts above ₹10 lakh, which continues to capitalise the normal way.

How do I check CSIS status?

For Vidyalakshmi portal applications, log in to your account, open the relevant loan application, and check the CSIS status field, which shows submitted, under verification, approved, rejected, or claim disbursed. For offline applications, your branch is the only point of contact, as there is no standalone borrower-facing CSIS portal. You can also confirm by checking your monthly or quarterly loan statement for a line item labelled “interest subsidy received under CSIS” or similar wording.

Can I claim CSIS for abroad studies?

No. CSIS covers professional and technical courses pursued in India only. For abroad studies, the comparable subsidy is the Dr Ambedkar Central Sector Scheme for OBC and EBC students (income ceiling ₹8 lakh, covers Master’s, MPhil and PhD abroad) or the Padho Pardesh scheme for students from notified minority communities. Both have their own eligibility filters and approved-course lists. Read the dedicated Dr Ambedkar scheme post for the abroad-studies subsidy mechanics.

Why was my CSIS claim rejected?

The most common rejection reasons are: income certificate from a non-competent authority such as a village panchayat or employer, family income just above the ₹4.5 lakh ceiling, loan not classified under the IBA scheme (this is the case for all NBFC loans), course or institution not approved by a recognised regulator, loan slab incorrectly recorded by the branch, or a delay in filing the claim until after the moratorium ended. Confirm each of these with your branch before refiling. Most rejections can be cured by correcting the documentation and resubmitting.

How much can CSIS actually save me?

On a ₹10 lakh education loan at 10 percent interest with a 30-month moratorium, CSIS prevents approximately ₹2.5 lakh of interest from being capitalised. Translated into EMI terms over a 10-year repayment, your monthly EMI drops from around ₹13,215 (on a capitalised balance of ₹12.5 lakh) to around ₹13,215 on the original ₹10 lakh principal. Total interest paid over the loan life reduces by roughly ₹3 lakh. The exact saving scales with your loan amount up to the ₹10 lakh cap and with your moratorium length.

Does CSIS need to be reapplied every year?

No, the CSIS claim is filed once at the start of the loan and remains valid for the entire moratorium period as long as the underlying conditions hold. The bank files quarterly claims with Canara Bank for the subsidy payout, but you do not need to refile the application or resubmit the income certificate each quarter. If your family income changes materially during the moratorium, you are expected to inform the bank, but in practice the income certificate at sanction is the document of record for the full moratorium.

Faz · The Honest Journey · 2026