A truly 0 percent interest education loan does not exist from any Indian bank, NBFC, or RBI-regulated lender, because every formal loan carries a cost of funds the bank must recover. What you see marketed as 0 percent is almost always a scholarship, a subvention scheme where someone else pays the interest, or a no-cost EMI structure that hides the charge in the principal. Always ask for the APR in writing.

Someone forwarded you a WhatsApp message, or you saw an Instagram reel, or a consultant in a glass-walled office said it across a desk: “education loan at 0 interest.” Maybe it was phrased as a government scheme. Maybe it was framed as a special tie-up only this consultancy has access to. Either way, the number that stuck in your head was zero, and now you are sitting with a loan decision that feels like it has a free option in it.

I am going to be blunt with you, because the people selling you this version of the story will not be. This post tells you exactly what is real, what is mis-sold, and what you can actually claim.

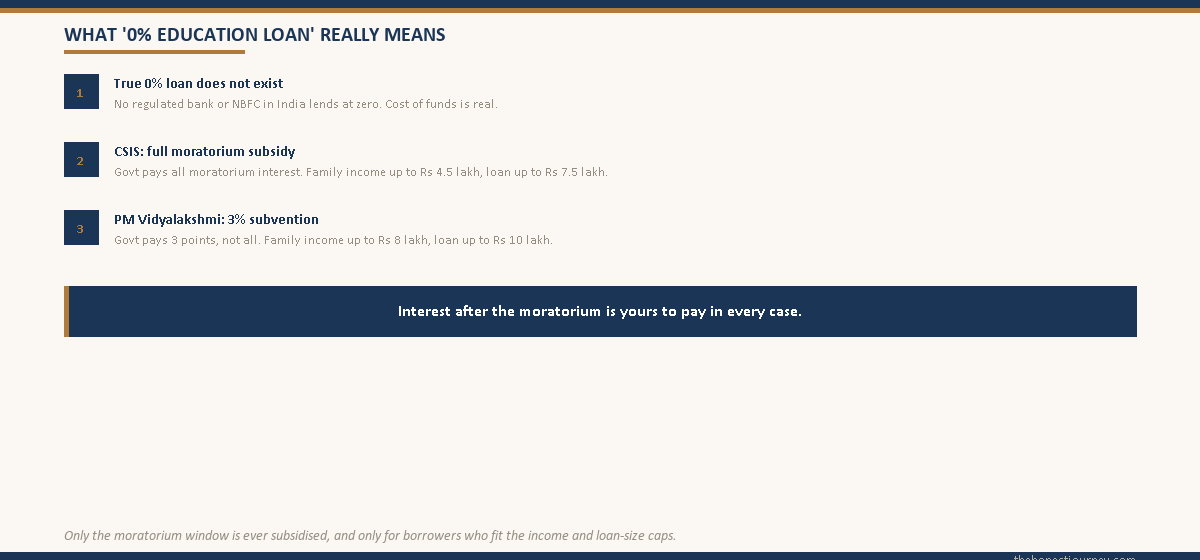

There is no genuine education loan at 0 interest from any bank or NBFC in India. What exists, and what gets repackaged as “zero interest,” is a government interest subsidy that pays your interest during a specific window if your family income is low enough. It is real money, but it is not a zero-interest loan, and most students funding studies abroad do not qualify for the full version.

For the full guide, read Education Loan in India: The Complete 2026 Guide.

Why a true 0% education loan cannot exist

Start with the obvious thing that the marketing skips. A bank does not own the money it lends you. It borrows that money itself, from depositors who expect interest on their savings, and from the wider money market. The bank’s cost of funds is real, it is measured, and it is published. RBI requires every floating-rate retail loan, education loans included, to be linked to an external benchmark, usually the repo rate, through what is called the External Benchmark Lending Rate. You can read the rationale on the RBI site.

A loan priced at 0% would mean the bank lends you money, carries the credit risk that you might not repay, runs the operational cost of servicing the account for ten years, and earns nothing for any of it. No regulated lender does that, because it cannot. So when a message says “0% interest education loan,” one of three things is true. It is a scam. It is a misunderstanding of a subsidy scheme. Or someone is quietly counting on you not asking the follow-up question.

The follow-up question is simple: who is paying the interest? Because interest on your loan always gets paid. The only thing that changes is whether you pay it or someone else does.

Faz's rule

If a loan looks like 0%, find out who is paying the interest, because someone always is.

The bank borrows the money it lends you and has a real cost of funds. A genuine 0% loan would mean the bank earns nothing for ten years of risk and servicing. That does not happen. What happens is a subsidy: the government, an employer, or a trust pays the interest in your place.

What gets mis-sold as “zero interest”: the interest subsidy

The real thing behind the myth is the government interest subsidy. India runs interest subsidy schemes for education loans, and within those schemes, for the period they cover, your effective interest cost can genuinely drop to nothing. That is where the “0%” claim comes from. It is a half-truth stretched into a slogan.

Here is the honest version. The interest still accrues on your loan every month. The bank still records it. But instead of that interest being added to your balance for you to repay later, the government pays it directly to the bank. For the covered window, you owe nothing extra. For everything outside that window, you are on a normal loan at a normal rate.

Two schemes matter here, and they are not the same thing. People mix them up constantly, including the consultants who quote them.

CSIS: the full moratorium-interest subsidy

The Central Sector Interest Subsidy scheme, CSIS, pays the entire interest that accrues during your moratorium period if your family’s annual income is up to ₹4.5 lakh. The moratorium is the window covering your course duration plus one year. If you qualify, the government covers all of that interest, you do not get any of it capitalized into your principal, and you begin repayment on the original sanctioned amount only. CSIS applies to loans up to ₹7.5 lakh for approved courses, and it was built primarily for domestic higher education. You can check the live parameters on the Vidya Lakshmi portal.

PM Vidyalakshmi: the 3% subvention

PM Vidyalakshmi is the newer scheme, and it works differently. For loans up to ₹10 lakh, students from families with annual income up to ₹8 lakh get a 3% interest subvention during the moratorium period. Note the word: subvention, not full subsidy. The government pays 3 percentage points of your interest. If your loan rate is 10.5%, you effectively carry 7.5% during the moratorium, not 0%. The scheme also offers a credit guarantee on loans up to ₹7.5 lakh, which is a separate benefit from the rate subvention. Current details sit on the the official Vidya Lakshmi portal portal and on myScheme.

So when a slogan says “zero interest,” it is usually pointing at CSIS, which can genuinely zero out your moratorium interest, but only inside a narrow income and loan-size box. It is almost never pointing at PM Vidyalakshmi, which is a partial subvention, not a free loan. And neither scheme touches the interest you pay after the moratorium ends, which is the bulk of the loan’s total cost.

The two schemes side by side

The detail that the WhatsApp forwards flatten is that these schemes differ on income limit, loan ceiling, and how much interest they actually cover. Here is the full grid.

| Feature | CSIS | PM Vidyalakshmi |

|---|---|---|

| Family annual income ceiling | Up to ₹4.5 lakh | Up to ₹8 lakh |

| Loan amount covered | Up to ₹7.5 lakh | Up to ₹10 lakh |

| Interest benefit | Full interest during moratorium | 3% interest subvention during moratorium |

| Effective rate during moratorium if you qualify | 0% for the borrower | Loan rate minus 3 percentage points |

| Interest after moratorium | Full normal rate, borrower pays | Full normal rate, borrower pays |

| Course coverage | Approved courses, India focus | Quality higher education institutions per scheme list |

Read the last two rows carefully. Neither scheme makes your loan free. CSIS, at best, makes the moratorium interest free for a small loan in a low-income household. PM Vidyalakshmi shaves 3% off the moratorium rate for a slightly larger income band. The years of repayment that follow, the part where most of the total interest actually piles up, run at the full rate in both cases. A “0% education loan” is, at most, a partially subsidised moratorium on a small loan.

Why most abroad students do not qualify for the “zero” part

This is the part the consultancy desk skips, and it is the part that matters most to the typical reader of this site.

Look at the income ceilings again. CSIS needs family income up to ₹4.5 lakh a year. PM Vidyalakshmi extends to ₹8 lakh. Now look at what it takes to actually get a loan sanctioned for studies abroad. To clear a lender’s FOIR check on a ₹25 lakh to 40 lakh abroad loan, your co-applicant, usually a parent, needs a documented income that comfortably services the projected EMI. A family that can put forward a co-applicant strong enough to pass that check almost never has a household income under ₹4.5 lakh. Often it is well above ₹8 lakh too.

Then look at the loan ceilings. CSIS covers loans up to ₹7.5 lakh. PM Vidyalakshmi covers up to ₹10 lakh. A master’s degree in the US, UK, Canada, or Australia routinely costs ₹30 lakh to 60 lakh all in. Even if your family income somehow fits the ceiling, the subsidy only ever touches the first ₹7.5 lakh or ₹10 lakh of the loan. The remaining ₹20 lakh to 50 lakh carries full interest with no subsidy at all.

So for the realistic abroad-studies borrower, the honest math is this. You will probably not qualify on income. Even if you do, the subsidy caps out at a fraction of your loan. The “0% education loan” you were sold is, for you specifically, somewhere between a small partial discount and nothing at all. I am not saying this to discourage you. I am saying it so you size your loan and your repayment plan on the real rate, not the slogan.

Faz's rule

If your family can pass a lender's income check for a ₹30 lakh abroad loan, you have probably priced yourself out of the full subsidy.

The subsidy schemes were built for low-income households and small loan amounts. The income that qualifies you for a large unsecured abroad loan is usually the same income that disqualifies you from CSIS, and often from PM Vidyalakshmi too. Plan on paying the full rate.

What actually lowers your interest cost

If a true 0% loan is off the table, the useful question becomes: what genuinely reduces what you pay? There are real levers here, and none of them involve a slogan.

A collateral-secured loan from a public sector bank. This is the single biggest rate lever for most people. Secured loans against property or an FD from public sector banks tend to price around 8-10%, while unsecured loans from NBFCs sit closer to 11-14%. On a ₹20 lakh loan over ten years, a 2 to 3 percentage point gap is several lakh in total interest. If you are weighing options, the education loan interest rate comparison lays out where each lender category lands.

Servicing simple interest during the moratorium. If you, your family, or a part-time job can cover even the monthly interest while you study, you prevent that interest from being capitalised into your principal. This is not a rate cut, but it removes interest-on-interest, and the saving over a full tenure is large. The mechanics are walked through in the education loan moratorium period and interest post.

Section 80E tax deduction. The interest paid on an education loan qualifies for a deduction under Section 80E of the Income Tax Act, with no upper cap on the amount, for up to eight years from when repayment starts. If your co-applicant is on the old tax regime, this lowers the real, after-tax cost of the loan. It is not 0%, but it is a genuine reduction the schemes do not advertise.

Scholarships and grants. A scholarship reduces the amount you need to borrow at all, which beats any interest scheme, because the cheapest interest is on money you never borrowed. Many Indian students underuse this route. The scholarships for Indian students after 12th post covers where to actually look.

Employer sponsorship and family loans. Some employers fund further study in exchange for a service bond. A loan from family, structured honestly and ideally documented, can genuinely be interest-free, because your family chooses to charge you nothing. That is the only real “0% loan” most people will ever see, and it is not a bank product. Just be clear-eyed that a service bond is a commitment, and an informal family loan still has to be repaid.

How to spot the mis-selling

You will keep running into the “0% interest” claim, so here is how to test it on the spot. None of these checks take more than a minute.

Ask who pays the interest. A legitimate person will say “the government, through CSIS or PM Vidyalakshmi, during the moratorium, if you qualify.” A mis-seller will get vague, pivot to “special tie-up,” or push you to sign quickly.

Ask for the scheme name and the official portal. Real schemes have names, eligibility rules, and government websites. CSIS and PM Vidyalakshmi are on the Ministry of Education site, on Vidya Lakshmi, and on myScheme. If the answer is a private consultancy’s brand name and no government source, that is the answer.

Ask whether the “0%” applies after the moratorium. It never does, under any scheme. If someone implies your entire ten-year loan is interest-free, they are either confused or lying. Walk away from a consultancy that lets that impression stand to close a sale.

Watch for an upfront fee. A genuine subsidy never requires you to pay a private agent a “processing fee” or “scheme registration fee” to access it. You apply for these schemes through your lending bank and the Vidya Lakshmi portal directly. Any demand for cash to “unlock” a 0% loan is a scam, full stop.

The honest closing take

I understand the appeal of the phrase. Studying abroad is frightening on the money side, and “0% interest” sounds like a door out of that fear. But a slogan that sounds like a way out is usually a way in, into a loan you understood worse than you thought.

Here is what is true. No regulated lender in India offers a genuine 0% education loan. The government does run interest subsidy schemes, CSIS and PM Vidyalakshmi, and for borrowers who qualify, they can cut or even zero out the interest during the moratorium only. Most students funding a degree abroad will not qualify for the full benefit, because their family income is too high or their loan is too large for the scheme caps, and even when they do qualify, the subsidy touches only a slice of the total borrowing.

So plan on the real rate. Size your loan against the EMI you will actually face after the moratorium, not against a discount you may never receive. Check the schemes properly through the official portals, because if you do qualify, the benefit is worth claiming, and the PM Vidyalakshmi portal guide walks through the application. But build your decision on the assumption that you are paying full interest, and treat any subsidy as a bonus, not a foundation.

If the only reason a loan feels affordable is a 0% claim someone made verbally, you do not yet have an affordable loan. You have a decision still to make, and it is yours to make with the real numbers in front of you.

FAQ

Is there a 0% interest education loan in India?

No. No bank or NBFC in India offers a genuine 0% interest education loan, because every lender has a real cost of funds and is required by RBI to price floating-rate loans against an external benchmark. What exists is a government interest subsidy that can pay your interest during the moratorium period if you meet income and loan-size limits. That is a subsidy on a normal loan, not a zero-interest product.

Does the government give interest-free education loans?

The government does not give interest-free loans. It runs interest subsidy schemes. Under CSIS, for families earning up to ₹4.5 lakh a year, the government pays the full interest during the moratorium on loans up to ₹7.5 lakh, so for that window your cost is effectively nil. After the moratorium, you pay the full rate. The loan itself is a normal bank loan with a normal interest rate throughout.

Is PM Vidyalakshmi a zero-interest loan?

No. PM Vidyalakshmi is a portal and a scheme that offers a 3% interest subvention during the moratorium for loans up to ₹10 lakh, for families with annual income up to ₹8 lakh. A 3% subvention means the government covers three percentage points of your interest, not all of it. If your loan rate is 10.5%, you effectively carry 7.5% during the moratorium. It is a partial discount, not a free loan.

What is the CSIS interest subsidy?

CSIS, the Central Sector Interest Subsidy scheme, pays the entire interest that accrues during your moratorium period if your family’s annual income is up to ₹4.5 lakh. It applies to education loans up to ₹7.5 lakh for approved courses and was designed mainly for domestic higher education. For eligible borrowers, no moratorium interest gets capitalised, and repayment begins on the original sanctioned amount. Interest after the moratorium is paid by the borrower at the normal rate.

Which bank has the lowest education loan interest rate?

There is no single permanent answer, but the pattern is consistent. Public sector banks offering collateral-secured loans tend to price lowest, often around 8-10%, because the pledged security reduces their risk. Unsecured loans from NBFCs sit higher, typically 11-14%. Rates move with the repo rate and depend on your collateral, course, and co-applicant profile. Compare current rates across lender categories before you commit rather than relying on any one name.

Can I get an education loan without interest?

Not from a bank or NBFC. The closest thing to a genuinely interest-free loan is one from your own family, where they choose to charge you nothing, or an employer-sponsored study program tied to a service bond. Government schemes can subsidise interest during the moratorium for eligible low-income borrowers, but the loan still carries interest, and you pay it in full after the moratorium ends.

Do students going abroad qualify for the interest subsidy?

Usually not for the full benefit. The income ceilings, ₹4.5 lakh for CSIS and ₹8 lakh for PM Vidyalakshmi, are low relative to what it takes to get a large abroad loan sanctioned. The loan caps, ₹7.5 lakh and ₹10 lakh, are far below typical abroad tuition. Even an eligible student sees the subsidy applied only to a small slice of a much larger loan. Check the official portals, but plan on paying the full rate.

How can I tell if a 0% education loan offer is a scam?

Ask who pays the interest and demand a specific government scheme name with an official portal link. Real schemes are listed on the Ministry of Education site, Vidya Lakshmi, and myScheme. Be very wary if someone claims the whole loan is interest-free, stays vague about a “special tie-up,” or asks for an upfront cash fee to unlock the offer. Genuine subsidies are applied through your bank and the official portal, never through a paid private agent.

Faz · The Honest Journey · 2026